Photocatalytic Coatings Market Report Scope & Overview:

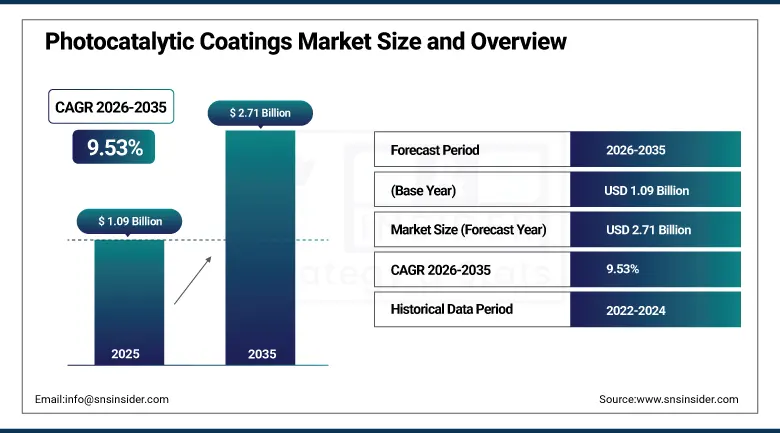

The Photocatalytic Coatings Market was valued at USD 1.09 Billion in 2025 and is expected to reach USD 2.71 Billion by 2035, growing at a CAGR of 9.53% from 2026-2035.

The Photocatalytic Coatings market is growing due to an increase in the demand for self-cleaning and air purification solutions. Regulations and compliance issues, together with global standards, keep playing a role in pushing the uptake of these coatings in the construction, transportation, and consumer goods industry segments. A complete supply chain and distribution channel analysis identifies the key players involved in the process, together with logistic aspects in each geographical area. In the light of increasing sustainability concerns, the ecological footprint of such coatings is being studied increasingly by end-users focusing on pollution prevention and energy savings.

In August 2024, the MediaCo Group integrated a photocatalytic topcoat in retail advertising applications to combat climate change, partnering with Convergent Print Group and PURETi Group LLC to improve air quality by breaking down pollutants, representing the commercial direction of photocatalytic coating technology development toward new application categories beyond traditional construction whose pollutant-breakdown capability sustains expanding adoption across large-format printing and outdoor advertising through the forecast period.

Market Size and Forecast

-

Market Size in 2026E: USD 1.20 Billion

-

Market Size by 2035: USD 2.71 Billion

-

CAGR: 9.53% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Photocatalytic Coatings Market - Request Free Sample Report

Photocatalytic Coatings Market Trends

-

Increasing integration of photocatalytic coatings in green building certifications including LEED is driving structured demand across commercial and residential construction projects.

-

Growing municipal adoption of photocatalytic surfaces on roads and public infrastructure is creating new demand channels for pollutant-reducing and self-cleaning coating applications.

-

Rising research into visible-light activated photocatalysts is addressing UV-dependency limitations and expanding the coatings' commercial applicability to indoor and low-light environments.

-

Expanding solar panel self-cleaning coating adoption is improving energy efficiency and panel longevity, creating new demand from the renewable energy infrastructure sector.

-

Growing exploration of photocatalytic coatings in electric vehicle exterior and interior surfaces is creating emerging automotive sector demand for self-cleaning, low-maintenance solutions.

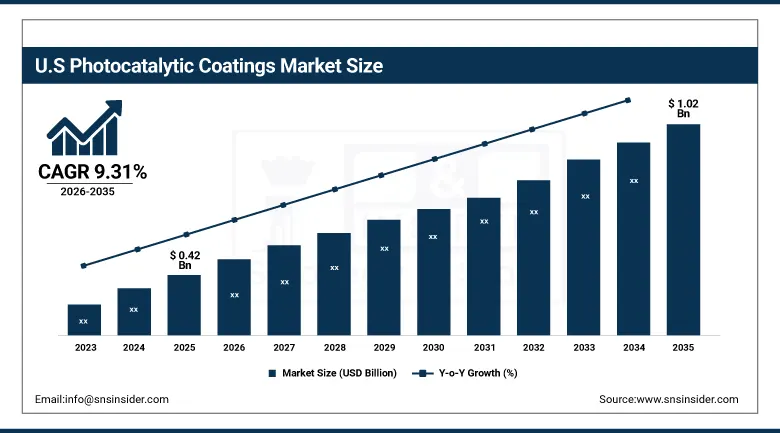

U.S. Photocatalytic Coatings Market Outlook

The U.S. Photocatalytic Coatings Market was valued at approximately USD 0.42 Billion in 2025 and is expected to reach approximately USD 1.02 Billion by 2035, growing at a CAGR of approximately 9.31%.

Growth in the U.S. Photocatalytic Coatings Market can be attributed to increasing environmental regulations and the need for eco-friendly solutions. The EPA encourages efforts for improving air quality, leading to the increase in usage of these coatings for air purification applications. Firms such as PURETi Group have made great strides towards developing self-cleaning solutions that are being used extensively in the construction sector. Green building standards such as the LEED and smart city programs have also contributed significantly to market growth. As cities aim at pollution prevention and energy conservation, these coatings become an important element of their strategy.

Municipalities in cities including Los Angeles and New York have deployed photocatalytic coatings on roads and public infrastructure to mitigate nitrogen oxide emissions, with the Los Angeles “smog-eating” walls project successfully demonstrating the effectiveness of Titanium Dioxide-based coatings in reducing urban pollution, representing the direction of U.S. photocatalytic coating development toward municipal infrastructure applications whose measurable pollution reduction benefits sustain expanding adoption through the 2025-2035 forecast period.

Photocatalytic Coatings Market Segment Analysis

-

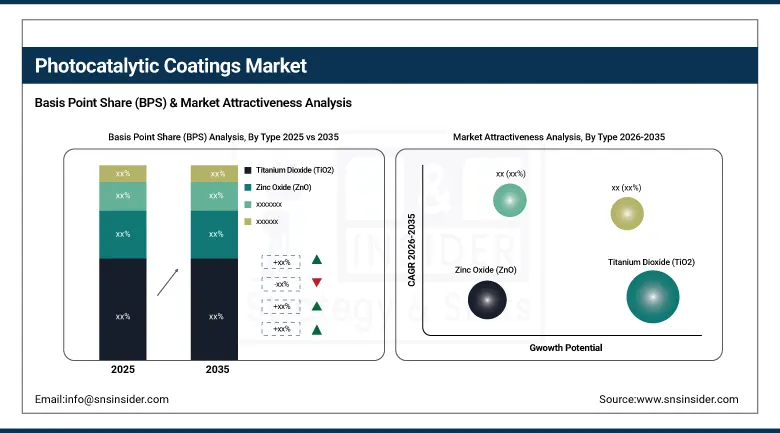

By Type, the Titanium Dioxide (TiO2) segment dominated the photocatalytic coatings market with approximately 58.2% share in 2025, owing to its exceptional photocatalytic efficiency, stability under UV light, and cost-effectiveness.

-

By Application, the Self-Cleaning segment dominated the photocatalytic coatings market with approximately 45.7% share in 2025, driven by the growing trend of smart buildings and sustainable urban infrastructure.

-

By End-use Industry, the Building & Construction segment dominated the photocatalytic coatings market with approximately 52.1% share in 2025, supported by increasing urbanization and strict environmental regulations.

By Type, Titanium Dioxide dominates the market

Titanium Dioxide (TiO2) held the largest market share in the photocatalytic coatings market of about 58.2% in 2025. The factors that drive Titanium Dioxide (TiO2)'s leadership are high efficiency, UV stability, and cost-effectiveness when compared to other materials. It is extensively used for self-cleaning, air purification, and antimicrobial coatings owing to its capability to decompose organic pollutants and harmful gases such as nitrogen oxides (NOx) and volatile organic compounds (VOCs). Its efficacy is recognized by regulatory authorities such as the U.S. EPA and ECHA to improve air quality and reduce emissions.

The major players in the industry have made significant investments in Titanium Dioxide-based coatings in construction materials, paints, and automobiles. Growing preference towards sustainable and maintenance-free building materials is also responsible for increasing demand for titanium dioxide coatings. Thus, it will remain as the dominant material in the market through the forecast period from 2025 to 2035.

By Application, Self-Cleaning dominates

The Self-Cleaning applications segment led the market in 2025 with a market share of around 45.7% in terms of volume. The increasing popularity of smart buildings and sustainable infrastructure has created strong demand for self-cleaning coating products. Self-cleaning coatings use Titanium Dioxide (TiO2) to react with sunlight in order to decompose dirt, organic contaminants, and other harmful materials in order to make cleaning easy. Government and regulatory organizations like the U.S. Department of Energy (DOE) are pushing self-cleaning solar panels for better energy efficiency.

Urban planners have adopted self-cleaning glass and concrete coatings for use in infrastructural projects that will help them save money on maintenance costs. Self-cleaning coating manufacturers have developed high-quality self-cleaning coatings that can be used by corporations for their commercial buildings, hospital facilities, and public transportation infrastructures. Emphasis on energy efficient buildings has played an important role in making self-cleaning applications dominate the market until 2035.

By End-use Industry, Building & Construction dominates

The Building & Construction segment was estimated to dominate the photocatalytic coating market in 2025 with a market share of around 52.1%. Urbanization, stricter environmental standards, and demand for sustainable infrastructure drive the growth of this market segment. Smart buildings, offices, commercial buildings, and other types of infrastructure use photocatalytic coatings because of self-cleaning and air purifying features of such technology. Various government agencies, such as the U.S. EPA and the U.S. Green Building Council, encourage the development of environmentally friendly and energy-efficient building materials.

Various large-scale infrastructure projects, including airports and skyscrapers, incorporate self-cleaning and air purification coatings into their structures in order to achieve higher sustainability and cut expenses for maintenance. The companies operate in development of high-quality construction grade photocatalytic coatings in order to provide long-lasting performance and improved air quality of modern buildings. Growth of market in the building & construction segment is fueled by the growing popularity of green building certifications.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

38.6% |

|

Europe |

Germany |

23.7% |

|

Asia Pacific |

China |

34.9% |

|

Middle East & Africa |

UAE |

28.4% |

|

Latin America |

Brazil |

36.8% |

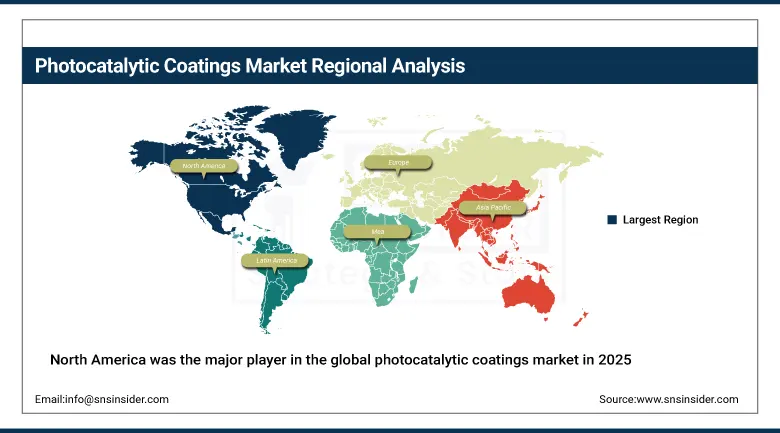

North America Photocatalytic Coatings Market Insights

North America was the major player in the global photocatalytic coatings market in 2025, accounting for around 38.6% market share due to strict environmental laws, infrastructural development, and the proliferation of smart cities initiatives. North America is dominated by the U.S., which has an emphasis on sustainable construction, air pollution laws, and technologies related to self-cleaning products. Both the U.S. EPA and the Department of Energy have been supporting the use of photocatalytic coatings in order to control volatile organic compounds (VOCs) and nitrogen oxide (NOx).

In terms of growth, Canada is considered to be the fastest growing country in North America in the field of photocatalytic coating technology due to their adoption in hospitals, residential buildings, and transport nodes. CaGBC has been actively working for the adoption of such technology in Canada. The U.S. solar energy industry has also adopted this technology for efficient solar panels.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Photocatalytic Coatings Market Insights

Europe commands about 23.7% of the revenue share from the region in 2025, owing to rigorous environmental regulations by EU, increased adoption of green building certification, and rising demand for sustainable building materials. The largest part of Europe’s revenue comes from Germany, due to the presence of efficient industrial coatings production facilities and investments made in sustainable building materials in the construction sector.

The other three important secondary markets in Europe include United Kingdom, France, and Netherlands, where green building investments and increasing infrastructure modernization ensure steady purchases of photocatalytic coatings.

Asia Pacific Photocatalytic Coatings Market Insights

Asia Pacific became the fastest-growing region within the market on account of rapid urbanization, growing pollution levels, and government efforts to develop smart infrastructure. Being the leading country in the region, China is propelling the market by virtue of growing construction industry, pollution control, and development of green buildings. The Ministry of Ecology and Environment of China has adopted stringent air quality norms that encourage the use of air purification coatings in urban areas. Approximately 34.9% of Asia Pacific revenues are accounted for by China.

India is experiencing growing demands for self-cleaning and antimicrobial coatings in the commercial and healthcare segments because of initiatives of the government, which include the Smart Cities Mission and Swachh Bharat Abhiyan. Japan is noted for technological innovations in nanomaterials and functional coatings and integrates photocatalytic coatings into transport infrastructure, ensuring its position as the fastest-growing regional market until 2035.

MEA & Latin America Photocatalytic Coatings Market Insights

The UAE is the leading market for MEA photocatalytic coatings revenues at approximately 28.4% of the regional purchasing due to its developed construction industry, development of smart cities infrastructure, and adoption of sustainable building materials. Smart cities initiatives in Saudi Arabia under the Vision 2030 will be the secondary revenue generator for MEA.

Brazil leads the Latin America revenues at approximately 36.8% due to its developing construction industry and increasing adoption of sustainable building materials. Argentina and Colombia are emerging secondary markets with the development of their construction industry maintaining high average regional procurement growth until 2035.

Market Dynamics

Drivers: Increasing government initiatives for sustainable infrastructure development drives the growth of the market

Sustainable development of infrastructure on the part of governments all over the world is a key factor propelling the market. Governments all over the world are showing interest in eco-friendly alternatives to combat pollution in their urban environments. The United States' Environmental Protection Agency (EPA) and the Department of Energy (DOE) encourage green buildings by introducing photocatalytic coatings in urban infrastructure projects. Photocatalytic coatings are self-cleaning and help to eliminate pollutants, and they are being used in LEED-certified buildings as well as smart city projects.

Photocatalytic coatings are being introduced in roads and infrastructure in cities such as Los Angeles and New York to minimize the effects of nitrogen oxides. Large government backing in this regard is helping the industry grow rapidly owing to increased awareness. Net-zero emission buildings and strict environmental regulations will increase the demand for photocatalytic coatings in the future.

Restraints: Limited consumer awareness and industry-specific knowledge hinders the growth of the photocatalytic coatings market

Although there are many advantages to using photocatalytic paints, the two problems associated with them are lack of consumer knowledge and lack of industry-specific knowledge about the product. Many possible users, including construction workers, car manufacturers, and consumers themselves, are not aware of the technology and the benefits of using it in the long run. Lack of education and marketing efforts is preventing the product from penetrating the market.

This paint differs from other coatings like anti-corrosive paint or anti-UV paint because one needs to understand the chemistry of how the coating works through photocatalysis. This is making it hard for the users to accept the product. Lack of performance metrics also adds to the challenge.

Opportunities: Integration of photocatalytic coatings in electric vehicle manufacturing creates new growth prospects for the market

The rising trend of electric vehicles (EVs) provides huge prospects for the Photocatalytic Coatings Market. With a quest for sustainable, maintenance-free, and cleaning applications, photocatalytic coatings are becoming an attractive choice for exterior and interior parts of automobiles. These coatings help in maintaining aesthetics and reducing the pollution level in and around the vehicles.

Automobile giants are seeking innovative technologies to increase the efficiency and durability of their products and this provides new opportunities for market growth. Moreover, the charging stations for EVs are being developed using these coatings to ensure cleanliness and reduction of environmental pollution levels. Future improvements in nanotechnology and materials would help in increasing the efficiency of these coatings and their use in the next generation of electric and autonomous cars up until 2035.

Recent Developments:

-

August 2024: The MediaCo Group integrated a photocatalytic topcoat in retail advertising to combat climate change. Partnering with Convergent Print Group and PURETi Group LLC, the initiative aimed to improve air quality by breaking down pollutants, setting a sustainability benchmark in large-format printing.

-

August 2023: Sparc Technologies filed a patent for advanced photocatalyst coatings to enhance green hydrogen production, focusing on improving solar-to-hydrogen efficiency and reducing costs in photocatalytic water-splitting reactors.

Photocatalytic Coatings Market Key Players

-

TOTO Ltd.

-

KON Corporation

-

Green Millennium

-

PURETi Group, LLC

-

Photocatalytic Coatings NZ Ltd.

-

Eco Active Solutions Ltd.

-

PPG Industries, Inc.

-

BASF SE

-

Akzo Nobel N.V.

-

The Sherwin-Williams Company

-

Nippon Paint Holdings Co., Ltd.

-

Kansai Paint Co., Ltd.

-

Daikin Industries, Ltd.

-

Kronos Worldwide, Inc.

-

Ishihara Sangyo Kaisha, Ltd.

-

Hempel A/S

-

Nanopool GmbH

Photocatalytic Coatings Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.09 Billion |

| Market Size by 2035 | USD 2.71 Billion |

| CAGR | CAGR of 9.53% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Titanium Dioxide (TiO2), Zinc Oxide (ZnO), Tungsten Trioxide (WO3), Others) • By Application (Self-Cleaning, Air Purification, Water Treatment, Anti-Fogging, Others) • By End-use Industry (Building & Construction, Healthcare, Transportation, Electronics & Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Mitsubishi Chemical Corporation, Saint-Gobain, TOTO Ltd., KON Corporation, USA Nanocoat, Green Millennium, PURETi Group, LLC, Photocatalytic Coatings NZ Ltd., Eco Active Solutions Ltd., PPG Industries, Inc., BASF SE, Akzo Nobel N.V., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Daikin Industries, Ltd., Kronos Worldwide, Inc., Ishihara Sangyo Kaisha, Ltd., Hempel A/S, and Nanopool GmbH. |

Frequently Asked Questions

The Photocatalytic Coatings Market is expected to grow at a CAGR of 9.53% from 2026 to 2035.

The Photocatalytic Coatings Market was valued at USD 1.09 Billion in 2025.

The growing emphasis on sustainable infrastructure development by governments worldwide, increasing demand for self-cleaning and air-purifying technologies, and rising adoption of green building certifications including LEED are the primary growth factors driving the Photocatalytic Coatings Market.

Titanium Dioxide (TiO2) dominated the Photocatalytic Coatings Market in 2025 with approximately 58.2% market share, owing to its exceptional photocatalytic efficiency and cost-effectiveness.

North America dominated the Photocatalytic Coatings Market in 2025 with a market share of approximately 38.6%, while Asia Pacific emerged as the fastest-growing region during the forecast period.

Get in Touch