OLED Display Market Report Scope & Overview:

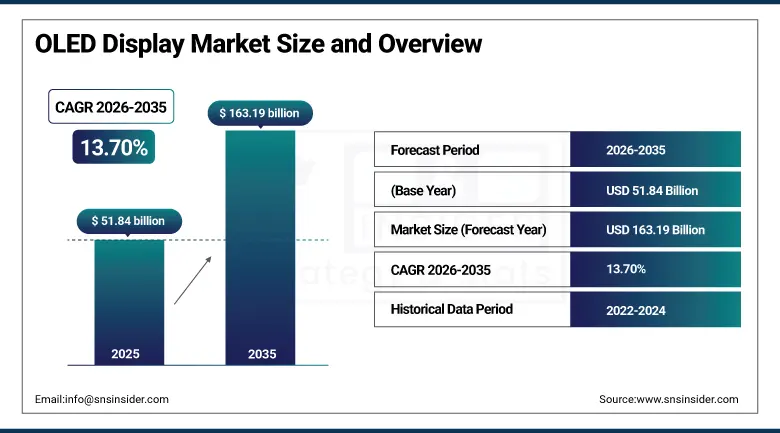

The OLED Display Market size was valued at USD 51.84 Billion in 2025 and is expected to reach USD 163.19 Billion by 2035, growing at a CAGR of 13.70% from 2026 to 2035.

The technology behind organic light-emitting diode displays has proven to be the display technology par excellence within all of the world’s most premium electronic product sectors, having superseded LCD technology within flagships of smartphone brands, shifted OLED TVs into the premium mass market segment, and steadily made inroads into laptop screens, computer monitors, and car displays as well. The key benefit OLEDs possess in comparison to LCD technology lies in the fact that the pixels are made from an organic semiconductor material, and as such can emit their own light without the necessity for a backlight system, polarizer, and colour filter, which are essential parts of LCD technology. As a result, OLED panels can offer infinite contrast ratios, while at the same time being physically superior to LCD technology.

In January 2025, LG Electronics unveiled its revolutionary fully transparent Signature OLED T television, a 77-inch set featuring a 40% transparency mode that allows the display to become a fully see-through panel when not displaying content.

Market Size and Forecast

-

Market Size in 2025: USD 51.84 Billion

-

Market Size in 2026E: USD 58.95 Billion

-

Market Size by 2035: USD 163.19 Billion

-

CAGR: 13.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On OLED Display Market - Request Free Sample Report

OLED Display Market Trends Highlights:

-

Adoption of foldable and rollable OLED displays is increasing in premium smartphones and laptops as manufacturing efficiency improves.

-

OLED demand in laptops and monitors is growing due to its thin design, high contrast, and superior image quality.

-

Automotive OEMs are expanding OLED use in digital cockpits, instrument clusters, and advanced lighting applications.

-

Quantum Dot OLED (QD-OLED) technology is enhancing brightness and colour performance in premium televisions.

-

Tandem OLED architectures are improving display brightness, lifespan, and energy efficiency for next-generation devices.

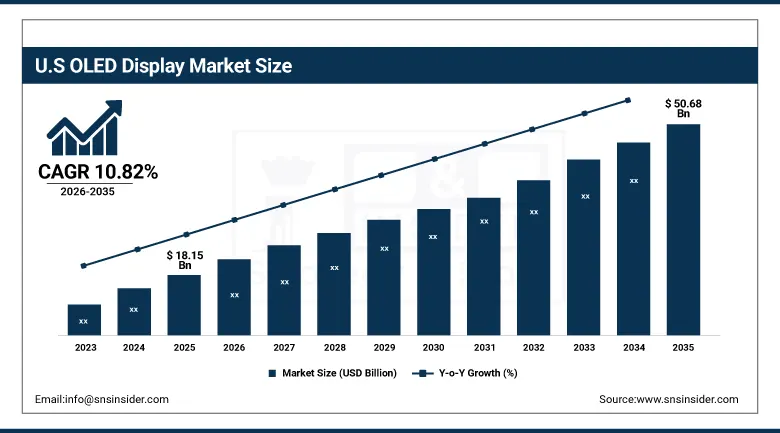

U.S. OLED Display Market Size Outlook

The U.S. OLED Display Market was valued at approximately USD 18.15 Billion in 2025 and is expected to reach approximately USD 50.68 Billion by 2035, growing at a CAGR of approximately 10.82%.

OLED display revenue generated in the United States represents the biggest share worldwide, considering the high cost of devices featuring OLED display technology such as iPhones and iPads by Apple, flagships by Samsung Galaxy, OLED TVs produced by both LG and Sony, and an increasing number of laptops and monitors using OLED panels manufactured by Dell, Asus, and Lenovo. The release of new iPhones creates an unprecedented consumer electronics event in the global demand for OLED screens, whereby millions of consumers upgrade their phones on three to four-year cycles, which means huge orders annually for panel makers such as Samsung Display and LG Display.

Samsung Display announced a 10% production increase in small and mid-sized OLED panel output for 2025, targeting 475.6 million annual units with particular emphasis on high-value products including IT rigid OLED for laptop and tablet applications and foldable displays for the Galaxy Z Fold series, whose 150% planned foldable panel volume increase reflected both growing consumer adoption of foldable form factor devices.

OLED Display Market Segment Analysis

-

By Technology, the RGB-OLED segment dominated the OLED display industry in 2025, while the AMOLED segment is growing at a strong CAGR of 15.29% as smartphones, wearables, and automotive displays drive active-matrix adoption.

-

By Application, the smartphones & tablets segment dominated the OLED display market in 2025, while the automotive displays segment is the fastest growing application during 2026 to 2035.

-

By Panel Size, the small panels segment dominated the OLED display industry in 2025 through smartphone volume, while large panels are growing with OLED television and laptop display expansion.

-

By End User, the consumer electronics segment dominated the OLED display market in 2025, while the automotive segment is the fastest growing end user during 2026 to 2035.

By Technology, RGB-OLED dominates, AMOLED grows fastest

OLED displays using RGB technology – which involves having dedicated emitters for red, green, and blue colours to achieve colour output without using the colour filter – led the way in creating a dominant market revenue share in 2025, as their use in high-end OLED televisions and large-screen displays where economies of scale enable the use of evaporation techniques used in RGB-OLED is possible. Samsung’s QD-OLED televisions and Sony’s Bravia XR OLED televisions showcase the superior colour volume and brightness achieved by RGB-OLED.

AMOLED technology, which uses a white OLED emitter with colour filters driven by an active-matrix TFT backplane, is growing fastest at 15.29% CAGR through its dominant deployment in the world's highest-volume premium display application, the smartphone. Samsung Display's Galaxy series AMOLED supply, LG Display's iPhone panel production, and BOE Technology's expanding AMOLED smartphone panel capacity collectively sustain the AMOLED segment's growth leadership.

By Application, smartphones & tablets dominate, automotive grows fastest

The smartphones and tablets category provided the major application share in revenues in 2025, as OLED gained near-perfect penetration into the premium smartphones market beyond $500 retail price and became increasingly used in midrange devices as increased yield rates and supply chain competitiveness bring the OLED panel price down to be equal to that of LCD panels at prices between USD 300 to USD 500. The use of OLED in the iPhone and Samsung's Galaxy lineup guarantees an annual demand for the OLED panel in smartphones that justifies the capital investments required for the production process and helps to drive down costs further.

Automotive displays are growing fastest as the transformation of vehicle cockpit architecture from discrete analogue instruments to integrated digital display systems creates a new high-value OLED application whose per-vehicle display area and value content substantially exceeds any prior automotive display technology generation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Asia Pacific |

South Korea |

42.84% |

|

Europe |

Germany |

28.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America OLED Display Market Insights

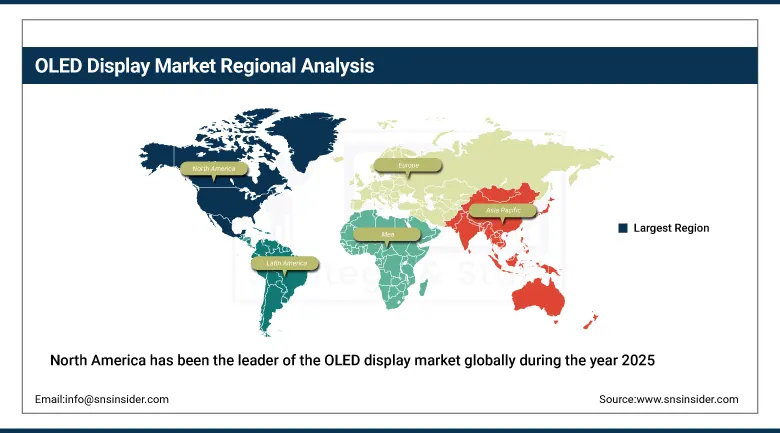

North America has been the leader of the OLED display market globally during the year 2025. North America holds the biggest regional revenue share of the OLED display industry on the basis of the value of devices used by consumers in this region. Almost 82.47% of revenue from the regional market belongs to the United States owing to being the biggest consumer market in the world for OLED enabled high-end electronics such as iPhones, Samsung Galaxy series, OLED TVs, and OLED laptops. The U.S.-headquartered smartphone development policies of Apple determine the specifications required for OLED displays across the world, and premium pricing of American consumer electronics ensures maximum OLED revenue per unit in comparison with other leading national markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific OLED Display Market Insights

Asia Pacific region is the highest revenue generating and fastest growing OLED Display manufacturing region, having the largest share of OLED panel manufacturing capacity in the global display market through its companies like Samsung Display and LG Display in South Korea, BOE Technology in China, and Japan Display in Japan. Around 42.84% share of revenue generated by Asia Pacific comes from South Korea due to dominance of the OLED panel manufacturing capacity of Samsung Display and LG Display, which generate considerable annual revenue for South Korea by providing OLED panels for smartphones, television screens, laptop computers, and automobiles. On the other hand, China is expanding fast because of the AMOLED smartphone panel manufacturing capacity of BOE Technology, Tianma, and Visionox.

Europe OLED Display Market Insights

The share of Europe in the global OLED Display revenue was very substantial in 2025 owing to the premium consumer electronics industry's love of OLED TV, the investments in OLED displays for the automotive industry, and the premium professional display market applications such as broadcast, medical imaging, and creative professional applications made in Europe through the media and healthcare sectors. Approximately 28.47% of Europe's revenue came from Germany due to the investments in premium automotive OEM segment in terms of the cockpit display, the large consumer electronics retail industry in Germany, and development programmes for automotive displays in Europe through Continental, Bosch, and Valeo.

MEA & Latin America OLED Display Market Insights

Middle East and Latin America are witnessing increasing demand owing to increasing adoption of premium consumer electronics, growth in the automotives industry, and increased investment in retail and commercial displays. UAE dominates MEA revenues at around 22.84% of the region's revenues because of the strong demand from its wealthy consumers for premium consumer electronics such as OLED phones and TVs, OLED commercial displays used in retailing, and OLED passenger entertainment systems and ambient displays by the airlines and hotels industries respectively. Brazil is the market leader in Latin America with about 43.84% of the region's revenues driven by its strong consumer electronics industry, increasing adoption of premium smartphones, and entry of OLED TVs.

Market Dynamics

Growth Drivers: Expanding OLED adoption in mid-range smartphones and growing use in laptops and monitors are driving sustained market growth.

The expansion of the OLED display market is facilitated by the gradual shift in OLED usage from exclusive devices to mid-tier products due to yield improvements and competitive development of the supply chain along with economies of scale bringing down the gap between the cost of OLED panels compared to LCD panels, traditionally being significantly higher to gradually moving towards equal costs. The number of unit shipments per year per each succeeding price range that OLEDs reach for smartphones under USD 500 increases substantially compared to the previous range.

The IT OLED market includes laptops and desktop monitors larger than 27 inches whose display quality serves as the key factor influencing the decision to buy an expensive device, and the adoption of OLEDs in that segment is rapidly growing due to the inclusion of OLED displays in the offerings by PC manufacturers along with increasing consumer awareness regarding OLED laptop display benefits.

Restraints: Burn-in concerns and lower peak brightness compared to advanced LCD technologies limit adoption in some applications.

The differential aging of organic materials presents a danger of screen retention in cases where there is static interface elements displayed at a high brightness level for a considerable amount of time, such as navigation map screens, desktop task bars, and broadcast monitors with static overlay components that could form burn-in images across thousands of hours of usage. While significant efforts have been made by display makers to eliminate burn-in risks by utilizing pixel shift, brightness control of static elements, and advancements in organic materials, the legacy perception of burn-in risk deters consumers from buying monitors that might be subject to static content exposure.

Meanwhile, the brightness capability of mini-LED and micro-LED display technologies surpasses 4,000 nits for HDR content, a standard that OLED panels cannot yet achieve, leaving LCDs relevant in outdoor, bright environments, and video wall displays due to their ability to produce brighter images.

Opportunities: Foldable and rollable displays, along with increasing OLED integration in automotive cockpit systems, offer significant growth potential through 2035.

The ability of OLED to be foldable and rollable leads to form factor innovations possible with OLED but not possible at all by LCD’s rigid glass substrate structure, allowing for creation of unique form factor categories of devices powered only by OLED and enabled because of its foldability and rollable nature, categories where the value per panel grows due to greater durability, decreased creasing, and premium that is smaller relative to non-foldable equivalents.

The Samsung Galaxy Z Fold, Motorola Razr, and Huawei Mate X line-up of foldable phones, and the newly emerging foldable laptops produced by Lenovo and Asus represent a growing number of OLED display applications where value of per-panel sales exceeds value of rigid OLED display panels used in regular smartphones. The adoption of automotive OLED into the pillar-to-pillar OLED dashboards makes for display area per car that allows automotive OLED segment to move from a small panel niche market to a large one equal to premium smartphone market.

Recent Developments:

-

2025: LG Electronics unveiled its Signature OLED T fully transparent television at CES 2025, a 77-inch panel that transitions to 40% transparency when not displaying content, creating a new ultra-premium product category whose transparent OLED capability is exclusive to OLED's backlight-free self-emissive architecture.

-

2025: Samsung Display announced a 10% production increase in small and mid-sized OLED panels targeting 475.6 million annual units, with 150% growth in foldable display volumes for the Galaxy Z Fold series, reflecting both consumer adoption acceleration and Samsung's strategy of manufacturing scale leadership in premium flexible OLED.

-

2024: BOE Technology achieved AMOLED smartphone panel qualification with international OEM customers beyond domestic Chinese brands, marking a significant supply chain diversification milestone that introduces a third major source of smartphone OLED panel supply alongside Samsung Display and LG Display for global smartphone manufacturers.

OLED Display Companies are:

-

Samsung Display Co. Ltd.

-

BOE Technology Group Co. Ltd.

-

Tianma Microelectronics Co. Ltd.

-

Visionox Technology Inc.

-

Japan Display Inc.

-

Royole Corporation

-

Kateeva Inc.

-

Applied Materials Inc.

-

Merck KGaA (Display Materials)

-

Sumitomo Chemical Co. Ltd.

-

DuPont de Nemours Inc.

-

Cynora GmbH

-

Joled Inc.

-

Sharp Corporation (Foxconn)

-

AUO Corporation

-

Innolux Corporation

-

CSOT (TCL Technology Group)

-

Futaba Corporation

OLED Display Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 51.84 Billion |

| Market Size by 2035 | USD 163.19 Billion |

| CAGR | CAGR of 13.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (AMOLED, PMOLED, Flexible/Foldable OLED, Transparent OLED, Others) • By Application (Smartphones & Tablets, Televisions, Wearable Devices, Automotive Displays, Monitors & Laptops, Industrial & Medical, Others) • By Panel Size (Small, Medium, Large) • By End User (Consumer Electronics, Automotive, Healthcare, Industrial, Government & Defense) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsung Display Co. Ltd., LG Display Co. Ltd., BOE Technology Group Co. Ltd., Tianma Microelectronics Co. Ltd., Visionox Technology Inc., Japan Display Inc., Royole Corporation, Universal Display Corporation, Kateeva Inc., Applied Materials Inc., Merck KGaA (Display Materials), Sumitomo Chemical Co. Ltd., DuPont de Nemours Inc., Cynora GmbH, Joled Inc., Sharp Corporation (Foxconn), AUO Corporation, Innolux Corporation, CSOT (TCL Technology Group), and Futaba Corporation. |

Frequently Asked Questions

North America dominated the OLED Display Market in 2025 by end-consumer device revenue, with the United States accounting for approximately 82.47% of North American revenues through its premium consumer electronics market and the Apple iPhone product line's OLED panel procurement driving global demand.

The smartphones & tablets segment dominated the OLED Display Market in 2025 as the highest-volume premium display application.

Growth drivers include continued smartphone OLED penetration into mid-range price segments, rapid IT OLED expansion across laptop and monitor markets, foldable and rollable OLED form factor innovation enabling new device categories, automotive cockpit digital display proliferation driving high-value OLED adoption, and quantum dot and tandem stack OLED technology advances improving brightness and lifetime performance.

The OLED Display Market was valued at USD 51.84 Billion in 2025.

The OLED Display Market is expected to grow at a CAGR of 13.70% from 2026 to 2035.

Get in Touch