Smart Assault Rifle Market Report Scope & Overview:

To get more information on Smart Assault Rifle Market - Request Sample Report

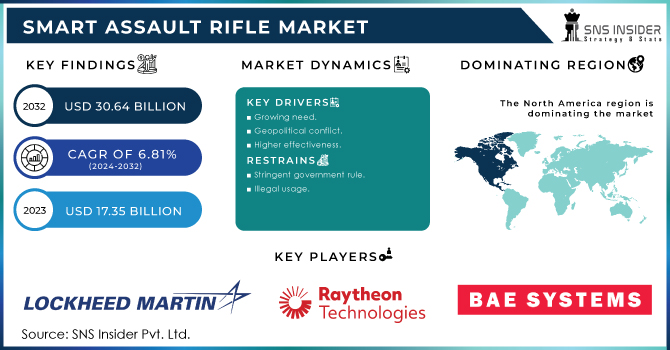

The Smart Assault Rifle Market Size was valued at USD 17.35 Billion in 2023 and is expected to reach USD 30.64 Billion by 2032 and grow at a CAGR of 6.81% over the forecast period 2024-2032.

Smart weapons are computer-controlled devices equipped with radio, infrared, laser, global positioning system,s and satellite navigation systems, which provide incredible accuracy and precision. Smart weapons are also referred to as precision-directed weapons aimed at direct targeting strikes and minimizing associated hazard injuries. Smart weapons are used and aided by the use of external applications, located locally. The smart weapons system has changed the course of military involvement and its tactics. Cruise Arrows use information from the navigation satellite to maintain proper direction and direction during flight. Smart guns have protections that allow them to operate only when activated by an authorized person, thus reducing misuse, theft of firearms, and situations of self-harm. Protective features on smart devices include RFID (Radiofrequency Identification Device) chips, fingerprint recognition, biometric sensors, machine locks, and magnetic kit.

MARKET DYNAMICS

KEY DRIVERS

-

Growing need

-

Geopolitical conflict

-

Higher effectiveness

RESTRAINTS

-

Stringent government rule

-

Illegal usage

OPPORTUNITIES

-

Market expansion

-

Modern enhancement

CHALLENGES

-

Middle East & Africa conflict

-

High cost

THE IMPACT OF COVID-19

According to the SNS Insider, the current projections for the growth of the global smart market by 2030 are expected to be lower than the previous COVID-19 estimates. The epidemic has had a devastating effect on the aviation, defense, and maritime industry worldwide. In the defense industry, due to declining tax revenues by declining GDP, it is also expected to reduce the demand for new aircraft, submarines, underground vehicles, and related defense application programs over the next few years. This is also expected to reduce the need for smart weapons.

Many governments around the world are focused on controlling the COVID-19 outbreak in their countries. Therefore, they invest heavily in health care and vaccine development. Therefore, the cost of protection in new systems is expected to decrease over the next few years. The cost of protection is expected to increase gradually during the forecast period after the end of the epidemic.

By Product

Missiles

The missiles segment held the most market share and is expected to grow at the fastest rate during the review period. This is due to the increased development of technologically advanced missiles as well as increased global demand.

Munitions

During the projection period, this category is expected to develop at a stable rate. This is due to a rise in the demand for munitions as weapons.

Guided Projectiles

During the forecast period, this segment is expected to have the greatest CAGR. This is owing to the rising use of guided projectiles by military forces around the world for UAVs, fighter jets, and helicopters.

By platform

The market is divided into three categories according to on the platform: air, land, and naval.

During the forecast period, the land segment is expected to increase the fastest. Increased defense spending, rapid military force expansion, and increased procurement of smart weapons will drive segmental growth. CGI has signed a contract with the United States Army to assist its Aviation and Missile Command programs. The contract was valued at USD 92.5 million. The air segment will experience significant expansion as air forces increase their desire for precision weaponry. The DRDO-developed Smart Anti-Airfield Weapon was launched from the Indian Air Force's Sukhoi Su-30MKI and SEPECAT Jaguar aircraft. The naval segment will experience moderate growth as naval forces increase their procurement of directed energy weapons.

By Technology

The development of technologically advanced products will drive the most rapid growth in the laser guidance segment. The market is classified into laser guidance, infrared guidance, radar guidance, satellite guidance, and others based on technology.

The laser guidance market is expected to increase at an exponential rate in the future years. The advent of cutting-edge technology, such as lasers, has resulted in increased precision and operating efficiency. During the forecast period, the satellite guidance segment is expected to increase significantly. The increase is attributed to an increase in demand for GPS-guided smart guns, which can work efficiently even in adverse weather conditions.

COMPETITIVE LANDSCAPE

The worldwide smart weapons market is likely to expand significantly in the future years as defense spending and navy modernization plans increase. The presence of various worldwide and regional suppliers characterizes the global smart weapons industry. The market is extremely competitive, with all firms attempting to achieve the greatest possible market share. The primary variables influencing global market growth include frequent changes in government policies, fierce rivalry, and government restrictions. The vendors compete on price, product quality, and dependability.

KEY MARKET SEGMENTATION

By Technology:

-

Laser

-

Radar

-

GPS

-

Infrared

-

Others

By Platform:

-

Air

-

Land

-

Naval

By Product:

-

Telescopic Sight

-

Collimating Optical Sight

-

Reflex Sight

-

Missiles

-

Munitions

-

Guided Projectiles

-

Guided Rockets

-

Precision Guided Firearms

REGIONAL ANALYSIS

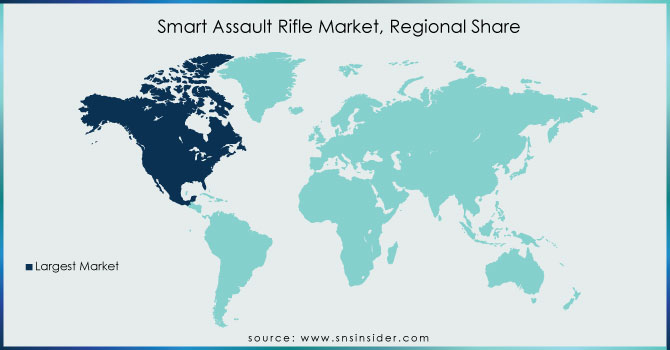

North America is made up of two large countries: the United States and Canada. North America leads the world in military spending and technology breakthroughs, and there is a huge demand for smart weaponry. Although Canada invests in the development of such advanced weaponry, the country's smart weapons business is mostly reliant on the United States. Because of the presence of significant manufacturers such as Lockheed Martin, Raytheon Technologies Corporation, and Northrop Grumman, the region held the greatest proportion of the overall market in 2022.

Furthermore, the increased military expenditures by the US Department of Defense on smart weapons in recent years have resulted in a major surge in demand in the regional market. APAC Races Ahead at the Quickest Rate as China and India Take the Lead SNS Insider expects the Asia-Pacific market to grow at the fastest rate during the forecast period, owing to key economies' increased defense spending. Due to increased investments in smart weaponry, major countries such as China, Japan, India, and Australia are driving market expansion in Asia-Pacific.

Need any customization research on Smart Assault Rifle Market - Enquiry Now

REGIONAL COVERAGE:

North America

-

USA

-

Canada

-

Mexico

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

Asia-Pacific

-

Japan

-

South Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

KEY PLAYERS

The Key Players are Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems, PLC, The Boeing Company, L-3 Communications Holdings, Inc., MBDA, Inc, General Dynamics Corporation, Orbital ATK, Thales Group, Textron Inc, Rheinmetall Ag & Other Players.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 17.35 Billion |

| Market Size by 2032 | US$ 30.64 Billion |

| CAGR | CAGR of 6.81% From 2023 to 2030 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Telescopic Sight, Collimating Optical Sight, Reflex Sight, Missiles, Munitions, Guided Rockets, Guided Projectiles, Guided Firearms) • By Technology (Infrared, Laser, Radar, Global Positioning System, and Others) • By Platform (Land, Naval, and Air) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems, PLC, The Boeing Company, L-3 Communications Holdings, Inc., MBDA, Inc, General Dynamics Corporation, Orbital ATK, Thales Group, Textron Inc, Rheinmetall Ag |

| DRIVERS | • Growing need • Geopolitical conflict • Higher effectiveness |

| RESTRAINTS | • Stringent government rule • Illegal usage |

Frequently Asked Questions

Stringent government rule and illegal usage are the restraining factors of the Smart Assault Rifle Market.

North America region dominated the Smart Assault Rifle Market.

The key players of the Smart Assault Rifle Market are Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems, PLC, The Boeing Company, L-3 Communications Holdings, Inc., MBDA, Inc, General Dynamics Corporation, Orbital ATK, Thales Group, Textron Inc, and Rheinmetall Ag.

The growth rate of the Smart Assault Rifle Market is 6.81% over the forecast period 2024-2032.

The market size of the Smart Assault Rifle Market was valued at USD 17.35 billion in 2023.

Get in Touch