Ophthalmic Clinical Trials Market Report Scope & Overview:

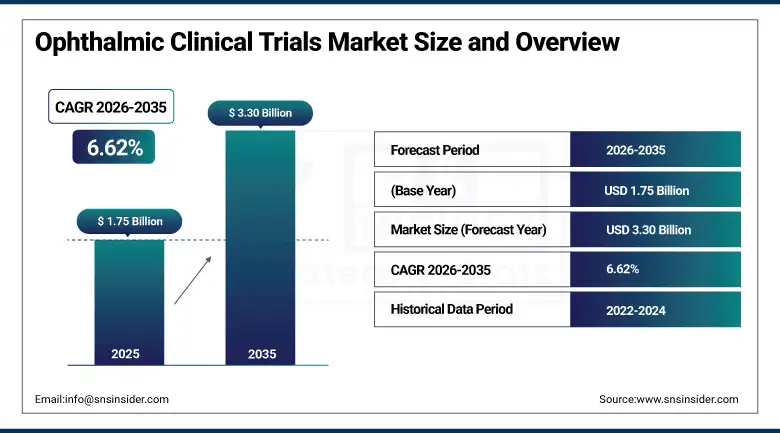

The Ophthalmic Clinical Trials Market was valued at USD 1.75 Billion in 2025 and is expected to reach USD 3.30 Billion by 2035, growing at a CAGR of 6.62% from 2026–2035.

The global ophthalmic clinical trials market is experiencing robust growth driven by rising prevalence of ocular diseases including macular degeneration, glaucoma, dry eye disease, and diabetic retinopathy. Ophthalmic clinical trials encompass the complete clinical development continuum from Phase I safety studies through Phase III efficacy pivotal trials for ophthalmic drugs, biologics, gene therapies, devices, and combination products targeting vision-threatening conditions across the growing global population of ocular disease patients. The ageing global population whose visual impairment burden grows with longevity, combined with the gene therapy revolution creating curative treatment programmes for inherited retinal dystrophies, represents the most commercially transformative development driving the market’s expansion.

In 2024, Apellis Pharmaceuticals advanced its pegcetacoplan intravitreal injection programme in a Phase III extension study evaluating long-term efficacy and safety in geographic atrophy secondary to dry AMD. The programme demonstrates the commercial momentum of complement pathway inhibition as a therapeutic approach in geographic atrophy whose unmet medical need in 8 million U.S. patients creates structured Phase III investment motivation from pharmaceutical companies seeking the first approved treatment for this debilitating late-stage AMD complication.

Market Size and Forecast

-

Market Size in 2026E: USD 1.87 Billion

-

Market Size by 2035: USD 3.30 Billion

-

CAGR: 6.62% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Ophthalmic Clinical Trials Market - Request Free Sample Report

Ophthalmic Clinical Trials Market Trends

-

Gene therapy ophthalmic trials are expanding rapidly for inherited retinal disorders, attracting high-value investments for potential one-time curative treatments.

-

Next-generation anti-VEGF therapies, including biosimilars and sustained-release systems, are driving strong Phase II and III ophthalmic trial activity.

-

Decentralized ophthalmic trials are increasing using teleophthalmology, wearable monitoring, and remote visual acuity assessments for patient convenience.

-

AI-based retinal imaging analysis is improving biomarker detection and treatment response evaluation in ophthalmic clinical trials.

-

Dry eye disease trials are growing due to high prevalence and unmet therapeutic demand beyond existing standard treatments.

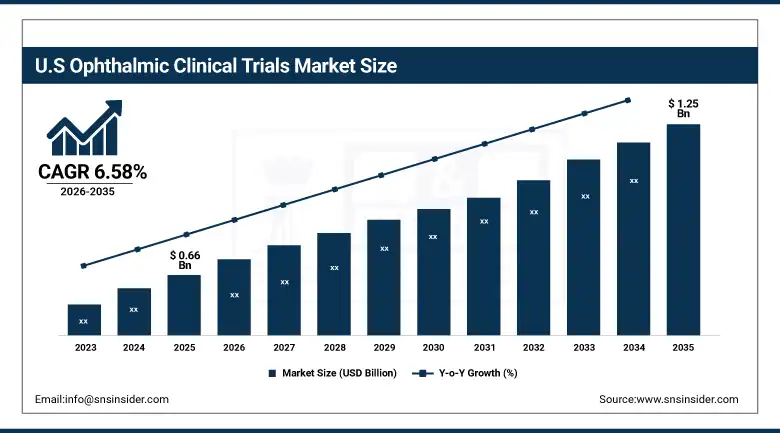

The U.S. Ophthalmic Clinical Trials Market Outlook

The U.S. Ophthalmic Clinical Trials Market was valued at approximately USD 0.66 Billion in 2025 and is expected to reach approximately USD 1.25 Billion by 2035, growing at a CAGR of approximately 6.58%.

The U.S. is the world’s most commercially significant ophthalmic clinical trials market within North America’s dominant revenue position. Regeneron Pharmaceuticals, Novartis, Roche/Genentech, Apellis Pharmaceuticals, Allergan (AbbVie), and REGENXBIO collectively define the domestic ophthalmic clinical development commercial landscape. The FDA’s Ophthalmology Division’s accelerated approval pathway for serious ophthalmic conditions, the Breakthrough Therapy designation available for innovative ocular treatments, and the NEI’s research funding infrastructure create the world’s most favorable ophthalmic drug development regulatory environment. The glaucoma, AMD, and diabetic retinopathy patient populations concentrated in the ageing U.S. demographic create the most commercially concentrated ophthalmic clinical trial recruitment environment globally.

In 2025, Regeneron received FDA approval for aflibercept 8 mg high-dose formulation under the brand name Eylea HD for neovascular AMD and diabetic macular edema, demonstrating the commercial momentum of extended-duration anti-VEGF programme development whose 12–16-week dosing interval substantially reduces injection burden relative to 4-8 week alternative regimens. The approval creates structured market opportunity for biosimilar and next-generation anti-VEGF trial programmes targeting the extended-duration specification demonstrated by Eylea HD’s clinical success.

Ophthalmic Clinical Trials Market Segment Analysis

-

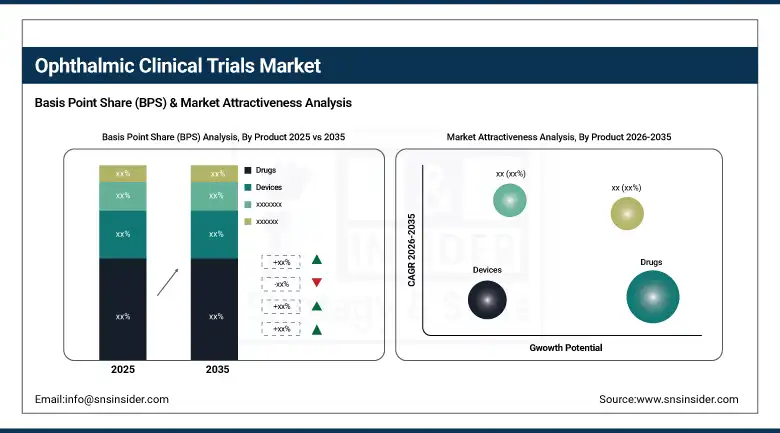

By Product, the drugs segment dominated the ophthalmic clinical trials market with approximately 58% share in 2025, while the devices segment is the fastest growing.

-

By Indication, the macular degeneration segment dominated the ophthalmic clinical trials market with approximately 28% share in 2025, while the dry eye disease segment is the fastest growing.

-

By Phase, the clinical phase segment dominated the ophthalmic clinical trials market with approximately 72% share in 2025, while the preclinical phase is the fastest growing.

-

By Sponsor Type, the pharmaceutical/biopharmaceutical companies segment dominated the ophthalmic clinical trials market with approximately 68% share in 2025, while the medical device companies segment is the fastest growing.

By Product, drugs segment dominates, devices segment grows fastest

The drugs segment held the largest share of the ophthalmic clinical trials market in 2025 due to extensive development of novel therapeutics across major disease areas such as age-related macular degeneration, diabetic retinopathy, glaucoma, and dry eye disease. Strong pipeline activity in anti-VEGF therapies, gene therapies, corticosteroids, and immunomodulatory drugs continues to drive clinical trial investments. Pharmaceutical companies dominate trial sponsorship due to high commercial potential and unmet clinical needs, particularly in chronic and vision-threatening retinal disorders requiring long-term treatment solutions.

The devices segment is the fastest-growing area in the ophthalmic clinical trials market due to rapid innovation in diagnostic and therapeutic ophthalmic technologies. Growth is driven by increasing adoption of advanced imaging systems, intraocular pressure monitoring devices, surgical tools, and drug delivery implants such as sustained-release ocular systems. Integration of AI-enabled diagnostic devices and minimally invasive surgical technologies is further accelerating clinical evaluation activity. Rising demand for precision ophthalmic care and technology-driven treatment monitoring is expanding device-based clinical trial programs globally.

By Indication, macular degeneration dominates, dry eye grows fastest

Macular degeneration retained the dominant indication position with approximately 28% of the ophthalmic clinical trials market in 2025. The AMD indication’s commercial dominance reflects the extraordinary per-programme investment of late-stage anti-VEGF, complement inhibitor, and gene therapy clinical programmes whose pivotal Phase III trial costs for large patient populations create per-indication trial expenditure exceeding any other ophthalmic condition. Regeneron’s aflibercept, Novartis’s ranibizumab biosimilar programme, Roche/Genentech’s faricimab Phase III and Phase IV programmes, and Apellis’s pegcetacoplan geographic atrophy programme collectively create the most commercially concentrated single-indication ophthalmic trial investment. The 200 million global AMD patients creating extraordinary patient population for trial recruitment sustains AMD’s indication leadership.

Dry eye disease is the fastest-growing indication because the large chronic patient population whose DED prevalence estimates range from 5-50% of adults globally creates commercial pharmaceutical development motivation for next-generation treatments beyond the established cyclosporine and lifitegrast market. Each novel DED mechanism programme creates Phase II trial investment whose commercial DED indication motivation compounds with multiple programmes advancing simultaneously. The DED market’s chronic treatment paradigm whose continuous prescription creates above-average per-patient commercial lifetime value sustains pharmaceutical development investment beyond the acute treatment economics of infectious eye disease.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Ophthalmic Clinical Trials Market Insights

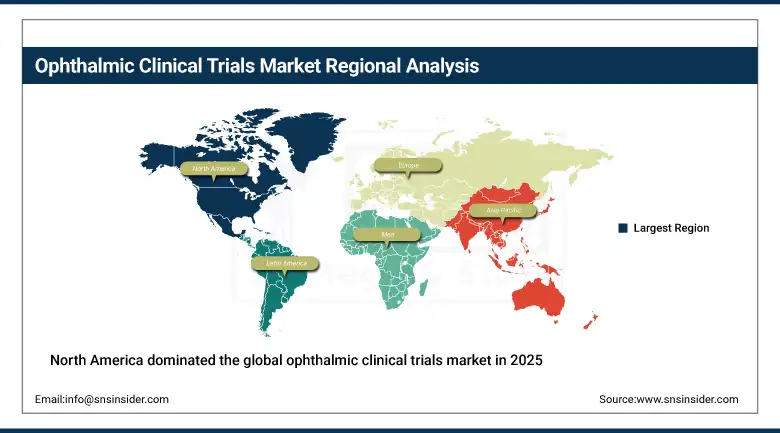

North America dominated the global ophthalmic clinical trials market in 2025, driven by the highest concentration of ophthalmic drug development programmes, advanced clinical research infrastructure, and favorable FDA regulatory environment. The United States accounts for approximately 87.4% of North American revenues through Regeneron, Novartis US, Roche/Genentech, and Apellis Pharmaceuticals’ commercial clinical programmes.

Canada contributes approximately 12.6% of North American revenues through academic ophthalmic research at University Health Network and Montreal Neurological Institute, the growing domestic biotech sector’s ophthalmic programme development, and clinical site participation in multinational ophthalmic trials.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Ophthalmic Clinical Trials Market Insights

Europe is a sophisticated ophthalmic clinical trials market where the EMA’s ophthalmic product regulatory framework, Moorfields Eye Hospital’s clinical research leadership, and the established European ophthalmic biotech ecosystem create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through Bayer AG’s aflibercept programme, the University Eye Hospitals’ clinical trial participation, and the retinal specialist community’s trial recruitment infrastructure.

The United Kingdom, Switzerland, and the Netherlands are significant secondary markets where UCB Pharma’s ophthalmic programmes, Alcon’s Swiss headquarters device trials, and Novartis’ Basel-based ophthalmic clinical operations create consistent commercial demand.

Asia Pacific Ophthalmic Clinical Trials Market Insights

Asia Pacific is the fastest-growing regional ophthalmic clinical trials market, driven by the world’s largest myopia patient population in East Asia, China’s growing domestic pharmaceutical development, Japan’s advanced ophthalmic clinical research infrastructure, and India’s cost-competitive clinical trial site environment. China accounts for approximately 44.8% of Asia Pacific revenues through its growing domestic ophthalmic drug development, the ageing population’s AMD and glaucoma burden, and multinational sponsor’s China regulatory submission requirement creating domestic trial investment.

Japan and South Korea represent technically sophisticated secondary markets where the domestic pharmaceutical companies’ ophthalmic pipeline, the specialist ophthalmologist community’s clinical trial participation, and the regulatory submission pathway create consistent ophthalmic trial commercial demand.

MEA & Latin America Ophthalmic Clinical Trials Market Insights

Israel leads MEA revenues at approximately 38.4% through its advanced life sciences ecosystem, Hadassah Medical Centre’s ophthalmic research leadership, and the domestic biotech sector’s retinal and corneal disease therapeutic development creating above-average MEA commercial concentration.

Brazil leads Latin American revenues at approximately 44.2% through its large ophthalmic patient population, Federal University ophthalmology department clinical trial participation, and the growing domestic pharmaceutical sector’s regulatory submission infrastructure. Saudi Arabia’s Vision 2030 healthcare investment and South Africa’s academic eye hospital network collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Ageing population visual disease burden and gene therapy pipeline creating above-average trial investment

The ageing global population’s visual impairment burden is the ophthalmic clinical trials market’s most commercially certain structural growth driver. WHO’s estimate of 2.2 billion people with vision impairment globally, whose prevalence increases dramatically above age 60, creates an expanding patient population whose AMD, glaucoma, and cataract burden creates structured pharmaceutical development motivation. Each demographic cohort entering the peak vision impairment age creates new trial participant availability that sustains the ophthalmic clinical trial’s patient recruitment economics across the forecast period.

Gene therapy pipeline expansion for inherited retinal dystrophies represents the most commercially transformative near-term market development whose single-administration curative treatment concept creates per-programme Phase III investment substantially exceeding conventional small molecule ophthalmic drug development economics. Each IRD gene therapy programme that advances through Phase I/II toward pivotal Phase III creates trial infrastructure investment whose per-patient cost, reflecting gene vector manufacturing, specialized administration, and long-term safety follow-up, exceeds conventional ophthalmic drug trial economics.

Restraints: High ophthalmic trial cost and patient recruitment complexity

Ophthalmic clinical trials’ above-average per-patient cost reflects the specialized ophthalmology equipment required for visual acuity measurement, optical coherence tomography imaging, fluorescein angiography, and intraocular pressure assessment at each trial visit whose combined equipment and specialist personnel cost creates higher site overhead than general medicine trial comparators. Each Phase III ophthalmic trial whose primary endpoint requires graded retinal imaging at multiple time points creates per-patient data collection costs that substantially exceed equivalent pharmaceutical trial economics in less equipment-intensive therapeutic areas.

Patient recruitment complexity for rare ophthalmic conditions including inherited retinal dystrophies, uveitis, and severe glaucoma creates enrolment challenges whose small eligible patient population requires international multi-site trial designs whose coordination complexity creates above-commodity trial management investment.

Opportunities: Gene therapy trials and decentralized ophthalmic trial models

Gene therapy ophthalmic trial investment represents the most commercially premium emerging trial category whose curative treatment potential, rare disease orphan designation economics, and premium pricing justification create above-average pharmaceutical development investment motivation. Each new IRD gene therapy programme advancing through Phase I/II creates structured Phase III investment that compounds with the growing identified IRD patient population from whole genome sequencing programme expansion.

Decentralized ophthalmic trial adoption represents the most commercially accessible near-term innovation whose remote visual assessment, patient-reported outcome digitization, and teleophthalmology consultation reduce site visit burden that conventional protocol requirements create for patients with vision impairment and mobility limitations.

Recent Developments:

-

2026: Novartis AG accelerated clinical evaluation of advanced retinal disease therapies, including combination biologic approaches aimed at improving long-term vision preservation outcomes.

-

2025: Regeneron Pharmaceuticals Inc. expanded late-stage ophthalmic trials for next-generation anti-VEGF therapies, focusing on longer durability dosing regimens for retinal disease treatment.

-

2025: REGENXBIO Inc. advanced its gene therapy clinical pipeline for inherited retinal disorders, strengthening programs targeting rare vision loss conditions with single-dose treatment approaches.

-

2025: Regeneron received FDA approval for aflibercept 8 mg high-dose (Eylea HD) for neovascular AMD and DME, validating the extended-duration anti-VEGF clinical programme strategy and creating commercial motivation for competitive extended-duration programme development.

Ophthalmic Clinical Trials Market key players are:

-

Regeneron Pharmaceuticals Inc.

-

Novartis AG

-

Roche/Genentech Inc.

-

AbbVie

-

Apellis Pharmaceuticals Inc.

-

REGENXBIO Inc.

-

Alcon Inc.

-

Bayer AG

-

Bausch + Lomb Corporation

-

Johnson & Johnson Vision Care Inc.

-

Roche/Genentech Inc.

-

MeiraGTx Holdings plc

-

4D Molecular Therapeutics

-

ProQR Therapeutics

-

Astellas Pharma Inc.

-

Santen Pharmaceutical Co. Ltd.

-

Sun Pharmaceutical Industries Ltd.

-

Ocugen Inc.

-

Kala Bio (Kala Pharmaceuticals)

-

Iridex Corporation

Ophthalmic Clinical Trials Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.75 Billion |

| Market Size by 2035 | USD 3.30 Billion |

| CAGR | CAGR of 6.62% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Devices: Surgical & Diagnostic Devices, Vision Care Devices; Drugs: OTC Drugs, Prescription Drugs) • By Indication (Macular Degeneration, Glaucoma, Dry Eye Disease, Retinopathy, Uveitis, Macular Edema, Blepharitis, Cataract, Optic Neuropathy, Others) • By Phase (Discovery Phase, Preclinical Phase, Clinical Phase) • By Sponsor Type (Pharmaceutical/Biopharmaceutical Companies, Medical Device Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Regeneron Pharmaceuticals Inc., Novartis AG, Roche/Genentech Inc., AbbVie, Apellis Pharmaceuticals Inc., REGENXBIO Inc., Alcon Inc., Bayer AG, Bausch + Lomb Corporation, Johnson & Johnson Vision Care Inc., MeiraGTx Holdings plc, 4D Molecular Therapeutics, ProQR Therapeutics, Astellas Pharma Inc., Santen Pharmaceutical Co. Ltd., Sun Pharmaceutical Industries Ltd., Ocugen Inc., Kala Bio (Kala Pharmaceuticals), Iridex Corporation |

Frequently Asked Questions

The market is expected to grow at a CAGR of 6.62% from 2026 to 2035.

The Ophthalmic Clinical Trials Market was valued at USD 1.75 Billion in 2025.

Rising global prevalence of age-related macular degeneration, glaucoma, and inherited retinal dystrophies creating pharmaceutical development investment.

Macular Degeneration dominated the market with approximately 28% share in 2025.

North America dominated the Ophthalmic Clinical Trials Market in 2025.

Get in Touch