PV Inverters Market Report Scope & Overview:

The PV Inverters Market size was estimated at USD 12.9 billion in 2023 and is predicted to reach over USD 47.44 billion by 2032 with an emerging CAGR growth of 18.5% Over the Forecast Period of 2024-2032.

Get More Information on PV Inverters Market - Request Sample Report

Demand for electricity continues to grow year by year, further enhancing the demand for various renewable resources such as solar power and machinery. Since the fall in gas prices in 2014, different energy sources, especially wind and solar, have been placed on the back burner and this trend has changed in many industries.

By Product-In terms of revenue, the central inverter had a larger revenue share of more than 49.0% by 2023. These converters are very reliable with timely repairs and are stored in a secure place for installation. Inverters combined with large arrays installed in stadium installations, industrial facilities, and buildings, take DC power across all PV panels and convert it into AC power into a single power distribution point.

Part of the string inverter took its second-largest market share in 2023. The string inverter is widely used in the commercial and residential sectors. Low initial cost and easy installation are among the key factors responsible for partial growth. These inverters are robust, allow for high design flexibility, deliver high efficiency, offer three-phase variability, are well supported (with reliable products), and have the ability to monitor remote systems.

Part of the micro PV inverters is expected to witness a significant growth rate during the forecast period. Micro PV inverters are module-level electronics and have become popular in the commercial and industrial sectors. These inverters have the advantage of high reliability, increased efficiency and performance with Maximum Power Point Tracker (MPPT), easy installation, no space constraints, and cost savings.

By Applications-In position of revenue generated, the utility segment led the PV inverter market by 2022, accounting for a budget of about 44.0%. The most widely used PV Inverter in the service sector is the central & string inverter. Increased demand for renewable energy, lowering the cost of solar energy and equipment, and government subsidies are the main reasons for the growth of the resource sector. The presence of key players, providing consumers with industry-leading service rating solutions to achieve high efficiency and reducing system balance costs through their pre-assembled power stations drives partial growth.

Based on end-use, the market is divided into commercial, residential and industrial, and services. The residential sector has seen growth due to the growing demand for renewable solar energy among consumers for electrical purposes. Governments in various countries have taken practical steps through policies and financing to promote the grip of power-gripped power generation with renewable resources such as residential power. Commercial buildings include supermarkets, shops, offices, hospitals, and schools that install solar panels for use in captivity. These sectors require continuous power supply in order to operate without interruption.

IMPACT OF COVID-19

The outbreak of COVID-19 has severely hampered the growth of the PV inverter market. The virus has affected large countries, thus curbing the growth of businesses. However, it is expected that the industry will renew its capacity to measure these impacts in the coming years.

COMPETITIVE LANDSCAPE

The market is very competitive and compact due to the presence of a large number of market players. A key practice in the operation of these solar companies involves direct integration that protects market power and reduces competition. Acquisition of technology, skilled workers, and strong R&D are among the key factors that control the competitiveness of the PV inverters industry. In March 2020, the Fimer team acquired the ABB solar switching business, making the company the 4th largest manufacturer of solar inverter worldwide. This acquisition strategy will help the company grow its global presence..

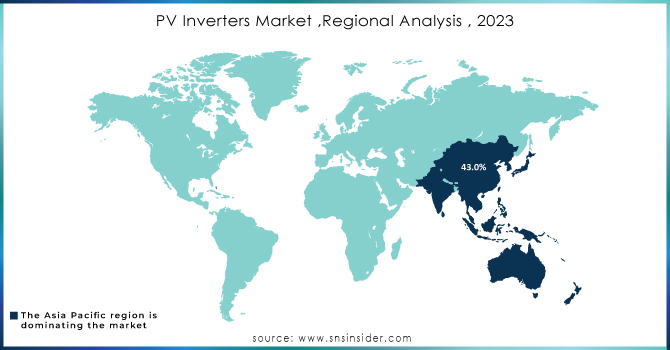

REGIONAL ANALYSIS:

The Asia Pacific is expected to have a higher revenue share of more than 43.0% over the forecast period. China plays a major role in the rapid growth of the region's solar market and is a major global competitor. The growing number of solar installations in developing countries has also contributed significantly to regional market growth.

North America captured the largest share of revenue in 2023, and the US played a major role in market growth. The U.S. is a leading market for different types of PV inverter. Some of the latest inverter systems in the world include 60 kW plus power for three phase unit inverters and 1.5 MW and medium capacity inverters. Although North America has seen strong growth of cable inverters, central PV inverters are expected to maintain the largest market share in the forecast period.

Europe is expected to see an important CAGR in the forecast period due to the existence of favorable government policies and the provision of subsidies such as residential taxes that encourage consumers to invest in renewable energy. Germany holds a leading position in the production of solar inverters in line with the hi-tech nature of inverters. So German solar companies make more competitive profit than other players.

Need any Customization as Per Your Business Requirement on PV Inverters Market - Enquiry Now

KEY PLAYERS:

The Major Players are Delta Electronics Inc, Eaton, Emerson Electric Co, Omron Corporation, Hitachi Hi-Rel Power Electronics Pvt Ltd, Power Electronics, Siemens AG, SMA Solar Technolgy AG and SunPower Corporation., Siemens Energy, Fimer Group, SMA Solar, Technology AG, Delta Electronics, Inc, SunPower Corporation, Eaton and Other Players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 12.9 Billion |

| Market Size by 2032 | US$ 47.44 Billion |

| CAGR | CAGR of 18.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by type(Central, String, Micro, Others) • by Product (Central PV inverter, String PV inverter, Micro PV inverter, Others) • by Application (Residential, Commercial & industrial, Utilities) • by Connectivity (Standalone, On-grid) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Delta Electronics Inc, Eaton, Emerson Electric Co, Omron Corporation, Hitachi Hi-Rel Power Electronics Pvt Ltd, Power Electronics, Siemens AG, SMA Solar Technolgy AG |

Frequently Asked Questions

Yes, and they are Raw material vendors, Distributors/traders/wholesalers/suppliers, Regulatory authorities, including government agencies and NGOs, Commercial research & development (R&D) institutions, Importers and exporters, Government organizations, research organizations, and consulting firms, Trade/Industrial associations, End-use industries.

The residential sector of the PV inverter market is the fastest-growing market.

North America has the PV Inverters greatest market share in terms of revenue and region market.

PV Inverters market size was valued at 12.9 billion in 2023 at a CAGR of 18.5%.

Get in Touch