Semiconductor Plant Construction Market Size & Trends:

The Semiconductor Plant Construction Market was valued at USD 48.41 billion in 2025 and is expected to reach USD 143.29 billion by 2035, growing at a CAGR of 11.57% from 2026-2035.

Semiconductor Plant Construction Market trends are rapid expansion, advanced cleanroom technologies, sustainable building practices, automation integration, and increased investments in Asia-Pacific fabs. The Semiconductor Plant Construction Market is growing due to the escalating global demand for semiconductors driven by advancements in technologies such as 5G, artificial intelligence, electric vehicles, and the Internet of Things. Increasing investments in new fabrication facilities and the expansion of existing plants to support advanced node manufacturing are significant contributors.

Apple has committed to a USD 600 billion U.S. investment over four years, which includes partnerships with TSMC, Broadcom, Texas Instruments, and others to bolster domestic chip supply chains

Semiconductor Plant Construction Market Size and Forecast

-

Market Size in 2025: USD 48.41 Billion

-

Market Size by 2035: USD 143.29 Billion

-

CAGR: 11.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Semiconductor Plant Construction Market - Request Free Sample Report

Semiconductor Plant Construction Market Trends

-

Rising demand for advanced semiconductor manufacturing is driving the semiconductor plant construction market.

-

Growing adoption of cutting-edge fabrication technologies like EUV lithography is boosting plant expansion.

-

Expansion of chip manufacturing across automotive, consumer electronics, and AI applications is fueling growth.

-

Increasing focus on cleanroom design, automation, and energy-efficient infrastructure is shaping adoption trends.

-

Advancements in modular, scalable, and multi-story fab construction are improving build efficiency.

-

Rising government incentives and investments in semiconductor self-reliance programs are supporting market expansion.

-

Collaborations between construction firms, semiconductor manufacturers, and technology providers are accelerating innovation and global deployment.

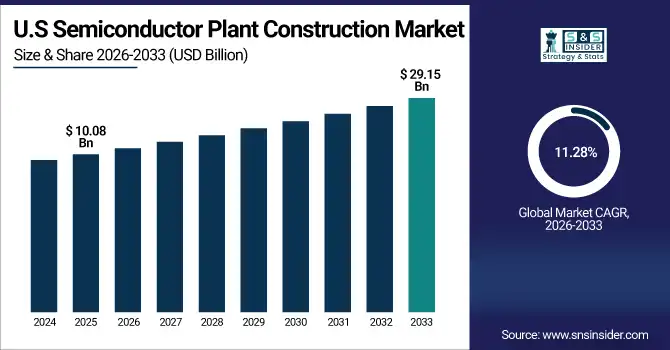

The U.S. Semiconductor Plant Construction Market was valued at USD 10.08 billion in 2025 and is expected to reach USD 29.15 billion by 2035, growing at a CAGR of 11.28% from 2026-2035. The U.S. Semiconductor Plant Construction Market is growing due to massive government incentives, major investments by leading chipmakers, increasing demand for advanced fabs, and strategic efforts to strengthen domestic semiconductor supply chains.

Semiconductor Plant Construction Market Dynamics:

Semiconductor Plant Construction Market Drivers:

-

Surging Semiconductor Demand and Government Incentives Propel Global Plant Construction and Capacity Expansion Efforts

Key market drivers fueling the global Semiconductor Plant Construction Market growth include the surging demand for semiconductors driven by rapid advancements in technologies such as 5G, artificial intelligence, electric vehicles, and the Internet of Things. Governments worldwide are offering substantial incentives and funding to boost domestic semiconductor manufacturing, encouraging companies to invest heavily in new fabrication plants and expand existing facilities. The push for cutting-edge nodes and enhanced production capacity is accelerating construction activities globally, especially in Asia-Pacific and North America, making semiconductor plants critical infrastructure for the technology ecosystem.

Intel is investing around USD 30 billion to build two new semiconductor fabrication plants in Arizona, aiming to produce advanced 7nm chips using cutting-edge technology.

Semiconductor Plant Construction Market Restraints:

-

Complex Fab Construction, Cleanroom Standards, and Project Coordination Challenge Semiconductor Plant Development Worldwide

Key challenges in the Semiconductor Plant Construction Market include the complexity of building advanced fabrication facilities that require highly specialized cleanroom environments and strict contamination controls. Designing and constructing fabs that can support rapidly evolving semiconductor technologies demands cutting-edge engineering expertise and adherence to stringent quality standards. Additionally, long project timelines and coordination across multiple specialized contractors pose significant logistical challenges.

Semiconductor Plant Construction Market Opportunities:

-

Sustainable Construction, Smart Technologies, and Emerging Markets Drive Growth in Semiconductor Plant Infrastructure

Opportunities in the market lie in adopting sustainable and energy-efficient construction methods, integrating automation and smart technologies into plant design, and developing flexible, modular cleanroom environments. Additionally, emerging markets in regions like India, Southeast Asia, and the Middle East are opening new avenues for semiconductor manufacturing infrastructure, driven by strategic diversification of supply chains and growing local demand for advanced chips.

India has approved multiple semiconductor manufacturing projects with investments totaling over USD 500 million, supported by government incentives to build local capacity and diversify supply chains.

Semiconductor Plant Construction Market Challenges:

-

Global Skilled Labor Shortages and Regulatory Challenges Hinder Semiconductor Plant Construction Progress and Timelines

Another major restraint is the global shortage of skilled labor with expertise in semiconductor manufacturing construction and maintenance, which can delay project completion. Regulatory approvals and environmental compliance add further layers of complexity, especially as governments impose stricter sustainability and safety standards. Moreover, supply chain disruptions for critical construction materials and high-tech equipment continue to impact project schedules, affecting overall market growth and timely plant commissioning.

Semiconductor Plant Construction Market Segmentation Analysis:

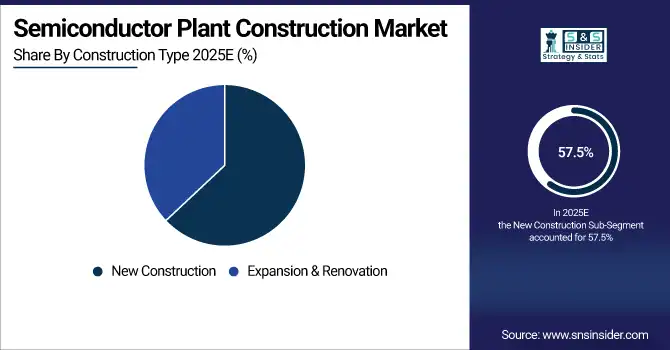

By Construction Type

In 2025, New Construction dominates the Semiconductor Plant Construction Market share, accounting for approximately 57.5% of activities. This dominance is driven by the urgent need for building entirely new fabrication plants to meet the surging global demand for advanced semiconductors. Companies are investing heavily in state-of-the-art fabs equipped with cutting-edge technologies to support next-generation chip manufacturing, especially for applications in 5G, AI, and electric vehicles.

Expansion & Renovation is expected to witness the fastest growth from 2026 to 2035. As existing fabs upgrade to support more advanced process nodes and increase production capacity, renovation projects are becoming increasingly critical. This trend is fueled by the need to optimize current infrastructure, incorporate energy-efficient technologies, and rapidly adapt to evolving semiconductor manufacturing requirements.

By Plant Type

Front-end Semiconductor Fab Plants dominated the market with a 68.4% share in 2025 and are expected to grow at the fastest CAGR from 2026 to 2035. This dominance is due to the high complexity and capital intensity of wafer fabrication processes required for advanced semiconductor manufacturing. The increasing demand for cutting-edge chips in industries like AI, 5G, and automotive fuels investments in new front-end fabs and upgrades to existing facilities, driving significant growth in this segment.

By Construction Material

Concrete dominated the Semiconductor Plant Construction Market with a 53.4% share in 2025, largely due to its fundamental role in building the strong foundations and structural components essential for semiconductor fabrication plants. Its durability, cost-effectiveness, and adaptability make it the preferred choice for constructing cleanroom floors, walls, and support structures, ensuring the stability and contamination control necessary for high-precision manufacturing.

Steel is expected to experience the fastest growth from 2026 to 2035. Increasing demand for flexible and modular plant designs is driving the use of steel frameworks, which offer superior strength, faster construction timelines, and adaptability for future expansions or technology upgrades. This trend supports evolving semiconductor manufacturing needs and the shift toward more sustainable and efficient construction practices.

By End-User Industry

Consumer Electronics dominated the Semiconductor Plant Construction Market with a 39.4% share in 2025, driven by the booming demand for smartphones, laptops, wearables, and other connected devices. Rapid technological advancements and growing consumer preferences for smarter, more powerful electronics have fueled the need for increased semiconductor manufacturing capacity. This surge in demand encourages significant investments in new fabrication plants and expansions, making consumer electronics the largest end-user segment supporting the growth of semiconductor plant construction globally.

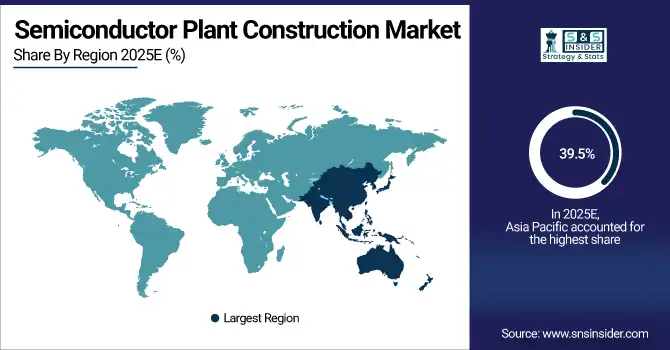

Semiconductor Plant Construction Market Regional Analysis:

Asia Pacific Semiconductor Plant Construction Market Insights

Asia Pacific dominated the Semiconductor Plant Construction Market with a 39.5% share in 2025 and is expected to grow at the fastest CAGR from 2026 to 2035. This leadership is driven by massive investments in semiconductor fabrication facilities, government support, and the presence of major chip manufacturers expanding capacity to meet growing global demand. The region continues to be the focal point for advanced semiconductor manufacturing and plant construction activities.

Get Customized Report as per Your Business Requirement - Enquiry Now

In Asia Pacific, Taiwan leads the market, followed closely by South Korea, China, and Japan, due to their strong semiconductor manufacturing ecosystems and government incentives.

North America Semiconductor Plant Construction Market Insights

North America holds a significant position in the Semiconductor Plant Construction Market, driven by substantial investments from industry leaders like Intel, Texas Instruments, and GlobalFoundries. The region benefits from strong government support, including incentives from the CHIPS and Science Act, aimed at strengthening domestic semiconductor manufacturing. Advanced technology development, skilled labor availability, and a focus on cutting-edge fabs contribute to the growth. North America continues to expand its semiconductor infrastructure to reduce supply chain dependence and meet increasing demand for high-performance chips.

Europe Semiconductor Plant Construction Market Insights

Europe’s Semiconductor Plant Construction Market is steadily growing, supported by increasing investments in advanced semiconductor manufacturing to boost regional chip production and reduce reliance on imports. The European Union’s initiatives like the European Chips Act provide significant funding and policy support to develop new fabrication plants and expand existing facilities. Key countries such as Germany, France, and the Netherlands lead in semiconductor infrastructure development, focusing on automotive, industrial electronics, and 5G applications, driving demand for state-of-the-art semiconductor plants across the region.

Middle East & Africa and Latin America Semiconductor Plant Construction Market Insights

Latin America and the Middle East & Africa regions are emerging as important players in the Semiconductor Plant Construction Market. Both regions are attracting growing investments to develop semiconductor manufacturing infrastructure, supported by government initiatives aimed at diversifying global supply chains. Countries like Brazil and Mexico in Latin America, along with the UAE and Saudi Arabia in the Middle East, are focusing on building fabs and related facilities. These efforts are driven by rising local demand for advanced electronics and strategic economic diversification plans.

Semiconductor Plant Construction Market Competitive Landscape:

Bechtel

Bechtel Corporation is a global engineering, construction, and project management company delivering large-scale industrial, infrastructure, and energy projects. With expertise in complex facility design, megaproject execution, and technology integration, Bechtel serves semiconductor, oil & gas, transportation, and power sectors. Its semiconductor facility portfolio includes advanced chip manufacturing plants, supporting U.S. domestic supply chains, fostering technological development, and enabling high-precision, high-volume manufacturing infrastructure across global semiconductor ecosystems.

-

2025 – Bechtel selected to build Intel’s semiconductor manufacturing facilities in New Albany, Ohio, supporting U.S. chipmaking and domestic supply chain revitalization.

-

2025 – Bechtel will present at SEMICON West 2025 on strategies for accelerating and de-risking semiconductor fab construction projects.

Fluor & JGC Corporation

Fluor Corporation, in partnership with JGC Corporation, delivers engineering, procurement, and construction solutions globally, specializing in energy, infrastructure, and industrial facilities. Their joint ventures focus on FEED and project expansions, including LNG and chemical plants, combining technical design expertise with execution capabilities to optimize cost, safety, and schedule performance.

-

August 2025 – Fluor-JGC JV awarded contract to update FEED for LNG Canada Phase 2 expansion in Kitimat, British Columbia, enhancing LNG production capacity.

Samsung Austin Semiconductor

Samsung Austin Semiconductor operates advanced semiconductor fabrication facilities, producing memory and logic chips. The company emphasizes workforce development, academic partnerships, and technology innovation to support U.S. semiconductor ecosystem growth and high-performance chip production. Its Taylor facility integrates cutting-edge manufacturing, automation, and sustainability initiatives for domestic and global semiconductor supply chains.

-

July 2025 – Samsung Austin Semiconductor launched a 5-star workforce development program with U.S. engineering schools to strengthen the semiconductor ecosystem and support its Taylor facility.

Key Players

Some of the Semiconductor Plant Construction Market Companies

-

Fluor

-

Jacobs

-

Kiewit

-

Bechtel

-

Samsung Engineering

-

JGC

-

Taisei

-

Shimizu

-

Obayashi,

-

Tecnicas Reunidas

-

Hochtief

-

AECOM

-

McDermott

-

Balfour Beatty

-

Kajima

-

Gilbane

-

PCL

-

Turner Construction

| Report Attributes | Details |

| Market Size in 2025 | USD 48.41 Billion |

| Market Size by 2035 | USD 143.29 Billion |

| CAGR | CAGR of 11.57% From 2026 to 2035 |

| Base Year | 2024 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Construction Type (New Construction, and Expansion & Renovation) • By Plant Type (Front-end Semiconductor Fab Plants, and Back-end Semiconductor Assembly and Testing Plants) • By Construction Material (Concrete, Steel, and Others (Glass, Aluminum)) • By End-User Industry (Consumer Electronics, Automotive Electronics, Industrial Electronics, and Telecommunications) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Fluor, Jacobs, Kiewit, Skanska, Bechtel, Samsung Engineering, JGC, Taisei, Shimizu, Obayashi, Lendlease, Tecnicas Reunidas, Hochtief, AECOM, McDermott, Balfour Beatty, Kajima, Gilbane, PCL, and Turner Construction. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Semiconductor Plant Construction Market in 2025.

Ans: Front-end Semiconductor Fab Plants Segmentation dominated the Semiconductor Plant Construction Market.

Ans: The major growth factor driving the Semiconductor Plant Construction Market is the rapid global demand for advanced semiconductor manufacturing capacity fueled by 5G, AI, and electric vehicle technologies.

Ans: The Semiconductor Plant Construction Market was valued at USD 48.41 billion in 2025 and is expected to reach USD 143.29 billion by 2035.

Ans: The Semiconductor Plant Construction Market is expected to grow at a CAGR of 11.57% from 2026-2035.

Get in Touch