An accurate research report requires proper strategy as well as implementation. There are multiple factors involved in the completion of a good and accurate research report, and selecting the best methodology to conduct the research is the toughest part. Since the research reports we provide play a crucial role in any company's decision-making process, we at SNS Insider always believe in choosing the methodology that delivers results closest to reality. This enables us to provide our clients with the best possible investment-to-output ratio.

Each report that we prepare requires approximately 300–350 business hours for production. Beginning with title selection, followed by in-depth brainstorming sessions, comprehensive research, validation, quality assurance, and final publishing, our team follows a structured process to ensure every report meets the highest standards of accuracy and reliability.

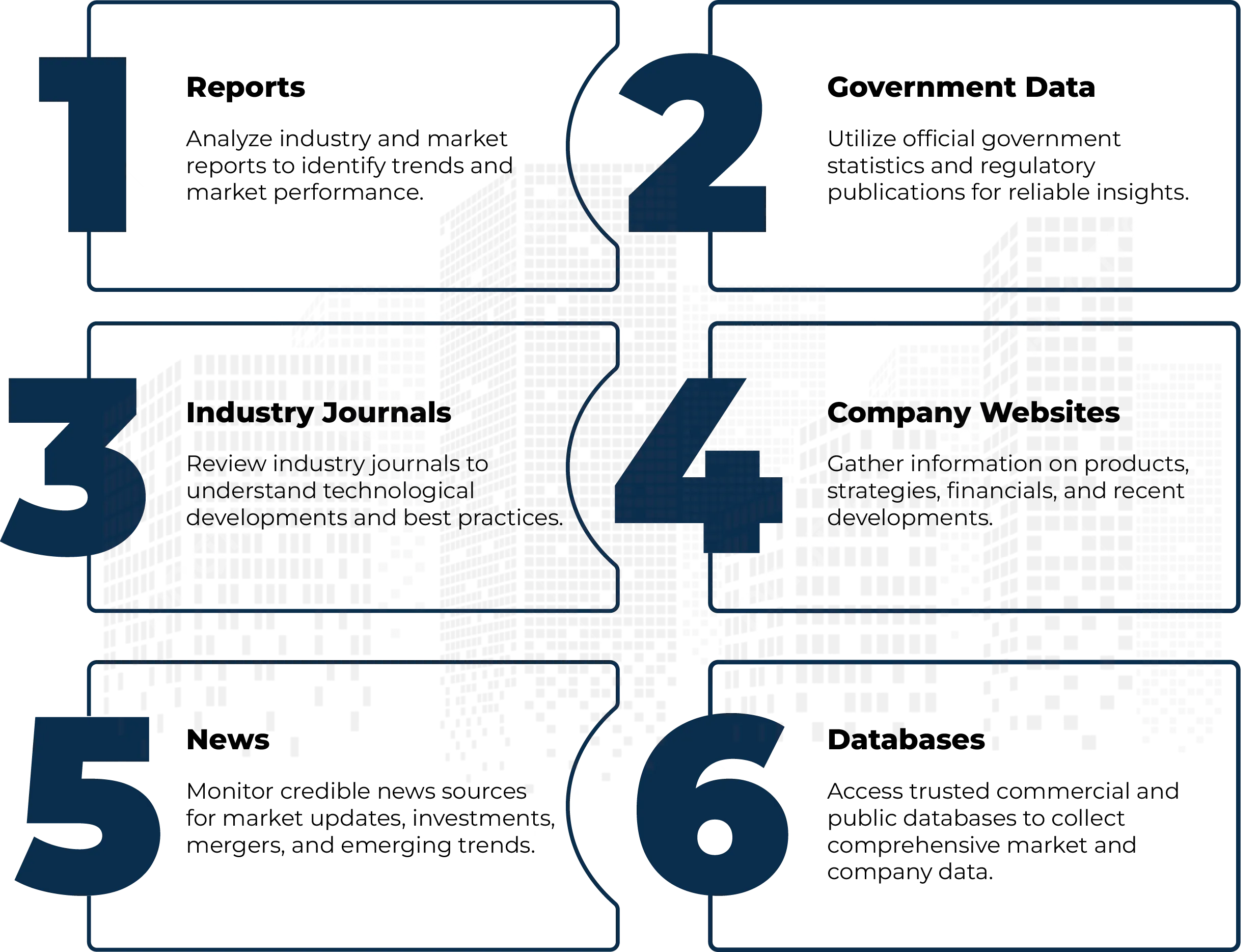

Secondary Research

Extensive secondary research is conducted to understand the market landscape and collect existing information. Multiple trusted public and commercial sources are reviewed to establish a strong research foundation before primary validation begins.

Sources typically include:

- Company annual reports and investor presentations

- Government publications and regulatory databases

- Industry associations and trade journals

- White papers and technical publications

- Company websites and press releases

- Reputable news sources and market databases

Primary Research

Primary research validates secondary findings and gathers firsthand insights from industry participants. Our analysts conduct detailed interviews with professionals across the value chain to obtain accurate market intelligence, validate assumptions, and understand current industry trends.

Interviews are conducted with:

- CEOs and Senior Executives

- Product Managers

- Sales and Marketing Professionals

- Distributors and Suppliers

- Manufacturers

- Industry Consultants

- Subject Matter Experts (SMEs)

- End Users and Customers

Market Size Estimation

The market size is estimated using multiple analytical approaches to improve accuracy:

Top-down analysis

- The analysis starts from a macro-level view, considering overall market size and industry trends.

- Large-scale data and market indicators are used to make general assumptions about the market.

- This method identifies key drivers and trends, narrowing the focus as more detailed data is explored and specific segments are examined.

- It is particularly effective for quickly evaluating market potential and regional opportunities.

Bottom-up analysis

- The process begins with gathering micro-level data, such as individual data points or small sample sets.

- This data is then aggregated and analyzed to draw broader conclusions.

- Vendor market share and contributions are assessed, providing a detailed understanding of key market players.

- This approach offers a granular view, ideal for markets with diverse segments and varied customer preferences.

Demand-side Assessment

The demand-side approach estimates market size by analyzing product consumption and purchasing patterns across various end-use industries. It focuses on understanding customer demand and market adoption.

Analyses Purchasing Behaviour of End Users

- Examines customer buying patterns, purchasing frequency, and product preferences.

- Identifies key factors influencing purchase decisions, including price, quality, and brand value.

Evaluates Demand Across Industries and Applications

- Measures product demand across different industries and application areas.

- Determines which sectors contribute the highest revenue and growth.

Estimates Consumption Volumes and Adoption Rates

- Calculates product consumption based on historical sales and usage data.

- Evaluates adoption rates of new technologies and products across industries.

Assesses Future Demand Based on Market Trends

- Forecasts future demand using economic indicators, industry developments, and statistical forecasting models.

- Considers factors such as urbanization, sustainability initiatives, and changing consumer preferences.

Supply-side Assessment

The supply-side approach estimates market size by evaluating the production capabilities and supply chain performance of manufacturers and suppliers.

Assesses Production Capacity of Manufacturers

- Evaluates manufacturing capacity, production output, and facility expansion plans.

- Identifies leading manufacturers and their production capabilities.

Evaluates Supplier Networks and Distribution Channels

- Analyses supplier relationships, distribution networks, and logistics infrastructure.

- Assesses product availability across different regions and sales channels.

Analyses Product Availability and Market Supply

- Examines inventory levels, manufacturing output, and product availability.

- Evaluates the balance between market demand and product supply.

Estimates Market Size Using Production and Shipment Data

- Calculates market size using production volumes, shipment statistics, and company revenue data.

- Validates estimates through manufacturer interviews and industry reports.

QA/QC Process

After data collection and validation, our team performs a final level of quality check and quality assurance to provide appropriate and factual data. This process includes eliminating typographical errors, removing duplicate information, validating numerical accuracy, and ensuring no important information is missing.

The QA/QC process is carried out by experienced content writers, editors, research heads, and graphics designers. Once every stage is completed successfully, the report is uploaded to our platform and made available to clients.

Report Delivery

Executive Summary

A concise overview highlighting key findings, market opportunities, competitive landscape, and future outlook to support informed decision-making.

Market Insights

Comprehensive analysis of industry dynamics, customer behaviour, technological developments, and competitive trends to identify growth opportunities.

Charts & Visualizations

Clear graphical representations of market trends, comparisons, and forecasts that simplify complex data.

Strategic Recommendations

Actionable recommendations that help organizations improve operational efficiency and strengthen their market position.

Market Forecasts

Forecasts developed using historical data, industry trends, economic indicators, and statistical models to support long-term business planning.

Frequently Asked Questions

The Rugged Servers Market is expected to grow at a CAGR of 5.5% from 2026-2035.

Ans: The Rugged Servers Market size was USD 683.72 Million in 2025 and is expected to reach USD 1167.89 Million by 2035.

Rugged servers market is driven by increasing demand for durable, high-performance computing in harsh industrial, defense, and aerospace environments.

Hardware segment dominated the Rugged Servers Market.

North America dominated the Rugged Servers Market in 2025.

Get in Touch