Biobetters Market Report Scope & Overview:

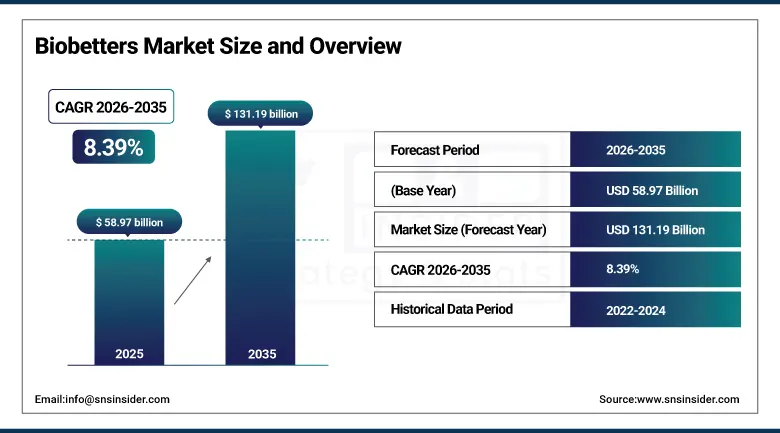

The Biobetters Market was valued at USD 58.97 Billion in 2025 and is expected to reach USD 131.19 Billion by 2035, growing at a CAGR of 8.39% from 2026 to 2035.

Biobetters represent a distinct and rapidly evolving category of biological medicines that are engineered variants of existing approved biologic drugs, specifically developed to deliver clinically meaningful improvements over the original reference products rather than merely replicating their therapeutic profiles. Unlike biosimilars, which are designed to match the efficacy and safety of an originator molecule, biobetters are purposefully engineered with structural or formulation changes that lead to improved pharmacokinetics, increased receptor binding affinity, decreased immunogenicity, extended half-life, or enhanced delivery convenience. This distinction positions biobetters as true next-generation therapeutic assets that can unlock commercial value across a wide range of high-burden disease indications, including oncology, autoimmune diseases, metabolic disorders, and hematologic diseases.

180+ active clinical-stage biobetter candidates in pipeline Dominated by oncology and autoimmune engineering programs. 70% of leading hospitals integrate Fc-engineered biologics in formulary use High adoption of next-gen antibody modifications

Market Size and Forecast:

-

Market Size in 2026E: USD 63.53 Billion

-

Market Size by 2035: USD 131.19 Billion

-

CAGR: 8.39% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Biobetters Market - Request Free Sample Report

Biobetters Market Trends:

-

Biologics patent expirations are driving growth in engineered biobetters across oncology and autoimmune diseases.

-

Subcutaneous reformulations are improving convenience and reducing treatment costs versus IV biologics.

-

Half-life extension technologies (PEGylation, Fc-fusion) enable longer dosing intervals and better compliance.

-

Advanced mammalian expression systems enhance glycoengineering and improve therapeutic efficacy in oncology.

-

Evolving FDA and EMA pathways are increasing regulatory clarity and boosting pipeline investment confidence.

U.S. Biobetters Market Outlook

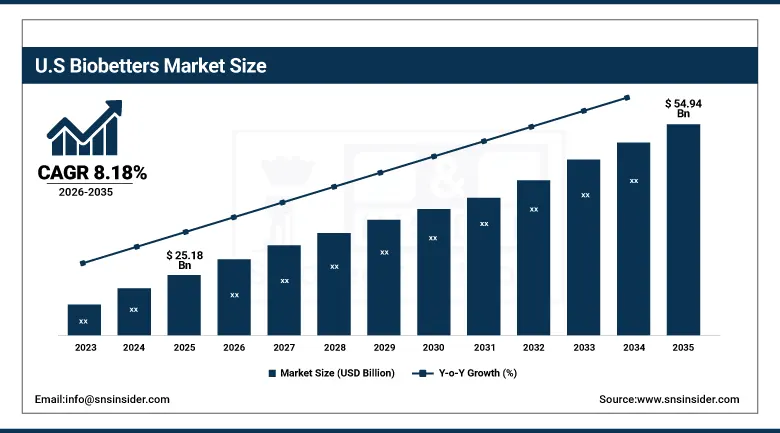

The U.S. Biobetters Market was valued at USD 25.18 Billion in 2025 and is expected to reach USD 54.94 Billion by 2035, growing at a CAGR of 8.18%.

The United States represents the single largest national market for biobetters globally, reflecting the country's established leadership in biopharmaceutical innovation, its favorable regulatory environment under FDA's Biologics License Application pathway, and the willingness of private payers and government healthcare programs to reimburse premium biologics demonstrating clinical differentiation. The U.S. biobetter market benefits from the concentration of leading academic research centers, specialized contract development and manufacturing organizations (CDMOs), and the depth of venture and institutional capital committed to biologic engineering platforms. Oncology biobetters command particular commercial strength in the U.S. market due to the high disease burden, established oncologist prescribing infrastructure, and patient advocacy support for innovative cancer therapies.

The FDA received over 50 Biologics License Applications annually in recent years, with biobetter-class assets representing an increasing proportion of novel biologic submissions as sponsors leverage structural engineering advantages to differentiate from both originator products and emerging biosimilar competition.

Biobetters Market Segmentation Analysis

-

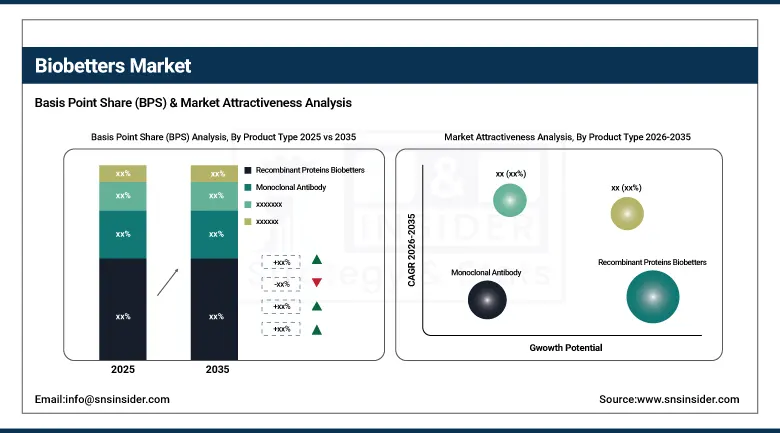

By Product Type, recombinant proteins biobetters dominated the market with 38.15% share in 2025, while fusion protein biobetters are the fastest growing product type with the highest CAGR of 10.18% from 2026 to 2035.

-

By Application, oncology dominated the market with 34.06% share in 2025, while metabolic disorders are the fastest growing application with the highest CAGR of 9.30% from 2026 to 2035.

-

By Expression System, mammalian cell systems dominated the market with 70.21% share in 2025, while plant-based expression systems are the fastest growing expression system with the highest CAGR of 9.92% from 2026 to 2035.

-

By Route of Administration, subcutaneous dominated the market with 52.16% share in 2025, while oral route is the fastest growing route with the highest CAGR of 10.65% from 2026 to 2035.

By Product Type, recombinant proteins biobetters dominate the biobetters market, while fusion protein biobetters is the fastest-growing segment.

Recombinant Proteins Biobetters segment dominated the market with the highest revenue share of about 38.15% in 2025 owing to the broad therapeutic applicability of engineered recombinant proteins across oncology, autoimmune, and hematological indications, combined with the established manufacturing infrastructure that enables cost-effective production scaling. Engineering improvements such as optimized glycosylation patterns, site-specific PEGylation, and albumin-fusion technologies have produced clinically validated recombinant protein biobetters with demonstrably superior pharmacokinetic profiles compared to originator reference products, driving physician preference and formulary placement in high-volume therapeutic segments.

Fusion Protein Biobetters segment is estimated to register the highest CAGR of 10.18% during the forecast period of 2026–2035 owing to advancing protein engineering capabilities that enable creation of multi-functional therapeutic entities combining targeting domains with effector functions, cytokine components, or extended half-life scaffolds within a single molecular architecture. The clinical and commercial success of pioneering fusion protein biologics has validated the platform approach, and biobetter variants offering improved half-life, reduced immunogenicity, or enhanced receptor engagement are progressing through advanced clinical stages with strong commercial potential in autoimmune and oncology applications.

By Application, oncology dominates the biobetters market, while metabolic disorders is the fastest-growing segment.

Oncology segment dominated the biobetters market with the largest revenue share of about 34.06% in 2025 due to the high clinical and commercial value of oncology biologics, the substantial unmet need for improved therapeutic outcomes in cancer treatment, and the premium pricing environment that rewards clinical differentiation in solid tumor and hematological malignancy indications. Glycoengineered antibody biobetters with enhanced ADCC activity, antibody-drug conjugate improvements, and half-life extended checkpoint inhibitor variants represent key oncology biobetter categories advancing through clinical development pipelines.

Metabolic Disorders segment is projected to witness the fastest CAGR of 9.30% during 2026–2035 driven by the massive and growing global prevalence of type 2 diabetes and obesity, the proven commercial success of GLP-1 receptor agonist biologics, and the active engineering programs targeting longer-acting, orally bioavailable, or dual-receptor engaging biobetter insulin and incretin analogs. The regulatory and commercial validation of extended-duration insulin analogs and the transformative market impact of obesity biologic therapies have established metabolic disorders as the highest-growth application domain within the biobetters market.

By Expression System, mammalian cell systems dominate the biobetters market, while plant-based expression systems are the fastest-growing segment.

Mammalian Cell Systems segment emerged as the market leader with a dominant share of around 70.21% in 2025 owing to the critical importance of human-like glycosylation patterns in biobetter engineering, which mammalian expression systems uniquely provide. CHO cell platforms in particular have become the industry standard for manufacturing therapeutic antibodies and Fc-fusion proteins, benefiting from decades of bioprocess optimization, regulatory acceptance, and the availability of cell line engineering tools that enable precise glycan profile control required for biobetter differentiation strategies including afucosylation for enhanced ADCC activity.

Plant-based Expression Systems segment is anticipated to record the fastest CAGR of 9.92% throughout the forecast period of 2026–2035 driven by increasing recognition of plants as cost-efficient, scalable, and contamination-resistant manufacturing platforms for biobetter proteins. Advances in plant expression vector design, post-translational modification engineering in plant cells, and the increasing regulatory acceptance of plant-made pharmaceuticals are creating new development opportunities particularly for biobetter proteins targeting emerging markets and diseases where cost of goods reduction is essential for commercial viability.

By Route of Administration, subcutaneous dominates the biobetters market, while oral route is the fastest-growing segment.

Subcutaneous segment dominated the biobetters market with the highest revenue share of 52.16% in 2025 due to the significant clinical and patient convenience advantages of subcutaneous administration over the intravenous formulations used by many originator reference biologics. Converting high-volume intravenous biologics into subcutaneous biobetter formulations using hyaluronidase co-formulation technology, concentrated formulation engineering, or autoinjector delivery systems represents one of the most commercially validated biobetter development strategies, enabling self-administration at home and reducing infusion center healthcare costs.

Oral route segment is projected to register the highest CAGR of 10.65% during the forecast period of 2026–2035 owing to the transformative commercial potential of oral biologic delivery, which eliminates injection-related barriers, dramatically improves patient adherence, and opens entirely new commercial markets for biologic therapies in diseases where injectable administration has historically limited adoption. Advances in oral peptide delivery technologies including intestinal permeation enhancers, protease inhibitor co-formulation, and lipid nanoparticle oral systems are enabling clinical progression of oral biobetters particularly in the insulin and GLP-1 analog space.

Regional Analysis:

|

Region |

Major Country |

2025 Share (%) |

|---|---|---|

|

North America |

United States |

90.54% |

|

Europe |

Germany |

31.46% |

|

Asia Pacific |

China |

42.16% |

|

Latin America |

Brazil |

30.89% |

|

Middle East & Africa |

UAE |

44.34% |

North America Biobetters Market Insights

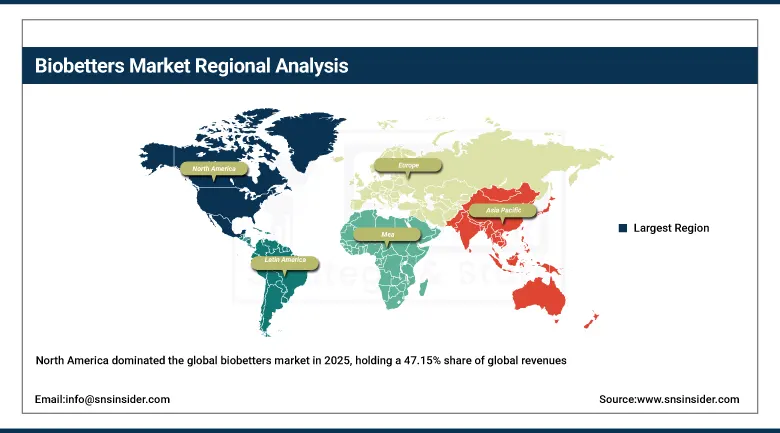

North America dominated the global biobetters market in 2025, holding a 47.15% share of global revenues, with the United States accounting for 90.54% of regional revenue. Market leadership is underpinned by the region's unparalleled biopharmaceutical innovation ecosystem, deep venture and institutional capital commitment to biological engineering platforms, favorable FDA regulatory pathways for biobetter assets demonstrating clinical differentiation, and the strong formulary preference of U.S. payers for biologics with demonstrated therapeutic improvements over reference products. Canada contributes supplementary demand through its publicly funded healthcare system, which actively evaluates biobetter therapies demonstrating health economic value in reducing treatment burden and improving patient outcomes.

The U.S. biopharmaceutical sector invested over USD 100 billion annually in research and development in recent years, with biologics engineering programs representing the fastest-growing component of pharmaceutical R&D investment as companies prioritize next-generation biologic innovation over small molecule development.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Biobetters Market Insights

Europe represents the second largest biobetters market globally, with Germany serving as the leading national market and home to major biopharmaceutical innovators including Bayer and an extensive network of specialized biologic contract manufacturers. The European market benefits from both demand-side and supply-side strengths, combining the EMA's evolving regulatory guidance on demonstrating biobetter clinical differentiation with the presence of world-class biologic manufacturing clusters in Germany, Switzerland, Belgium, and Ireland. The European health technology assessment environment rewards biobetters that demonstrate clear clinical improvements over originator biologics, creating a favorable reimbursement landscape for well-characterized biobetter assets with robust clinical evidence packages. The United Kingdom's post-Brexit regulatory independence through the MHRA has introduced additional flexibility in biobetter development pathways.

Europe's biopharmaceutical manufacturing sector contributes over EUR 40 billion annually to the regional economy, with biologic drug substance manufacturing representing the highest-growth component of pharmaceutical production investment across the continent. 65% utilization of subcutaneous reformulated biologics in chronic care .Shift from hospital IV to outpatient care models

Asia Pacific Biobetters Market Insights

Asia Pacific is the fastest-growing regional biobetters market at a CAGR of 8.93% through 2035. China accounts higher in Asia Pacific revenues as the country's expanding biopharmaceutical innovation sector, government support for next-generation biologic development under national bioeconomy strategies, and the massive domestic patient population in oncology, diabetes, and autoimmune disease indications create a compelling home market for both domestic and multinational biobetter developers. India represents a high-growth country market through its established biologics manufacturing capabilities and increasing government healthcare spending on advanced biologic therapies. South Korea and Japan maintain sophisticated biobetter development ecosystems supported by Samsung Biologics and Takeda respectively, with strong regulatory capabilities and manufacturing quality standards aligned with international requirements.

China's biopharmaceutical market exceeded USD 10 billion in recent years, with the National Medical Products Administration approving increasing numbers of novel biologic and biobetter assets as the country transitions from a primarily generics and biosimilars manufacturing base toward genuine biologic innovation capability.

MEA & Latin America Biobetters Market Insights

Middle East & Africa and Latin America represent commercially emerging biobetters markets that are advancing through increasing healthcare infrastructure investment, growing prevalence of oncological and metabolic disease indications, and improving biologic therapy reimbursement environments. The UAE leads MEA revenues with 30.45% of regional share, supported by advanced healthcare infrastructure in Dubai and Abu Dhabi, high per-capita healthcare spending, and government investment in biotechnology sector development as part of economic diversification strategies. Saudi Arabia presents significant growth potential through Vision 2030 healthcare system investments. Brazil dominates Latin America with 46.29% of regional revenues, benefiting from the country's public healthcare system which increasingly includes advanced biologic therapies within reimbursed treatment protocols for oncology and autoimmune diseases.

The Middle East biopharmaceutical market is projected to benefit from over USD 65 billion in planned healthcare infrastructure investments across GCC countries through the mid-2030s, with advanced biologic therapy adoption identified as a strategic priority within regional health system modernization programs.

Growth Drivers: Biologics patent expirations and demand for therapeutic improvements

The unprecedented wave of biologics patent expirations sweeping through the pharmaceutical industry across the 2025–2035 period is creating the primary structural growth catalyst for biobetter development, as the scientific freedom to operate on expired originator molecules enables engineering improvements that biosimilar development regulations explicitly exclude. The documented clinical limitations of first-generation biologic drugs, including inconvenient dosing frequencies, immunogenicity profiles, infusion administration requirements, and suboptimal tissue penetration, provide engineering targets that biobetter developers are systematically addressing through platform technologies including half-life extension, glycan engineering, and novel delivery formulation. The demonstrated commercial success of pioneering biobetter assets, including engineered insulin analogs and Fc-optimized antibody variants, has validated the investment thesis and is attracting increasing capital commitment to the biobetter sector.

Restraints: Complex regulatory landscape and manufacturing development costs

The regulatory pathway for biobetters occupies an ambiguous space between novel biologics and biosimilars, requiring developers to conduct full clinical programs demonstrating the safety and efficacy of the modified molecule while also characterizing the nature and clinical relevance of the improvements over the reference product. This regulatory complexity translates into development timelines and clinical investment costs that can approach those of novel biologic development, creating significant financial risk particularly for smaller biotechnology companies without the capital resources to sustain multi-year clinical programs. Manufacturing process development for engineered biobetters requires specialized capabilities in glycoengineering, protein modification chemistry, and advanced analytical characterization that represent significant technical barriers to entry.

Opportunities: Novel delivery technology platforms and emerging market expansion

The convergence of multiple enabling technology platforms including oral peptide delivery systems, subcutaneous high-concentration formulation technology, autoinjector device innovation, and sustained-release depot formulations is creating a new generation of biobetter development opportunities centered on delivery route transformation rather than molecular modification alone. The ability to convert successful intravenous oncology or immunology biologics into convenient subcutaneous or oral biobetter formulations represents a near-term commercial opportunity with potentially shorter development timelines than molecular engineering approaches.

Recent Developments:

-

2026: Samsung Biologics announced a strategic biobetter development collaboration with a leading U.S. oncology biotechnology firm leveraging its CHO cell glycoengineering platform to advance two Fc-optimized antibody biobetter candidates through IND-enabling studies.

-

2026: AbbVie launched its subcutaneous formulation biobetter of a major immunology biologic using proprietary hyaluronidase co-formulation technology, achieving regulatory approval in the U.S. and EU based on bioequivalence and patient preference clinical data.

-

2025: Amgen advanced its glycoengineered anti-CD20 antibody biobetter into Phase III clinical trials targeting non-Hodgkin's lymphoma with enhanced ADCC activity compared to rituximab originator, with interim data demonstrating superior progression-free survival in high-risk patient subgroups.

-

2025: Novo Nordisk received FDA approval for its next-generation once-weekly insulin analogy biobetter demonstrating significantly reduced hypoglycaemia rates and improved time-in-range glycaemic control metrics compared to the reference daily insulin product in pivotal Type 1 and Type 2 diabetes trials.

Biobetters Market Key Players are:

-

AbbVie

-

Novartis

-

Sanofi

-

Pfizer

-

Merck & Co.

-

Bristol Myers Squibb

-

Johnson & Johnson

-

Eli Lilly and Company

-

AstraZeneca

-

GlaxoSmithKline

-

Biogen

-

Regeneron Pharmaceuticals

-

Takeda Pharmaceutical Company

-

Bayer

-

CSL Limited

-

Gilead Sciences

-

Samsung Biologics

Biobetters Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 58.97 Billion |

| Market Size by 2035 | USD 131.19 Billion |

| CAGR | CAGR of 8.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Recombinant Proteins Biobetters, Monoclonal Antibody (mAb) Biobetters, Hormone Biobetters (e.g., insulin analogs), Cytokine/Growth Factor Biobetters, Fusion Protein Biobetters, Others) •By Application (Oncology, Autoimmune Diseases (Rheumatoid Arthritis, Psoriasis, IBD), Metabolic Disorders (Diabetes, Obesity), Hematological Disorders, Infectious Diseases, Others) •By Expression System (Mammalian Cell Systems (CHO, HEK), Microbial Systems (E. coli, Yeast), Plant-based Expression Systems, Transgenic Systems) •By Route of Administration (Subcutaneous, Intravenous, Intramuscular, Oral) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Roche, Amgen, AbbVie, Novartis, Sanofi, Pfizer, Merck & Co., Bristol Myers Squibb, Johnson & Johnson, Eli Lilly and Company, AstraZeneca, GlaxoSmithKline, Biogen, Regeneron Pharmaceuticals, Takeda Pharmaceutical Company, Bayer, Novo Nordisk, CSL Limited, Gilead Sciences, Samsung Biologics |

Frequently Asked Questions

The biobetters market is expected to grow at a CAGR of 8.39% from 2026 to 2035.

The biobetters market was valued at USD 58.97 Billion in 2025.

Growth is driven by biologics patent expirations, demand for improved pharmacokinetics and dosing convenience, and rising investment in biobetter development platforms.

Fusion Protein Biobetters is the fastest-growing product type in the Biobetters Market, with a CAGR of 10.18% from 2026 to 2035.

North America dominated the biobetters market in 2025, holding a 47.15% share of global revenues, with the United States accounting for 90.54% of North American revenues.

Get in Touch