Specialty Generics Market Report Scope & Overview:

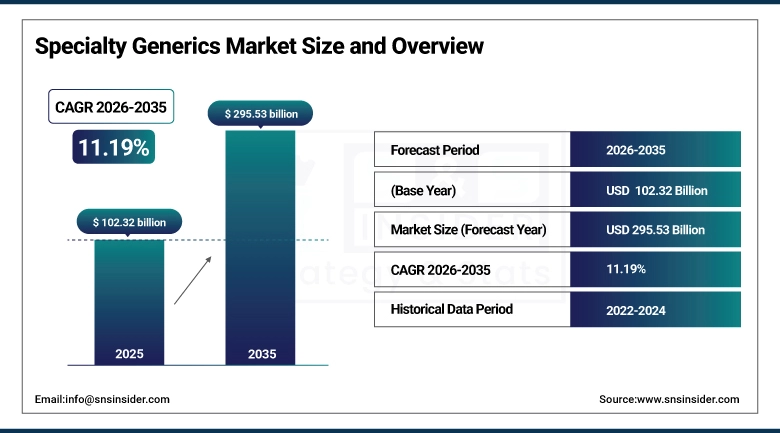

The Specialty Generics Market was estimated at USD 102.32 billion in 2025 and is expected to reach USD 295.53 billion by 2035 and grow at a CAGR of 11.19% over the forecast period of 2026-2035.

The growth in the Specialty Generics Market is fuelled by the increase in cases of chronic diseases including cancer, diabetes, and autoimmune disorders, leading to an increased requirement for cost-effective medicines. The expiry of patents on expensive specialty drugs is resulting in higher utilization of biosimilars. An increase in access to healthcare in developing nations, favorable government regulations, and greater awareness about generic biologics is driving market growth. Moreover, rising healthcare spending and robust pipeline developments are propelling market growth.

For instance, the World Health Organization estimates that the number of persons aged 80 years or older is projected to triple between 2020 and 2025, reaching 424 million, directly related to the increased incidence of chronic diseases, including cancer, diabetes, and arthritis.

Market Size and Forecast:

-

Market Size in 2025: USD 102.32 Billion

-

Market Size by 2035: USD 295.53 Billion

-

CAGR: 11.19% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Specialty Generics Market - Request Free Sample Report

Specialty Generics Market Trends:

-

Rising demand for cost-effective treatment alternatives to branded drugs is driving the specialty generics market.

-

Growing prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders is boosting market growth.

-

Expansion of patent expirations for high-value specialty drugs is fueling generic drug entry.

-

Increasing focus on biosimilars and complex generics is shaping adoption trends.

-

Advancements in drug formulation, delivery systems, and manufacturing technologies are enhancing product quality and efficacy.

-

Rising pressure on healthcare cost reduction and insurance coverage expansion is supporting market growth.

-

Collaborations between pharmaceutical manufacturers, healthcare providers, and regulatory bodies are accelerating innovation and global adoption.

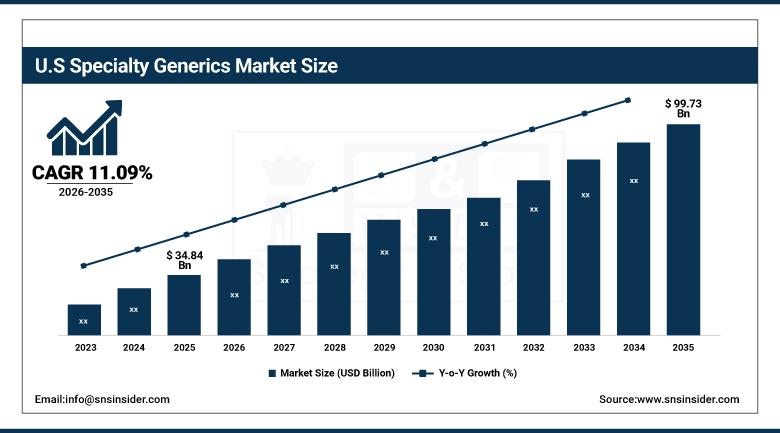

The U.S. Specialty Generics Market was valued at USD 34.84 Billion in 2025 and is expected to reach USD 99.73 Billion by 2035, growing at a CAGR of 11.09% from 2026-2035.

U.S. Specialty Generics Market is witnessing growth because of the increased incidence of chronic diseases, growing demand for specialty generic products at reduced prices, and high uptake of biosimilars. Other factors facilitating the growth of the market include the increase in healthcare spending, expiry of patents of leading specialty generics, and improved pharmaceutical infrastructure.

Specialty Generics Market Segment Insights:

-

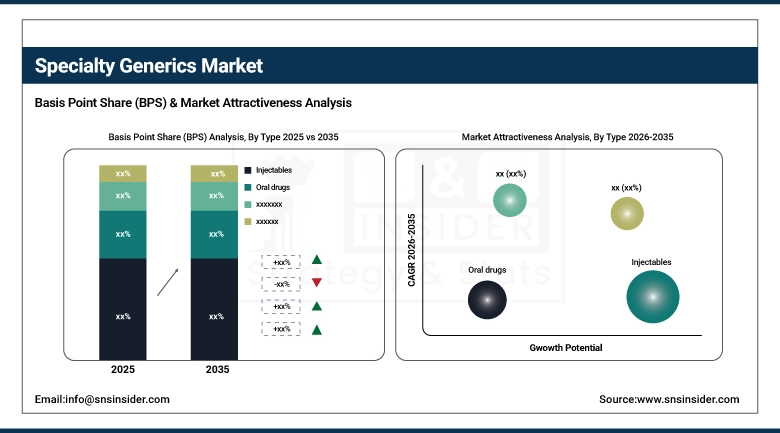

By Type, Injectables segment dominated the Specialty Generics Market in 2025 with ~62.35% share; Oral drugs segment fastest growing during 2026–2035.

-

By Indication, Inflammatory conditions segment dominated the Specialty Generics Market in 2025 with the largest share; Oncology segment fastest growing during 2026–2035.

-

By End Use, Specialty pharmacy segment dominated the Specialty Generics Market in 2025; Hospital pharmacy segment fastest growing during 2026–2035.

By Type, Injectables segment dominates the Specialty Generics Market, Oral Drugs segment expected to grow fastest

Injectables account for the largest share in the specialty generics market because of their importance in the treatment of complicated, chronic, and hospital-based illnesses requiring fast and accurate delivery of the drugs. Injectables are preferred in cases such as oncology, autoimmune disorders, and intensive care units when orally administered drugs prove inefficient. The rising prevalence of biosimilars and innovative formulations makes this a dominant market segment. Furthermore, high demand from hospitals and the rising availability of more affordable oral generics drive this trend.

Oral medications represent the fastest-growing segment owing to the rising preference among patients for a convenient and non-invasive way of treatment and better accessibility of specialty generics. With the improvement in formulation technology leading to an increase in the efficacy and availability of these drugs, oral specialty drugs are being used extensively for managing various chronic disorders. Escalating pressure on the healthcare sector along with a growing trend towards outpatient treatments is driving adoption.

By Indication, Inflammatory Conditions segment dominates the Specialty Generics Market, Oncology segment expected to grow fastest

The inflammatory segment account for the dominant position of specialty generics because of their high prevalence rate globally as well as the long duration of treatment that patients require. Some examples include rheumatoid arthritis, psoriasis, and other autoimmune diseases, which require ongoing treatment, leading to sustained demand for specialty generics. The presence of more affordable biosimilars and immunosuppressants is another factor behind this market dominance.

Oncology is the fastest-growing segment because of the increasing prevalence of cancer cases in the world. Cancer treatment methods have become expensive over time, making patients seek cheaper treatment. The segment is gaining popularity because of the development of specialty generics and biosimilars that are inexpensive and effective. Advances in targeted cancer treatment and increased healthcare access are some of the factors boosting the growth rate in the segment.

By End Use, Specialty Pharmacies segment dominates the Specialty Generics Market, Hospital Pharmacies segment expected to grow fastest

Specialty pharmacies dominate the market since they have a specialization in dealing with expensive drugs that require unique handling procedures. Their significance is highlighted by their contribution to the management of long-term and rare medical conditions through personalized services and the guarantee of compliance with the drugs prescribed. In addition, they ensure effective coordination between health care providers and insurance schemes, increasing their prominence in generic specialty drug distribution.

The hospital pharmacies have experienced the highest growth rate among the different segments. This growth is attributed to the high rates of inpatient medication and the rising use of specialty generics in clinical settings. There are rising concerns about the increase in medical costs, which requires hospitals to stock more cost-effective specialty generics in their formularies. Furthermore, the increasing number of patients with complicated diseases needing urgent and controlled administration of drugs is contributing to the growth.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88.9% |

|

Europe |

United Kingdom |

20.8% |

|

Asia Pacific |

Australia |

7.1% |

|

Middle East & Africa |

UAE |

13.4% |

|

Latin America |

Brazil |

52.2% |

North America Specialty Generics Market Insights:

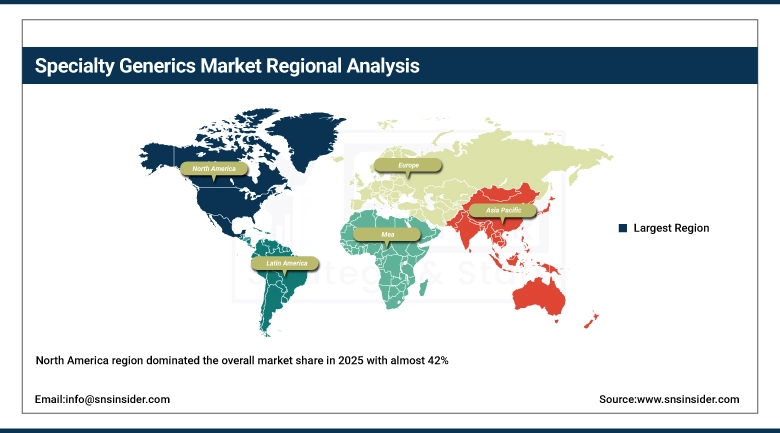

The specialty generics market in the North America region dominated the overall market share in 2025 with almost 42%. Factors such as well-developed health care infrastructure, increased utilization of specialty medicines, and an increase in the incidence rate of cancer and autoimmune diseases are the factors that drive the growth of the market in the region. Apart from this, the presence of leading pharmaceutical companies, efficient reimbursement structure, and supportive government regulations towards biosimilars also play important roles in driving market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Specialty Generics Market Insights:

Asia-Pacific is the fastest-growing market for specialty generics owing to the fast development of healthcare infrastructure and patient access to effective therapies. The factors contributing to the demand include the rising prevalence of chronic diseases, increased patient population, and greater awareness about cost-effective treatment methods. There is an increase in government support for affordable healthcare and acceptance of generic drugs. Also, the increased investment from multinational pharma firms, establishment of specialty pharmacies, and conducting clinical trials have added pace to market growth.

Europe Specialty Generics Market Insights:

Europe Specialty Generics Market is witnessing consistent growth due to its robust healthcare infrastructure, growing acceptance of biosimilars, and escalating demand for affordable treatments. The prevalence of chronic conditions and favorable regulatory environment is fostering fast-track approval processes for specialty generics. Countries like Germany, France, and the United Kingdom are dominating this market owing to their higher expenditure on healthcare and pharmaceutical infrastructure. Aging population and the need to cut down healthcare spending are adding to the future growth prospects of the market.

Middle East & Africa and Latin America Specialty Generics Market Insights:

Middle East & Africa and Latin America Specialty Generics Market will experience gradual growth because of better healthcare facilities and increased demand for cost-effective medications. Governments are concentrating on providing more healthcare services, along with generics and biosimilars. Countries like Brazil, Mexico, South Africa, and UAE have experienced higher adoption rates owing to the increased prevalence of chronic diseases and health reform policies. Nevertheless, the lack of infrastructure continues to hinder rapid market penetration.

Specialty Generics Market Growth Drivers:

-

Rising Demand for Affordable Specialty Medicines and Expanding Chronic Disease Burden Driving Strong Growth in Specialty Generics Market Globally

The increase in the number of people suffering from chronic diseases like cancer, diabetes, heart diseases, and autoimmune diseases is fueling the demand for specialty generics across the globe. Specialty generics offer an economically sound option that can be used for treating patients suffering from chronic diseases and providing them relief at a lower price than branded specialty drugs. The increase in healthcare spending and the increased pressure on health systems have made it essential for healthcare professionals to embrace economically feasible treatment options. Patent expiries on some best-selling drugs and specialty drugs have created many market opportunities.

Specialty Generics Market Restraints:

-

Stringent Regulatory Approval Processes and Complex Manufacturing Requirements Limiting Entry and Expansion in Specialty Generics Market

The rigorous regulatory standards for obtaining approval for specialty generics, especially biosimilars, pose substantial difficulties for producers. The complicated nature of clinical trials, stringent quality specifications, and extended approval periods raise development expenses and delay the time to market for such products. Large investments in scientific research and manufacturing facilities discourage smaller pharmaceutical organizations from entering the market. In addition, differences in regulatory standards among various geographical locations present additional obstacles for the expansion of the product into the international market environment. Furthermore, the production process for specialty generics entails sophisticated technology, making its manufacture difficult.

Specialty Generics Market Opportunities:

-

Rising Adoption of Biosimilars and Increasing Investment in Biopharmaceutical Research Driving Innovation in Specialty Generics Market

Increased investments and research and development in the biopharmaceutical sector is driving innovation in biosimilars and specialty generic drugs. Pharmaceutical companies have been emphasizing on producing more complex compounds that provide effective and safer medicines at cost-effective prices. Collaborations between biotechnology companies and leading pharmaceutical companies have also been increasing which helps in accelerating their processes. Regulatory agencies also play an important role in promoting the development of biosimilars as it leads to increased competition and better availability of medications. Increased interest in targeted therapeutics in the field of cancer therapy and immunology therapies is also contributing to the innovation process. Advancements in biotechnological techniques and cell culture technologies will contribute significantly in reducing costs and growing in the market.

Recent Developments:

-

2025: Sun Pharma expanded specialty portfolio through acquisition of Checkpoint Therapeutics, strengthening oncology-focused specialty generics and immunotherapy pipeline in regulated markets, enhancing high-margin specialty medicine presence globally

-

2025: Cipla expanded specialty and complex generics portfolio in respiratory and oncology segments, strengthening differentiated product pipeline and improving access in global markets through strategic partnerships and product launches.

-

2024: Sun Pharma completed acquisition of Taro Pharmaceuticals stake, expanding specialty generics and dermatology-focused portfolio across US markets, strengthening branded generics leadership.

Specialty Generics Market Key Players:

-

Teva Pharmaceutical Industries Ltd.

-

Sandoz (Novartis Division)

-

Viatris Inc.

-

Sun Pharmaceutical Industries Ltd.

-

Lupin Limited

-

Dr. Reddy’s Laboratories Ltd.

-

Aurobindo Pharma Ltd.

-

Zydus Lifesciences Ltd.

-

Cipla Ltd.

-

Fresenius Kabi AG

-

Mylan Pharmaceuticals (now Viatris)

-

Amneal Pharmaceuticals, Inc.

-

Hikma Pharmaceuticals PLC

-

Apotex Inc.

-

Stada Arzneimittel AG

-

Torrent Pharmaceuticals Ltd.

-

Alvogen

-

Glenmark Pharmaceuticals Ltd.

-

Bausch Health Companies Inc.

-

Endo International plc

Specialty Generics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 102.32 Billion |

| Market Size by 2035 | USD 295.53 Billion |

| CAGR | CAGR of 11.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Oral drugs, Injectables, and Others) • By Application (Hepatitis C, Inflammatory conditions, Oncology, Multiple sclerosis, and Others) • By End Use (Hospital pharmacy, Specialty pharmacy, and Retail pharmacy) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Teva Pharmaceutical Industries Ltd., Sandoz (Novartis Division), Viatris Inc., Sun Pharmaceutical Industries Ltd., Lupin Limited, Dr. Reddy’s Laboratories Ltd., Aurobindo Pharma Ltd., Zydus Lifesciences Ltd., Cipla Ltd., Fresenius Kabi AG, Mylan Pharmaceuticals (now Viatris), Amneal Pharmaceuticals, Inc., Hikma Pharmaceuticals PLC, Apotex Inc., Stada Arzneimittel AG, Torrent Pharmaceuticals Ltd., Alvogen, Glenmark Pharmaceuticals Ltd., Bausch Health Companies Inc., Endo International plc |

Frequently Asked Questions

The Specialty Generics Market is expected to grow at a CAGR of 11.19% from 2026 to 2035.

The Specialty Generics Market was valued at USD 102.32 billion in 2025.

Rising Demand for Affordable Specialty Medicines and Expanding Chronic Disease Burden Driving Strong Growth in Specialty Generics Market Globally.

The Inflammatory conditions segment dominated the Specialty Generics Market in 2025.

North America dominated the Specialty Generics Market in 2025.

Get in Touch