Allergy Treatment Market Report Scope & Overview:

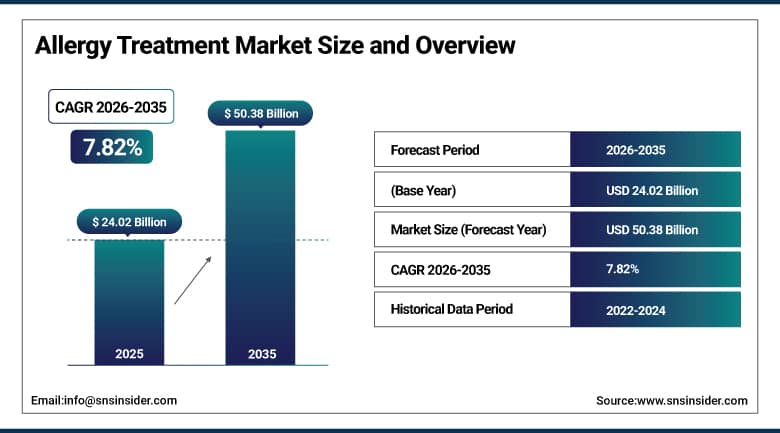

The Allergy Treatment Market was valued at USD 24.02 Billion in 2025 and is expected to reach USD 50.38 Billion by 2035, growing at a CAGR of 7.82% from 2026 to 2035.

Allergy treatment covers a wide therapeutic area that deals with the diagnosis, management and long-term control of immunological hypersensitivity reactions that together affect a large proportion of the world’s population across respiratory, dermatological, gastrointestinal and systemic clinical presentations. The global allergy treatment market has witnessed strong growth momentum due to rising global prevalence of allergic conditions, which is attributed to urbanisation, changing environmental exposures, increased air pollution, dietary transitions, and the hygiene hypothesis that links reduced microbial exposure in early life with increased rates of allergic sensitisation in developed and developing economies alike. Through pharmaceutical innovation, allergy treatment has evolved from first-generation antihistamines to targeted biologics, leading to better disease control and tolerability for moderate-to-severe allergy.

Sanofi and Regeneron's dupilumab (Dupixent) recorded global net sales exceeding USD 11 billion in 2024, with allergy-related indications including atopic dermatitis, asthma, and chronic rhinosinusitis with nasal polyps collectively representing the core revenue base and ongoing label expansion applications targeting additional allergic conditions sustaining the product's long-term commercial growth trajectory. Childhood asthma remains a major segment of global disease burden, with 95–120 million children affected worldwide, though age-standardized rates have gradually declined over time due to improved management

Market Size and Forecast

-

Market Size in 2026E: USD 25.59 Billion

-

Market Size by 2035: USD 50.38 Billion

-

CAGR: 7.82% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Allergy Treatment Market - Request Free Sample Report

Allergy Treatment Market Trends

-

-

Rising biologics and targeted therapies are improving treatment of severe asthma, dermatitis, and chronic rhinosinusitis.

-

Sublingual immunotherapy adoption is increasing, supporting better adherence and home-based care.

-

Growing food allergy burden is driving oral and epicutaneous immunotherapy development.

-

AI and digital tools are enhancing diagnosis accuracy and enabling personalized allergy care.

-

Expanding awareness and testing are increasing diagnosis rates in emerging APAC and Latin American markets.

-

The U.S. Allergy Treatment Market Outlook

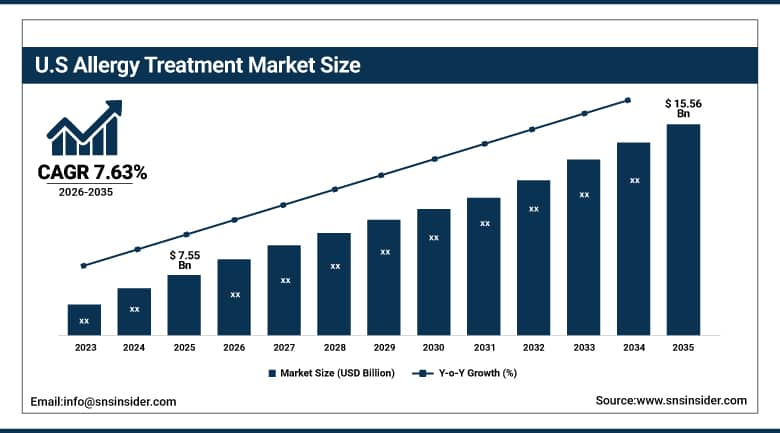

The U.S. Allergy Treatment Market was valued at USD 7.55 Billion in 2025 and is expected to reach USD 15.56 Billion by 2035, growing at a CAGR of 7.63%.

The U.S. is the largest national allergy treatment market in the world, supported by the highest per-capita healthcare spending, the largest number of allergy and immunology specialist physicians, a mature payer landscape that has increasingly supported reimbursement of biologic therapies, and a regulatory environment that has enabled both accelerated approval of novel allergy therapeutics and label expansions for existing therapies.

Allergic disease burden in the United States is substantial, with allergic rhinitis affecting an estimated 60 million Americans, asthma affecting >25 million individuals, and food allergies emerging as an increasing clinical and public health challenge across paediatric and adult populations. The move from symptom management to biologics and immunotherapy is increasing revenue per patient and growing faster than the disease incidence.

50 million Americans experience some form of allergy annually, making allergic disease the sixth leading cause of chronic illness in the United States and generating over USD 8 billion in direct healthcare costs including physician visits, medications, and emergency care attributable to allergic reactions each year. In developed and urban regions, allergy prevalence trends are consistently higher due to air pollution, lifestyle factors, and reduced early-life immune exposure, reinforcing the “allergy epidemic” pattern globally.

Allergy Treatment Market Segment Analysis

-

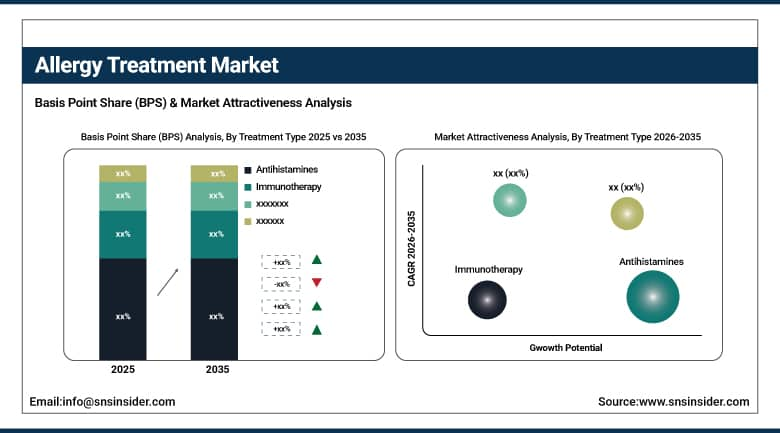

By Treatment Type, antihistamines dominated the market with 32.06% share in 2025, while immunotherapy is the fastest growing treatment type with the highest CAGR of 8.56% from 2026 to 2035.

-

By Allergy Type, respiratory allergies dominated the market with 48.15% share in 2025, while food allergies are the fastest growing allergy type with the highest CAGR of 8.73% from 2026 to 2035.

-

By Route of Administration, oral route dominated the market with 46.06% share in 2025, while sublingual route is the fastest growing with the highest CAGR of 9.65% from 2026 to 2035.

-

By End User, hospitals dominated the market with 34.15% share in 2025, while homecare settings are the fastest growing end user segment with the highest CAGR of 8.51% from 2026 to 2035.

By Treatment Type, antihistamines dominate the allergy treatment market, while immunotherapy is the fastest-growing segment.

The antihistamines segment dominated the market with the highest revenue share of 32.06% in 2025 due to their broad clinical applicability across allergic rhinitis, urticaria, conjunctivitis and other common allergic conditions, extensive over-the-counter availability, well-established safety profiles and strong physician and patient familiarity developed over decades of widespread use. The presence of non-sedating second generation antihistamines including cetirizine, loratadine and fexofenadine in both branded and generic forms are driving high market penetration across socioeconomic groups globally. Newer generation formulations are also continuing to increase market value through premium pricing in developed markets.

The immunotherapy segment is expected to register a CAGR of 8.56% during 2026-2035 owing to increasing clinical evidence base for long-term disease modification through allergen desensitisation, growing confidence of physicians in subcutaneous as well as sublingual formats, and development of standardised allergen extracts and proprietary formulations that are improving treatment consistency and commercial scalability. The expansion of food allergy immunotherapy programs, the ongoing development of epicutaneous and oral desensitisation platforms for peanut and other high-prevalence food allergens, and the growing awareness of the value of immunotherapy versus lifelong symptomatic pharmacotherapy are expanding the addressable patient population in key markets.

By Allergy Type, respiratory allergies dominate the allergy treatment market, while food allergies are the fastest-growing segment.

The respiratory allergies segment of the market contributed the largest share of revenue, 48.15% in 2025. This is due to the high global prevalence of allergic rhinitis and allergic asthma, the complexity and chronicity of disease management that leads to sustained consumption of pharmaceuticals across antihistamine, corticosteroid, leukotriene antagonist, and biologic treatment categories, and the disproportionately large share of high-cost biologic therapies used in moderate-to-severe respiratory allergic disease. The World Health Organization estimates that over 400 million people around the world have allergic rhinitis, which makes respiratory allergies the largest allergy category by far in terms of patient numbers and generates consistent demand across the entire range of treatment types, from over-the-counter symptomatic agents to specialist-administered biologic therapies.

The food allergies segment is projected to see the highest CAGR of 8.73% in 2026–2035, fuelled by the increasing global prevalence of food allergies, the rapid clinical development and commercialisation of oral immunotherapy products following the FDA approval of Palforzia for peanut allergy, and the significant unmet clinical need among patients who have historically been limited to allergen avoidance and emergency epinephrine provision for their management. In addition to peanut, the growing pipeline of desensitisation therapies for tree nut, milk and wheat allergens presents a significant near-term market expansion opportunity that should drive above average revenue growth in the food allergy treatment category over the forecast period.

By Route of Administration, oral route dominates the allergy treatment market, while sublingual route is the fastest-growing segment.

The oral route segment held the largest market share of around 46.06% in 2025, owing to easy availability of oral antihistamine, corticosteroid, leukotriene antagonist, and decongestant formulations via prescription and over-the-counter channels worldwide, along with high patient preference for oral medication formats that do not require clinical administration and facilitate self-management of allergic symptoms across outpatient and home settings. The oral dosage form remains the market leader throughout the forecast period due to its compatibility with the most prescribed and highest volume allergy drug classes, even with the above-average growth of alternative administration routes.

The fastest growing segment of sublingual route with a CAGR of 9.65% during the forecast period of 2026-2035 is attributed to the regulatory approval and commercialisation of standardised sublingual immunotherapy tablets for grass pollen, house dust mite, and tree pollen allergens in major markets, the patient and physician preference for home-based administration over clinic-based subcutaneous injection protocols, and the ongoing clinical development of sublingual oral immunotherapy formulations for food allergy desensitisation. The safety benefit of sublingual administration over subcutaneous immunotherapy, which minimises the risk of systemic reactions and can be administered at home, is slowly widening the eligible patient population for allergen immunotherapy.

By End User, hospitals dominate the allergy treatment market, while homecare settings are the fastest-growing segment.

Hospitals segment accounted for the largest revenue share of around 34.15% in 2025 due to the availability of specialist allergy and immunology services, allergy testing infrastructure, biologic therapy administration, and emergency anaphylaxis management capabilities in hospital settings which capture the highest-acuity and highest-value allergy treatment encounters. Although the dispensing of allergy medications in outpatient and retail pharmacies is high, the lower revenue per visit helps hospitals maintain their share of the allergy treatment market through their administration of injectable biologic therapies such as dupilumab, omalizumab, and mepolizumab in the outpatient hospital and day treatment setting.

The homecare settings segment is expected to grow at the highest CAGR of 8.51% during the forecast period (2026–2035) owing to the increasing availability of self-injectable biologic therapies with home administration approval, increasing adoption of sublingual immunotherapy programs allowing home-based allergen desensitisation, and the trend in the healthcare system to decentralise chronic disease management from institutional settings to home settings facilitated by telehealth platforms, remote monitoring tools, and patient education programs. The “convenience” benefit of home-based allergy management is particularly compelling in chronic allergy conditions requiring frequent medication administration, where the reduction in clinic visit burden substantially improves long-term patient adherence to treatment protocols.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.84% |

|

Europe |

Germany |

33.45% |

|

Asia Pacific |

China |

42.25% |

|

Latin America |

Brazil |

45.37% |

|

Middle East & Africa |

UAE |

32.68% |

North America Allergy Treatment Market Insights

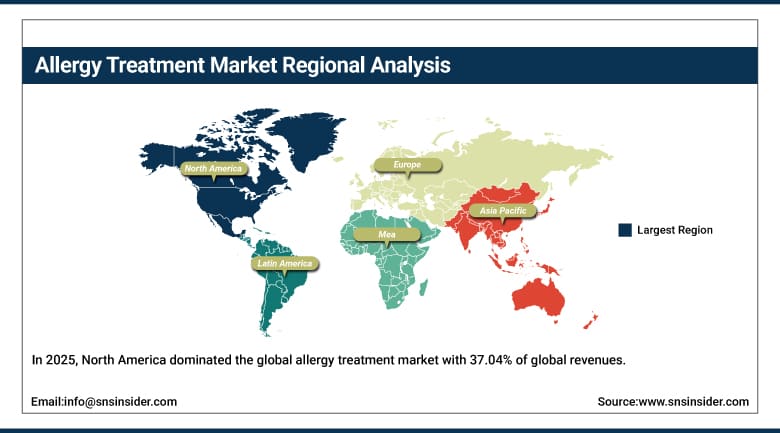

In 2025, North America dominated the global allergy treatment market with 37.04% of global revenues, with the United States accounting for 84.84% of regional revenues. The region's market-leading position results from the highest per-capita rates of biologic therapy adoption globally, a favourable reimbursement environment facilitating broad patient access to high-cost targeted allergy treatments, a large and well-resourced allergy and immunology specialist community, and a sophisticated pharmaceutical commercial infrastructure that enables rapid uptake of novel therapeutic approvals. Commercially successful IL-4/IL-13 pathway-targeting biologic therapies have elevated the standard of care and average treatment cost in atopic dermatitis and asthma, and have been particularly transformative for the U.S. market, contributing disproportionately to revenue growth relative to patient volume expansion.

Canada has additional demand arising from the progressive inclusion of biologic allergy therapies on provincial formularies within its universal healthcare system, increased awareness of food allergy management options following regulatory approvals similar to U.S. FDA decisions, and the country’s existing allergy speciality care infrastructure that supports both immunotherapy programs and biologic therapy delivery in large metropolitan centers across the country.

The U.S. allergy therapeutics market receives USD 4.5 billion annually in pharmaceutical research and development investment across biologic, small molecule, and immunotherapy platforms. Allergic rhinitis and asthma represent the majority of diagnosed cases. 60–70% of patients initiate treatment via OTC antihistamines and nasal sprays.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Allergy Treatment Market Insights

The European allergy treatment market is supported by high allergy disease burden in Northern and Southern European populations, established European allergy immunotherapy specialists and research centres, and increasing regulatory and clinical acceptance of sublingual immunotherapy tablets, which have been available in Europe for longer than in many other markets. Germany is the largest pharmacy market in Europe and has a sophisticated network of allergy specialists and an advanced health technology assessment framework that has steadily supported reimbursement for biologic allergy therapies. Pan-European clinical guidelines published by the European Academy of Allergy and Clinical Immunology help to standardise treatment protocols and facilitate the adoption of evidence-based therapies across the wider European market.

Allergic rhinitis affects 100 million Europeans, with the European Allergy White Paper estimating that allergy disease collectively costs the European healthcare system over EUR 150 billion annually in direct medical costs and indirect productivity losses, providing a compelling economic rationale for investment in more effective and disease-modifying allergy treatment approaches. Pollen-driven seasonal peaks strongly influence annual treatment demand cycles. Strong clinical infrastructure supports allergist-led care pathways.

Asia Pacific Allergy Treatment Market Insights

Asia Pacific is the fastest-growing regional allergy treatment market at a CAGR of 8.38% through 2035. China has the highest share in the region, fuelled by the rapid expansion of its pharmaceutical market, increasing allergy prevalence due to urbanisation and growing government investment in healthcare, which has led to better access to specialist allergy care and enhanced reimbursement coverage for allergy treatment products. India is the fastest growing country-level market in the region, fuelled by rapidly growing allergy awareness, expanding urban air pollution driving the incidence of respiratory allergy, a growing middle class with improved healthcare access, and a large and growing pharmaceutical manufacturing sector, increasing the availability and affordability of allergy treatment products across the country’s diverse healthcare settings.

Allergy prevalence in Asia Pacific has risen by an estimated 30–40% over the past two decades, with urbanization, changing dietary patterns, and increasing environmental pollution exposure identified as primary drivers. Allergy testing volumes are rising significantly in metropolitan cities. Growing adoption of OTC antihistamines supports self-care trend. Biologics adoption is still limited but expanding in developed APAC markets.

MEA & Latin America Allergy Treatment Market Insights

Both Middle East & Africa and Latin America showed growth trajectories above the global market average, driven by increasing allergy disease burden, expanding healthcare infrastructure and improved pharmaceutical access. UAE is a leader in Middle East & Africa revenues driven by its advanced private healthcare system, high per-capita income and a cosmopolitan expatriate population with high health awareness, which is driving demand for comprehensive allergy diagnosis and treatment services including biologic therapies and immunotherapy programs. Brazil leads allergy treatment in Latin America, given the high disease burden and the large healthcare systems, while Mexico’s urban growth is increasing access to specialists. Strong generic manufacturing makes medicines more widely available, and rising incomes improve access to immunotherapy and biologics.

The Gulf Cooperation Council allergy treatment market is estimated to grow at above-average rates through the forecast period, supported by an estimated 30–35% allergy prevalence rate across GCC populations influenced by extreme temperature variations, dust exposure, and dietary westernization, with the UAE and Saudi Arabia collectively representing over 60% of regional pharmaceutical allergy treatment revenues. Air pollution and desert dust are key respiratory allergy triggers. OTC antihistamines dominate first-line treatment behaviour.

Market Dynamics

Growth Drivers: Rising allergy prevalence and biologic therapy expansion

The prevalence of allergic disease continues to increase globally across the respiratory, dermatologic and food allergy categories driven by urbanisation, environmental pollution, changes in diet, and reduced microbial diversity in early life environments, leading to an expanding patient population and structural long-term demand growth for allergy treatment products across all therapeutic categories. The clinical and commercial validation of biologic therapies targeting specific immunological pathways has effectively raised the revenue potential of the allergy treatment market by establishing a premium treatment tier with significantly higher per-patient revenue than traditional symptomatic pharmacotherapy. The ongoing expansion of indications for biologic therapy into other allergic conditions including food allergy, eosinophilic oesophagitis and allergic contact dermatitis is further expanding the addressable market.

Restraints: High biologic therapy costs and complex reimbursement access

A key access barrier in markets with limited and not comprehensive pharmaceutical reimbursement coverage that restricts the penetrable patient population within the highest-growth segment of the allergy treatment market in price-sensitive healthcare systems is the high acquisition cost of biologic allergy therapies with the approved products costing USD 30,000–50,000 or more per patient annually. The administrative burden of prior authorisation requirements, step therapy protocols and formulary restrictions set by payers across key markets including the United States hinders the allergy specialists and delays patient access to the right biologic treatment, dampening the commercial uptake trajectory versus the clinical potential of approved therapies.

Opportunities: Precision immunotherapy and emerging market expansion

The development of precision immunotherapy platforms, including peptide immunotherapy, recombinant allergen extracts and adjuvanted formulations that enhance efficacy and accelerate the desensitisation timeline relative to conventional allergen immunotherapy, presents a significant near-term commercial opportunity for companies able to deliver clinical validation and regulatory approval in the most commercially relevant allergen categories. Regulatory approvals of sublingual immunotherapy tablets in Europe and the United States have paved the way for standardised, home-administrable allergen immunotherapy, which is increasingly transforming the immunotherapy market and broadening patient access to disease-modifying allergy treatment. Biosimilars of biologics such as omalizumab enhance access in price-sensitive markets via reduced cost barriers and increased patient uptake.

Recent Developments:

-

2026: Sanofi and Regeneron expanded Dupixent's (dupilumab) label to include additional pediatric allergy indications, following positive Phase III trial results in children with moderate-to-severe allergic conditions, further broadening the commercial reach of the world's highest-revenue allergy biologic therapy.

-

2026: ALK-Abelló launched an expanded sublingual immunotherapy tablet portfolio targeting house dust mite and multiple tree pollen allergens in key Asia Pacific markets, accelerating the region's transition from subcutaneous to home-based sublingual immunotherapy formats.

-

2025: AstraZeneca reported positive Phase III results for tezepelumab in patients with allergic asthma comorbid with allergic rhinitis, supporting a supplemental indication filing that would further expand the addressable patient population for this biologic thymic stromal lymphopoietin pathway inhibitor.

-

2025: Nestlé Health Science (Aimmune) advanced the commercialization of Palforzia (peanut allergen powder-dnfp) oral immunotherapy in European markets following EMA approval, initiating a systematic rollout through allergy specialty clinic networks across Germany, France, and the United Kingdom.

Allergy Treatment Market Key Players are:

-

Sanofi

-

Regeneron Pharmaceuticals

-

GlaxoSmithKline (GSK)

-

Pfizer

-

Novartis

-

Johnson & Johnson (Janssen)

-

AstraZeneca

-

Roche

-

AbbVie

-

Merck & Co.

-

Teva Pharmaceutical Industries

-

Bayer

-

Viatris

-

ALK-Abelló

-

Stallergenes Greer

-

Allergy Therapeutics

-

DBV Technologies

-

HAL Allergy Group

-

Nestlé Health Science (Aimmune)

-

Amgen

Allergy Treatment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 24.02 Billion |

| Market Size by 2035 | USD 50.38 Billion |

| CAGR | CAGR of 7.82% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Antihistamines, Corticosteroids, Decongestants, Mast Cell Stabilizers, Leukotriene Receptor Antagonists, Immunotherapy, Biologics) • By Allergy Type (Respiratory Allergies – Allergic Rhinitis, Asthma; Skin Allergies – Dermatitis, Urticaria; Food Allergies; Drug Allergies; Insect Sting Allergies) • By Route of Administration (Oral, Nasal, Injectable, Topical, Sublingual) • By End User (Hospitals, Specialty Clinics, Homecare Settings, Retail Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sanofi, Regeneron Pharmaceuticals, GlaxoSmithKline (GSK), Pfizer, Novartis, Johnson & Johnson (Janssen), AstraZeneca, Roche, AbbVie, Merck & Co., Teva Pharmaceutical Industries, Bayer, Viatris, ALK-Abelló, Stallergenes Greer, Allergy Therapeutics, DBV Technologies, HAL Allergy Group, Nestlé Health Science (Aimmune), Amgen |

Frequently Asked Questions

The allergy treatment market is expected to grow at a CAGR of 7.82% from 2026 to 2035.

The allergy treatment market was valued at USD 24.02 Billion in 2025.

Key growth drivers include rising global allergy prevalence, increasing adoption of biologics targeting specific immune pathways, and expanding use of disease-modifying immunotherapy, collectively increasing treated patient volumes and per-patient revenue in the allergy treatment market.

Immunotherapy is the fastest-growing treatment type in the allergy treatment market, with a CAGR of 8.56% from 2026 to 2035.

North America dominated the allergy treatment market in 2025, holding 37.04% of global revenues, with the United States accounting for 84.84% of North American revenues.

Get in Touch