Optical Film Market Report Scope & Overview:

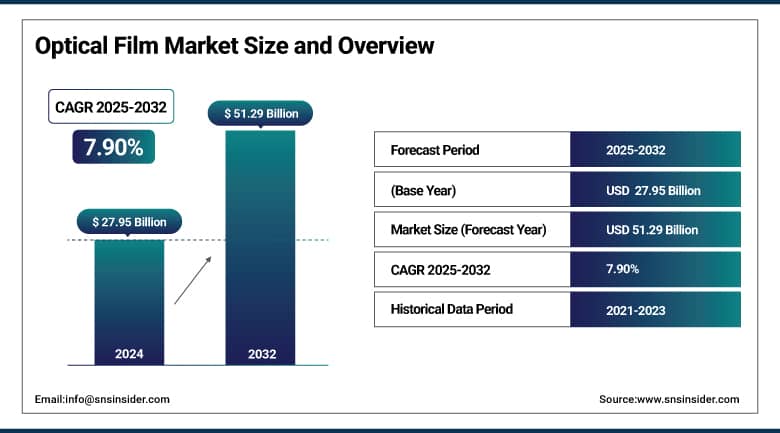

The Optical Film Market size was valued at USD 27.95 billion in 2024 and is expected to reach USD 51.29 billion by 2032, growing at a CAGR of 7.90% over the forecast period of 2025-2032.

The optical films market is growing at a fast pace as the demand for high-resolution, energy-efficient screens in smartphones, tablets, and automotive displays is increasing. The application of optical films has been further expanded with an increase in demand for functional films, such as anti-reflective and polarizer films, and new devices, including OLED and foldable. Market trends of optical film indicate rapid growth in automotive HUDs and digital dashboards. Companies including 3M make multi-layer optical films with up to 71% solar IR rejection and 76% reduction in glare. Optical film companies focus on R&D, particularly in the polarizer film market and the functional films market.

According to Nitto Denko’s FY2024 integrated report, the information fine materials segment, totaling USD 2456.65 million, recorded 52.7% of its revenue from optical film products. This further highlights the significance of optical film market size, optical film market analysis, optical film market share, and optical film market growth in product development, strategic decision making, and product development in the optical film market.

To Get More Information On Optical Film Market - Request Free Sample Report

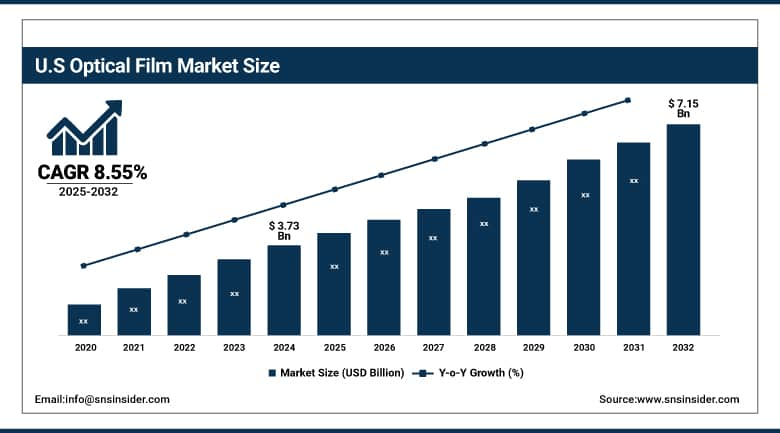

North America is the second dominating region in the optical film market in 2024, holding a market share of 20.2% and is the fastest growing region with a CAGR of 8.55%. This growth is predominantly attributed to the increasing adoption of advanced display technologies in the automotive and consumer electronics industries. The U.S. is the highest valued sub-market in North America, valued at USD 3.73 billion in 2024 and anticipated to reach USD 7.15 billion by 2032 holding approximately 66% of market share with policies and programs backing the use of energy-efficient displays along with investments by optical films companies such as 3M and Nitto Denko. Rising need for ergonomic high-performance polarizer film, market and functional films market applications such as smartphones and automotive head-up displays, boosts the market growth and trends in the optical film market in this region.

Market Dynamics:

Drivers:

-

Rapid Adoption of Foldable Displays Demands Advanced Optical Films for Enhanced Durability

The growing popularity of foldable smartphones and OLED displays is among the other factors driving the demand in the optical film market. These devices need tough polarizer films and functional films to ensure durability performance under bending. Nitto Denko predicted that demand for such films would rise sharply in its 2024 report. 3M also spent USD 250 million on increasing multilayer optical film capacity. Advanced technologies, help a company retain its share in the optical film market and also contribute to the growth of the global optical film market for flexible display applications. This is fueling the polarizer film market and functional films market globally.

-

Rising automotive heads-up display adoption drives the need for high-performance films

The use of optical film in automotive displays is increasing with the increasing penetration of digital dashboards and heads-up displays. According to the U.S. Department of Energy, HUD penetration rose from 22% in 2021 to 38% in 2023. For such displays, functional films of a low reflection and high clarity are required. Nitto Denko released earlier this year new polarizer films designed for automotive applications in extreme temperature environments. Such films serve an important function for the safety and visibility aspects of vehicles. This trend is expected to reinforce the growth of the optical film market and broaden the role of the functional films market in automotive technology.

Restraints:

-

Limited Recycling Infrastructure Hinders Circular Economy Potential in Optical Films

The optical film market is restricted by low recovery rates of multilayer polymer films. In 2023, the U.S. EPA demonstrated less than 30% recycling of PET-type optical films. Films are complex, and the separation of film and processing is difficult, thus increasing the 20% cost for disposal. Without a robust infrastructure in place, these market segments for functional films cannot migrate to circular production models. This means that the optical film companies have no choice but to depend on virgin raw materials, which have substantial environmental effects. This puts market share for optical films at risk and flies in the face of sustainability targets for consumer electronics and packaging.

Segmentation Analysis:

By Film Type

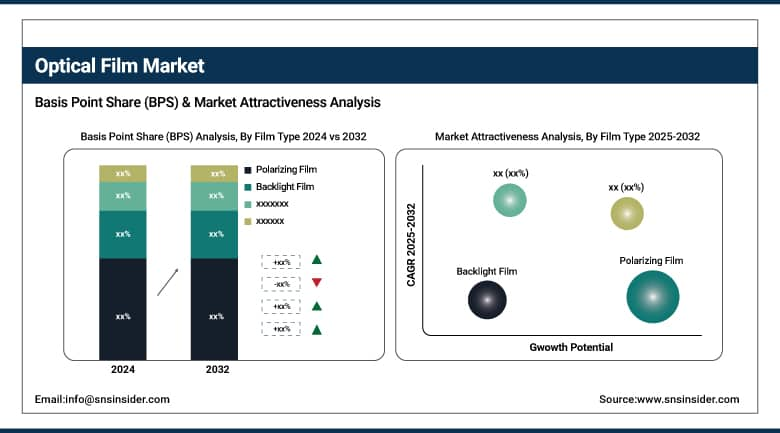

In 2024, polarizing film dominated and held a 46.5% share of the optical film market, as its use has increased in high-resolution LCD and OLED displays. This subsegment of linear polarizers emerged as the leading one due to its wide adoption in smartphones, laptops, and automotive displays. One of the leading optical film companies, Nitto Denko, has reported a strong increase in sales of linear polarizers, driven by Asian display makers. Such films improve screen readability and brightness capability. Consumer perception toward the premium flexible electronics is rising, leading to increased polarizer film market penetration, increased optical film market share, and even further influx of domination in different device varieties.

Backlight films are the fastest growing segment during the forecast period of 2025-2032, with a CAGR of 8.32%, fueled by the demand for thin and energy-saving LED displays for TVs, monitors, and automotive panels. Therefore, brightness enhancement films (BEF) are prevailing as they increase luminance and reduce power consumption. 3M's global BEF volume shipments rose 22%, driven by adoption among OEMs moving to thinner and eco-friendly displays. The functional films market in applications, such as these benefits, as global energy standards become more stringent. Advances in light control and optical clarity are driving their use case expansion and aligning with broader optical film market trends in consumer and industrial electrical devices.

By Application

Smartphones and tablets dominated and accounted for 33.8% of the optical film market in 2024, driven by new OLED and foldable screen applications. Polarizing and functional films are required to increase contrast, color saturation, and battery life. OLED smartphone display shipments from Samsung Display were up 18% YoY, due to increases in shipments to North American and Asian markets. The segment is benefiting from ongoing short upgrade cycles and rising global smartphone penetration. Work on market applications continues for functional films with every new device, continuing to keep this a dominant segment. These conditions indicate significant growth in the optical film market, and highlight the significance of the market in the global analysis.

Automotive display is the fastest growing application segment in the forecast period of 2025-2032 with a CAGR of 8.81%, due to the growing digitalization of vehicles. Polarizing and backlight substrates are broadly employed in HUDs, center stacks, and instrument clusters. The U.S. Department of Energy found the use of HUD in the passenger car jumped from 22% in 2021 to 38% in 2023. The move to connected and electric cars demands high-visibility and low-reflection films that perform in harsh temperatures. Degradation of the light-diffusing effect in the film types shifting to a new technology, such as from the optical film to the OC film is becoming a major issue, so there is a growing need to offer new solutions, and optics in automotive is a major growth driver in the analysis of optical film market and future investment planning.

Regional Analysis:

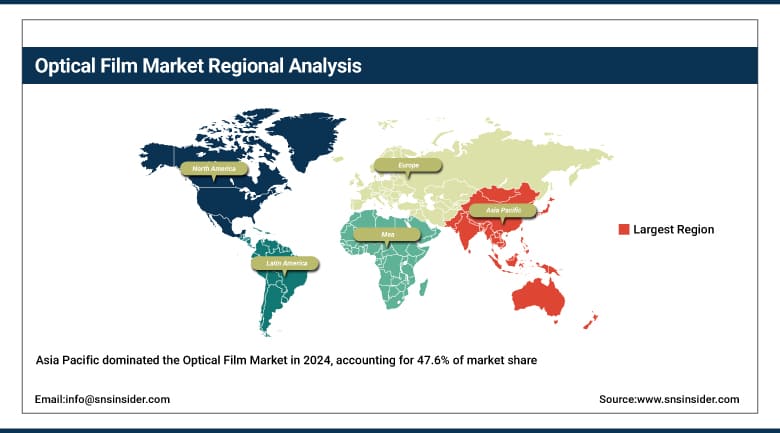

Asia Pacific dominates the optical film market in 2024, commanding a substantial 47.6% market share, due to high consumption of consumer electronics in China, South Korea, and Japan. Furthermore, the dominance of the region is attributed to the presence of leading optical film companies, including LG Chem and Samsung SDI, which innovate the polarizer film market and the functional films market. Quick urbanization and the growing production of smartphones and automotive displays also bolster the development of the optical film market. Government policies promoting export-oriented electronics manufacturing and investments in new display technologies make Asia Pacific the dominant market in optical film applications.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe ranks third in the optical film market with a significant 17.4% market share on account of the rising demand for energy-efficient display technologies in Germany, France, and the U.K. The region’s emphasis on eco-friendly electronics and central government support for green manufacturing propels the optical film industry's growth. Companies including Toray and Mitsubishi Chemical are increasing their operations here, taking advantage of growing demand in the polarizer film market. Strong R&D in Europe's functional films market applications is stimulating the growth of the optical film market analysis, which is witnessing momentum from shifting consumer preference and renewed focus on stricter environmental compliance.

Key Players:

-

3M

-

LG Chem, Ltd.

-

Toray Industries, Inc.

-

Mitsubishi Chemical Corporation

-

Sumitomo Chemical Co., Ltd.

-

Kolon Industries, Inc.

-

Teijin Limited

-

Hyosung Chemical

-

BenQ Materials Corporation.

Recent Developments:

-

In October 2024 - Mitsubishi Chemical, expanded its optical film production facility for polarizing plates to meet rising display industry demand, boosting manufacturing capacity and strengthening its position in the global optical film market.

-

In October 2024 - Korea University, developed a high-efficiency optical film technology to enhance display clarity and energy efficiency, gaining interest from major display manufacturers for use in smartphones and televisions.

-

In June 2023 - Dai Nippon Printing, launched a durable, high-performance polarizing film aimed at the automotive and consumer electronics sectors to address growing demand for advanced optical films.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 27.95 billion |

| Market Size by 2032 | USD 51.29 billion |

| CAGR | CAGR of 7.90% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Film Type (Polarizing Film, Backlight Film, Others) •By Application (Automotive Display, Televisions, Desktop & Laptops, Smartphones and Tablets, Signage & Advertising Display Boards, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | 3M, Nitto Denko Corporation, LG Chem, Ltd., Toray Industries, Inc., Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., Kolon Industries, Inc., Teijin Limited, Hyosung Chemical, and BenQ Materials Corporation |

Get in Touch