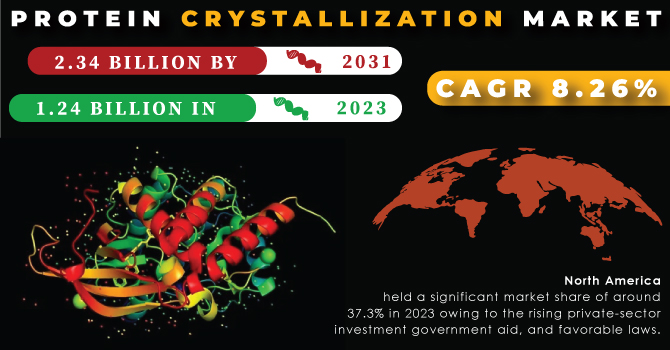

The Protein Crystallization Market size was estimated USD 1.24 billion in 2023 and is expected to reach USD 2.34 billion by 2031 at a CAGR of 8.26% during the forecast period of 2024-2031.

Protein crystallization is the process of creating protein crystals from a solution that is supersaturated in the macromolecule but does not disrupt its normal state. Protein crystallization is the creation of an orderly array of individual protein molecules in the form of crystals. These protein crystals are made for scientific and industrial uses, primarily for X-ray crystallography research.

Get More Information on Protein Crystallization Market - Request Sample Report

Several developing proteomics players are receiving financing and investments in order to advance proteomics applications. For example, in January 2023, Evosep, a proteomics technology business, obtained a USD 40 million investment from Novo Holdings to develop a high-throughput proteomics solution. Furthermore, various investments under government initiatives are growing the use of protein crystallization in proteomics research and development.

DRIVERS

Increasing demand for protein therapeutics

Protein treatments have become an important aspect of the healthcare industry in recent years. Protein treatments are frequently used to treat a variety of serious diseases, including cancer, due to their low immunogenicity and specificity. The execution of expansion strategies by manufacturers to secure the biggest market share in response to increased demand for protein-based medications and therapies will boost market growth. In January 2022, for example, Amgen and Generate Biomedicines cooperated to find and develop protein therapeutics for five targets across multiple treatment modalities and therapeutic domains. As a result, rising demand for protein therapies, as well as leading industry players' strategies, will drive market growth over the forecast period.

RESTRAIN

Protein crystallization complexity

Both X-ray crystallography and formulation development require high-quality protein crystals; this difficult process begins with a pure, highly concentrated protein sample in solution. In an ideal world, the liquid component of the solution gradually evaporates, leaving protein crystals in its stead. For some proteins, this technique routinely produces high-quality crystals. For example, crystalline insulin is used as a long-acting insulin substitute. Producing high-quality crystals from other proteins is significantly more difficult.

OPPORTUNITY

Technological progress

Technological advancements in crystallization methods, such as cell-free protein crystallization methods, are expected to give appealing market opportunities during the forecast period. Scientists at the Tokyo Institute of Technology, for example, developed a groundbreaking cell-free protein crystallization process in October 2022. The method adds greatly to structural biology improvements by permitting the analysis of unstable proteins that cannot be explored using other traditional approaches. Such advancements promote the development of novel and improved protein crystal treatments for a wide range of ailments, including cancer and muscular dystrophy.

CHALLENGES

Maintaining their stability throughout the crystallization process

Proteins are not inherently crystallizable substances and inherently complicated and sensitive substances. Maintaining its stability during the crystallization process might be a difficult task in the protein crystallization business. Temperature, pH, protein concentration, and other factors affect protein stability and cause aggregation or denaturation, which can disrupt crystals. As a result, maintaining the proper environment has become a difficult issue in the protein crystallization business. Obtaining adequate quantities of pure and high-quality protein samples might be another issue, particularly for membrane proteins or protein complexes.

The Russian Ukraine war influence on many aspects of daily life, including a considerable load on the healthcare system, and is particularly affecting research trials. Clinical trials are a set of events in which patients are screened, recruited, dossed, followed-up, tracked, and monitored to test the safety and efficacy of a medicine in patients, and regulatory organizations give approvals based on the data acquired. Ukraine has been a popular location for clinical trials because it has a well-established centralized healthcare system that allows pharmaceutical companies to recruit more easily and quickly. Furthermore, Ukraine has a substantial number of treatment-naive patients as well as GCP-compliant workforce and infrastructure. With the conflict still going on, there are numerous circumstances affecting the entire clinical trials system, including the unavailability of new and ongoing patients, as well as a blocked supply chain, which will and has damaged the whole pharmaceutical sector.

IMPACT OF ECONOMIC DOWNTURN

Economic downturns or recessions have a negative impact on our operating results since our customers frequently reduce or postpone capital expenditures. Customers may potentially acquire lower-cost products from competitors and not return to us even if economic conditions improve. These circumstances would lower our revenues and profits. Furthermore, a worldwide financial crisis affecting financial institutions would most likely have a negative impact on global capital markets and our industry.

By Product

Instruments

Liquid Handling Instruments

Crystal Imaging Instruments

Consumables

Reagents & Kits/Screens

Micro Plates

Others

Software & Services

In 2023, Consumables segment is expected to held the highest market share of 67.2% during the forecast period due to consumables include reagents and kits/screens, microplates, and other products used to support crystallization processes. Protein crystallization kits offer an efficient screening tool for establishing the ideal solubility conditions for protein crystallization. These kits also include the chemicals needed for fast screening to find the optimal conditions for crystallization of purified protein samples.

By Technology

X-ray Crystallography

Cryo-electron Microscopy

NMR Spectroscopy

Others

In 2023, the X-ray Crystallography segment is expected to dominate the market growth of 53.5% during the forecast period due to X-ray crystallography is the most often used technique for determining the structure of biological macromolecules and proteins. It entails crystallizing proteins, bombarding them with X-rays, and reconstructing their structure based on the tell-tale patterns of diffracted light that occur. The method has various advantages, including a two-dimensional image that indicates the three-dimensional structure of a protein. Furthermore, X-ray crystallography is generally easy and inexpensive, gives superior diffraction, reduces radiation damage to crystals, and allows for safe crystal storage, transit, and reuse. These technological skills are strengthening the segment.

By End User

Pharmaceutical and Biotechnology Companies

Academic and Research Institutes

In 2023, Pharmaceutical and Biotechnology Companies segment is expected to dominate the market growth of 71.7% during the forecast period to due to the Protein crystallization technologies play two important functions in structural biology: in silico drug design and controlled drug discovery. Protein crystallography in silico drug design determines a molecule's 3-D structure. Protein crystal formation resulted in more precise 3-D protein structures. These high-quality crystals may eventually lead to a better understanding of biological function and improved drug creation in pharmaceutical and biotechnology companies.

North America held a significant market share of around 37.3% in 2023 owing to the rising private-sector investment, government aid, and favorable laws. The region is primarily focused on drug development and proteome structure prediction research, which is pushing market expansion. The presence of innovators and important operational players has resulted in greater product penetration in the region.

Asia-Pacific is witness to expand fastest CAGR rate during the forecast period due to the rapid expansion of emerging economies such as China and India's pharmaceutical and biotechnology industries. This region's profitable expansion can also be attributed to continued government backing for the development of the pharmaceutical sector in developing countries. Furthermore, continuing research in the realms of cancer and infectious diseases such as COVID-19 is likely to boost significant growth in the region's protein crystallization market.

REGIONAL COVERAGE

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are FORMULATRIX, Rigaku Corporation, METTLER TOLEDO, Greiner Bio-One International GmbH, Corning Incorporated, HAMPTON RESEARCH CORP, Jena Bioscience GmbH, Bruker,Molecular Dimensions, Creative Proteomics, and Others.

METTLER TOLEDO, in July 2022, METTLER TOLEDO announced plans to expand its manufacturing facilities in Vacaville, California. This initiative is designed to strengthen the company's protein crystallization capabilities in Vacaville.

Bruker Corporation, in March 2021, Bruker Corporation announced the launch of new plasma proteomics software, PaSER software v.1.1, which will allow “run & done” high-throughput 4D proteomics with immediate availability of identified peptides and protein groups after the experiment is done. In the same announcement, the company unveiled new consumables and software for chemical cross linking of proteins to study protein structure and interactions.

| Report Attributes | Details |

| Market Size in 2023 | US$ 1.24 Billion |

| Market Size by 2031 | US$ 2.34 Billion |

| CAGR | CAGR of 8.26 % From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Instruments, Consumables, Software & Services) • By Technology (X-ray Crystallography, Cryo-electron Microscopy, NMR Spectroscopy, Others) • By End User (Pharmaceutical and Biotechnology Companies, Academic and Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | FORMULATRIX, Rigaku Corporation, METTLER TOLEDO, Greiner Bio-One International GmbH, Corning Incorporated, HAMPTON RESEARCH CORP, Jena Bioscience GmbH, Bruker,Molecular Dimensions, Creative Proteomics, |

| Key Drivers | • Increasing demand for protein therapeutics |

| Market Opportunity | • Technological progress |

Ans: Protein Crystallization Market size was valued at USD 1.24 billion in 2023.

Ans: Protein Crystallization Market is anticipated to expand by 8.26% from 2024 to 2031.

Ans: USD 2.34 billion is expected to grow by 2031.

Ans: Rising demand for protein therapeutics.

Ans: Maintaining their stability during the process of crystallization.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Protein Crystallization Market Segmentation, By Product

9.1 Introduction

9.3 Instruments

9.3.1 Liquid Handling Instruments

9.3.2 Crystal Imaging Instruments

9.4 Consumables

9.4.1Reagents & Kits/Screens

9.4.2 Micro Plates

9.4.3 Others

9.5 Software & Services

10. Protein Crystallization Market Segmentation, By Technology

10.2 Trend Analysis

10.3 X-ray Crystallography

10.4 Cryo-electron Microscopy

10.5 NMR Spectroscopy

11. Protein Crystallization Market Segmentation, By End user

11.1 Introduction

11.3 Pharmaceutical and Biotechnology Companies

11.4 Academic and Research Institutes

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 Trend Analysis

12.2.2 North America Protein Crystallization Market by Country

12.2.3 North America Protein Crystallization Market By Product

12.2.4 North America Protein Crystallization Market By Technology

12.2.5 North America Protein Crystallization Market By End user

12.2.6 USA

12.2.6.1 USA Protein Crystallization Market By Product

12.2.6.2 USA Protein Crystallization Market By Technology

12.2.6.3 USA Protein Crystallization Market By End user

12.2.7 Canada

12.2.7.1 Canada Protein Crystallization Market By Product

12.2.7.2 Canada Protein Crystallization Market By Technology

12.2.7.3 Canada Protein Crystallization Market By End user

12.2.8 Mexico

12.2.8.1 Mexico Protein Crystallization Market By Product

12.2.8.2 Mexico Protein Crystallization Market By Technology

12.2.8.3 Mexico Protein Crystallization Market By End user

12.3 Europe

12.3.1 Trend Analysis

12.3.2 Eastern Europe

12.3.2.1 Eastern Europe Protein Crystallization Market by Country

12.3.2.2 Eastern Europe Protein Crystallization Market By Product

12.3.2.3 Eastern Europe Protein Crystallization Market By Technology

12.3.2.4 Eastern Europe Protein Crystallization Market By End user

12.3.2.5 Poland

12.3.2.5.1 Poland Protein Crystallization Market By Product

12.3.2.5.2 Poland Protein Crystallization Market By Technology

12.3.2.5.3 Poland Protein Crystallization Market By End user

12.3.2.6 Romania

12.3.2.6.1 Romania Protein Crystallization Market By Product

12.3.2.6.2 Romania Protein Crystallization Market By Technology

12.3.2.6.4 Romania Protein Crystallization Market By End user

12.3.2.7 Hungary

12.3.2.7.1 Hungary Protein Crystallization Market By Product

12.3.2.7.2 Hungary Protein Crystallization Market By Technology

12.3.2.7.3 Hungary Protein Crystallization Market By End user

12.3.2.8 Turkey

12.3.2.8.1 Turkey Protein Crystallization Market By Product

12.3.2.8.2 Turkey Protein Crystallization Market By Technology

12.3.2.8.3 Turkey Protein Crystallization Market By End user

12.3.2.9 Rest of Eastern Europe

12.3.2.9.1 Rest of Eastern Europe Protein Crystallization Market By Product

12.3.2.9.2 Rest of Eastern Europe Protein Crystallization Market By Technology

12.3.2.9.3 Rest of Eastern Europe Protein Crystallization Market By End user

12.3.3 Western Europe

12.3.3.1 Western Europe Protein Crystallization Market by Country

12.3.3.2 Western Europe Protein Crystallization Market By Product

12.3.3.3 Western Europe Protein Crystallization Market By Technology

12.3.3.4 Western Europe Protein Crystallization Market By End user

12.3.3.5 Germany

12.3.3.5.1 Germany Protein Crystallization Market By Product

12.3.3.5.2 Germany Protein Crystallization Market By Technology

12.3.3.5.3 Germany Protein Crystallization Market By End user

12.3.3.6 France

12.3.3.6.1 France Protein Crystallization Market By Product

12.3.3.6.2 France Protein Crystallization Market By Technology

12.3.3.6.3 France Protein Crystallization Market By End user

12.3.3.7 UK

12.3.3.7.1 UK Protein Crystallization Market By Product

12.3.3.7.2 UK Protein Crystallization Market By Technology

12.3.3.7.3 UK Protein Crystallization Market By End user

12.3.3.8 Italy

12.3.3.8.1 Italy Protein Crystallization Market By Product

12.3.3.8.2 Italy Protein Crystallization Market By Technology

12.3.3.8.3 Italy Protein Crystallization Market By End user

12.3.3.9 Spain

12.3.3.9.1 Spain Protein Crystallization Market By Product

12.3.3.9.2 Spain Protein Crystallization Market By Technology

12.3.3.9.3 Spain Protein Crystallization Market By End user

12.3.3.10 Netherlands

12.3.3.10.1 Netherlands Protein Crystallization Market By Product

12.3.3.10.2 Netherlands Protein Crystallization Market By Technology

12.3.3.10.3 Netherlands Protein Crystallization Market By End user

12.3.3.11 Switzerland

12.3.3.11.1 Switzerland Protein Crystallization Market By Product

12.3.3.11.2 Switzerland Protein Crystallization Market By Technology

12.3.3.11.3 Switzerland Protein Crystallization Market By End user

12.3.3.1.12 Austria

12.3.3.12.1 Austria Protein Crystallization Market By Product

12.3.3.12.2 Austria Protein Crystallization Market By Technology

12.3.3.12.3 Austria Protein Crystallization Market By End user

12.3.3.13 Rest of Western Europe

12.3.3.13.1 Rest of Western Europe Protein Crystallization Market By Product

12.3.3.13.2 Rest of Western Europe Protein Crystallization Market By Technology

12.3.3.13.3 Rest of Western Europe Protein Crystallization Market By End user

12.4 Asia-Pacific

12.4.1 Trend Analysis

12.4.2 Asia-Pacific Protein Crystallization Market by Country

12.4.3 Asia-Pacific Protein Crystallization Market By Product

12.4.4 Asia-Pacific Protein Crystallization Market By Technology

12.4.5 Asia-Pacific Protein Crystallization Market By End user

12.4.6 China

12.4.6.1 China Protein Crystallization Market By Product

12.4.6.2 China Protein Crystallization Market By Technology

12.4.6.3 China Protein Crystallization Market By End user

12.4.7 India

12.4.7.1 India Protein Crystallization Market By Product

12.4.7.2 India Protein Crystallization Market By Technology

12.4.7.3 India Protein Crystallization Market By End user

12.4.8 Japan

12.4.8.1 Japan Protein Crystallization Market By Product

12.4.8.2 Japan Protein Crystallization Market By Technology

12.4.8.3 Japan Protein Crystallization Market By End user

12.4.9 South Korea

12.4.9.1 South Korea Protein Crystallization Market By Product

12.4.9.2 South Korea Protein Crystallization Market By Technology

12.4.9.3 South Korea Protein Crystallization Market By End user

12.4.10 Vietnam

12.4.10.1 Vietnam Protein Crystallization Market By Product

12.4.10.2 Vietnam Protein Crystallization Market By Technology

12.4.10.3 Vietnam Protein Crystallization Market By End user

12.4.11 Singapore

12.4.11.1 Singapore Protein Crystallization Market By Product

12.4.11.2 Singapore Protein Crystallization Market By Technology

12.4.11.3 Singapore Protein Crystallization Market By End user

12.4.12 Australia

12.4.12.1 Australia Protein Crystallization Market By Product

12.4.12.2 Australia Protein Crystallization Market By Technology

12.4.12.3 Australia Protein Crystallization Market By End user

12.4.13 Rest of Asia-Pacific

12.4.13.1 Rest of Asia-Pacific Protein Crystallization Market By Product

12.4.13.2 Rest of Asia-Pacific Protein Crystallization Market By Technology

12.4.13.3 Rest of Asia-Pacific Protein Crystallization Market By End user

12.5 Middle East & Africa

12.5.1 Trend Analysis

12.5.2 Middle East

12.5.2.1 Middle East Protein Crystallization Market by Country

12.5.2.2 Middle East Protein Crystallization Market By Product

12.5.2.3 Middle East Protein Crystallization Market By Technology

12.5.2.4 Middle East Protein Crystallization Market By End user

12.5.2.5 UAE

12.5.2.5.1 UAE Protein Crystallization Market By Product

12.5.2.5.2 UAE Protein Crystallization Market By Technology

12.5.2.5.3 UAE Protein Crystallization Market By End user

12.5.2.6 Egypt

12.5.2.6.1 Egypt Protein Crystallization Market By Product

12.5.2.6.2 Egypt Protein Crystallization Market By Technology

12.5.2.6.3 Egypt Protein Crystallization Market By End user

12.5.2.7 Saudi Arabia

12.5.2.7.1 Saudi Arabia Protein Crystallization Market By Product

12.5.2.7.2 Saudi Arabia Protein Crystallization Market By Technology

12.5.2.7.3 Saudi Arabia Protein Crystallization Market By End user

12.5.2.8 Qatar

12.5.2.8.1 Qatar Protein Crystallization Market By Product

12.5.2.8.2 Qatar Protein Crystallization Market By Technology

12.5.2.8.3 Qatar Protein Crystallization Market By End user

12.5.2.9 Rest of Middle East

12.5.2.9.1 Rest of Middle East Protein Crystallization Market By Product

12.5.2.9.2 Rest of Middle East Protein Crystallization Market By Technology

12.5.2.9.3 Rest of Middle East Protein Crystallization Market By End user

12.5.3 Africa

12.5.3.1 Africa Protein Crystallization Market by Country

12.5.3.2 Africa Protein Crystallization Market By Product

12.5.3.3 Africa Protein Crystallization Market By Technology

12.5.3.4 Africa Protein Crystallization Market By End user

12.5.3.5 Nigeria

12.5.3.5.1 Nigeria Protein Crystallization Market By Product

12.5.3.5.2 Nigeria Protein Crystallization Market By Technology

12.5.3.5.3 Nigeria Protein Crystallization Market By End user

12.5.3.6 South Africa

12.5.3.6.1 South Africa Protein Crystallization Market By Product

12.5.3.6.2 South Africa Protein Crystallization Market By Technology

12.5.3.6.3 South Africa Protein Crystallization Market By End user

12.5.3.7 Rest of Africa

12.5.3.7.1 Rest of Africa Protein Crystallization Market By Product

12.5.3.7.2 Rest of Africa Protein Crystallization Market By Technology

12.5.3.7.3 Rest of Africa Protein Crystallization Market By End user

12.6 Latin America

12.6.1 Trend Analysis

12.6.2 Latin America Protein Crystallization Market by country

12.6.3 Latin America Protein Crystallization Market By Product

12.6.4 Latin America Protein Crystallization Market By Technology

12.6.5 Latin America Protein Crystallization Market By End user

12.6.6 Brazil

12.6.6.1 Brazil Protein Crystallization Market By Product

12.6.6.2 Brazil Protein Crystallization Market By Technology

12.6.6.3 Brazil Protein Crystallization Market By End user

12.6.7 Argentina

12.6.7.1 Argentina Protein Crystallization Market By Product

12.6.7.2 Argentina Protein Crystallization Market By Technology

12.6.7.3 Argentina Protein Crystallization Market By End user

12.6.8 Colombia

12.6.8.1 Colombia Protein Crystallization Market By Product

12.6.8.2 Colombia Protein Crystallization Market By Technology

12.6.8.3 Colombia Protein Crystallization Market By End user

12.6.9 Rest of Latin America

12.6.9.1 Rest of Latin America Protein Crystallization Market By Product

12.6.9.2 Rest of Latin America Protein Crystallization Market By Technology

12.6.9.3 Rest of Latin America Protein Crystallization Market By End user

13. Company Profiles

13.1 Rigaku Corporation

13.1.1 Company Overview

13.1.2 Financial

13.1.3 Product/ Services Offered

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 METTLER TOLEDO

13.2.1 Company Overview

13.2.2 Financial

13.2.3 Product / Services Offered

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 FORMULATRIX

13.3.1 Company Overview

13.3.2 Financial

13.3.3 Product / Services Offered

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 Corning Incorporated

13.4.1 Company Overview

13.4.2 Financial

13.4.3 Product / Services Offered

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 Greiner Bio-One International GmbH

13.5.1 Company Overview

13.5.2 Financial

13.5.3 Product/ Services Offered

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 HAMPTON RESEARCH CORP

13.6.1 Company Overview

13.6.2 Financial

13.6.3 Product/ Services Offered

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 Jena Bioscience GmbH

13.7.1 Company Overview

13.7.2 Financial

13.7.3 Product/ Services Offered

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8.1 Company Overview

13.8.2 Financial

13.8.3 Product/ Services Offered

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 Creative Proteomics

13.9.1 Company Overview

13.9.2 Financial

13.9.3 Product/ Services Offered

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 Molecular Dimensions

13.10.1 Company Overview

13.10.2 Financial

13.10.3 Product/ Services Offered

13.10.4 SWOT Analysis

13.10.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3.3 Mergers & Acquisitions

15. Use Case and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Report Scope & Overview: The Infusion Pump Software Market Size was valued at USD 924.28 million in 2022 and is expected to reach USD 1660 million by 2030 and grow at a CAGR of 7.6% over the forecast period 2023-2030.

The pharma 4.0 is very much focused on data integrity, robotics, automation and so forth. The use of the data is been done to analyse the quality control and user feedback which will eventually help the key players in revising their products and services.

The Molecular Quality Controls Market size was estimated USD 0.17 billion in 2022 and is expected to reach USD 0.28 billion by 2030 at a CAGR of 6.8% during the forecast period of 2023-2030.

The Patient Handling Equipment Market size was estimated USD 13,241 million in 2022 and is expected to reach USD 18974.67 million By 2030 at a CAGR of 4.6 % during the forecast period of 2023-2030.

The Dual Chamber Prefilled Syringes Market size was USD 154.21 million in 2022 and is expected to Reach USD 268.56 million by 2030 and grow at a CAGR of 7.08 % over the forecast period of 2023-2030.

The Antibiotics Market size is valued at USD 49.51 Bn in 2022 and is expected to reach USD 68.22 Bn by 2030 and grow at a CAGR of 4.09% over the forecast period of 2023-2030.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd