Reverse Factoring Market Report Scope & Overview:

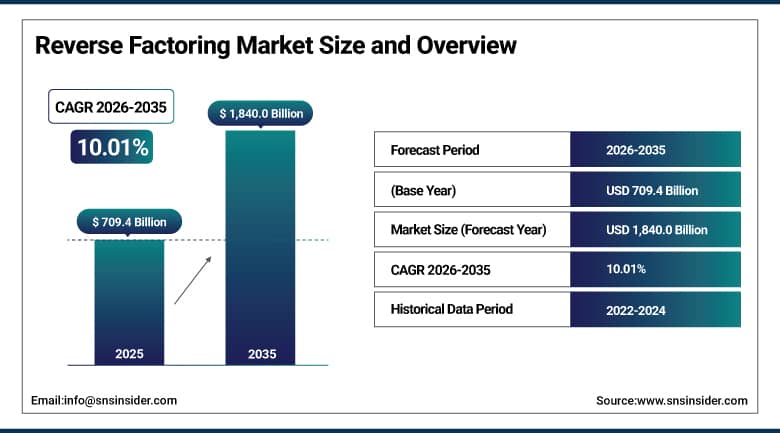

Reverse Factoring Market Market was valued at USD 709.4 billion in 2025 and is expected to reach USD 1,840.0 billion by 2035, growing at a CAGR of 10.01% from 2026–2035.

The Reverse Factoring Market is burgeoning as enterprises (SMEs and MNCs) in various industries/touchpoints continue to adopt supply chain finance solutions for maximizing working capital, enhancing supplier relationships, and improving liquidity management. Reverse factoring–responsible for some supplier finance–is where suppliers can use a financial institution to get early payment on approved invoices or to have extended buyer payment terms. Increasing globalization of supply chains, digitization of financial services and expansion of fintech-bank partnerships are driving adoption across manufacturing, healthcare, retail and transportation industries worldwide.

Across industry studies, the data consistently tell you that enterprises that benefit from reverse factoring programs see quantifiable enhancements in supplier stability, payment predictability and working capital efficiency with large buyers reporting supplier exit-level reductions of upwards of 30% and financing cost improvements as high as 15–25 basis points compared to traditional bank credit facilities for suppliers.

More recently, regulatory frameworks across the European Union, the United Kingdom and North America have increasingly supported an effort to provide transparency and standardization of supply chain finance practices which has fostered greater confidence among financial institutions and corporates in reverse factoring becoming a mainstream liquidity management instrument.

Reverse Factoring Market Size and Forecast

-

Market Size in 2025: USD 709.4 Billion

-

Market Size by 2035: USD 1,840.0 Billion

-

CAGR: 10.01% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Reverse Factoring Market - Request Free Sample Report

Reverse Factoring Market Trends

-

Accelerating adoption of AI and machine learning for real-time supplier credit assessment and dynamic discount pricing within reverse factoring platforms.

-

Growing integration of blockchain technology to enhance transparency, immutability, and settlement efficiency in reverse factoring transactions.

-

Rising demand from SMEs for accessible, technology-enabled reverse factoring programs as alternative working capital solutions.

-

Expanding cross-border reverse factoring programs driven by globalization of supply chains and growth in international trade volumes.

-

Increasing ESG-linked supply chain finance programs incentivizing supplier sustainability improvements through favorable financing terms.

-

Growing involvement of Non-Banking Financial Institutions (NBFIs) and fintech platforms challenging traditional bank-dominated reverse factoring markets.

-

Rising healthcare sector adoption of reverse factoring to address liquidity challenges among medical device and pharmaceutical suppliers.

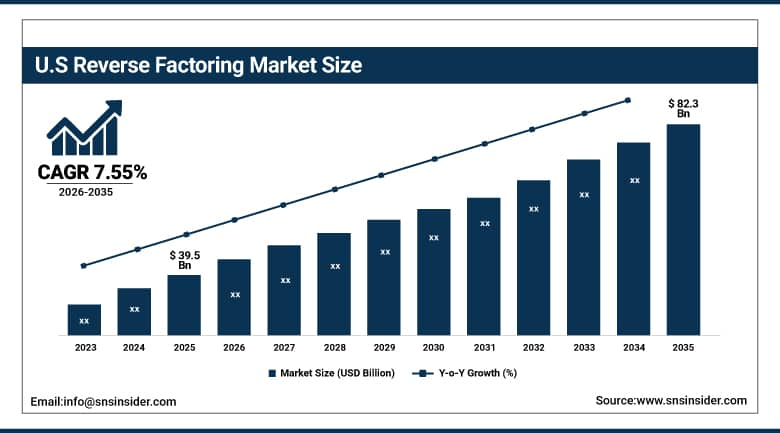

The U.S. Reverse Factoring Market was valued at USD 39.5 billion in 2025 and is expected to reach USD 82.3 billion by 2035, registering a CAGR of 7.55% during 2026–2035.

U.S. Reverse Factoring Market is developing rapidly due to the rapid expansion of financial technology adoption, broad participation of SMEs in supply chain finance programs and strong fintech-bank partnerships. As we have talked about in previous articles, big U.S. corporations including retailers, manufacturers and technology companies are utilizing reverse factoring platforms to provide liquidity support for their supplier ecosystem. Federal Reserve financial stability frameworks coupled with rising corporate sustainability commitments toward supplier economic health are other market adoption accelerants.

Strengthened by their rapid digitization and broader adoption of blockchain-based supply chain finance platforms, in tandem with AI-powered credit scoring, U.S. trade finance is moving faster and transparently addressing reverse factoring transactions that are attracting a more extensive supplier participant base outside the traditional large-enterprise channel.

Reverse Factoring Market Segment Insights

-

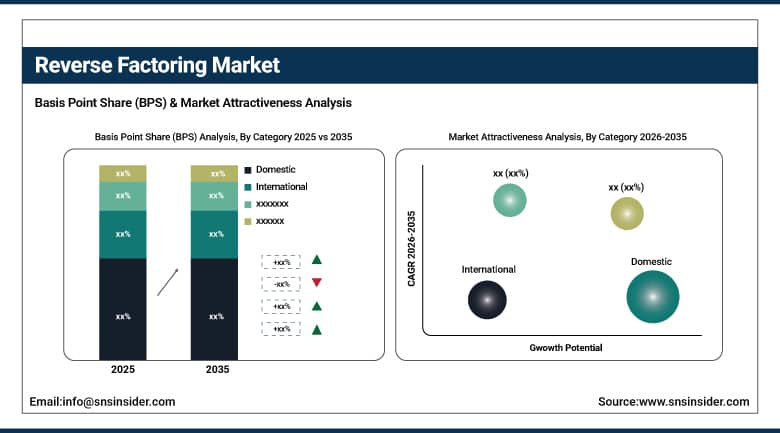

Based on Category, Domestic segment accounted for the largest market share in 2025; International segment is expected to be the fastest-growing segment during the forecast period.

-

Based on Financial Institution, Banks accounted for the largest market share in 2025; Non-banking Financial Institutions (NBFIs) are expected to be the fastest-growing segment during the forecast period.

-

Based on End-Use, Manufacturing accounted for the largest market share in 2025; Transport & Logistics is expected to be the fastest-growing segment during the forecast period.

Reverse Factoring Market Segment Analysis

By Category, Domestic segment dominates, International expected to grow fastest

In 2025, the domestic segment dominated the market with a share of about 91.7% of total reverse factoring revenue generated globally. Established frameworks of legal acceptance and the reduced cross-border compliance complexity, well-developed networks of trusted originators amongst financial institutions and ease of connecting with ERP systems contribute to domestic reverse factoring programs which remain the most appealing option for most buyers along with their national supplier bases.

For instance, the international segment is expected to grow at the fastest CAGR of 13.34% over the forecast period. Cross-border reverse factoring has other barriers, like being blocked by currency risk, jurisdictional complexity and correspondent banking but here several factors come into play globalization of supply chains, cross-border processes have been simplified or multinational manufacturing and retail operations establish factories in countries with lower production costs with the expansion of digital trade finance platforms.

By Financial Institution, Banks dominate, NBFIs expected to grow fastest

In 2025, the largest market share by revenue and the better competitive position was held by Banks segment with ~80.49% of reverse factoring revenue. Leading global banks such as HSBC, Santander, BNP Paribas and JPMorgan Chase have built extensive reverse factoring platforms supported by an expansive corporate client base, large capital pools, and backstop risk management capabilities helping retain their incumbent positions.

You will likely also like: Segment NBFIs (Non-Banking Financial Institutions) is expected to attain the fast CAGR with 11.57% until 2035 AI-based onboarding, on-demand transaction processing and flexible financing structures that grow with mid-market buyers (and their suppliers) are all driving a shift in the traditional banking model, which fintech companies and alternative finance providers have no clear path to replicating. This disruption is being led by such companies as C2FO, Taulia and PrimeRevenue who are stealing market share with low-cost, tech-enabled supply chain finance solutions.

By End-Use, Manufacturing dominates, Healthcare expected to grow fastest

The Manufacturing revenue segment was the largest with share of ~29.79% in 2025, owing to capital intensive manufacturing supply chains and supplier practicing stability cash flows for raw materials procurement to avoid disruption on production line due to labor payment as well as other payments during raw material shortage. Overseas, reverse factoring programs have thus far been adopted most extensively by large automotive, electronics and industrial manufacturers.

Due to increasing computerised x-ray analysis and digital pathology, the Healthcare segment is anticipated to post fastest CAGR over 2026 to 2035. Increasing complexity and cost squeezes in healthcare supply chains coupled with robust demand for medical devices, pharmaceuticals, and hospital supplies are creating a significant new driver of reverse factoring. The growing importance of organization-wide working capital for things like operational investments and shifts to value-based care is facing an obstacle in the form of supplier liquidity, which healthcare supply chain finance is solving.

Reverse Factoring Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

United Kingdom |

59% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

52% |

Europe Reverse Factoring Market Insights

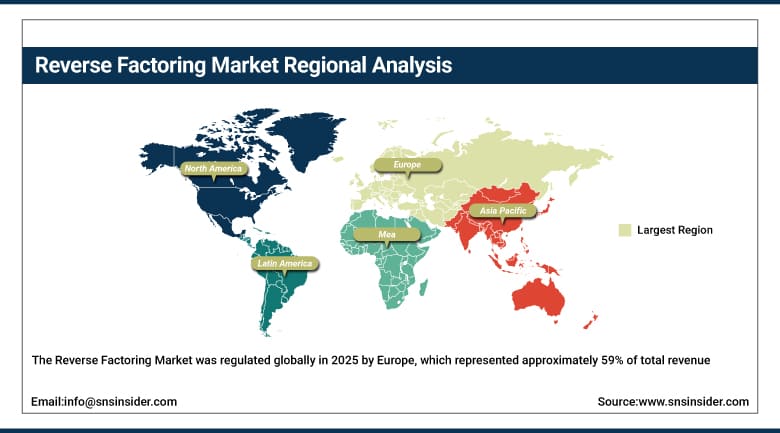

The Reverse Factoring Market was regulated globally in 2025 by Europe, which represented approximately 59% of total revenue. Its market leadership is bolstered by the region's strong regulatory frameworks supporting supply chain finance (especially for prevalent reverse factoring), well-developed financial infrastructure, and high corporate awareness of reverse factoring as a working capital tool. Leading global markets with a highly developed reverse factoring ecosystems led by large manufacturers and retailers, and their large supplier networks are Germany, France, the UK, Spain, and the Netherlands. The availability of European Central Bank liquidity policies in turn has supported how attractive supply chain finance rates are for buyers and financial institutions alike.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Reverse Factoring Market Insights

North America accounted for nearly 20% of global Reverse Factoring Market revenue in 2025. In the region, The United States is the most dominant market supported by huge corporate supply chain finance programs, active fintech presence and a mature financial services ecosystem. North America is anticipated to continue generating sales through 2035, driven by growing SME integration and expansion of ESG-linked supply chain finance.

Asia Pacific Reverse Factoring Market Insights

The Asia Pacific region accounted for around 16% of the global revenue in 2025 and is predicted to witness the second-highest growth during the forecast period. The mighty Chinese manufacturing industry, the emerging Asian corporate finance market in India and an increase in international trade volumes coming from Southeast Asia are some of the big drivers for demand. Market development is further expedited by government-backed supply chain finance initiatives in various regions, and the presence of digital finance platforms on a regional scale.

Middle East & Africa and Latin America Reverse Factoring Market Insights

The Middle East & Africa and Latin America Reverse Factoring Markets are accounted as emerging high growth reverse factoring markets due to the fact that they are backed with traditionally low trade volumes, a rise in financial inclusion initiatives and an on-going digital transformation of trade finance ecosystems. Brazil takes the pole position in Latin America and Gulf countries implement supply chain finance programs as part of broader economic diversification plans. The reverse factoring adoption is gaining traction in both the regions due to rising cross border trade and entry of international financial institutions.

Reverse Factoring Market Growth Drivers:

-

Increasing demand for working capital optimization and supply chain liquidity management

Continued corporate demand to effectively facilitate working capital management despite the rise of extended payment terms, supply chain disruptions and increased cost of finance is the primary growth driver for the Reverse Factoring Market. Reverse factoring is a highly attractive choice since it provides simultaneous benefits to buyers (extended payment terms, improved cash flow) and suppliers (access to early payment at lower financing cost), creating an auto-reinforcing cycle of adoption. This is why, with the implementation of global supply chains, along with their critical role to continuously keep running in case one supplier gets financial issues, reverse factoring has grown from a financing instrument to become as current as an important risk management tool.

The COVID-19 pandemic combined with subsequent supply chain disruptions and shocks have moved executive awareness of supplier financial risk from an occasional agenda point to a systemic business risk that must be actively managed, driving the adoption of reverse factoring programs by large corporations defending their supplier health management strategies within manufacturing, retail, healthcare and technology sectors around the globe.

Reverse Factoring Market Restraints

-

Lack of standardization and regulatory complexity limiting global scalability

The absence of harmonized global standards for disclosure, accounting treatment and regulatory classification limits Reverse Factoring Market growth. Uncertain national accounting standards on whether reverse factoring programs are treated as trade payables or financial debt cause confusion for corporates and their auditors which may discourage the take-up of such programs. The inherent challenge of differentiating between Requirements-associated regulatory obligations for program implementation is further complicated by conflicting jurisdictional currency controls and financial institution licensing requirements on a cross-border basis.

Reverse Factoring Market Opportunities

-

Digitization and blockchain-enabled transparent supply chain finance ecosystems

Integrating Blockchain, AI & Cloud-based platforms into a reverse factoring solution is a new age growth enhancement. Through reducing fraud risk, ease of invoice authentication and real-time settlement brought by blockchain-enabled supply chain finance platforms, reverse factoring become more secure and available for wider financial institutional participants as well as suppliers segment. AI-enabled credit scoring is expanding reverse factoring advantages to sub-investment-grade suppliers who have long been locked out from bank-financed initiatives. Reverse factoring programs linked to ESG in which companies reward their suppliers for sustainability improvements with more favorable financing terms produce a new and powerful market segment aligned with corporate climate and social responsibility commitments.

Recent Developments:

-

2026: Leading fintech platforms including Taulia and C2FO expanded their AI-powered dynamic discounting capabilities, enabling real-time pricing of reverse factoring transactions based on supplier credit profiles, buyer payment history, and market liquidity conditions. ESG-linked supply chain finance programs gained significant traction, with major global corporations integrating sustainability performance metrics into reverse factoring pricing structures.

-

2025 (July): HSBC launched an enhanced digital supply chain finance platform integrating blockchain-based invoice verification and AI-driven supplier onboarding, significantly reducing program enrollment time for new supplier participants and improving transaction transparency for corporate buyers managing large, geographically distributed supply chains.

-

2024 (January): Banco Bilbao Vizcaya Argentaria (BBVA) introduced a Green Supply Chain Finance Program, providing preferential financing rates to suppliers meeting defined environmental sustainability criteria, marking a significant milestone in the integration of ESG principles into mainstream reverse factoring program design.

Reverse Factoring Market Key Players

Some of the Reverse Factoring Market Companies

-

Banco Bilbao Vizcaya Argentaria, S.A.

-

Barclays Plc

-

Credit Suisse Group AG

-

Deutsche Factoring Bank

-

Drip Capital Inc.

-

eFactor Network

-

HSBC Group

-

JP Morgan Chase & Co.

-

Mitsubishi UFJ Financial Group

-

PrimeRevenue, Inc.

-

Taulia Inc.

-

C2FO

-

Santander Corporate & Investment Banking

-

BNP Paribas

-

Greensill Capital

-

Standard Chartered

-

Citigroup Inc.

-

ING Group

-

Wells Fargo & Company

-

UBS Group AG

Reverse Factoring Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 709.4 Billion |

| Market Size by 2035 | USD 1,840.0 Billion |

| CAGR | CAGR of 10.01% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Category (Domestic, International) • By Financial Institution (Banks, Non-banking Financial Institutions) • By End-use (Manufacturing, Transport & Logistics, Information Technology, Healthcare, Construction, Others [Retail, Food & Beverages, Among Others]) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Banco Bilbao Vizcaya Argentaria, S.A., Barclays Plc, Credit Suisse Group AG, Deutsche Factoring Bank, Drip Capital Inc., eFactor Network, HSBC Group, JP Morgan Chase & Co., Mitsubishi UFJ Financial Group, PrimeRevenue, Inc., Taulia Inc., C2FO, Santander Corporate & Investment Banking, BNP Paribas, Greensill Capital, Standard Chartered, Citigroup Inc., ING Group, Wells Fargo & Company, UBS Group AG |

Frequently Asked Questions

Ans: Europe dominated the Reverse Factoring Market in 2025, accounting for approximately 59% of global market revenue.

Ans: The Domestic segment dominated the Reverse Factoring Market in 2025, accounting for approximately 91.7% of global revenue.

Ans: The increasing demand for working capital optimization, supply chain liquidity management, and the digitization of trade finance platforms enabling broader adoption across buyer-supplier ecosystems globally.

Ans: The Reverse Factoring Market was valued at USD 709.4 billion in 2025.

Ans: The Reverse Factoring Market is expected to grow at a CAGR of 10.01% from 2026 to 2035.

Get in Touch