Quantum Dot Display Market Size Analysis:

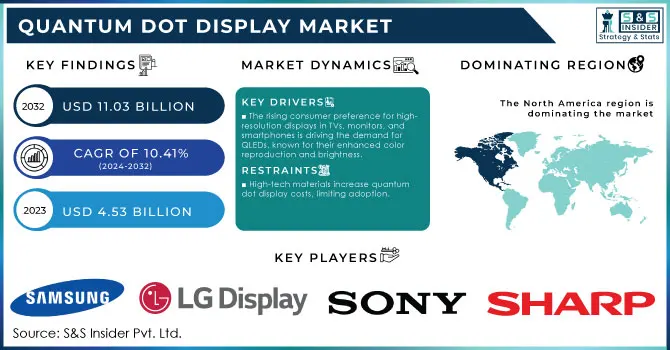

The Quantum Dot Display Market size was valued at USD 5.52 billion in 2025E and is expected to grow at 10.41% CAGR to reach USD 12.19 billion by 2033.

The Quantum Dot Display market analysis is highlighting the advancements and growth due to quantum dot display's ability to enhance energy efficiency and display quality. Semiconductor nanocrystals are used by quantum dot technology for producing pure colors, that results in vibrant and accurate displays, which further outperform traditional OLED and LED screens. The adoption of this technology is rising in different applications, including televisions, smartphones, monitors, and wearable devices, further leading to a notable rise in consumer demand.

To Get More Information on Quantum Dot Display Market - Request Sample Report

Quantum Dot Display Market Trends:

• Rapid consumer shift toward high-resolution displays (4K/8K) driving demand for premium visual quality.

• Strong adoption of QLED technology due to superior brightness performance reaching ~2,000 nits.

• Expansion of wide color gamut displays, with QLEDs exceeding 90% DCI-P3 coverage for richer color reproduction.

• Increasing use of quantum dots to enhance image vibrancy and brightness, outperforming traditional LCD/LED.

• Manufacturers prioritizing display innovations to satisfy rising consumer expectations for immersive viewing experiences.

Market Size and Forecast: 2025E

- Market Size in 2025E USD 5.52 Billion

- Market Size by 2033 USD 12.19 Billion

- CAGR of 10.41% From 2026 to 2033

- Base Year 2024

- Forecast Period 2026-2033

- Historical Data 2021-2024

Quantum Dot Display Market Growth Drivers:

-

Surging Consumer Preference for High-Resolution Displays in TVs, Smartphones, and Monitors is Propelling the Market Growth

The increasing high-quality displays’ demand is substantially reshaping the electronics landscape, especially in monitors, televisions, and smartphones. As consumers become more discriminating about their viewing experiences, the surging shift toward high-resolution displays has now become evident. This growing preference is largely propelled due to the desire for superior image quality, with the Quantum Dot Light Emitting Diodes (QLEDs), which are emerging as a favored choice owing to their exceptional brightness and color reproduction. The quantum dots are largely used by QLEDs for improving the color accuracy and brightness levels, offering vibrant images, which are appealing to viewers.

According to research, the QLED displays have the ability to reach higher brightness levels of approximately 2,000 nits, that allows impressive performance even in environments with high brightness. Moreover, the color gamut of QLEDs commonly exceeds 90% of the DCI-P3 standard, further providing a large range of colors compared with the traditional LED or LCD displays. This advancement in technology not only improves the viewing experience for consumers but it also positions QLEDs as an attractive option for producers that are aiming to fulfill the increasing quality expectations. The rise of 8K and 4K content also boosts the demand, as consumers are looking for displays, which can completely exploit the potential of high-definition content.

Quantum Dot Display Market Restraints:

-

Advanced Technology and Specialized Materials Required to Produce Quantum Dot Displays Result in Higher Manufacturing Costs Hampering Market Growth

Quantum dot displays represent a significant advancement in display technology, offering enhanced color accuracy, brightness, and energy efficiency. However, their production entails high manufacturing costs primarily due to the sophisticated technology and specialized materials required. The process begins with the synthesis of quantum dots, which are nanometer-sized semiconductor particles that emit specific colors when illuminated. This synthesis involves complex chemical processes that require precision and control, driving up costs. In addition to the quantum dots themselves, the manufacturing process necessitates advanced fabrication techniques, including precision layer deposition and encapsulation methods to ensure stability and longevity. These processes are not only labor-intensive but also demand high-quality raw materials, further inflating production expenses.

As a result of these factors, the retail price of quantum dot displays remains significantly higher than that of traditional LCD or OLED displays. According to the research 70% of manufacturers cited high production costs as a barrier to scaling up quantum dot technology. Consequently, while the performance benefits of quantum dot displays are compelling, the elevated costs pose challenges for widespread adoption in consumer electronics and other industries, limiting their penetration in the market despite their technological advantages.

Quantum Dot Display Market Segment Analysis:

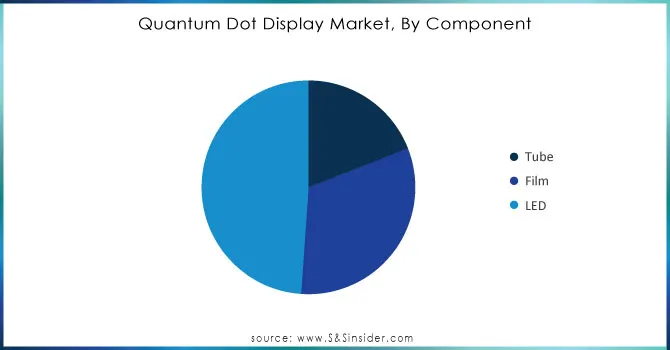

By Component

In 2025E, the LED segment dominated the market, contributing 48.9% of total revenue. LEDs are essential in quantum dot display technologies, serving as the primary light source. The integration of quantum dots enhances the color performance of LEDs, allowing for richer and more vibrant visuals. This synergy between LEDs and quantum dots results in displays with improved color accuracy and brightness. Furthermore, LEDs offer significant design flexibility, enabling innovative display configurations that are not possible with traditional lighting solutions. Their compatibility with quantum dot films allows for efficient manufacturing processes, leading to compact display designs that can be produced at a lower cost than older technologies including bulky glass tubes.

Do You Need any Customization Research on Quantum Dot Display Market - Inquire Now

By Material

In 2025E, cadmium-containing quantum dot (QD) displays captured a significant quantum dot display market share of 53.08%, primarily due to their outstanding ability to reproduce a wide color gamut. This capability enables the production of displays with vibrant and highly accurate colors, which is particularly important for manufacturers of high-definition televisions and other premium display technologies. Additionally, cadmium-based quantum dots boast superior light-emitting efficiency, allowing for higher brightness levels without the need for increased power consumption. This energy efficiency not only enhances the viewing experience for consumers but also reduces operating costs for manufacturers. As a result, the demand for cadmium-containing QD displays continues to grow, as they meet the expectations for quality and performance in today’s competitive market.

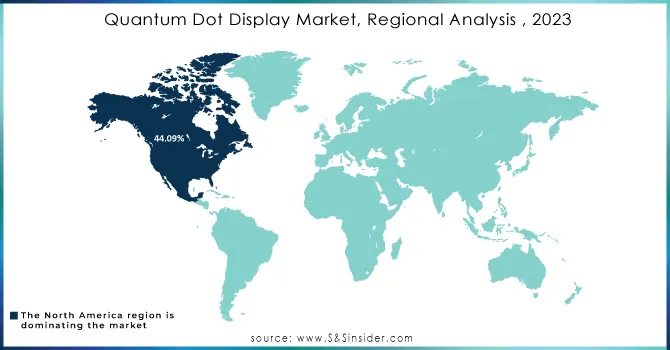

Quantum Dot Display Market Regional Analysis:

North America Quantum Dot Display Market Insights

In 2025E, North America dominated the market with a notable share of 44.09%, driven by its concentration of leading technology firms specializing in advanced display solutions. The consumer shift toward premium display options, including 4K, UHD, QLED, and 8K screens, further propels the quantum dot display market growth. According to research, approximately 70% of consumers in North America prioritize high-resolution displays for enhanced viewing experiences, reflecting a strong demand for cutting-edge visual technologies. Additionally, the adoption of quantum dot displays, known for their superior color accuracy and energy efficiency, is gaining traction, further supporting the region's leadership in the quantum dot display market.

Asia Pacific Quantum Dot Display Market Insights

The Asia Pacific region is poised for rapid growth in the adoption of quantum dot display technology, driven by rising disposable incomes among the working population. As consumers gain more purchasing power, there is an increased demand for advanced consumer electronics, notably smartphones, televisions, and tablets, which benefit significantly from quantum dot technology. This technology enhances picture quality, offering vibrant colors and improved energy efficiency compared to traditional displays. Additionally, governments in the Asia Pacific are actively encouraging the use of energy-efficient technologies through subsidies and regulations, further supporting the transition to quantum dot displays. As a result, the region is expected to lead in the implementation of this cutting-edge display technology, aligning consumer preferences with sustainability initiatives.

Europe Quantum Dot Display Market Insights

Europe’s Quantum Dot Display market is driven by premium consumer electronics, strong 4K/8K adoption, and increasing preference for energy-efficient high-brightness displays. Demand from smart TVs, gaming monitors, and digital signage is accelerating. Leading OEMs leverage cadmium-free QD materials, with sustainability regulations pushing manufacturers toward environmentally compliant production.

Latin America (LATAM) and Middle East & Africa (MEA) Quantum Dot Display Market Insights

LATAM and MEA Quantum Dot Display markets are in a growth phase, led by expanding middle-class consumer electronics demand and rising adoption of advanced TVs. Telecom modernization, e-commerce penetration, and increasing urban digital transformation support display upgrades. Falling premium panel costs and retail availability are accelerating regional QLED and QD-enhanced device adoption.

Quantum Dot Display Market Key Players:

-

Samsung Electronics Co., Ltd. (QD-OLED Displays, QLED TVs)

-

LG Display Co., Ltd. (QD-OLED Panels, Quantum Dot TV)

-

Sony Corporation (Triluminos Displays)

-

Sharp Corporation (4K Quantum Dot TVs)

-

The Dow Chemical Company (Quantum Dot Materials)

-

3M Company (Quantum Dot Enhancement Film)

-

Nanosys, Inc. (Quantum Dot Enhancement Film (QDEF))

-

TCL Corporation (QD TVs)

-

BOE Technology Group Co., Ltd. (Quantum Dot Display Panels)

-

Innolux Corporation (Quantum Dot Displays)

-

AU Optronics Corp. (Quantum Dot LCD Panels)

-

Nanoco Group plc (Cadmium-Free Quantum Dots)

-

InVisage Technologies (Apple) (Quantum Film for Imaging Sensors)

-

Shoei Electronic Materials, Inc. (Quantum Dot Solutions)

-

NN-Labs (NNCrystal US Corporation) (Quantum Dot Materials)

-

Ocean NanoTech (High-Purity Quantum Dots)

-

QD Laser (Quantum Dot Lasers)

-

QLight Nanotech (Quantum Dot Films)

-

Quantum Materials Corporation (Cadmium-Free Quantum Dot Materials)

-

CSOT (China Star Optoelectronics Technology Co., Ltd.) (QD Display Technology)

Competitive Landscape for Quantum Dot Display Market:

Samsung Display is a global leader in advanced display technologies, driving innovation in OLED, QD-OLED, and QLED panel manufacturing. The company supplies high-performance displays for TVs, smartphones, IT devices, and automotive systems. Its quantum dot advancements enable superior brightness, color accuracy, and energy efficiency, positioning it at the forefront of premium display markets.

-

In October 2024: Samsung Display has developed a quantum dot ink recycling technology that enhances the efficiency of its QD-OLED manufacturing process. This innovation enables the recovery and reprocessing of up to 80% of unused QD ink, significantly reducing waste. By adopting this technology, the company anticipates annual cost savings exceeding KRW 10 billion approximately USD 7.2 million.

Shoei Chemical, Inc. specializes in advanced materials for the electronics and display sectors, particularly high-purity quantum dot solutions. Its products support next-generation QLED, MicroLED, and display enhancement technologies by delivering superior color stability, brightness, and durability. The company’s materials enable manufacturers to achieve high-performance, cadmium-free display applications in consumer electronics and imaging systems.

-

In September 2023: Shoei Chemical, Inc. and its North America-based subsidiary, Shoei Electronic Materials, Inc., revealed their acquisition of Nanosys, Inc., a leader in quantum dot technology. This strategic move is anticipated to enhance Shoei's position within the advanced materials sector.

Nanoco Technologies is a leading developer of cadmium-free quantum dot materials used in next-generation displays, sensors, and imaging systems. The company’s patented CFQD® technology enables environmentally compliant quantum dot solutions with high color accuracy and efficiency. Nanoco works with global display manufacturers to enhance QLED performance and accelerate sustainable display innovation.

-

In May 2023: Nanoco Technologies entered into a licensing and collaboration agreement with Guangdong Poly Optoelectronics Co., Ltd. Under this agreement, the two companies will work together to develop cadmium-free quantum dot solutions for various applications, including advanced displays and lighting films. Additionally, this partnership will enable Nanoco to promote its eco-friendly CFQD quantum dots in China.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 5.52 Billion |

| Market Size by 2033 | USD 12.19 Billion |

| CAGR | CAGR of 10.41% From 2026 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2026-2033 |

| Historical Data | 2021-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Tube, Film, LED) • By Material (Cadmium Containing, Cadmium-free) • By Application (Consumer Electronics, Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsung Electronics Co., Ltd., LG Display Co., Ltd., Sony Corporation, Sharp Corporation, The Dow Chemical Company, 3M Company, Nanosys, Inc., TCL Corporation, BOE Technology Group Co., Ltd., Innolux Corporation, AU Optronics Corp., Nanoco Group plc, InVisage Technologies (Apple), Shoei Electronic Materials, Inc., NN-Labs (NNCrystal US Corporation), Ocean NanoTech, QD Laser, QLight Nanotech, Quantum Materials Corporation, CSOT (China Star Optoelectronics Technology Co., Ltd.) |