Semiconductor Recycling & Sustainability Market Size Analysis:

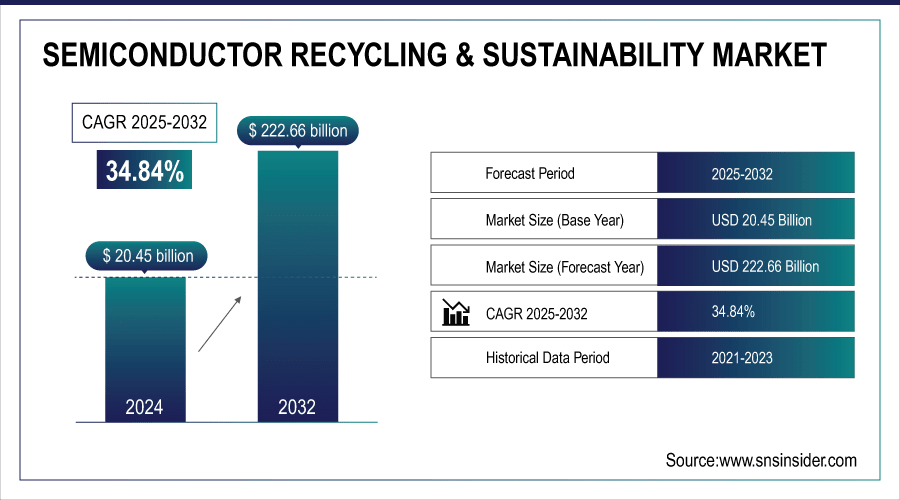

The semiconductor recycling & sustainability market size was valued at USD 20.45 billion in 2024 and is expected to reach USD 222.66 billion by 2032, growing at a CAGR of 34.84% over the forecast period of 2025-2032.

To Get More Information On Semiconductor Recycling & Sustainability Market - Request Free Sample Report

The semiconductor recycling & sustainability market growth is driven by factors, such as increasing e-waste, demand for sustainable electronics, government regulations, technological advancements in recycling, and the transformation of electric vehicles and IoT.

Increased sustainability concerns, stringent regulations imposed by the government, and the demand for eco-friendly production processes are some of the major factors driving the semiconductor recycling and sustainable market. Businesses are looking to spend less on electronic waste and to recycle materials like silicon, gold, and rare earth metals. There is also a push for considering the circular economy as well as the high prices for raw semiconductor materials that are helping to promote recycling efforts. Green chemistry and innovations within recycling technologies also make it more effective, thus contributing to the sustainability of semiconductor supply chains in the longer run.

For instance, Samsung launched a circular battery supply chain, recycling cobalt from used Galaxy devices to reuse in future batteries, such as 50% recycled cobalt in Galaxy S25 batteries.

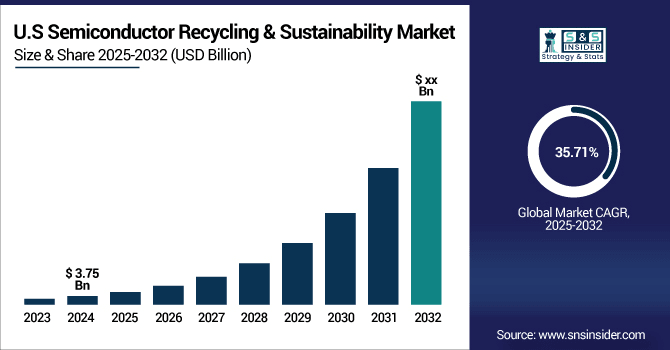

The U.S. semiconductor recycling & sustainability market is estimated to be USD 3.75 billion in 2024 and is projected to grow at a CAGR of 35.71% during the forecast period. Growth in corporate ESG commitments, semiconductor manufacturing incentives in the U.S. under the CHIPS Act, and supply chain resiliency drives market growth in the U.S. semiconductor recycling & sustainability market. Moreover, alliances between technology companies and recyclers are accelerating the establishment of closed-loop systems.

Semiconductor Recycling and Sustainability Market Dynamics:

Key Drivers:

-

Driving Sustainability Through Semiconductor Recycling and Eco Friendly Material Recovery Solutions

A key driver for the semiconductor recycling and sustainability market is the growing pressure to reduce electronic waste and minimize environmental impact. Rising demand for rare and expensive materials like silicon and precious metals is pushing companies to adopt recycling practices. Additionally, strict environmental regulations and sustainability goals are encouraging manufacturers to implement eco-friendly solutions. The shift toward a circular economy, along with technological advancements in material recovery and recycling processes, is further propelling market growth and long-term environmental responsibility.

According to the Global E-waste Monitor 2024, global e-waste hit 62 million metric tons in 2023, with only 22% being recycled formally, highlighting the urgency of this challenge.

Restraints:

-

High Costs, Complex Processes, and Lack of Global Regulatory Standards Hamper Market Expansion

The complexity and cost of the recycling process itself are one of the major restraints for semiconductor recycling & sustainability market growth. The chip itself includes multiple layers of sophisticated materials, such as silicon, gallium arsenide, and even rare metals, which are blended fairly intricately during manufacturing. High-end specialized techniques and methods are used to separate these materials without destroying integrity, but they are expensive. Moreover, a lot of older semiconductor materials are toxic and thus, safe disposal and recovery tend to be more difficult. The absence of standard global recycling regulations causes further delay in collection and processing.

For instance, in 2023 report from the United Nations states that more than three-quarters of global electronic waste is either undocumented or treated informally, reducing recovery efficiency and risk to the environment.

Opportunities:

-

Growing EV and IoT Adoption Accelerates Demand for Semiconductor Recycling and Sustainable Global Supply Chains

Increased usage of EVs, IoT devices, and smart electronics gives semiconductor recycling an added consideration. As these technologies become more ubiquitous, and given that semiconductors can be in a large number, such as more than 3,000 chips can go into some EVs, the amount of semiconductor consumption rises. The increase in demand is fueling the creation of recovery systems and sustainable supply chains. In addition, the EU, South Korea, and Japan, together represent just under 50% of the battery-critical minerals sourcing value chain, have established favourable regulatory frameworks and incentive schemes to drive companies toward sustainable recycling technologies.

For instance, in 2023 alone, global EV sales surged beyond 14 million units according to the International Energy Agency (IEA), further driving the demand for sustainable semiconductor solutions.

Challenges:

-

Lack of Infrastructure and Economic Viability Hinder Semiconductor Recycling in Developing Global Markets

The massive barrier, especially in developing economies, remains the lack of capital-intensive advanced recycling infrastructure. Due to logistical obstacles in the home country, the majority of semiconductor recycling sites are located in the EU, Japan, and South Korea. Additionally, wider electronic streams, advances in technology, and shorter innovation cycles lead to components that are not applicable for reuse or refurbished and therefore not economically viable for recycling.

According to the Global E-waste Monitor 2024 says that in 2023, nearly 50 million metric tons of e-waste were improperly discarded in lower-income regions, but less than 5% have been processed through formal recycling channels.

Semiconductor Recycling & Sustainability Market Segmentation Analysis:

By Material

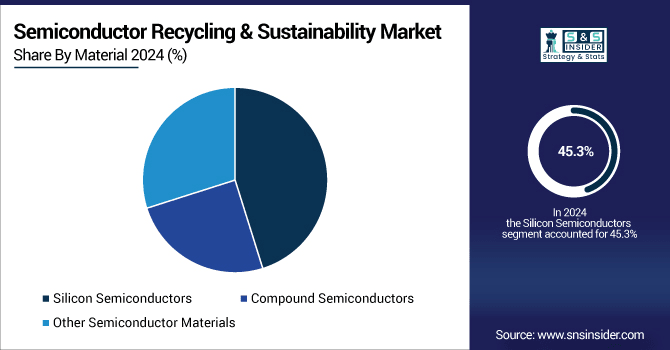

In 2024, the silicon semiconductors segment accounted for the largest share of 45.3%, and it is expected to grow the fastest in terms of CAGR from 2025 to 2032. This dominance stems from their extensive applications in major sectors, including consumer electronics, automotive, and renewable energy systems. Silicon still serves as the substrate for integrated circuits, owing to its abundance, low cost, and well-developed manufacturing infrastructure. To heighten its sustainable quality, it is also recyclable, which is an essential feature as businesses and countries move toward electronics to be greener. The growing environmental issues and demand for sustainable supply chains make silicon recycling more technically and economically viable. To overcome these challenges, innovations in wafer reclamation, including kerfless wafering, had gained considerable attention along with chemical treatment technologies to enhance the purification of materials while improving recovery yields.

By Application

In 2024, consumer electronics accounted for 31.4% share in the market, making it the dominant segment. The growth is attributed to the ubiquitous nature of semiconductors in consumer products, such as smartphones, laptops, wearables, and other consumer devices, which sustain this segment as the largest contributor to semiconductor demand. The evolution of smarter, more connected, and energy-efficient electronics drives a strong demand for new and advanced semiconductors. Consumer electronics innovation, such as displays, sensors, and processors, also work to drive demand for semiconductor recycling, which continues to grow as a segment.

Automotive is projected to witness highest CAGR growth during 2025–2032. The segment’s expansion is driven by the automotive industry trend away from internal combustion engines to EVs and other new technologies, including driver-assistance systems (ADAS). As each EV contains thousands of semiconductor chips, there is increasing potential for these materials to be recycled. The continuous developments globally for greener and more sustainable transport, and in this context, the automotive semiconductor recycling market value is expected to increase in the automotive sector by 2032 as a means to minimize the dependency on raw materials and the ecological footprint associated with the broader development of vehicles.

Semiconductor Recycling & Sustainability Market Regional Overview:

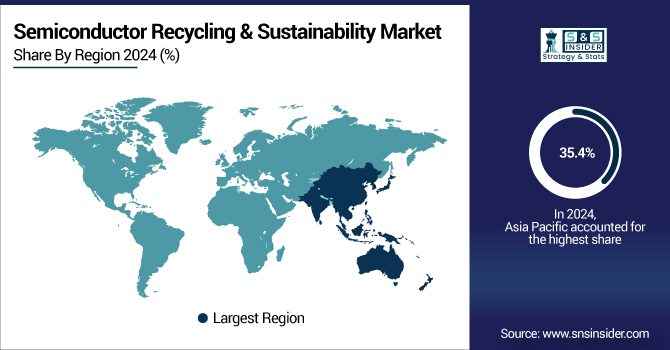

In 2024, Asia Pacific accounted for 35.4% of the semiconductor recycling & sustainability market, as it is the largest producer with a strong manufacturing ecosystem, rapid technological changes, and a high level of government support for sustainability initiatives. Semiconductor recycling solutions demand in the region is primarily driven by the presence of major semiconductor manufacturers, including TSMC, Samsung Electronics, and SMIC. China, Japan, and South Korea are the leading countries in the region, and large volumes of these materials are originating from China due to its main production capacity, low labor cost, and considerable investments in both electronics manufacturing and recycling facilities.

-

TSMC has made meaningful progress with its commitment to using 100% renewable energy throughout every global operation by 2050. The company has also poured resources into leading-edge wastewater recycling technologies to recycle over 85% of water used in fabrication plants.

-

ASML’s refurbishment center in Taoyuan, Taiwan, is representative of a circular economy trend, boasting an 88% reuse rate of defective parts on older lithography systems.

North America is anticipated to grow with the highest CAGR from 2025 to 2032 due to the fast adoption of EVs, tech advancements, and rapidly growing global demand for sustainable semiconductor solutions for EVs in the region. Similarly, given the number of high-tech giants in the U.S., such as Intel and Tesla, the country has been investing in the development of semiconductor recycling technologies and semiconductor recycling policies to advance green manufacturing. Additionally, the growing focus of the U.S. government toward e-waste reduction through legislation and providing incentives for green technologies further augments growth.

The Environmental Protection Agency (EPA) rolled out a record money pathway USD 100 million, for e-waste recycling projects in states, the largest amount of federal funding for recycling in more than 30 years.

Europe is a prominent region for the Semiconductor Recycling & Sustainability Market due to stringent environmental regulations, implementation of e-waste management programs, and initiatives focused on the circular economy. Its area is the basis for slight material dependence and improves recycling innovation.

Germany is the largest market owing to its comprehensive recycling infrastructure and dedication to the sustainable production of electronic waste.

Latin America and the Middle East & Africa have been slowly progressing in developing awareness of environmental issues and working toward greener practices. Growing urbanization, industrialization, and diverse government initiatives promoting waste management and circular economic policies in these regions are expected to drive the semiconductor recycling technology adoption globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players in the Semiconductor Recycling & Sustainability Market are:

Some of the major players are Intel, GlobalWafers, ASML, Veolia North America, Entegris, Umicore, Reciprocity, SungEel HiTech, Siemens, and KLA Corporation.

Recent Trends:

-

In December 2023, Siemens and Intel announced a strategic collaboration to advance semiconductor manufacturing, focusing on sustainability, energy efficiency, and digitalization.

-

In March 2025, ASML and imec signed a five-year partnership to advance semiconductor research and sustainable innovation. The collaboration aims to develop cutting-edge technologies and promote environmental responsibility, reinforcing Europe's position in the semiconductor industry.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 20.45 Billion |

| Market Size by 2032 | USD 222.66 Billion |

| CAGR | CAGR of 34.84% From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Silicon Semiconductors, Compound Semiconductors, Other Semiconductor Materials) • By Application (Consumer Electronics, Automotive, IT & Telecom, Industrial, Energy, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Intel, GlobalWafers, ASML, Veolia North America, Entegris, Umicore, Reciprocity, SungEel HiTech, Siemens, and KLA Corporation |

Frequently Asked Questions

Ans: Asia Pacific dominated the Semiconductor Recycling & Sustainability Market in 2024.

Ans: The Silicon Semiconductors segment dominated the Semiconductor Recycling & Sustainability Market in 2024.

Ans: The major growth factor of the Semiconductor Recycling & Sustainability Market is the increasing demand for eco-friendly practices and resource efficiency in semiconductor production.

Ans: The Semiconductor Recycling & Sustainability Market size was USD 20.45 billion in 2024 and is expected to reach USD 222.66 billion by 2032.

Ans: The Semiconductor Recycling & Sustainability Market is expected to grow at a CAGR of 34.84% from 2025-2032.

Get in Touch