Residential Energy Storage Market Report Scope and Overview:

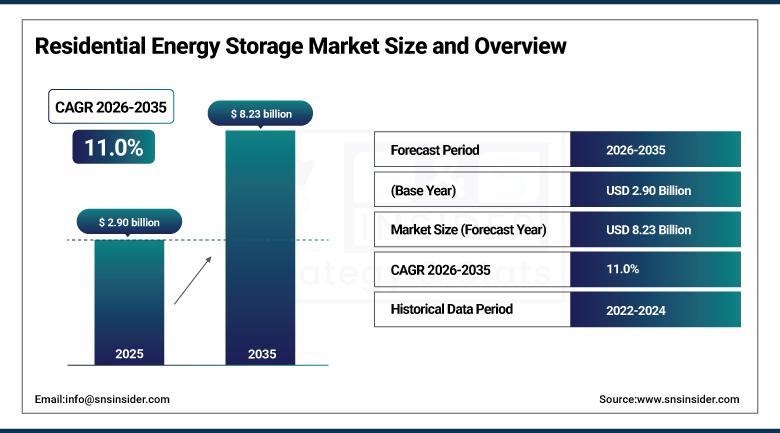

The Residential Energy Storage Market size was valued at USD 2.90 Billion in 2025 and is projected to reach USD 8.23 Billion by 2035, registering a CAGR of 11.0% from 2026 to 2035.

The residential energy storage market is about the sales of energy storage technologies meant for residential buildings such as houses, providing homeowners with the possibility of storing energy from solar panels and the grid at those periods of time when electricity is cheaper. It may be used by homeowners when there is the need for more energy during peak hours or even during a power outage since these systems include batteries, inverters, and the system of monitoring that enables tracking of energy production and consumption. Residential energy storage systems have become more and more popular owing to additional load that grids have now in some areas because of the intermittent supply of renewable energy and aged grid infrastructure and more and more frequent extreme weather conditions which cause increased costs and even local power outages.

Tesla's Powerwall remains a market leader due to its seamless integration with solar panels and advanced energy monitoring features, with the company continuing to expand production capacity throughout 2025 to meet growing residential demand for reliable, solar-integrated backup power solutions across increasingly grid-strained markets worldwide.

Market Size and Forecast

-

Market Size in 2026E: USD 3.22 Billion

-

Market Size by 2035: USD 8.23 Billion

-

CAGR: 11.0% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information Residential Energy Storage Market - Request Free Sample Report

Residential Energy Storage Market Trends

-

Residential energy storage systems continue increasingly integrating with solar installations and smart home infrastructure, improving energy reliability and self-consumption.

-

Technological advancement in battery chemistry, power electronics, and energy management software continues shaping market development.

-

The declining cost of battery technologies, particularly lithium-ion systems, continues strengthening the business case for residential energy storage deployment.

-

Grid instability, extreme weather, and climate change events continue pushing consumers to seek genuine backup power independence at home.

-

Solar plus storage packages continue becoming increasingly common, particularly across regions with favorable net metering reforms.

US Residential Energy Storage Market Size Outlook

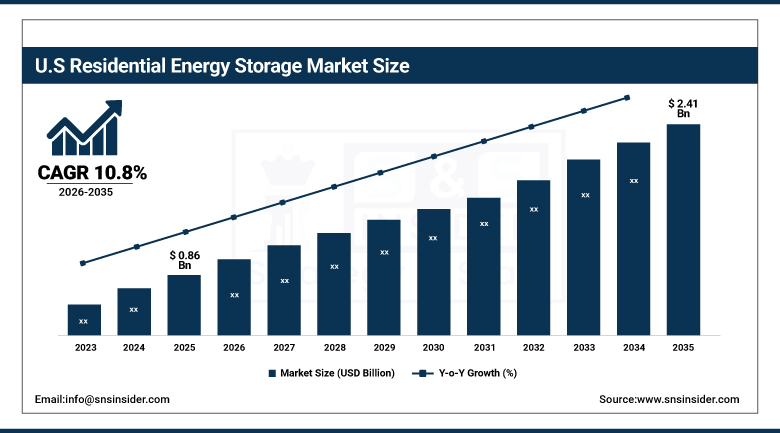

The US Residential Energy Storage Market was valued at approximately USD 0.86 Billion in 2025 and is projected to reach approximately USD 2.41 Billion by 2035, registering a CAGR of approximately 10.8% from 2026 to 2035.

The growth of the market for battery storage systems has been impressive over the past few years, with the fast-growing American residential energy storage market continuing to lead the commercial and utility battery storage systems market in terms of growth rate. America remained the biggest global residential energy storage market, due to rising number of blackouts and the rising demand for genuine energy independence among consumers during the year. Rising instances of grid instability, extreme weather conditions, and climate change events such as fires and storms continued to drive American consumers towards looking for ways to have reliable backup power at home, while government policies and incentives were helping make the cost of residential energy storage solutions more affordable for them.

Enphase Energy continued adding to its residential battery storage and solar integration solutions during 2025, with the target being the American homeowners who are looking for a solar plus storage solution that can provide them with true backup power resilience.

Residential Energy Storage Market Segment Analysis

-

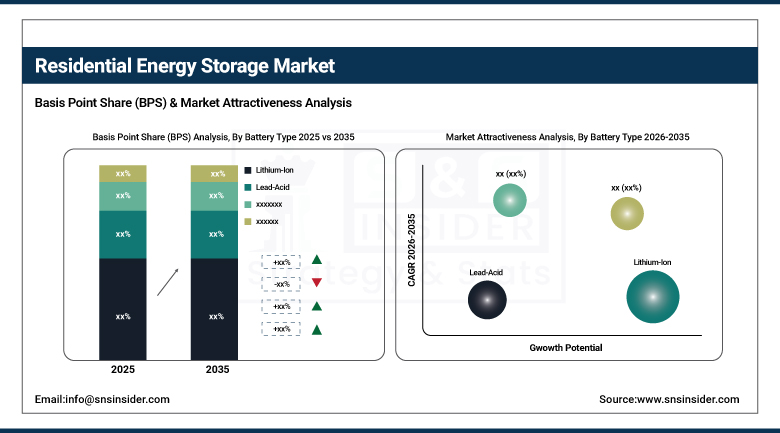

By Battery Type, Lithium-Ion led the market with the largest share in 2025, while Lead-Acid held approximately 19% share, primarily supported by lower upfront cost and established technology base.

-

By Component, Battery led the market with the largest share in 2025, while Software and Monitoring was the fastest-growing component, tracking rising smart home integration demand.

-

By Grid Connectivity, On-Grid led the market with the largest share in 2025, while Off-Grid was the fastest-growing connectivity type, tracking rising remote and rural adoption.

By Battery Type, Lithium-Ion led the market, emerging chemistries grew fastest

Lithium-ion held the dominant battery-type share in 2025, with the segment continuing to witness genuinely robust growth given its superior energy density, longer cycle life, and lower maintenance requirements relative to legacy alternatives. Companies including Tesla, LG Energy Solution, Sonnen, BYD, and Enphase Energy continued dominating the market by offering lithium-ion battery solutions with enhanced efficiency, longevity, and smart energy management capabilities, keeping this chemistry the clear dominant category by a considerable margin.

Lead-acid batteries continued holding a genuinely meaningful residual share of nearly 19%, primarily due to their lower upfront cost and established technology base that continues appealing to genuinely price-sensitive residential customers. Emerging chemistries, including flow batteries and next-generation solid-state technology, continue advancing at the fastest pace among battery types as manufacturers pursue genuinely improved safety, longevity, and environmental profiles beyond what conventional lithium-ion and lead-acid alternatives can currently deliver.

By Component, Battery led the market, Software and Monitoring grew fastest

The Battery component held the largest share of the market, reflecting its role as the single most capital-intensive element of every residential energy storage installation. That combination of genuine cost concentration and foundational technical necessity kept battery hardware the dominant component category across the broadest range of residential installations this market serves.

Software and Monitoring is recording the fastest growth among components during the forecast period. Residential energy storage systems continue increasingly integrating with solar installations and smart home infrastructure, and homeowners increasingly expect sophisticated monitoring mechanisms that let them track energy consumption and production in genuinely granular detail, keeping this component category's growth rate climbing ahead of the broader, still-dominant battery hardware segment.

By Grid Connectivity, On-Grid led the market, Off-Grid grew fastest

On-Grid systems held the largest share of grid-connectivity revenue in 2025, reflecting widespread grid connectivity and genuine net-metering benefits that continue making grid-tied residential energy storage the practical default choice for the vast majority of homeowners. That combination of established utility infrastructure integration and genuine financial incentive alignment kept on-grid systems the dominant connectivity category across the broadest range of residential markets this report covers.

Off-Grid systems are recording the fastest growth among connectivity types during the forecast period, as remote and rural areas increasingly adopt storage solutions where grid access remains genuinely limited. That expanding addressable market beyond traditional grid-connected suburban and urban installations keeps off-grid systems' growth rate climbing ahead of the broader, still-dominant on-grid category as residential energy storage continues reaching increasingly remote and underserved geographies.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.90% |

|

Europe |

Germany |

24.30% |

|

Asia Pacific |

China |

32.05% |

|

Middle East and Africa |

UAE |

26.20% |

|

Latin America |

Brazil |

34.45% |

North America Residential Energy Storage Market Insights

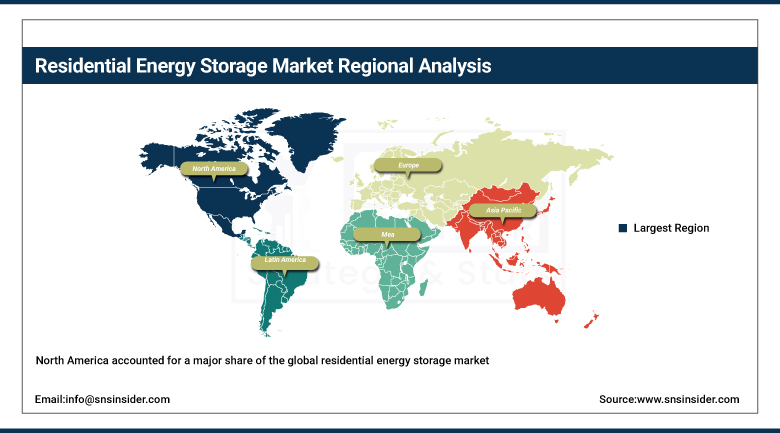

North America accounted for a major share of the global residential energy storage market, driven by increasing frequency of power outages and rising consumer demand for genuine energy independence across the continent. Grid assets continuing to age, combined with severe weather increasingly worsening bottlenecks and choke points in the energy delivery system, continued reinforcing this dominant regional position throughout the year.

The United States accounted for roughly 80.90% of regional revenue, anchored by its position as the leading global residential energy storage market and rapid growth outpacing commercial and utility battery storage segments. Canada added further regional demand through its own growing residential solar and storage adoption, and that combined strength kept North America the largest addressable market for residential energy storage vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Residential Energy Storage Market Insights

Europe held a meaningful share of global revenue, supported by favorable net metering reforms and growing solar-plus-storage package adoption across the region's major economies. Continued government incentive support for energy-efficient technologies kept reinforcing steady European demand for residential energy storage throughout the year.

Germany led demand at roughly 24.30% of European revenue, supported by its substantial residential solar adoption and favorable net metering policy environment. The UK and France contributed substantial additional demand, and continued European regulatory support for distributed energy resources should keep regional demand climbing through the forecast period.

Asia Pacific Residential Energy Storage Market Insights

Asia Pacific is advancing at the fastest pace among all regions tracked in this report, driven by rapidly industrializing developing economies and expanding residential solar adoption across the region's largest economies. Supportive government policies and incentives to promote energy-efficient technologies, including tax benefits, low-interest loans, and grants, continued driving regional adoption well ahead of every other region tracked in this report.

China led the pack, supported by its massive residential solar installation base and rapidly growing domestic battery manufacturing capability. Japan and South Korea contributed meaningful additional demand through their own established residential solar and storage adoption, and that broadening base of regional demand continued reinforcing Asia Pacific's position as the fastest-growing market tracked in this report.

MEA and Latin America Residential Energy Storage Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding residential solar adoption, growing grid reliability challenges, and rising government focus on energy access across both areas. As these markets continued developing modern residential energy infrastructure, storage adoption grew correspondingly from a considerably smaller base than in more mature residential energy storage markets.

The UAE led Middle East and Africa demand, supported by substantial residential solar investment and growing interest in energy independence solutions. Saudi Arabia contributed further demand through its own energy diversification programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing residential solar adoption continuing to anchor regional demand for energy storage systems.

Market Dynamics

Growth Drivers: Grid Reliability Concerns and Rising Power Outage Frequency

The residential energy storage system is gaining traction due to increased strain on the grid in many regions and the intermittent nature of renewable energy. Grid assets continue aging, and severe weather continues worsening bottlenecks and choke points in the energy delivery system, resulting in higher costs and threatening increased local power outages, with the increasing frequency of power outages serving as a significant driver for market growth.

Utilities continue deploying residential energy storage systems to replace thermal power plants, support renewable generation, and improve grid reliability and resilience. The residential energy storage system remains a genuinely flexible and valuable resource, improving efficiency for both system owners and the broader power grid, and that combination of genuine grid necessity and consumer-level energy independence appeal is exactly what keeps demand climbing at such a sustained pace across virtually every major consuming region.

Restraints: High Upfront System Costs and Complex Installation Requirements

High upfront costs for residential energy storage systems continue posing a genuine restraint on faster market-wide adoption, particularly among cost-sensitive homeowners without access to favorable financing or government incentive programs. That cost barrier has kept the most sophisticated lithium-ion residential storage installations concentrated among genuinely well-resourced households, even as lead-acid alternatives continue serving more price-sensitive customer segments.

The technical complexity of integrating battery storage, inverters, and monitoring systems with existing residential electrical infrastructure and, frequently, existing solar installations continues posing genuine installation challenges. That integration burden keeps professional installation genuinely necessary for most residential deployments, adding real cost and scheduling complexity beyond the storage equipment itself.

Opportunities: Smart Home Integration and Off-Grid Market Expansion

Residential energy storage systems increasingly integrating with solar installations and smart home infrastructure represents a genuinely significant opportunity, as this software and monitoring component category's fastest-growing status among all segments tracked in this market reflects genuine homeowner demand for sophisticated energy management capability. Vendors offering genuinely well-integrated, smart-home-compatible monitoring platforms stand to capture meaningful share as residential energy management continues converging with broader home automation trends.

Expanding off-grid adoption in remote and rural areas offers a second substantial opportunity, as this connectivity category's fastest-growing status reflects genuine demand from geographies where grid access remains limited. Vendors with proven, genuinely reliable off-grid residential storage technology stand to capture meaningful share as this application continues expanding well beyond the market's traditional grid-connected suburban and urban stronghold.

Recent Developments:

-

2025: Sonnen continued expanding its virtual power plant and smart home battery integration technology, targeting homeowners seeking to participate in grid balancing programs while maintaining genuine backup power resilience.

-

2025: BYD continued advancing its residential battery storage product portfolio, targeting global homeowners seeking cost-competitive, reliable lithium-ion energy storage solutions integrated with residential solar installations.

-

2024: Huawei continued expanding its residential energy storage and smart home energy management platform, targeting homeowners seeking integrated solar, storage, and monitoring capability across an increasingly connected home ecosystem.

Residential Energy Storage Market key players are:

-

Tesla, Inc.

-

LG Energy Solution Ltd.

-

Sonnen GmbH

-

BYD Company Limited

-

Enphase Energy, Inc.

-

Huawei Technologies Co., Ltd.

-

Samsung SDI Co., Ltd.

-

AlphaESS Co., Ltd.

-

Siemens AG

-

Toshiba Corporation

-

Generac Holdings Inc.

-

SolarEdge Technologies, Inc.

-

Panasonic Holdings Corporation

-

SunPower Corporation

-

Schneider Electric SE

-

Eaton Corporation plc

-

FranklinWH Energy Storage Inc.

-

Fortress Power LLC

-

Growatt New Energy Co., Ltd.

-

GoodWe Technologies Co., Ltd.

Residential Energy Storage Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.90 Billion |

| Market Size by 2035 | USD 8.23 Billion |

| CAGR | CAGR of 11.00% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Battery Type (Lithium-Ion, Lead-Acid, and Others) • by Component (Battery, Inverter and Power Conversion System, and Software and Monitoring) • by Grid Connectivity (On-Grid and Off-Grid) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Tesla, Inc., LG Energy Solution Ltd., Sonnen GmbH, BYD Company Limited, Enphase Energy, Inc., Huawei Technologies Co., Ltd., Samsung SDI Co., Ltd., AlphaESS Co., Ltd., Siemens AG, Toshiba Corporation, Generac Holdings Inc., SolarEdge Technologies, Inc., Panasonic Holdings Corporation, SunPower Corporation, Schneider Electric SE, Eaton Corporation plc, FranklinWH Energy Storage Inc., Fortress Power LLC, Growatt New Energy Co., Ltd., GoodWe Technologies Co., Ltd. |

Frequently Asked Questions

The Residential Energy Storage Market is expected to grow at a CAGR of approximately 11.0% from 2026 to 2035, based on triangulated secondary research estimates.

The Residential Energy Storage Market was valued at approximately USD 2.90 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is increased strain on the grid combined with the intermittent nature of renewable energy and increasing frequency of power outages.

The Lithium-Ion segment dominated the Residential Energy Storage Market by battery type, reflecting its superior energy density and longer cycle life in 2025.

North America dominated the Residential Energy Storage Market in 2025, driven by increasing frequency of power outages and rising consumer demand for energy independence.

Get in Touch