Patient Safety and Risk Management Software Market Size & Overview:

The Patient Safety And Risk Management Software Market Size was valued at USD 2.25 billion in 2023 and is expected to reach USD 6.07 billion by 2032 and grow at a CAGR of 11.69% over the forecast period 2024-2032.

Get more information on Patient Safety and Risk Management Software Market - Request Sample Report

The patient safety and risk management software market is seeing robust growth, driven by increasing patient safety concerns, regulatory requirements, and the widespread adoption of electronic health records. According to a study, nearly 400,000 deaths occur annually in the United States alone due to preventable medical errors, underlining the importance of risk management systems in healthcare. As healthcare facilities face growing pressure to reduce such errors, patient safety software has emerged as a critical tool to monitor, identify, and mitigate risks in real time.

For example, in 2019, the implementation of the EHR system in the UK’s National Health Service significantly improved the ability to track patient data and safety events, highlighting the correlation between digitized health records and improved patient outcomes. In addition, a 2020 study in The Journal of Patient Safety revealed that hospitals using advanced risk management systems saw a 20% reduction in the occurrence of medication errors and a 15% decrease in adverse events in general. This data supports the effectiveness of integrated safety and risk management software in addressing the most common sources of patient harm.

The growing integration of AI and machine learning technologies into these software solutions is another key factor driving market adoption. These technologies enable predictive analytics, allowing healthcare providers to anticipate potential risks before they manifest. A prominent example is the implementation of AI-powered predictive models at the Mayo Clinic, which has helped in the early detection of deteriorating patient conditions, thus reducing the number of critical care complications by up to 25%.

Moreover, government regulations like the Health Insurance Portability and Accountability Act and the Patient Protection and Affordable Care Act in the U.S. have led to stricter guidelines around patient safety, further encouraging the adoption of these systems. A 2019 HIMSS study showed that 85% of hospitals in the U.S. now utilize some form of safety and risk management software, demonstrating a clear shift toward prioritizing patient safety through technology.

Patient Safety And Risk Management Software Market Dynamics

Drivers

-

Rising Prevalence of Medical Errors

Medical errors remain one of the leading causes of death and injury worldwide. Studies suggest that over 400,000 deaths annually in the U.S. are linked to preventable medical errors, such as medication mistakes, misdiagnoses, or procedural issues. This alarming statistic has made patient safety a priority for healthcare systems, driving demand for advanced risk management software. Such systems help healthcare providers proactively monitor, identify, and address potential risks, ensuring a safer environment for patients. The software assists in minimizing errors through real-time alerts, predictive analytics, and streamlined workflows, leading to better care outcomes. As healthcare organizations increasingly focus on improving safety, the need for effective risk management tools that can reduce human error and prevent adverse events has grown significantly, making patient safety software a crucial investment in healthcare facilities worldwide.

-

Strict Regulatory Compliance and Patient Data Security

Government regulations, such as the Health Insurance Portability and Accountability Act in the U.S. and the General Data Protection Regulation in Europe, require healthcare organizations to adhere to strict safety and data security protocols. Compliance with these regulations is paramount, not just for avoiding fines, but also to ensure patients' sensitive data is protected. The integration of patient safety and risk management software enables organizations to meet these regulations by automating safety checks, securely managing patient information, and providing the transparency needed for audits. By implementing these systems, healthcare providers can enhance patient trust and safeguard against legal repercussions while also improving the quality of care. This regulatory pressure acts as a significant driver for the adoption of risk management software in the healthcare industry.

-

Technological Advancements in AI and Predictive Analytics

Advancements in artificial intelligence, machine learning, and predictive analytics have become significant catalysts for the growth of patient safety and risk management software. AI algorithms and ML models can analyze vast amounts of patient data in real time, identifying patterns and predicting potential risks before they manifest. These technologies enable healthcare providers to anticipate and prevent adverse events such as infections, falls, or complications in surgical procedures. Predictive analytics, for instance, can highlight high-risk patients and offer actionable insights, allowing for timely intervention and better decision-making. As these technologies evolve, their integration into patient safety software is transforming healthcare by allowing providers to move from a reactive to a proactive approach to managing patient risks, driving demand for advanced safety solutions.

Restraints

-

Significant upfront investment required for implementation, as well as the ongoing maintenance and training costs.

For many healthcare organizations, especially smaller hospitals or clinics, the financial burden of purchasing, integrating, and maintaining such software can be prohibitive. The initial costs involve not only software licensing but also infrastructure upgrades, data migration, and staff training to ensure the effective use of the system. Additionally, the complexity of integrating new systems with existing Electronic Health Records and hospital management software can further increase costs and extend implementation timelines. Despite the long-term benefits in patient safety and operational efficiency, the high financial investment may deter some organizations from adopting these solutions, particularly in regions with limited healthcare budgets or resources. This challenge could slow the growth of the market as healthcare systems weigh the costs against the anticipated returns.

Patient Safety And Risk Management Software Market Segmentation Analysis

By Type

In 2023, risk management & safety solutions dominated the market, accounting for 64.2% of the total market share. This dominance can be attributed to the increasing focus on minimizing medical errors, improving patient safety, and meeting stringent regulatory requirements. Healthcare organizations are investing in these solutions to proactively identify and mitigate risks in real time, ensuring safer environments for patients and reducing the likelihood of adverse events. These solutions also offer comprehensive monitoring of healthcare processes, ensuring compliance with safety protocols and enhancing overall care quality.

The governance, risk & compliance solutions segment is witnessing rapid growth in the Patient Safety and Risk Management Software market due to the increasing emphasis on regulatory compliance and the need for healthcare organizations to navigate complex legal and safety standards. With the rising complexity of regulations surrounding healthcare practices, including data security, patient privacy, and operational transparency, healthcare providers are increasingly adopting GRC solutions to manage compliance across various frameworks such as HIPAA, GDPR, and other local regulations.

By Deployment Mode

In 2023, private cloud dominated the deployment mode segment, capturing around 55% of the market share. The preference for private cloud solutions can be attributed to their enhanced security features, control over sensitive patient data, and compliance with strict regulatory frameworks like HIPAA and GDPR. Healthcare organizations prioritize data privacy and security, making private cloud deployment the preferred choice for those handling sensitive health information.

The public cloud deployment mode is the fastest-growing segment, driven by the increasing adoption of cloud computing across the healthcare sector. Public cloud solutions offer scalability, flexibility, and cost-effectiveness, making them especially appealing to small and medium-sized healthcare organizations that may lack the infrastructure or resources to manage on-premises systems. The ability to access data from anywhere is another key advantage, enhancing collaboration and improving workflow efficiency across healthcare networks.

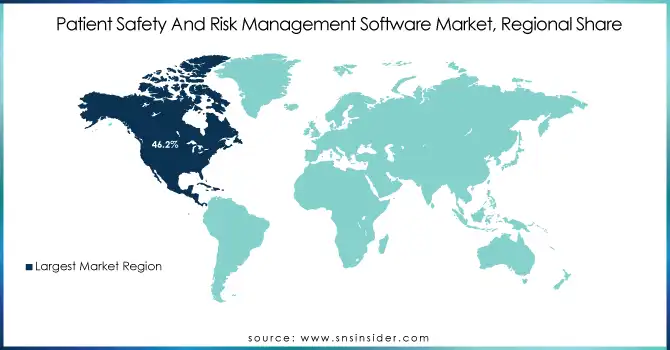

Patient Safety And Risk Management Software Market Regional Outlook

The North American region dominated the patient safety and risk management software market, accounting for a 46.2% share in 2023. The region's strong market position is driven by a well-established healthcare infrastructure, the presence of key market players, and stringent regulatory requirements such as HIPAA. With an increasing focus on improving patient safety and reducing medical errors, healthcare organizations in North America continue to invest heavily in risk management and safety solutions. Additionally, the rising adoption of advanced technologies, such as cloud computing and artificial intelligence, further contributes to the market's growth in this region.

Europe followed closely, holding a significant market share in 2023. The European healthcare industry is undergoing a digital transformation, with many countries adopting electronic health records and other digital health technologies. Regulations like the GDPR and the emphasis on patient privacy and safety are fueling the demand for risk management software solutions. As healthcare organizations in Europe focus on improving care quality and meeting regulatory standards, the adoption of risk management and safety solutions is on the rise.

In Asia-Pacific, the market is experiencing rapid growth. The increasing demand for healthcare services, expanding healthcare infrastructure, and rising government initiatives to enhance patient safety are key drivers. Countries such as China, India, and Japan are seeing a surge in the adoption of healthcare IT solutions, including risk management software, to address the challenges posed by large and diverse populations.

Need any customization research on Patient Safety and Risk Management Software Market - Enquiry Now

Key Players

-

Riskonnect, Inc. – Riskonnect Enterprise Risk Management (ERM), Riskonnect Healthcare Risk Management Software

-

Origami Risk LLC – Origami Risk Management Solutions, Healthcare Risk Management Solutions

-

RLDatix – RL6 Safety Management Software, RLDatix Risk Management Platform

-

Health Catalyst – Health Catalyst Data Platform for Healthcare Risk Management, Clinical Risk Management Software

-

Conduent, Inc. – Conduent Risk Management Solutions, Healthcare Risk Management Software Solutions

-

symplr – symplr Risk Management, symplr Compliance & Safety Solutions

-

Clarity Group, Inc. – Clarity Risk Management Software, Clarity Safety, and Compliance Solutions

-

Becton, Dickinson, and Company (BD) – BD Pyxis Risk Management Software, BD Medical Safety Solutions

-

RiskQual Technologies, Inc. – RiskQual Healthcare Safety Solutions, Healthcare Risk Qualifier (HRQ) Software

-

Prista Corporation – Prista Risk Management Solutions, Prista Patient Safety Management Software

-

Quantros, Inc. – Quantros Safety Management Software, Quantros Risk Management Suite

-

Smartgate Solutions Ltd. – Smartgate Risk Management Software, Patient Safety Solutions

-

The Patient Safety Company – Patient Safety Risk Management Solutions, Risk Reporting, and Monitoring Software

-

Verge Health – Verge Health Safety and Compliance Software, Verge Health Risk Management Solutions

Recent Developments

In May 2024, RLDatix launched the RLDatix Safety Institute, an approved Patient Safety Organization (PSO) focused on researching best practices for safety design and care delivery risk reduction. Leveraging its widespread presence in hospitals and access to vast data through its Healthcare Operations Cloud, the institute will utilize AI tools to identify key risk factors in healthcare safety.

In Feb 2024, Performance Health Partners was recognized as the top provider of healthcare Safety, Risk, and Compliance software in the “2024 Best in KLAS: Software & Services Report,” published on February 7. This marks the second consecutive year the company has earned the highest score in this category, particularly for its incident management system and risk management tools.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 2.25 Billion |

| Market Size by 2032 | US$ 6.07 Billion |

| CAGR | CAGR of 11.69% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

|

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles |

Riskonnect, Inc., Origami Risk LLC, RLDatix, Health Catalyst, Conduent, Inc., symplr, Clarity Group, Inc., Becton, Dickinson and Company (BD), RiskQual Technologies, Inc., Prista Corporation, Quantros, Inc., Smartgate Solutions Ltd., The Patient Safety Company, and Verge Health. |

| DRIVERS |

|

| RESTRAINTS |

|

Frequently Asked Questions

The market for patient safety and risk management software was dominated by North America.

The Patient Safety And Risk Management Software Market size was valued at US$ 2.25 Bn in 2023.

Patient safety and risk management software is intended to speed clinical processes, avoid injuries and other negative outcomes, help manage claims, cut administrative expenses, and improve overall efficiency of day-to-day operations for hospitals, long-term care facilities, and other end users.

Key drivers of the Patient Safety and Risk Management Software Market is Errors in medicine, Infection outbreaks at hospital.

Significant upfront investment required for implementation, as well as the ongoing maintenance and training costs.

Get in Touch