Ceramic Membranes Market Report Scope & Overview:

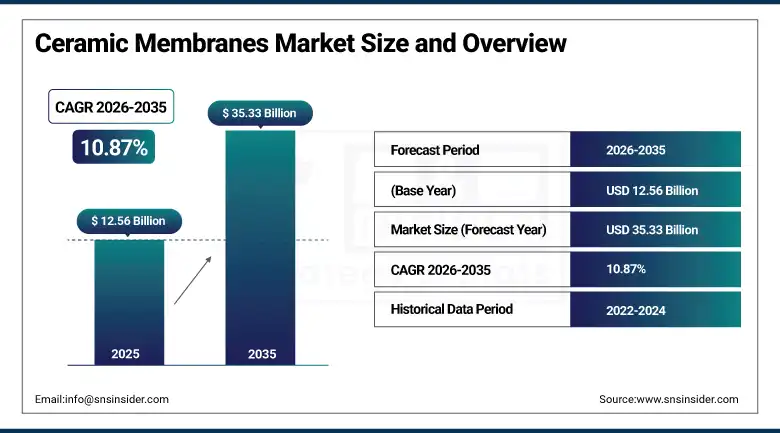

The Ceramic Membranes Market was valued at USD 12.56 Billion in 2025 and is expected to reach USD 35.33 Billion by 2035, growing at a CAGR of 10.87% from 2026–2035.

The global ceramic membranes market is advancing at an exceptional pace. Ceramic membranes are inorganic filtration structures fabricated from alumina, zirconia, titania, or silica materials whose chemical stability, thermal resistance, mechanical durability, and long operational lifespan create commercial advantages over polymeric membrane alternatives in demanding industrial and municipal filtration environments. Rising demand for clean and safe water, stringent environmental regulations on industrial effluent discharge, and the growing need for sustainable separation technologies across pharmaceutical, food, and chemical processing industries collectively sustain above-average market growth. In 2023, China, Germany, and the U.S. led ceramic membrane production with utilisation rates highest in wastewater treatment and food and beverage applications. Hybrid ceramic membrane development and AI-driven process optimisation are creating new commercial applications.

In 2023, Pall Corporation announced the launch of a new range of ceramic membranes designed for high-performance industrial filtration, aimed at reducing energy consumption and operational costs for end-users. The product range targets industrial operators seeking to replace polymeric membrane systems with ceramic alternatives whose superior resistance to chemical cleaning agents and backwashing enables higher recovery rates, lower replacement frequency, and reduced total cost of ownership across multi-year operational cycles.

Market Size and Forecast

-

Market Size in 2026E: USD 13.93 Billion

-

Market Size by 2035: USD 35.33 Billion

-

CAGR: 10.87% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Ceramic Membranes Market - Request Free Sample Report

Ceramic Membranes Market Trends

-

Hybrid ceramic–polymeric membranes are gaining traction by combining durability and cost efficiency for diverse industrial filtration applications.

-

AI-driven process optimization is improving membrane efficiency, reducing fouling, and lowering operational costs through real-time system control.

-

Growing pharmaceutical and biopharmaceutical adoption is driven by stringent sterile filtration and validated separation requirements.

-

Expanding use in hydrogen production and fuel cell systems is emerging as a key high-growth industrial application.

-

Rising demand for decentralized water treatment solutions is boosting adoption in remote and harsh operating environments.

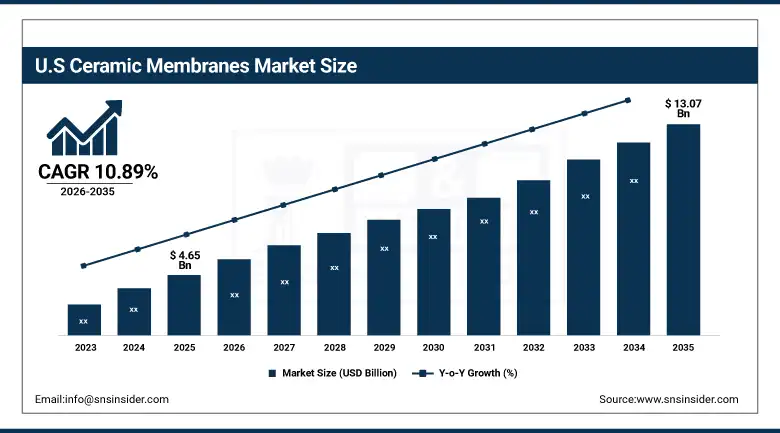

The U.S. Ceramic Membranes Market Outlook

The U.S. Ceramic Membranes Market was valued at approximately USD 4.65 Billion in 2025 and is expected to reach approximately USD 13.07 Billion by 2035, growing at a CAGR of approximately 10.89%.

The U.S. is the world’s most commercially sophisticated ceramic membranes market within North America’s approximately 38% global revenue leadership. Stringent EPA wastewater treatment standards, pharmaceutical FDA GMP filtration requirements, and the food and beverage industry’s FSMA compliance investment collectively create structured institutional demand for ceramic membrane filtration capability. Pall Corporation, CoorsTek, and Nanostone Water are U.S.-headquartered ceramic membrane technology companies whose domestic market presence and export capability sustain the country’s commercial and technology leadership position. IRA infrastructure investment in water treatment and industrial processing is creating above-average government-related procurement.

Nanostone Water expanded its ceramic membrane production capacity in 2024 for municipal water and wastewater treatment applications, targeting the growing U.S. municipal market’s interest in ceramic membrane replacement of ageing polymeric ultrafiltration systems. The expansion reflects the commercial recognition that ceramic membranes’ 20+ year operational lifespan and superior backwash tolerance create lifecycle economics that justify the higher initial capital cost relative to conventional polymeric membrane systems in long-duration municipal water treatment contracts.

Ceramic Membranes Market Segment Analysis

-

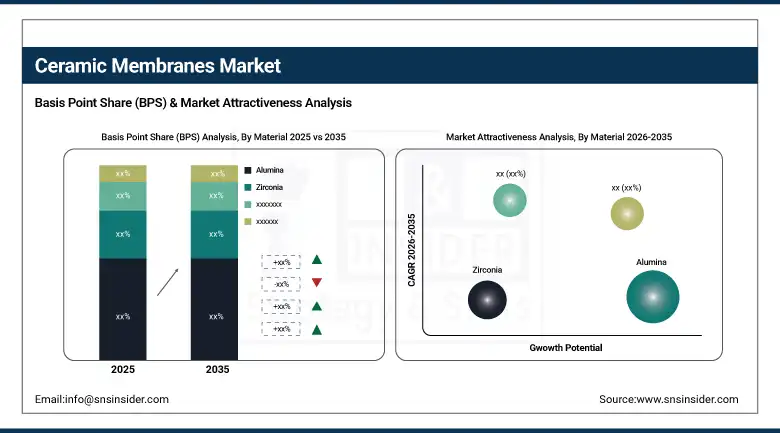

By Material, alumina segment dominated the ceramic membranes market with approximately 45.8% share in 2025, while the zirconia segment is the fastest growing with a CAGR of approximately 12.5%.

-

By Technology, ultrafiltration segment dominated the ceramic membranes market with approximately 33.7% share in 2025, while the microfiltration segment is the fastest growing with a CAGR of approximately 13.2%.

-

By Application, water & wastewater treatment segment dominated the ceramic membranes market with approximately 38% share in 2025, while the food & beverage processing segment is the fastest growing.

-

By End User, municipal segment dominated the ceramic membranes market with approximately 52% share in 2025, while the industrial segment is the fastest growing with a CAGR of approximately 12.8%.

By Material, alumina dominates, zirconia grows fastest

Alumina retained the dominant material position with approximately 45.8% of the ceramic membranes market in 2025. Its commercial primacy reflects the combination of superior chemical and thermal properties, wide raw material availability, and the competitive manufacturing cost that alumina’s established production infrastructure provides relative to premium alternatives. Alumina membranes withstand pH extremes from 0 to 14, temperatures up to 400°C, and aggressive chemical cleaning with caustic soda and nitric acid whose combined environmental tolerance profile makes alumina the default specification for water treatment, chemical processing, and food applications where harsh operating conditions are routine. The extensive published performance data and application reference base that alumina membranes have accumulated across decades of commercial deployment sustains their specification preference in procurement decisions.

Zirconia is the fastest-growing material at approximately 12.5% CAGR because the pharmaceutical, biopharmaceutical, and high-purity chemical industries’ adoption of ceramic membranes for critical separation applications requires the superior chemical inertness, narrower pore size distribution, and validated extractable profile that zirconia delivers at specifications alumina cannot achieve for the most demanding applications. Zirconia’s hydrophilic surface chemistry reduces protein fouling in biological filtration, creating flux advantages in fermentation harvest, cell culture clarification, and biopharmaceutical purification that justify zirconia’s premium pricing relative to alumina alternatives in these high-value application contexts.

By Application, water & wastewater dominates, food & beverage grows fastest

Water and wastewater treatment retained the dominant application position with approximately 38% of the ceramic membranes market in 2025. The extraordinary global scale of municipal and industrial water treatment investment, combined with increasingly stringent effluent discharge standards and drinking water quality regulation, creates the most commercially certain and largest aggregate ceramic membrane procurement category. Each new municipal membrane bioreactor installation and each industrial wastewater treatment compliance upgrade creates ceramic membrane procurement whose operational durability justifies ceramic’s higher capital cost over the 20+ year system lifetime. Rising alumina costs in China due to energy tariffs, documented by the SNS Insider report, create supply chain monitoring requirements but do not alter ceramic’s fundamental commercial advantage in high-value treatment applications.

Food and beverage processing is the fastest-growing application because ceramic membranes’ inert, non-contaminating, and steam-sterilisable properties uniquely satisfy the hygienic processing requirements of wine, beer, fruit juice, dairy, and edible oil applications whose product quality and food safety standards prohibit the leachable plasticisers and hydrolysable components that conventional polymeric membranes contain. Clean-in-place compatibility with hot caustic and acidic cleaning agents, combined with the elimination of membrane replacement frequency that polymeric systems impose, creates total cost of ownership advantages that are progressively overcoming ceramic’s higher initial capital cost barrier in food processing procurement.

By Technology, ultrafiltration dominates, microfiltration grows fastest

Ultrafiltration retained the dominant technology position with approximately 33.7% of the ceramic membranes market in 2025. Ceramic ultrafiltration’s 2-100nm pore size range spans the most commercially valuable separation applications including virus removal in biopharmaceutical manufacturing, macromolecule concentration in food processing, suspended solids removal in water treatment, and colloid and protein separation in chemical processing. The UF pore range’s alignment with the most commercially demanding molecular weight cut-off requirements for pharmaceutical protein purification creates above-average per-unit commercial value that sustains ceramic UF’s commercial leadership within the technology category.

Microfiltration is the fastest-growing technology at approximately 13.2% CAGR because the expanding adoption of ceramic microfiltration as a prefiltration stage before downstream reverse osmosis, nanofiltration, and ultrafiltration systems creates growing demand in municipal drinking water plants, industrial cooling water treatment, and swimming pool water recirculation systems where the MF stage’s turbidity and suspended solids removal improves downstream membrane performance and longevity. Each new membrane-based water treatment plant installation that specifies ceramic MF as its initial separation stage creates procurement that compounds with global water infrastructure investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Ceramic Membranes Market Insights

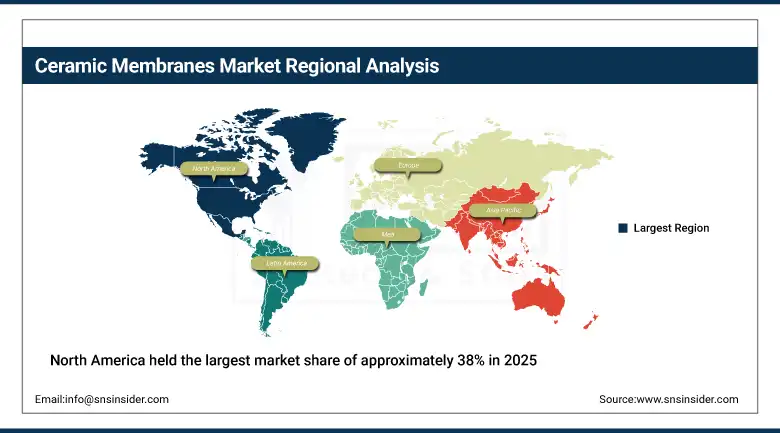

North America held the largest market share of approximately 38% in 2025, driven by stringent EPA environmental regulations, high investments in water treatment infrastructure, and developed industrial applications across pharmaceutical, food, and chemical processing sectors. The United States accounts for approximately 87.4% of North American revenues through Pall Corporation, CoorsTek, and Nanostone Water’s commercial presence, EPA wastewater treatment compliance investment, and the pharmaceutical industry’s FDA GMP filtration requirement.

Canada contributes in revenues through its municipal water treatment infrastructure investment, pharmaceutical manufacturing sector’s ceramic membrane adoption, and the mining industry’s industrial wastewater treatment requirements whose harsh chemical effluent streams favour ceramic membrane’s superior chemical resistance over polymeric alternatives.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Ceramic Membranes Market Insights

Europe is a technically sophisticated ceramic membranes market where the EU’s Water Framework Directive, Industrial Emissions Directive, and pharmaceutical GMP regulation collectively create structured institutional demand across multiple high-value application categories. Germany accounts for approximately 22.3% of European revenues through its advanced chemical industry’s ceramic membrane adoption, ATECH Innovations and Inocermic’s domestic technology leadership, and the municipal water treatment sector’s above-average ceramic membrane specification rate. European alumina cost stabilisation supported by government subsidies, documented by SNS Insider’s market analysis, sustains competitive membrane manufacturing economics.

France and the Netherlands are significant secondary European markets where TAMI Industries’ French commercial presence creates a domestic supply anchor, and the food and beverage industry’s ceramic membrane adoption for wine and dairy processing creates consistent high-value application procurement. The EU Green Deal’s water reuse regulation progressively creating ceramic membrane demand as the preferred technology for reclaimed water quality assurance represents a growing commercial programme.

Asia Pacific Ceramic Membranes Market Insights

Asia Pacific is the fastest-growing regional ceramic membranes market, driven by China’s rapid urbanization creating municipal water treatment investment, India’s industrial wastewater treatment compliance requirements, Japan’s advanced pharmaceutical manufacturing adoption, and the semiconductor industry’s ultra-pure water ceramic membrane demand across Taiwan, South Korea, and Singapore. China accounts for approximately 54.6% of Asia Pacific revenues through its leadership as one of three global ceramic membrane production centres alongside Germany and the U.S., substantial municipal water treatment infrastructure investment, and JIUWU HI-TECH’s domestic market leadership.

India represents the most commercially dynamic emerging market within Asia Pacific, where the National Clean Ganga Mission’s river remediation investment, industrial effluent treatment regulatory tightening, and the pharmaceutical sector’s ceramic membrane adoption for API purification are collectively creating above-average market growth whose commercial momentum is progressively attracting international ceramic membrane manufacturers.

MEA & Latin America Ceramic Membranes Market Insights

The Middle East and Africa and Latin America are growing ceramic membranes markets where water scarcity, industrial development, and environmental regulation are creating structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through its desalination infrastructure investment, ARAMCO’s industrial water treatment, and Vision 2030’s water security programme that creates above-average ceramic membrane procurement for the most demanding saline and industrial effluent treatment applications.

Brazil leads Latin American revenues at approximately 44.2% through its mining sector’s industrial wastewater treatment, the food and beverage industry’s ceramic membrane adoption for sugar cane juice processing and tropical fruit clarification, and the pharmaceutical sector’s growing ceramic filtration investment whose Brazilian manufacturing base creates consistent domestic procurement.

Market Dynamics

Growth Drivers: Water scarcity driving clean water demand and pharmaceutical regulatory requirements creating premium ceramic adoption

Rising global water scarcity and stricter effluent discharge regulation is the ceramic membranes market’s most structurally certain commercial growth driver. The UN’s projection that 5.7 billion people will face water shortage by 2050 creates non-discretionary investment motivation for water treatment infrastructure whose ceramic membrane component grows with the technology’s demonstrated performance superiority over conventional sand filtration and polymeric membrane alternatives. Each new municipal water treatment facility constructed in water-stressed regions and each industrial effluent compliance upgrade creates ceramic membrane procurement whose operational durability justifies the initial capital premium.

Pharmaceutical and biopharmaceutical regulatory requirements are creating a high-value ceramic membrane demand category whose per-module commercial value and application criticality sustain premium pricing independent of water treatment commodity market dynamics. FDA’s guidance on virus removal validation, EMA’s biologics purification requirements, and the growing GMP-grade filtration demand from the monoclonal antibody, vaccine, and gene therapy manufacturing sectors collectively create structured pharmaceutical ceramic membrane procurement whose commercial value per installation substantially exceeds municipal water treatment economics.

Restraints: High initial capital cost limiting adoption over polymeric alternatives and raw material price volatility

The high capital cost of ceramic membrane systems, typically 3-5 times the initial investment of equivalent polymeric membrane installations, creates adoption barriers in cost-sensitive municipal and industrial procurement environments where total cost of ownership analysis over the ceramic’s 20+ year lifespan demonstrates superior economics but budget allocation constraints favour the lower initial expenditure of polymeric alternatives. Infrastructure funding cycles and capital budget limitations frequently prioritise lower initial cost over long-term operational savings, delaying ceramic membrane adoption beyond its economically optimal deployment timing.

Raw material price volatility for alumina, zirconia, and titania creates manufacturing cost uncertainty that complicates ceramic membrane project pricing and margin management. Rising alumina costs in China due to energy tariffs, documented in market analysis, create supply chain cost pressure whose downstream impact on membrane pricing reduces competitive position relative to polymeric alternatives whose petroleum-derived raw material costs respond to different commodity market cycles.

Opportunities: Hydrogen production membrane applications and pharmaceutical bioprocessing expansion

Hydrogen production represents the most commercially significant new industrial application for ceramic membranes whose proton exchange membrane and gas separation functions in hydrogen electrolysis, steam methane reforming, and hydrogen purification create structured demand from the hydrogen economy’s investment programmes. European, Japanese, and U.S. hydrogen infrastructure investment programmes collectively represent a multi-billion-dollar procurement pipeline whose ceramic membrane component grows with each new hydrogen production facility commissioned.

Pharmaceutical bioprocessing expansion represents the most commercially valuable near-term ceramic membrane application growth opportunity. The biologics market’s double-digit growth, combined with the progressive adoption of continuous bioprocessing architectures that benefit from ceramic membrane’s reusability and validated cleanability, is creating a sustained commercial demand increase for high-specification pharmaceutical-grade ceramic membrane systems whose application diversity spans fermentation clarification, purification, and virus filtration across the biopharmaceutical manufacturing value chain.

Recent Developments:

-

2024: Nanostone Water expanded its ceramic membrane production capacity in 2024 for municipal water and wastewater treatment applications, targeting the growing U.S. municipal market’s interest in ceramic membrane replacement of ageing polymeric ultrafiltration systems whose 20+ year ceramic lifespan creates compelling lifecycle economics for long-duration infrastructure contracts.

-

2023: Pall Corporation launched a new range of ceramic membranes for high-performance industrial filtration in 2023, targeting energy consumption reduction and operational cost improvement for industrial end-users replacing polymeric systems with ceramic alternatives whose superior backwash tolerance and chemical resistance reduce total replacement cost.

-

2023: TAMI Industries introduced a next-generation ceramic membrane module optimised for biopharmaceutical applications in 2023, enhancing separation efficiency and selectivity for critical pharmaceutical production processes whose regulatory requirements demand validated, chemically inert filtration with documented extractable profiles.

Ceramic Membranes Market Key Players are:

-

Pall Corporation

-

TAMI Industries

-

Atech Innovations GmbH

-

Veolia Water Technologies

-

BASF SE

-

Nanostone Water

-

CoorsTek

-

Inocermic GmbH

-

Saint-Gobain

-

JIUWU HI-TECH Co., Ltd.

-

Liqtech International

-

Inopor GmbH

-

Kerasep (VEOLIA)

-

Mitsubishi Chemical

-

Membrana (3M)

-

ItN Nanovation

-

Hyflux Ltd.

-

TOTO Ltd.

-

Kyocera Corporation

-

Cembrane A/S

Ceramic Membranes Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.56 Billion |

| Market Size by 2035 | USD 35.33 Billion |

| CAGR | CAGR of 10.87% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Alumina, Zirconia, Titania, Silica, Others) • By Technology (Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis) • By Application (Water & Wastewater Treatment, Food & Beverage Processing, Pharmaceutical & Biotechnology, Chemical Processing, Energy & Power, Others) • By End User (Municipal, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pall Corporation, TAMI Industries, Atech Innovations GmbH, Veolia Water Technologies, BASF SE, Nanostone Water, CoorsTek, Inocermic GmbH, Saint-Gobain, JIUWU HI-TECH Co., Ltd., Liqtech International, Inopor GmbH, Kerasep (Veolia), Mitsubishi Chemical, Membrana (3M), ItN Nanovation, Hyflux Ltd., TOTO Ltd., Kyocera Corporation, and Cembrane A/S |

Frequently Asked Questions

The Ceramic Membranes Market is expected to grow at a CAGR of 10.87% from 2026 to 2035.

The Ceramic Membranes Market was valued at USD 12.56 Billion in 2025.

Rising global water scarcity, stricter wastewater discharge regulations, and increasing investments in water treatment infrastructure are driving the Ceramic Membranes Market.

Alumina dominated the Ceramic Membranes Market with approximately 45.8% share in 2026, while Zirconia is the fastest growing with a CAGR of approximately 12.5%.

North America dominated the Ceramic Membranes Market with approximately 38% share in 2025.

Get in Touch