Silicone Elastomer Market Report Scope & Overview:

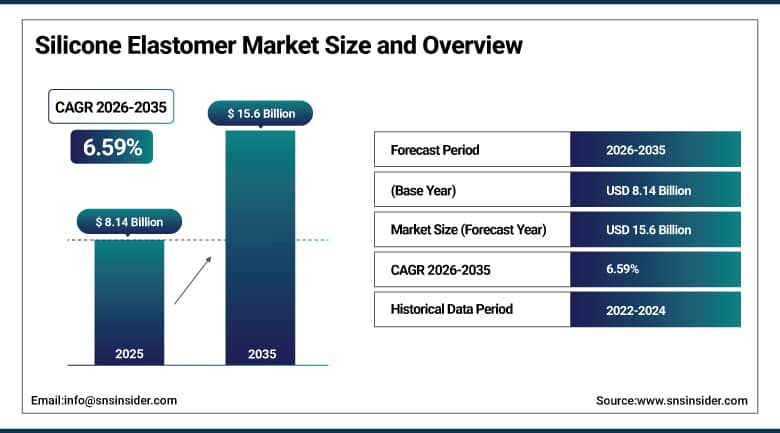

Silicone Elastomer Market was valued at USD 8.14 billion in 2025 and is expected to reach USD 15.6 billion by 2035, growing at a CAGR of 6.59% from 2026-2035.

Silicone elastomers occupy a unique position in the advanced materials landscape their silicon-oxygen polymer backbone creates a combination of properties that no organic rubber achieves stable flexibility from -60°C to 230°C continuous service temperature, biocompatibility and sterilization resistance whose medical device certification pathway is well-established by FDA and ISO standards, dielectric insulation properties that maintain consistency across the full service temperature range, and hydrophobic surface chemistry that prevents moisture absorption and sustains electrical and mechanical properties in humid environments. These properties make silicone elastomers indispensable across applications where organic rubbers nitrile, EPDM, neoprene would fail from thermal degradation, swelling from solvent or fuel exposure, or biocompatibility rejection. Its reflects the progressive expansion of silicone elastomers into application areas that temperature, regulatory, or performance requirements exclude alternative materials from serving electric vehicle thermal management systems, 5G infrastructure cable insulation, implantable medical devices, and LED lighting encapsulation each representing high-growth demand vectors that the silicone elastomer industry is simultaneously developing commercial products to address.

The Dow Chemical Company's advanced materials market analysis documents that liquid silicone rubber demand for medical device applications is growing at 7-8% annually the fastest growth rate of any end-use segment driven by the proliferation of minimally invasive medical device designs whose small-bore tubing, catheter coatings, and implant encapsulation requirements specify medical-grade LSR's biocompatibility and sterilization resistance. The automotive industry's electrification transition is creating new silicone elastomer demand estimated at 3-4 kg per electric vehicle above the 2-3 kg per ICE vehicle driven by battery thermal interface materials, EV powertrain seal requirements, and high-voltage cable insulation that EV's electrical architecture requires.

Silicone Elastomer Market Size and Forecast

-

Market Size in 2025: USD 8.14 Billion

-

Market Size by 2035: USD 15.6 Billion

-

CAGR: 6.59% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Silicone Elastomer Market - Request Free Sample Report

Silicone Elastomer Market Trends

-

Self-healing silicone elastomers incorporating dynamic covalent chemistry or supramolecular networks that autonomously repair mechanical damage are advancing toward commercial deployment in applications including wearable electronics and medical implants where crack propagation limits service life.

-

Bio-based silicone precursors using bio-derived silicon compounds or plant-based organic modifiers to reduce the petroleum content of silicone synthesis are creating sustainable silicone elastomer development pipelines whose environmental credentials sustain regulatory preference in medical and food-contact applications.

-

Electrically conductive silicone elastomers incorporating carbon nanotubes, graphene, or metallic particle fillers in silicone matrices are creating composite materials for electromagnetic shielding, flexible electronics, and heated clothing applications that combine silicone's flexibility with electrical conductivity.

-

5G infrastructure buildout is creating LSR demand for cable insulation and connector sealing in 5G small cell antennas whose outdoor installation in rain, UV, and thermal cycling environments requires silicone's weathering resistance at unprecedented small cell installation density.

-

Electric vehicle battery thermal interface material adoption where silicone-based phase-change materials, gels, and pads manage heat transfer between battery cells and cooling plates is creating a new high-volume automotive silicone elastomer demand category.

-

Food-contact silicone elastomers for flexible packaging, baking molds, and food processing seal applications are growing as silicone's inertness and temperature resistance create advantages over conventional food-contact materials including PTFE and fluorocarbon rubber.

-

3D printable silicone elastomers single-component formulations compatible with direct ink writing and stereolithographic printing are enabling custom silicone component production without mold tooling investment, reducing prototype iteration time by 30-40% in medical device and consumer electronics development programs.

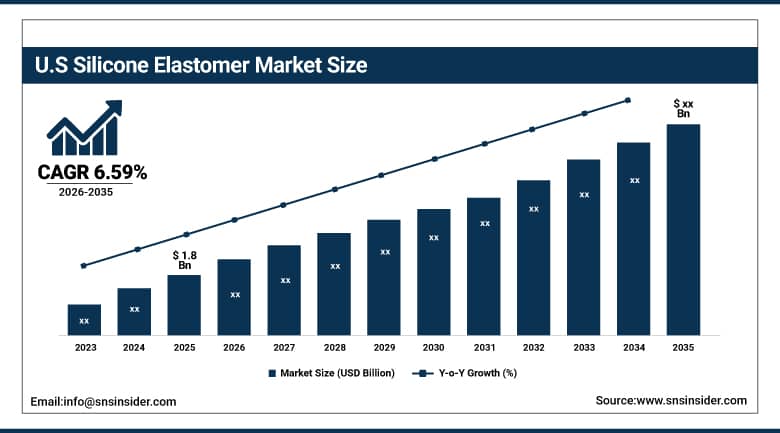

U.S. Silicone Elastomer Market was valued at approximately USD 1.8 billion in 2025 and is expected to grow at a CAGR of 6.59% from 2026-2035.

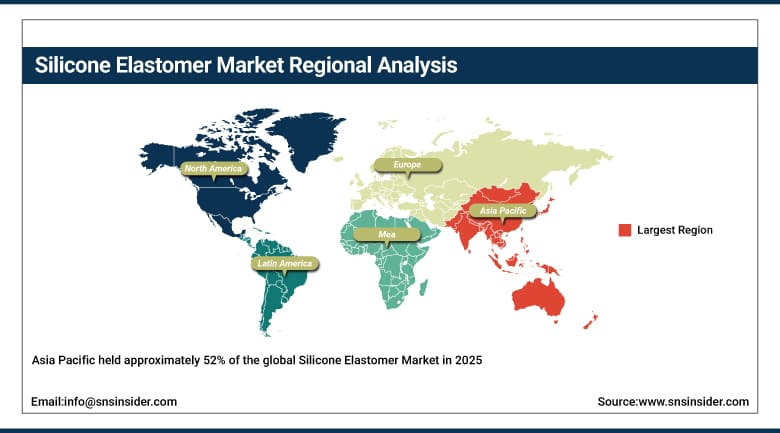

Asia Pacific held approximately 52% of the global Silicone Elastomer Market in 2025, reflecting the region's dominant manufacturing base across the construction, automotive, electronics, and healthcare industries that are the primary silicone elastomer end-use segments. China's construction sector whose use of silicone sealants and adhesives in curtain wall glazing, window sealing, and structural bonding represents the world's largest single silicone elastomer construction application by volume sustains China's position as the world's largest single national silicone elastomer market. Japan and South Korea's automotive and electronics manufacturing industries which apply LSR in EV components, 5G devices, LED lighting, and precision medical electronics sustain the Asia Pacific region's premium silicone elastomer demand above the volume concentration that China's construction market creates.

Dow Inc.'s 2024 SILASTIC Healthcare Silicones market report documents that Asia Pacific's medical-grade silicone elastomer market is growing at 9-11% annually faster than any other region — driven by the expansion of medical device manufacturing in China, Malaysia, Singapore, and India whose exports of catheters, tubing, and implant components to global healthcare markets sustain medical silicone demand. Samsung, LG, and TSMC collectively consume an estimated 25,000+ metric tons of silicone elastomers annually for electronics manufacturing applications including semiconductor package encapsulation, display module sealing, and EV battery management electronics potting.

Silicone Elastomer Market Segment Analysis

-

By Product Type, LSR (Liquid Silicone Rubber) dominated with 58% share in 2025; HCR (High-Consistency Rubber) and RTV each holding significant shares.

-

By Application, Construction dominated with 44% share in 2025; Healthcare and Electrical & Electronics growing fastest.

By Application: Construction dominates at 44%, Healthcare and Electronics growing fastest

Construction held approximately 44% of the Silicone Elastomer Market in 2025, reflecting the enormous volume of silicone sealant and adhesive consumed in building construction globally where glazing seals, expansion joint fillers, window and door perimeter sealing, and curtain wall structural bonding represent high-volume applications that the construction industry's global scale multiplies into the largest single application category by volume. Silicone construction sealants' performance advantages over organic sealant alternatives 20-50 year service life versus 10-15 years for polyurethane and silyl-terminated polyether sealants, UV stability maintaining flexibility and adhesion without degradation, and movement accommodation of ±50% elongation sustain premium specification despite higher material cost in demanding construction applications.

Healthcare is growing at one of the fastest application CAGRs, driven by the exponential growth in medical device complexity and volume each new catheter design, implantable sensor, or wearable health monitor requiring medical-grade silicone components whose biocompatibility and sterilization resistance are non-negotiable regulatory requirements. Electrical and Electronics is growing rapidly driven by 5G infrastructure cable insulation, EV battery thermal interface materials, LED encapsulation, and wearable electronic device sealing each a technology wave creating new silicone elastomer demand that was negligible five years ago.

By Product Type: LSR dominates at 58%, all types significant

Liquid Silicone Rubber held approximately 58% of the Silicone Elastomer Market in 2025, a dominant position reflecting LSR's unique processability advantages that drive its adoption across the highest-value silicone elastomer application segments. LSR's liquid state at room temperature enables injection molding where precision molds fill completely with LSR under pressure before rapid cure at elevated temperature producing complex geometries, undercut features, and thin walls that compression-molded HCR cannot achieve with equivalent dimensional accuracy. LSR's superior biocompatibility achieved through the two-part platinum-catalyzed addition cure system that produces no byproducts during curing sustains its specification in FDA Class III implantable devices and Class II medical devices where post-cure biocompatibility validation is a regulatory necessity. The high-volume injection molding automation compatibility that LSR provides enabling fully automated LSR injection molding cells running 24/7 without operator attendance creates manufacturing efficiency advantages that sustain LSR's market share growth above its established dominance.

High-Consistency Rubber maintains a significant market share as the traditional silicone elastomer form whose established fabrication processes compression molding, transfer molding, extrusion serve the industrial, automotive, and general-purpose applications where LSR's liquid processability advantage is less relevant than HCR's cost and formulation versatility. Room Temperature Vulcanizing silicones single-component or two-component systems that cure at ambient temperature serve the construction and maintenance markets whose field application requirements eliminate the heated tooling that HCR and LSR processing requires.

Silicone Elastomer Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

55% |

|

North America |

United States |

87% |

|

Europe |

Germany |

28% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

Asia Pacific Silicone Elastomer Market Insights

Asia Pacific held approximately 52% of the global Silicone Elastomer Market in 2025, a dominant position driven by China's construction and electronics manufacturing silicone consumption, Japan and South Korea's advanced electronics and automotive LSR demand, and the rapidly expanding medical device manufacturing in China, Malaysia, Singapore, and India. Chinese domestic silicone elastomer producers including Hoshine Silicon, Dongyue Group, and China National BlueStar have developed competitive positions in standard HCR and RTV grades while international companies including Dow, Wacker, Momentive, and Shin-Etsu maintain premium positions in medical-grade LSR and specialty electronic silicones.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Silicone Elastomer Market Insights

North America holds a significant Silicone Elastomer Market position, driven by the United States' advanced medical device manufacturing whose LSR demand for implantable components, medical tubing, and wearable health monitor sealing sustains premium medical-grade silicone consumption and the automotive silicone demand from U.S.-based EV manufacturing. Dow Inc., Momentive Performance Materials, and specialty compounders including Stockwell Elastomerics and Specialty Silicone Products sustain a sophisticated North American silicone elastomer supply ecosystem that develops and produces specialty formulations for defense, aerospace, medical, and semiconductor applications.

Europe Silicone Elastomer Market Insights

Europe's Silicone Elastomer Market is growing with automotive sector silicone demand particularly from EV manufacturers in Germany, France, and Sweden whose battery thermal management and high-voltage component sealing requirements drive LSR specification and the construction sector's premium silicone sealant adoption in sustainable building and facade renovation programs. Wacker Chemie AG headquartered in Germany and the world's second-largest silicone producer sustains European silicone elastomer production and R&D investment at the global frontier of specialty silicone development.

MEA and Latin America Silicone Elastomer Market Insights

The Middle East's Silicone Elastomer Market is growing with the Gulf states' construction activity where premium curtain wall glazing and high-performance building sealing create silicone sealant demand at major commercial and government building projects and the region's growing healthcare sector whose medical device procurement sustains medical-grade silicone import demand. Latin America's market concentrates in Brazil's automotive and construction industries and Mexico's manufacturing sector whose exports to North American automotive supply chains create silicone elastomer demand at the component specifications required by international OEM customers.

Silicone Elastomer Market Growth Drivers:

- EV automotive electrification and medical device proliferation driving sustained silicone elastomer market growth globally

The Silicone Elastomer Market is driven by the simultaneous acceleration of demand across multiple high-growth technology sectors that each require silicone elastomers' unique property combination. Electric vehicle production growth projected to reach 50 million units annually by 2030 creates 3-4 kg of incremental silicone elastomer demand per vehicle versus ICE vehicles through battery thermal interface materials, high-voltage cable insulation, and EV powertrain sealing requirements that conventional rubber alternatives cannot meet at the required thermal and electrical performance levels. Medical device proliferation driven by an aging global population requiring more implantable, wearable, and minimally invasive devices creates sustained growth in medical-grade LSR demand whose biocompatibility and sterilization resistance requirements are uniquely satisfied by silicone.

Silicone Elastomer Market Restraints:

- High production costs and feedstock availability creating silicone elastomer market challenges globally

Silicone elastomer production is capital-intensive requiring high-purity silicon metal, chloromethane, and specialized reactor infrastructure whose investment scale limits market entry to well-capitalized chemical companies and feedstock-dependent on silicon metal whose primary production is concentrated in China, where energy cost and environmental regulation create supply availability and cost variability that downstream silicone producers outside China find difficult to manage. The complexity of LSR processing whose platinum catalyst sensitivity to contamination, precise mixing ratio requirements, and mold temperature control specifications require operator expertise and quality control infrastructure creates adoption barriers in manufacturing environments whose technical capability does not extend to advanced elastomer processing.

Silicone Elastomer Market Opportunities:

- Self-healing materials and 5G infrastructure demand creating significant silicone elastomer market growth opportunities globally

Self-healing silicone elastomers represent the materials frontier with the most commercially compelling long-term opportunity where silicone matrices incorporating dynamic covalent boronate ester linkages or supramolecular hydrogen bonding networks autonomously repair mechanical damage at body temperature or mild heat treatment. The medical implant application where self-healing silicone restores implant integrity after microcrack formation during in-vivo mechanical loading represents a USD 100+ million near-term addressable market whose premium pricing would dwarf conventional medical silicone economics. 5G small cell infrastructure's explosive growth where base station densification requires 10-15x more individual radio antenna installations per square kilometer than 4G networks creates proportional demand for outdoor-grade silicone cable insulation, weatherproof connector sealing, and antenna radome materials.

Recent Developments:

- 2026: Dow launched SILASTIC SA 994X medical LSR — the first commercially available liquid silicone rubber formulated for Class III implantable cardiovascular device applications — achieving ISO 10993 cytotoxicity, sensitization, and chronic implantation biocompatibility validation that enables cardiovascular catheter and lead insulation specifiers to access LSR's processing and performance advantages in the most demanding medical device regulatory category.

- 2025: Wacker Chemie AG launched ELASTOSIL EV series silicone elastomers — specifically formulated for electric vehicle battery thermal interface applications with thermal conductivity of 2.5-4.5 W/m·K and maintained electrical insulation above 10 kV/mm breakdown strength — targeting the battery thermal management systems of BMW, Volkswagen, and Stellantis EV platforms whose cell-to-cooling-plate thermal management performance directly affects battery charging rate and cycle life.

- 2025: Momentive Performance Materials launched its SILOPREN 3D Printable LSR — a single-component LSR formulation compatible with direct ink writing and UV-assisted 3D printing enabling complex silicone geometries without mold tooling investment — reporting a 40% reduction in medical device prototype development timelines at partnered device manufacturers who replaced multi-week molding tool fabrication with 24-hour 3D print iterations for LSR component design validation.

Silicone Elastomer Market Key Players

Some of the Silicone Elastomer Market Companies

- Dow Inc. (SILASTIC)

- Wacker Chemie AG (ELASTOSIL)

- Momentive Performance Materials Inc. (SILOPREN)

- Shin-Etsu Chemical Co. Ltd.

- KCC Corporation

- China National BlueStar (Group) Co. Ltd.

- Hoshine Silicon Industry Co. Ltd.

- Dongyue Group Ltd.

- Zhejiang Xinan Chemical Industrial Group

- Reiss Manufacturing Inc.

- Mesgo SpA

- Specialty Silicone Products Inc.

- Stockwell Elastomerics Inc.

- Soudal Group NV

- Innovative Silicones

- Cauchos Pedro Romero SA

- Rogers Corporation

- Wynca Group

- Primasil Silicones Ltd.

- Quantum Silicones Inc.

Silicone Elastomer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.14 Billion |

| Market Size by 2035 | USD 15.6 Billion |

| CAGR | CAGR of 6.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (High-temperature Vulcanize (HTV), Room-temperature Vulcanize (RTV), Liquid Silicone Rubber (LSR)) •By Application (Electrical & Electronics, Automotive & Transportation, Industrial Machinery, Consumer Goods, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dow Inc. (SILASTIC), Wacker Chemie AG (ELASTOSIL), Momentive Performance Materials Inc. (SILOPREN), Shin-Etsu Chemical Co. Ltd., KCC Corporation, China National BlueStar (Group) Co. Ltd., Hoshine Silicon Industry Co. Ltd., Dongyue Group Ltd., Zhejiang Xinan Chemical Industrial Group, Reiss Manufacturing Inc., Mesgo SpA, Specialty Silicone Products Inc., Stockwell Elastomerics Inc., Soudal Group NV, Innovative Silicones, Cauchos Pedro Romero SA, Rogers Corporation, Wynca Group, Primasil Silicones Ltd., Quantum Silicones Inc. |

Frequently Asked Questions

Ans: The Silicone Elastomer Market was valued at USD 8.14 billion in 2025.

Ans: Asia Pacific dominated with approximately 52% share in 2025.

Ans: Construction dominated with approximately 44% share; Healthcare and Electronics growing fastest.

Ans: LSR (Liquid Silicone Rubber) dominated with approximately 58% share in 2025.

Ans: The Silicone Elastomer Market is expected to grow at a CAGR of 6.59% from 2026 to 2035.

Get in Touch