Oxidized Polyethylene Wax Market Report Scope & Overview:

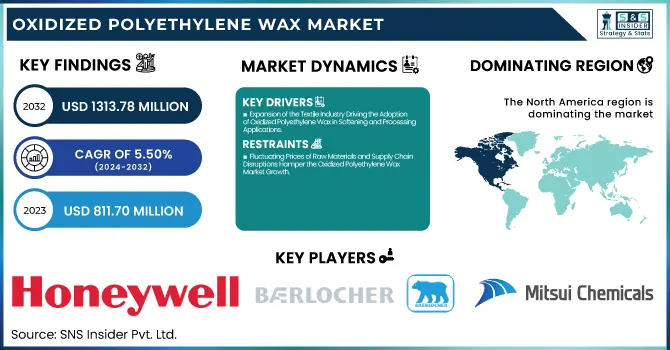

The Oxidized Polyethylene Wax Market Size was valued at USD 811.70 Million in 2023 and is expected to reach USD 1,313.78 Million by 2032, growing at a CAGR of 5.50% over the forecast period of 2024-2032.

To Get more information on Oxidized Polyethylene Wax Market - Request Free Sample Report

The Oxidized Polyethylene Wax Market is evolving as industries prioritize efficiency and sustainability. Raw material sourcing and pricing trends shape production costs, influenced by petroleum-based feedstocks and supply chain fluctuations. Investment and funding trends highlight capital influx for capacity expansion and innovation. A detailed cost structure analysis in the report uncovers key expenses, including raw materials, energy, and labor. As regulations tighten, social and environmental impact assessments gain prominence, driving eco-conscious manufacturing. The rise of sustainability and green alternatives is reshaping strategies, leading to advancements in bio-based and biodegradable waxes. Our report explores these pivotal aspects, offering a comprehensive analysis of market dynamics and future opportunities in this rapidly transforming industry.

Oxidized Polyethylene Wax Market Dynamics

Drivers

-

Expansion of the Textile Industry Driving the Adoption of Oxidized Polyethylene Wax in Softening and Processing Applications

The Oxidized Polyethylene Wax Market is witnessing strong growth due to its increasing application in the textile industry for softening, finishing, and processing fabrics. Textile manufacturers are adopting oxidized polyethylene wax as an essential processing aid to enhance fabric softness, smoothness, and durability. With the growing demand for high-performance textiles in apparel, home furnishings, and industrial applications, the need for advanced softening agents has surged. Additionally, the rise of sustainable and eco-friendly textile processing has prompted manufacturers to explore non-toxic and biodegradable alternatives, where oxidized polyethylene wax plays a crucial role. The demand for high-quality textile finishes, particularly in luxury clothing and technical textiles, has further propelled market expansion. Furthermore, the textile sector’s push toward energy-efficient and cost-effective processing techniques is increasing the adoption of oxidized polyethylene wax, as it reduces friction in fiber processing and improves dye penetration. The growing emphasis on wrinkle-free, water-repellent, and durable fabrics is also creating a favorable environment for the expansion of oxidized polyethylene wax applications in textile finishing.

Restraints

-

Fluctuating Prices of Raw Materials and Supply Chain Disruptions Hamper the Oxidized Polyethylene Wax Market Growth

The Oxidized Polyethylene Wax Market faces challenges due to fluctuating raw material prices and supply chain disruptions. Since the production of oxidized polyethylene wax is heavily dependent on petroleum-based feedstocks, price volatility in crude oil and petrochemical derivatives significantly impacts manufacturing costs. Additionally, supply chain constraints, including trade restrictions, transportation bottlenecks, and geopolitical tensions, have led to unpredictable availability of raw materials, affecting the overall production process. Many manufacturers are struggling to maintain cost efficiency while ensuring consistent product quality. The ongoing global push for sustainability has further pressured the market, as companies explore alternative bio-based and synthetic waxes, leading to increased competition and uncertainty. The reliance on limited suppliers and regional disparities in raw material sourcing has further contributed to price instability. These factors collectively hinder the widespread adoption of oxidized polyethylene wax, especially in price-sensitive industries such as packaging and textiles.

Opportunities

-

Adoption of Oxidized Polyethylene Wax in Advanced Electronic and Semiconductor Manufacturing Applications

The increasing integration of oxidized polyethylene wax in electronics and semiconductor manufacturing is unlocking new market opportunities. With the growing demand for precision coatings, thermal management, and anti-static applications, oxidized polyethylene wax is being utilized in electronic encapsulants, circuit board coatings, and conductive adhesives. The shift toward miniaturization of electronic components and the rise of wearable devices, flexible displays, and high-performance semiconductors are fueling the adoption of advanced wax formulations. Additionally, the emphasis on low-friction, heat-resistant coatings in microelectronics manufacturing is further boosting market demand. As the electronics and semiconductor industry expands globally, the use of oxidized polyethylene wax in specialized coatings and processing applications is expected to grow significantly.

Challenge

-

Limited Awareness and Standardization in Emerging Markets Restrict the Growth of the Oxidized Polyethylene Wax Market

One of the major challenges in the Oxidized Polyethylene Wax Market is the lack of awareness and standardization in emerging markets. While developed regions such as North America and Europe have established regulations and industrial applications for oxidized polyethylene wax, many developing economies lack standardized guidelines for its usage. This has resulted in inconsistent product quality, varied performance attributes, and limited adoption across industries such as plastics, coatings, and adhesives. The absence of strict industry standards and regulatory frameworks in regions like Latin America, the Middle East, and parts of Asia Pacific is restricting market penetration. Manufacturers must focus on awareness campaigns, regulatory compliance, and strategic partnerships to bridge the knowledge gap and enhance market acceptance in these regions.

Oxidized Polyethylene Wax Market Segmental Analysis

By Product

High-Density Oxidized Polyethylene Wax dominated the Oxidized Polyethylene Wax Market in 2023, holding a 54.2% market share. This dominance is driven by its superior thermal stability, hardness, and high molecular weight, making it the preferred choice in plastics, coatings, and adhesives. High-density oxidized polyethylene wax is widely used in polyvinyl chloride (PVC) processing, where it enhances lubrication, melt flow, and surface finish, making it essential for the construction and packaging industries. According to the American Chemistry Council (ACC), the increasing demand for durable and lightweight plastics in automotive and industrial applications has significantly boosted the adoption of high-density variants. Additionally, government initiatives promoting energy-efficient and recyclable materials have favored its use over alternative processing aids. For instance, the U.S. Environmental Protection Agency (EPA) has encouraged the shift towards low-emission additives in polymer production, reinforcing the market leadership of high-density oxidized polyethylene wax.

By Application

Plastics & Polymer Processing led the Oxidized Polyethylene Wax Market in 2023, securing a 38.5% market share. The sector's growth is primarily fueled by the rising demand for high-performance lubricants, dispersing agents, and mold release agents in PVC, polypropylene (PP), and polyethylene (PE) manufacturing. The Plastics Industry Association (PLASTICS) has reported a surge in PVC pipe production for infrastructure projects, significantly driving oxidized polyethylene wax consumption. Additionally, government-backed policies, such as the EU’s Circular Economy Action Plan, emphasize sustainable plastic production, increasing the adoption of oxidized polyethylene wax as a processing aid. The expansion of the automotive and packaging industries, where high-performance polymers are essential for lightweight and durable components, has further strengthened this segment’s dominance. With growing innovations in biodegradable plastics and high-strength composites, the demand for oxidized polyethylene wax in plastics and polymer processing is expected to remain strong.

Oxidized Polyethylene Wax Market Regional Outlook

In 2023, North America dominated the Oxidized Polyethylene Wax Market, accounting for 45.3% market share. This dominance is largely driven by the United States, which has seen significant growth in industries such as plastic manufacturing, automotive, and packaging, all of which utilize oxidized polyethylene wax as a vital processing aid. For example, the U.S. is home to major companies like Honeywell International Inc., which produces advanced polymer additives for the manufacturing sector. Government regulations, such as the EPA's restrictions on harmful chemicals in polymers, have boosted the adoption of eco-friendly and sustainable materials, increasing the demand for high-performance additives like oxidized polyethylene wax. Additionally, the U.S. construction and infrastructure sectors have contributed to growth, with rising demand for high-quality PVC pipes. Canada and Mexico, benefiting from the USMCA trade agreement, have also seen an increase in oxidized polyethylene wax consumption, especially in automotive and industrial coatings.

Moreover, Asia Pacific emerged as the fastest growing region in the Oxidized Polyethylene Wax Market, with a significant growth rate during the forecast period. This rapid growth is propelled by China, India, and Japan, where expanding manufacturing sectors and increasing demand for plastics and packaging have boosted the consumption of oxidized polyethylene wax. China’s dominance in the plastic processing industry, particularly in polyethylene and polypropylene production, has led to increased use of oxidized polyethylene wax in enhancing polymer properties like flowability and durability. Furthermore, India’s automotive and infrastructure sectors are growing rapidly, contributing to the demand for this product. The Chinese government’s support for manufacturing and sustainable technologies, as part of their Made in China 2025 initiative, has created a favorable environment for the market. As the Asia Pacific's industrialization continues, the demand for performance additives like oxidized polyethylene wax is set to surge, strengthening its position in this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Honeywell International Inc. (AC 629, AC 316)

-

Baerlocher GmbH (BAEROPOL RST, BAEROPOL T-Blend)

-

SCG Chemicals Co., Ltd. (SCG PE WAX LP1020P, SCG PE WAX LP1020F)

-

Mitsui Chemicals, Inc. (Hi-WAX 110P, Hi-WAX 220P)

-

Clariant (Licowax PE 520, Licowax PE 130)

-

Trecora Resources (PERFORMALENE 400, PERFORMALENE 500)

-

Westlake Chemical Corporation (Epolene N-10, Epolene N-34)

-

Deurex AG (DEUREX X 50, DEUREX X 51)

-

Marcus Oil & Chemical (OPE Wax 1020, OPE Wax 1025)

-

Munzing Chemie GmbH (CERETAN ME 0825, CERETAN ME 0830)

-

Sanyo Chemical Industries Ltd. (SANWAX 161P, SANWAX 171P)

-

Shanghai Fine Chemical Co., Ltd. (OPE Wax 629A, OPE Wax 629B)

-

Qingdao Sainuo Chemical Co., Ltd. (Sainuo OPE Wax 102, Sainuo OPE Wax 105)

-

EUROCERAS Sp. z o.o. (CERONAS OX 12, CERONAS OX 14)

-

Hase Petroleum Wax Company (Hase OPE Wax 100, Hase OPE Wax 200)

-

BASF (Luwax OA 3, Luwax OA 6)

-

Innospec Inc. (VISCO 200, VISCO 250)

-

Zell Wax (Zellwax OPE 85, Zellwax OPE 90)

-

MPI Chemie B.V. (MICHEM OX 12, MICHEM OX 14)

-

Industrial Raw Material LLC (IRM OPE Wax 100, IRM OPE Wax 200)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 811.70 Million |

| Market Size by 2032 | USD 1,313.78 Million |

| CAGR | CAGR of 5.50% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (High Density, Low Density) •By Application (Plastics & Polymer Processing, Paints, Coatings & Printing Inks, Textile Processing, Rubber Processing, Adhesives, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Honeywell International Inc., The Lubrizol Corporation (Berkshire Hathaway Inc.), SCG Chemicals Co., Ltd., Baerlocher GmbH, BASF SE, Clariant AG, Deurex AG, Mitsui Chemicals Inc., Sanyo Chemical Industries Ltd., Marcus Oil and other key players |

Frequently Asked Questions

Ans: The United States contributed the most to the Oxidized Polyethylene Wax Market in 2023.

Ans: The electronics and semiconductor manufacturing sectors are experiencing significant adoption of Oxidized Polyethylene Wax for specialized coatings and applications.

Ans: The Oxidized Polyethylene Wax Market is expected to grow at a CAGR of 5.50% over the forecast period from 2024 to 2032.

Ans: The Oxidized Polyethylene Wax Market is expected to reach USD 1,313.78 Million by 2032.

Ans: The Oxidized Polyethylene Wax Market size was valued at USD 811.70 Million in 2023.

Get in Touch