Diagnostics Market Report Scope & Overview:

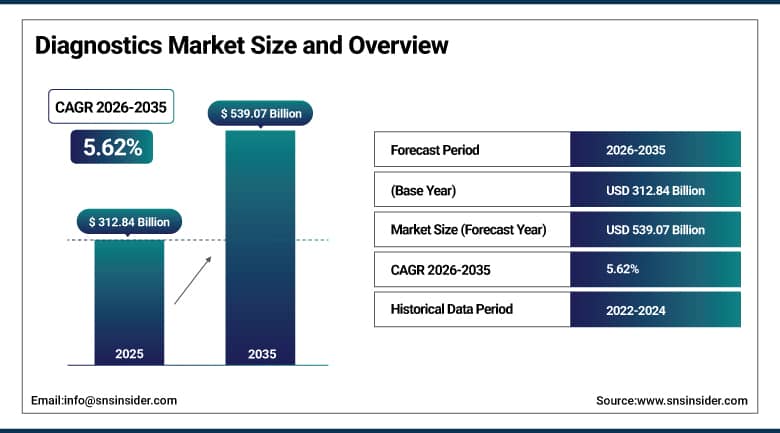

The Diagnostics Market was valued at USD 312.84 Billion in 2025 and is expected to reach USD 539.07 Billion by 2035, growing at a CAGR of 5.62% from 2026 to 2035.

The expansion of the market can be attributed to the increasing number of people suffering from chronic and infectious diseases, rising need for disease diagnosis at an early stage and rising demand for precision medicine. Increasing adoption of advanced molecular diagnostics tools, point of care testing technologies and AI enabled diagnostics platform are being used by the healthcare systems to aid clinical decision making. In addition, there is a growing trend of expenditure in the healthcare sector, increasing aging population and growing awareness of preventative healthcare. Moreover, the increasing demand for advanced diagnostic tools in hospitals, laboratories and research institutes is also due to technological advancements in genomics, digital pathology and laboratory automation.

In March 2025, Roche strengthened its portfolio of molecular diagnostics by launching innovative PCR based testing technologies that aid infectious disease diagnosis and laboratory efficiency. In January 2026, Siemens Healthineers launched new AI based diagnostic imaging and laboratory solutions.

Market Size and Forecast:

-

Market Size in 2026E: USD 329.42 Billion

-

Market Size by 2035: USD 539.07 Billion

-

CAGR: 5.62% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Diagnostics Market - Request Free Sample Report

Market Trends:

-

Increasing adoption of molecular diagnostics and precision medicine is driving demand for advanced testing technologies globally.

-

Growing investments in laboratory automation and AI-assisted diagnostic platforms are improving testing efficiency and clinical decision-making.

-

Rising prevalence of chronic diseases and infectious conditions is accelerating demand for early disease detection solutions.

-

Expansion of point-of-care testing and decentralized diagnostics is improving accessibility to healthcare services.

-

Increasing utilization of genomic testing and companion diagnostics is supporting the advancement of personalized healthcare worldwide.

U.S. Diagnostics Market Outlook:

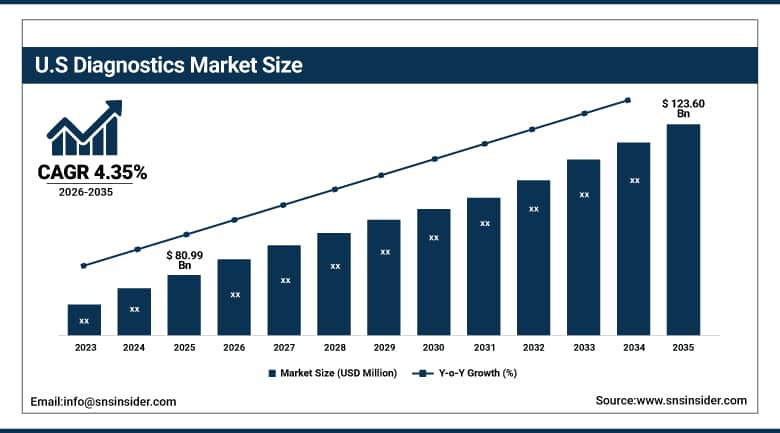

The U.S. Diagnostics Market was valued at USD 80.99 Billion in 2025 and is expected to reach USD 123.60 Billion by 2035, growing at a CAGR of 4.35% from 2026 to 2035.

The market growth is driven by the increasing prevalence of chronic diseases, rising demand for early disease detection, and increasing adoption of precision medicine across the United States. Healthcare providers are increasingly investing in molecular diagnostics, genomic testing and AI-enabled diagnostic platforms to improve clinical decision making and patient outcomes. Increasing healthcare expenditure, ageing population, and growing demand for preventive healthcare services are further contributing to the market growth. Additionally, the country’s advanced diagnostic ecosystem is being improved and the use of next-generation testing technologies is being promoted due to the increasing acceptance of point-of-care diagnostics, laboratory automation, and digital pathology solutions.

In March 2025, Roche Diagnostics USA expanded its molecular testing portfolio with the launch of new PCR-based solutions designed to improve infectious disease detection and laboratory efficiency for healthcare facilities in the U.S. Siemens Healthineers USA announced new AI-powered diagnostic imaging and laboratory workflow solutions in January to help improve clinical productivity and deliver precision diagnostics for hospitals and diagnostic centres across the country.

Diagnostics Market Segment Analysis:

-

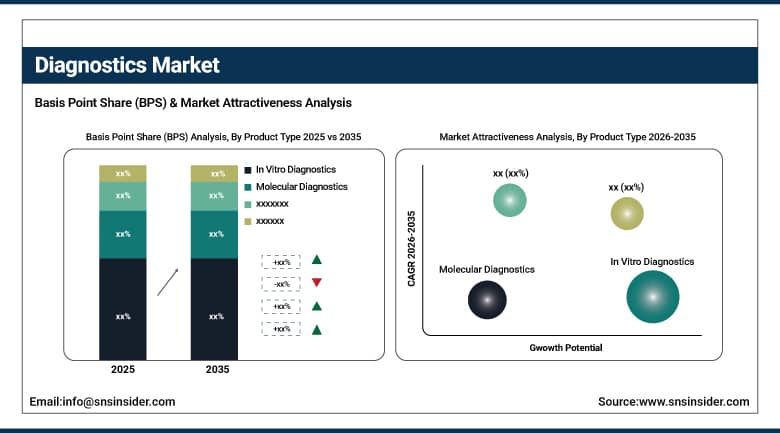

By Product Type, In Vitro Diagnostics (IVD) dominated the diagnostics market with approximately 43.00% share in 2025, while Molecular Diagnostics is the fastest growing product type segment from 2026 to 2035.

-

By Application, Infectious Diseases dominated the diagnostics market with approximately 27.00% share in 2025, while Oncology is the fastest growing application segment from 2026 to 2035.

-

By End User, Hospitals & Clinics dominated the diagnostics market with approximately 46.00% share in 2025, while Home Care Settings are the fastest growing end-user segment from 2026 to 2035.

-

By Technology, Immunodiagnostics dominated the diagnostics market with approximately 31.00% share in 2025, while Digital Diagnostics is the fastest growing technology segment from 2026 to 2035.

By Product Type, In Vitro Diagnostics dominates, Molecular Diagnostics grows fastest

In Vitro Diagnostics (IVD) dominated the diagnostics market in 2025 and held approximately 43% revenue share. Healthcare providers increasingly depended on blood testing, clinical chemistry, immunoassays, and laboratory diagnostics for routine screening, disease monitoring, and early disease detection. The worldwide leadership position of IVD segment was enhanced by the extensive diagnostic testing in hospitals and laboratories, and growing preventive healthcare initiatives and chronic disease management programmes.

Molecular Diagnostics is expected to register the fastest CAGR during the forecast period. The growth of this segment can be attributed to the increasing demand for precision medicine, genetic testing, and rapid pathogen detection technologies. Increasing utilisation of PCR-based testing, next-generation sequencing and companion diagnostics is driving growth of molecular testing capabilities in oncology, infectious diseases and personalised healthcare applications.

By Application, Infectious Diseases dominate, Oncology grows fastest

Infectious Diseases dominated the diagnostics market in 2025 and accounted for approximately 27% revenue share. The segment derived benefits from high testing volumes related to respiratory infections, hospital-acquired infections, sexually transmitted diseases and emerging infectious diseases. The demand for advanced diagnostic testing solutions worldwide increased with the growing attention for early diagnosis and public health surveillance.

Oncology is expected to witness the fastest CAGR during the forecast period. This is due to the growing incidence of cancer globally and the increasing use of genomic testing and biomarker-based diagnostics. The growing investments in precision oncology and companion diagnostics are facilitating the adoption of advanced cancer screening and personalised treatment approaches in healthcare systems.

By End User, Hospitals & Clinics dominate, Home Care Settings grow fastest

Hospitals & Clinics dominated the diagnostics market in 2025 and held approximately 46% revenue share. The segment is driven by large patient volumes, extensive laboratory infrastructure and increasing uptake of integrated diagnostic technologies for disease detection and treatment monitoring. Healthcare organisations are investing more in laboratory automation and advanced diagnostic platforms to improve clinical efficiency and patient outcomes.

The Home Care Settings segment is expected to witness the fastest CAGR during the forecast period owing to the rising demand for self-testing solutions and remote patient monitoring technologies. Growing consumer preference for convenient healthcare services, increasing availability of home-based diagnostic kits are creating large opportunities for decentralised and patient-centric diagnostic testing.

By Technology, Immunodiagnostics dominate, Digital Diagnostics grow fastest

Immunodiagnostics dominated the diagnostics market in 2025 and accounted for approximately 31% revenue share. The technology is widely used for infectious disease detection, autoimmune disease testing, hormone analysis and cancer diagnosis. Moreover, increasing demand for fast and accurate testing solutions along with continuous advancements in immunoassay technologies further supported the segment growth.

Digital Diagnostics is estimated to be fastest growing CAGR owing to the increasing use of artificial intelligence, cloud computing and advanced analytics in diagnostic workflows. Around the world, healthcare providers are embracing AI-assisted imaging interpretation, digital pathology and connected diagnostic platforms to improve accuracy, efficiency and real-time clinical decision-making.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.50% |

|

Europe |

Germany |

25.20% |

|

Asia Pacific |

China |

39.80% |

|

Middle East |

UAE |

29.00% |

|

Latin America |

Brazil |

44.50% |

North America Diagnostics Market Insights

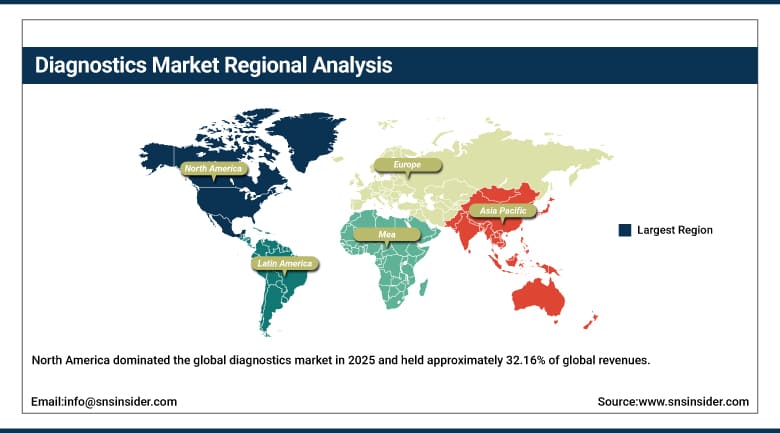

North America dominated the global diagnostics market in 2025 and held approximately 32.16% of global revenues. The U.S. and Canada continued to dominate the market, due to high expenditure on healthcare, advanced healthcare infrastructure, and high adoption of precision diagnostics. Medical providers increasingly are turning to molecular diagnostics, platforms for genomic testing and laboratory automation to improve the detection of disease and treatment outcomes.

Spending on diagnostics and investment in health care technology continued to grow across the region in 2025. The U.S. led the North America market with a share of nearly 80.50% in terms of revenues owing to large diagnostic testing market, broad network of laboratories and strong foothold of major diagnostic manufacturers in the country. Canada also boosted funding for laboratory modernisation and precision health initiatives.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Diagnostics Market Insights

Europe accounted for approximately 30.87% of global diagnostics market revenues in 2025. Growth in the region is attributed to growing demand for preventive healthcare, rising incidence of chronic diseases, and growing adoption of molecular testing technologies in Germany, France, Italy and the UK. Healthcare institutions increasingly implemented digital pathology, genomic diagnostics and advanced laboratory automation systems to improve clinical efficiency and patient management.

The area enjoys strong public health care systems and growing funding for precision medicine programmes. Germany held approximately 25.20% of the European revenues due to the presence of sophisticated healthcare infrastructure and strong diagnostics industry. In 2025 the United Kingdom and France also put more money into genomics and personalised healthcare programmes

Asia Pacific Diagnostics Market Insights

Asia Pacific accounted for approximately 28.12% of global diagnostics market revenues in 2025. Rapid expansion in the region is being driven by increasing healthcare expenditure, rising disease burden and growing access to advanced medical testing in China, Japan, India and South Korea. Healthcare systems increasingly used molecular diagnostics, point-of-care testing, and digital laboratory technologies to help with early disease detection and precision healthcare delivery.

The area continues to enjoy the benefits of expanding healthcare infrastructure and growing investment in medical technology. China represented around 39.80% of the Asia Pacific revenues attributable to its large patient population, growing diagnostic laboratory networks, and rising adoption of advanced testing technologies. India and Japan also sped up investments in precision medicine and laboratory modernisation initiatives.

Middle East & Africa & Latin America Diagnostics Market Insights

The Middle East and Latin America collectively accounted for approximately 8.85% of global diagnostics market revenues in 2025. Growing consciousness about preventive diagnostics, bettering of laboratory infrastructure and rising healthcare investments are supporting market growth in Brazil, Mexico, UAE, and Saudi Arabia. The healthcare providers increasingly adopted molecular testing, infectious disease diagnostics and point of care technologies to enhance the accessibility of healthcare and disease management.

Market growth continues to be driven by regional healthcare modernisation and increased investment in laboratory capabilities. Brazil continued to be the largest market in Latin America with around 44.50% of regional revenues and the UAE accounted for around 29.00% of Middle Eastern revenues due to increasing investments in advanced healthcare services and precision diagnostic capabilities.

Market Dynamics:

Growth Drivers: Rising prevalence of chronic diseases and increasing adoption of precision diagnostics

Cancer, heart ailments, diabetes, and infections have increased in prevalence causing the need for innovative diagnosis options around the world. Healthcare providers are turning more and more to molecular diagnostics, in vitro tests and imaging technologies to help diagnose diseases early for better treatment. Global awareness about preventive health care is also contributing to the increase in testing volumes.

Demand for diagnostic tools is growing as a result of genomics innovations, biomarker tests and precision medicine. In addition, the health care sector is increasingly adopting diagnosis and laboratory automation based on artificial intelligence to improve the efficacy of testing. Such factors are leading to growth opportunities in the diagnostics industry globally.

Restraints: High diagnostic costs and complex regulatory requirements

Market penetration by advanced diagnostics is also restricted in some of the emerging markets due to the high cost involved in the procurement of sophisticated equipment and laboratory infrastructure needed for such processes. Small healthcare organizations may not be able to afford the equipment required for carrying out such testing.

There are also operational constraints posed by stringent regulatory and approval processes that may have to be adhered to by producers of these diagnostics.

Opportunities: Expansion of point-of-care testing and digital diagnostics

Increased utilization of point-of-care diagnostics and decentralization of the process of health care delivery represent major opportunities for the diagnostics market. There is an increased tendency on the part of health care professionals to adopt portable diagnostic tools and rapid tests in order to enhance access to diagnostic solutions, shorten time intervals and facilitate clinical decision-making.

There is a growing use of artificial intelligence and digital pathology as well as cloud-based diagnostics that bring about additional growth opportunities in the market. Remote health care monitoring along with investments in predictive analytics represents additional growth opportunity for the diagnostics industry.

Recent Developments:

-

March 2025: Roche expanded its molecular diagnostics portfolio by introducing advanced PCR-based solutions designed to improve infectious disease detection and laboratory efficiency.

-

February 2025: Danaher Corporation increased investments in genomics and next-generation sequencing technologies to strengthen its precision diagnostics capabilities.

-

January 2026: Siemens Healthineers launched new AI-enabled diagnostic imaging and laboratory workflow solutions aimed at improving diagnostic accuracy and clinical productivity.

-

December 2025: Abbott Laboratories expanded its rapid diagnostics portfolio by introducing new point-of-care testing solutions to support decentralized healthcare delivery and early disease detection.

Key Players:

-

F. Hoffmann-La Roche Ltd.

-

Abbott Laboratories

-

Siemens Healthineers AG

-

Danaher Corporation

-

Becton, Dickinson and Company

-

Thermo Fisher Scientific Inc.

-

Bio-Rad Laboratories, Inc.

-

QIAGEN N.V.

-

Sysmex Corporation

-

Hologic, Inc.

-

Agilent Technologies, Inc.

-

bioMérieux SA

-

Illumina, Inc.

-

PerkinElmer Inc.

-

QuidelOrtho Corporation

-

Mindray Medical International Limited

-

FUJIFILM Holdings Corporation

-

Werfen S.A.

-

Sekisui Medical Co., Ltd.

-

DiaSorin S.p.A.

Diagnostics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 312.84 Billion |

| Market Size by 2035 | USD 539.07 Billion |

| CAGR | CAGR of 5.62% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (In Vitro Diagnostics, Imaging Diagnostics, Molecular Diagnostics, Point-of-Care Diagnostics, Clinical Chemistry Diagnostics, and Others) • By Application (Infectious Diseases, Oncology, Cardiology, Neurology, Diabetes Monitoring, and Others) • By End User (Hospitals & Clinics, Diagnostic Laboratories, Academic & Research Institutes, Ambulatory Care Centers, and Home Care Settings) • By Technology (Immunodiagnostics, Clinical Chemistry, Hematology, Microbiology, Molecular Diagnostics, and Digital Diagnostics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | F. Hoffmann-La Roche Ltd., Abbott Laboratories, Siemens Healthineers AG, Danaher Corporation, Becton, Dickinson and Company (BD), Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., QIAGEN N.V., Sysmex Corporation, Hologic, Inc., Agilent Technologies, Inc., bioMérieux SA, Illumina, Inc., PerkinElmer Inc., QuidelOrtho Corporation, Mindray Medical International Limited, FUJIFILM Holdings Corporation, Werfen S.A., Sekisui Medical Co., Ltd., DiaSorin S.p.A. |

Frequently Asked Questions

The Diagnostics Market is expected to grow at a CAGR of approximately 5.62% during the forecast period from 2026 to 2035.

The Diagnostics Market was valued at approximately USD 312.84 Billion in 2025.

The market is primarily driven by the rising prevalence of chronic and infectious diseases, increasing demand for early disease detection, and growing adoption of precision medicine and advanced molecular diagnostic technologies.

North America dominated the Diagnostics Market in 2025 owing to its advanced healthcare infrastructure, high healthcare expenditure, strong adoption of precision diagnostics, and significant investments in molecular testing and laboratory automation technologies.

Get in Touch