Nanochip Market Report Scope and Overview:

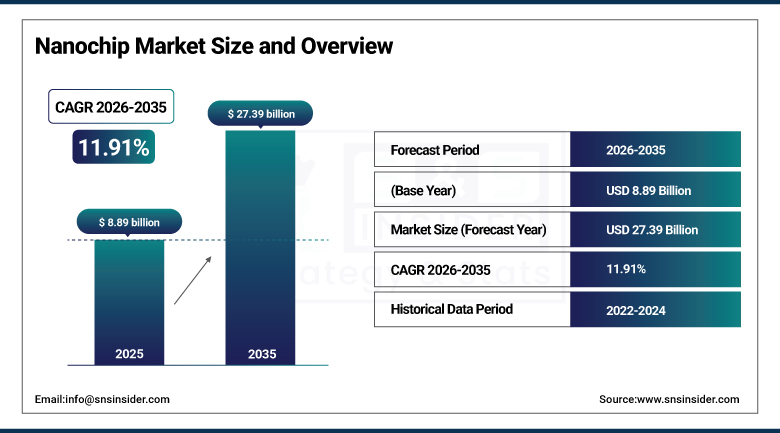

The Nanochip Market size was valued at USD 8.89 Billion in 2025 and is expected to reach USD 27.39 Billion by 2035, growing at a CAGR of 11.91% over the forecast period of 2026-2035.

The global Nanochip market is growing at a significant pace due to rising demand for the integration of nanoscale circuits in electrical and electronics, defense and medical industries. With an increasing need for high-performance ultra-small components, nanochips are now indispensable to the technology behind a variety of cutting-edge devices. Nanofabrication technologies are rapidly advancing, and research and development investments are increasing new application opportunities and production efficiency. It’s a rapidly changing market which is attracting increasing commercial attention with each new technological breakthrough, and it is driving innovation across many of the world’s high-tech industries.

According to research, more than 60% of new consumer electronics globally in 2024 utilize nanochip technology for increased speed, lower power consumption, and reduced form factor.

Nanochip Market Size and Growth Projection:

-

Market Size in 2025 USD 8.89 Billion

-

Market Size by 2035 USD 27.39 Billion

-

CAGR of 11.91% from 2026 to 2035

-

Base Year 2025

-

Forecast Period 2026–2035

-

Historical Data 2022–2024

To Get More Information On Nanochip Market - Request Free Sample Report

Nanochip Market Trends Highlights:

-

Nanochip technology is advancing rapidly due to breakthroughs in nanoscale heat conduction and material behavior, enabling higher performance and improved energy efficiency in next-generation semiconductor devices.

-

Improved thermal management at the nanoscale is addressing key limitations in chip reliability and power density, supporting wider adoption in AI processors, data centers, and high-performance computing systems.

-

Ongoing miniaturization and integration of nanoscale materials are expanding nanochip applications beyond traditional electronics into quantum computing, photonics, and advanced sensing technologies.

-

Growing demand for compact, high-speed, and low-power chips is accelerating nanochip deployment across smartphones, IoT devices, wearables, and edge computing platforms.

-

Nanochips are gaining traction in healthcare and biomedical applications, enabling advanced diagnostics, implantable devices, and real-time health monitoring solutions.

-

Continuous innovation in nanochip design and fabrication processes is driving market growth across consumer electronics, automotive electronics, and industrial automation sectors.

U.S. Nanochip Market Size Outlook

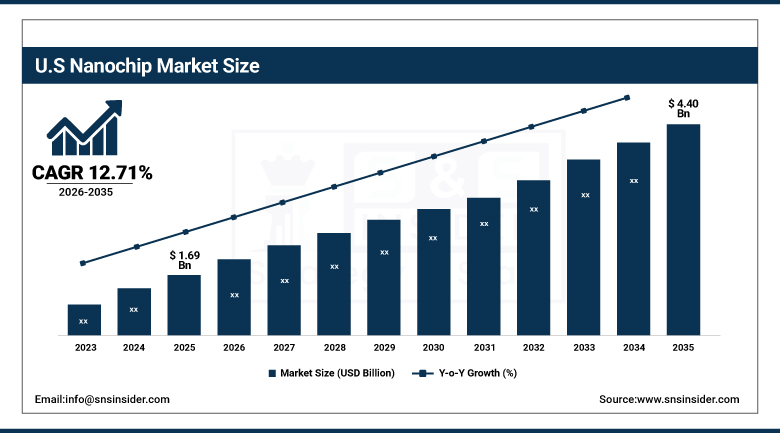

The U.S. Nanochip Market size was USD 1.69 billion in 2025 and is expected to reach USD 4.40 billion by 2035, growing at a CAGR of 12.71% over the forecast period of 2026–2035.The US nanochip market growth is fueled by rising investments in nanotechnology R&D, rising nanochips applications in defense and health care sectors and government led advancements in microelectronics. With the country’s advanced semiconductor infrastructure, home to leading chip suppliers and a burgeoning demand of small medical devices, the higher penetration will create significant demand for such adaptable technology, making the U.S. a significant player in the worldwide nanochip revolution.

According to research, as of 2024, the U.S. is constructing more than 10 new advanced fabs, many focusing on <5nm and sub-nano scale production, thanks to CHIPS Act incentives.

Nanochip Market Drivers:

-

Miniaturization trend in electronics is intensifying the demand for compact and energy-efficient nanochip solutions across applications.

With consumer electronics and IoT equipment becoming smaller, and requiring higher performance, the industry is heading towards advanced nanochips that offer tremendous processing capacity within very small spatial profiles. Nanochips are indispensable for enabling the peak performance of portable electronics (e.g., smartwatches, wearable health monitors, minidrones, etc.) without causing any increase in the form factor. The market for nanochips is expected to grow rapidly as this trend for miniaturization and a burgeoning preference for energy efficient chips becomes more prevalent; hardware makers across both industrial and consumer segments are looking to develop the next generation of hardware using nanochips.

According to research, Modern nanochips at 3nm deliver up to 45% more power efficiency compared to their 7nm predecessors, critical for battery-operated mini-devices.

Nanochip Market Restraints:

-

Limited standardization and integration compatibility with legacy systems pose adoption challenges for industrial users.

While nanochips were used because of its superior performance, they tend to be incompatible when mounted on traditional or outdated systems, especially, legacy industrial or healthcare systems. Lack of international standards for nanochip design, interface protocols and security benchmarks further complicates things. Organisations are not always keen to upgrade their current infrastructure for ‘nano’ allocations, as it would result in downtime, costly re-configuration and often there would be little in the way of enterprise-class support over time. These integration challenges, however, limit acceptance in conservative industries, as well as the near-term scalability of nanochip offerings.

Nanochip Market Opportunities:

-

Surging demand for AI and edge computing solutions is creating new avenues for nanochip integration.

The demands of edge computing and A

ial to real-time AI applications, in that they enable high-speed data processing with the lowest possible latency at a device’s ends. Nanochips are also now being used in AI accelerators and neuromorphic computing designs as industries have an increasing appetite for localized intelligence. This decentralization of computing architectures creates tremendous opportunities for nanochips to set a new benchmark for hardware performance.

According to research, Edge AI devices using nanochips can reduce latency by up to 70%, compared to cloud-based processing models.

Nanochip Market Segment Analysis:

By Sales Channel

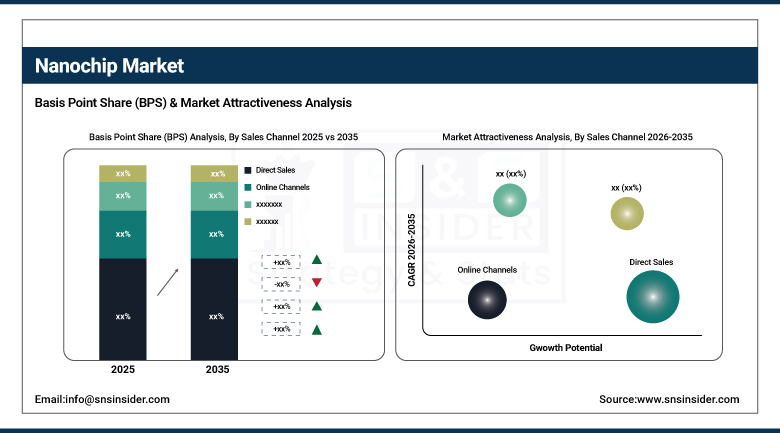

The Direct Sales segment dominated the highest Nanochip Market share of about 64.34% in 2025, because manufacturers & industrial buyer prefer customized solution, bulk order handling, and better aftersales service. Direct interaction provides for personal consultations and enables technical consultative sales support and a greater control over the supply chain, which are particularly important in high-precision fields such as nanoelectronics. For instance, Intel Corporation do the direct sales for OEMs and large enterprises and also efficient their distribution and establishing long term customer relationship.

The Online Channels segment is expected to grow at the fastest CAGR of about 13.31% from 2026–2035, due to the digitalization of the procurement system and rise in penetration of e-commerce platforms among SMEs and start-ups. Internet developments can increase the size of market, reduce the product individual comparison time and also the transaction cost. Businesses such as TSMC are now growing online, and bringing their online component catalogs, ordering systems and customer support automation online as well, leading nanochip procurement to be more common through these channels.

By End User

The Electronics and Semiconductors segment dominated the Nanochip Market with the highest revenue share of about 33.91% in 2025, driven by increasing adoption of nanochips in high miniatutrized memory devices, microprocessors and others. Due to their compact dimension, they are increasingly integrated into electronic devices for higher processing speeds and reduced consumption of energy, which is essential in consumer electronics, industrial automation, and computing hardware. Samsung Electronics, which has been leading the nanochip integration for semiconductors, is accelerating innovation in the density of chips and the performance, which keeps enhancing market concentration of a segment.

The Healthcare segment is expected to grow at the fastest CAGR of about 13.21% from 2026–2035 owing to the increasing application of nanochips for diagnosis, targeted-drug delivery, and smart medical equipment. Small chips allow early diagnosis, constant patient control, and individualized therapy. Nanochips companies such as Thermo Fisher Scientific are creating nano-based biosensors and lab-on-a-chip solutions, thereby expediting adoption of nanochips in advanced healthcare applications, which in turn is fuelling growth of the market.

Nanochip Market Regional Analysis:

Asia-Pacific Nanochip Market Trends:

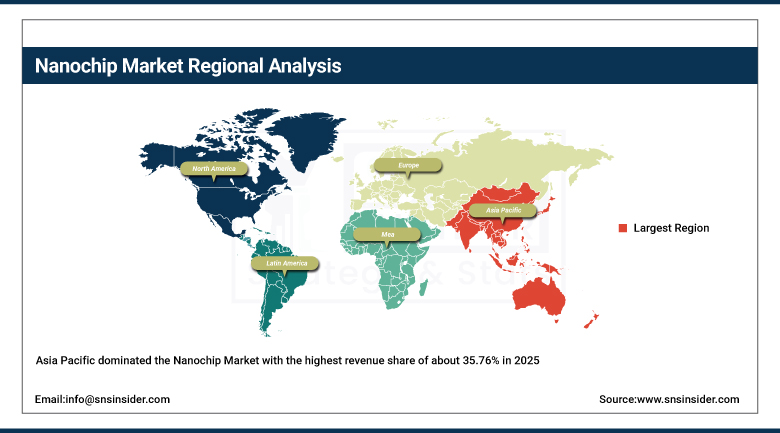

Asia Pacific dominated the Nanochip Market with the highest revenue share of about 35.76% in 2025, due to the strong manufacturing infrastructure in countries such as China, Korea, Taiwan, and Japan. The area is supported by mass production capacity, labor force and strong government investment in nanotechnology and advanced materials. The increasing consumer electronics market, export-oriented policies, as well as tight collaboration among universities and industry, also support the continued leadership in the production and technology of nanochips.

-

China leads the Asia Pacific nanochip market due to investments in semiconductor manufacturing, an active domestic electronics industry and government supported nanotech programs. Its size, skilled workers and growing exports also serve to bolster its regional leadership in chip production on the nano-scale.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Nanochip Market Trends:

North America is expected to grow at the fastest CAGR of about 13.25% from 2026–2035, driven by the increasing investments in nanotech R&D, early acceptance of new technologies, and high demand for nanochips in the defense, healthcare, and autonomous systems. The area boasts a mature innovative ecosystem, strong academic research programs, and effective government support for creating a domestic semiconductor industrial chain. These factors together are contributing toward the quick expansion of the North American nanochip market.

-

The United States dominates the North American nanochip market owing to advanced R&D infrastructure, leading semiconductor players and fierce support from the government. Strong defense, health and AI need, plus vibrant innovation ecosystems, maintain long-term growth and technological leadership.

Europe Nanochip Market Trends:

Europe’s nanochip market is also growing slowly but steadily on the back of advancement in microelectronics and growing adoption in medical devices, renewable energy solutions, and smart manufacturing. The region focuses on high-quality, application-specific nanochips, not mass production. Government projects like the the European Chips Act are targeting self reliance, while joint efforts between main players and research institutions are narrowing the technology gap with international leaders.

-

Germany is the leading country in the EU in the nanochip market, mainly because of advanced semiconductor infrastructure, high industrial demand and massive investments in nanotechnology. With its specialist expertise in automotive electronics, precision engineering and research driven innovation, it is a major contributor to the growth of Europe’s nanochip industry.

Latin America and Middle East & Africa Nanochip Market Trends:

The nanochip market in the Middle East & Africa and Latin America is developing due to digital transformation and technology penetration. MEA is dominated by the UAE and Saudi Arabia, which are leading in terms of smart cities and defense projects, and Brazil for Latin America is witnessing high demand for electronics, telecom and government-led semiconductor program.

Nanochip Market Competitive Landscape:

Samsung Electronics is a global leader in semiconductor technology, consumer electronics, and telecommunications equipment. Established in 1969, the company innovates in memory chips, system LSI, and mobile processors. Samsung drives advanced nanochip development, delivering high-performance solutions for AI, data centers, smartphones, and automotive industries worldwide with extensive manufacturing excellence.

-

In June 2024, Samsung advanced its nanochip roadmap by planning mass production of 3nm Exynos processors, intensifying competition with TSMC and targeting high-performance, power-efficient chips for smartphones and automotive electronics.

Qualcomm Incorporated was established in 1985. Qualcomm is a global semiconductor and wireless technology leader specializing in advanced nanochips and system-on-chips. The company is renowned for Snapdragon processors, enabling high-performance smartphones, AI computing, 5G connectivity, automotive platforms, and IoT devices, driving innovation across next-generation digital ecosystems worldwide.

-

In January 2025, Qualcomm’s Snapdragon 8 Gen 3 nanochip powers the Galaxy S25, enhancing on-device AI and energy efficiency with 4nm architecture, reinforcing Qualcomm’s dominance in flagship mobile chipsets.

Key Nanochip Companies are:

-

Intel Corporation

-

Samsung Electronics

-

NVIDIA Corporation

-

Advanced Micro Devices

-

Qualcomm Incorporated

-

SK Hynix Inc.

-

Broadcom Inc.

-

Texas Instruments Incorporated

-

Infineon Technologies AG

-

ASML Holding N.V.

-

STMicroelectronics

-

Renesas Electronics Corporation

-

GlobalFoundries

-

Semiconductor Manufacturing International Corporation

-

United Microelectronics Corporation

-

Tower Semiconductor Ltd.

-

Hua Hong Semiconductor

-

Rapidus Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.89 Billion |

| Market Size by 2035 | USD 27.39 Billion |

| CAGR | CAGR of 11.91% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sales Channel (Direct Sales, Distributors, Online Channels) • By End User (Healthcare, Electronics and Semiconductors, IT and Telecommunications, Aerospace and Defense, Energy and Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel Corporation, Samsung Electronics, Taiwan Semiconductor Manufacturing Company, NVIDIA Corporation, Advanced Micro Devices, Qualcomm Incorporated, SK Hynix Inc., Micron Technology Inc., Broadcom Inc., Texas Instruments Incorporated, Infineon Technologies AG, ASML Holding N.V., STMicroelectronics, Renesas Electronics Corporation, GlobalFoundries, Semiconductor Manufacturing International Corporation, United Microelectronics Corporation, Tower Semiconductor Ltd., Hua Hong Semiconductor, Rapidus Corporation. |

Frequently Asked Questions

Ans: The Nanochip Market size was valued at USD 8.89 Billion in 2025 and is expected to reach USD 27.39 Billion by 2035, growing at a CAGR of 11.91% over the forecast period of 2026-2035.

Ans: Direct Sales segment dominated the Nanochip Market.

Ans: The major growth factor of the Nanochip Market is the increasing demand for miniaturized, high-performance electronics across AI, IoT, and healthcare sectors.

Ans: Direct Sales segment dominated the Nanochip Market.

Ans: Asia Pacific dominated the Nanochip Market in 2025.

Get in Touch