Sputter Coatings Market Size & Trends:

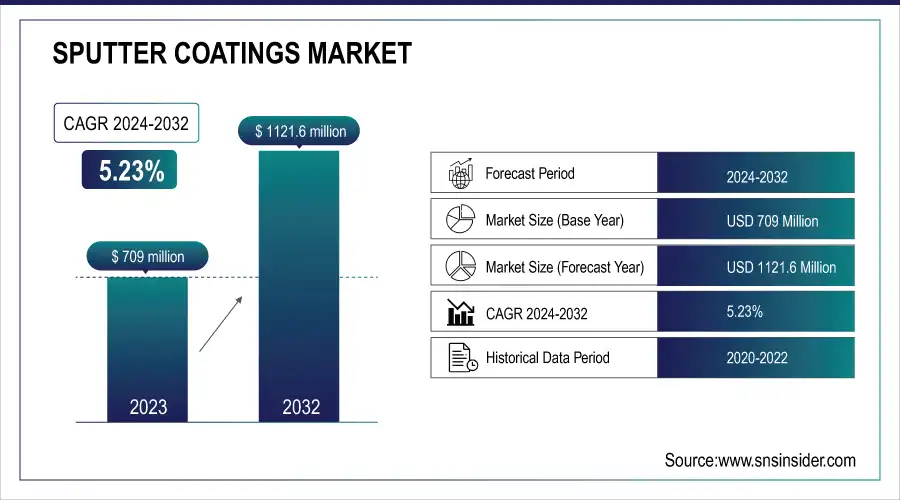

The Sputter Coatings Market was valued at USD 709 Million in 2023 and is projected to reach USD 1121.6 Million by 2032, growing at a CAGR of 5.23% from 2024 to 2032.

This growth is driven by significant advancements in sputter coating materials, including the development of nanomaterials and hybrid coatings that offer superior performance in various high-demand industries like electronics, automotive, and aerospace.

Market Size and Forecast:

-

Market Size in 2023: USD 709 Million

-

Market Size by 2032: USD 1121.6 Million

-

CAGR: 5.23% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

To Get more information on Sputter Coatings Market - Request Free Sample Report

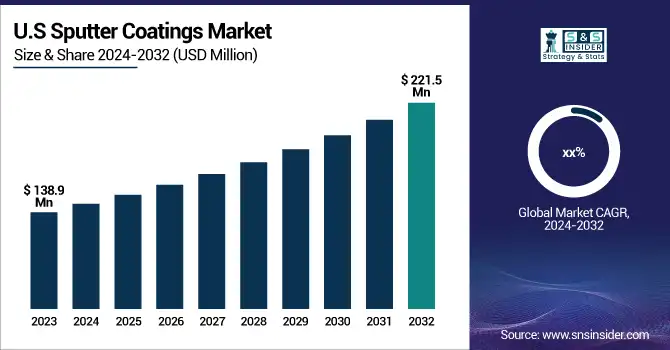

Additionally, the market is witnessing a rise in sputter coating applications in 3D printing and additive manufacturing, enabling precise, high-quality coatings for intricate parts. A notable trend is the increasing demand for sustainability and eco-friendly coatings, with the US market for such coatings valued at USD 138.9 million in 2023 and expected to reach USD 221.5 million by 2032. These eco-friendly coatings are gaining traction due to their reduced environmental impact and growing focus on energy efficiency. The continued development of these innovations, combined with strong market demand in emerging applications, positions the sputter coatings market for sustained growth through the next decade.

Sputter Coatings Market Trends:

-

Growing demand for thin-film coatings in semiconductor and microelectronics manufacturing is driving market expansion.

-

Increasing adoption of sputter coating technology in solar panels and renewable energy applications is boosting industry growth.

-

Rising use of decorative and protective coatings in automotive and architectural glass sectors is supporting market demand.

-

Advancements in vacuum deposition technologies and magnetron sputtering systems are improving coating efficiency and performance.

-

Expanding applications in medical devices and optical components are contributing to steady revenue growth.

-

Continuous R&D investments and collaborations among material science companies and electronics manufacturers are strengthening innovation and market penetration.

Sputter Coatings Market Dynamics:

Drivers:

-

Advancements in Sputter Coating for 3D Printing and Additive Manufacturing

The growing adoption of 3D printing and additive manufacturing technologies is transforming industries such as aerospace, automotive, and medical devices by driving the demand for sputter coatings. These coatings enhance the performance and durability of 3D printed parts, particularly for intricate and customized applications. In aerospace and automotive, sputter coatings improve components like turbine blades and sensors by offering superior wear resistance, thermal stability, and electrical conductivity. In medical devices, they ensure biocompatibility and corrosion resistance. Gold sputter coatings are widely used for low- to moderate-magnification imaging (<50,000x), providing ease of use, cost-efficiency, and suitability for thermally sensitive materials. Platinum coatings, with their finer grain size, are ideal for higher magnifications (50,000–200,000x), while iridium coatings are preferred for ultrahigh resolution imaging (>200,000x) due to their non-oxidizing nature and robustness. These advancements make sputter coating indispensable in improving surface quality and meeting the increasing demand for high-performance, specialized products in additive manufacturing.

Restraints:

-

The Limitation of Thin Coatings in Sputter Coating Technology for Heavy-Duty Industrial Applications

One of the main limitations of sputter coatings is the relatively thin coating layers they produce, which may not be suitable for certain applications that require thicker coatings for enhanced durability and protection. This is particularly important in heavy-duty industrial applications that experience extreme wear and abrasion or thermal extremes, where a thin sputter coating alone can be inadequate to protect components. Coatings executed through some other means for example thermal spraying or chemical vapor deposition (CVD) can enable thicker coverings on lesser components to keep sufficient coverage to perform. This constraint limits the widespread usage of sputter coatings in fields such as mining, oil and gas, and heavy machinery, which requires a thicker and, in turn, more enduring coating to endure extreme conditions.

Opportunities:

-

The Growing Demand for Sputter Coatings in Nano-Coatings and Specialty Applications across Aerospace, Optics, and Defense

The increasing adoption of nano-coatings across industries such as aerospace, optics, and defense presents a significant opportunity for sputter coatings. Nano-coatings are highly sought after for their ability to provide enhanced performance, durability, and functionality at the microscopic level. These metals play a crucial role in the performance, coating for sputter offer excellent control of layer thickness and uniformity, making them ideal candidates for high-performance applications. In the aerospace field, sputtered coatings can be used to enhance the corrosion resistance, thermal stability, and wear resistance of parts such as turbine blades and sensors. Likewise, Lens, Mirrors, and light-sensitive components use these coatings in optics to improve the performance, clarity and efficiency. Adoption of sputter coating in the electronic devices segment has been friendly owing to their interfacial weak links, which made them ideal to extend the life and functionality of critical components in the defense sector from harsh environments. With industries demanding more advanced technologies, aspects such as these specialty applications will give rise to the demand for sputter coatings.

Challenges:

-

High Equipment and Operational Costs in Sputter Coating Market

The high equipment costs and operational expenses associated with sputter coating processes are significant barriers, particularly for small and medium-sized enterprises (SMEs). Sputter coating equipment requires sophisticated machinery that operates under high vacuum conditions, and maintaining such systems incurs substantial costs in terms of energy, upkeep, and specialized workforce. Additionally, the complexity of controlling variables such as pressure, power, and temperature during the sputtering process requires advanced technologies and constant monitoring, further increasing the operational costs. For SMEs, these financial burdens can make it difficult to justify the investment, particularly when compared to other coating technologies that may have lower initial costs and operational requirements. This cost-related challenge limits the adoption of sputter coatings in various industries, slowing market growth and inhibiting smaller players from competing with larger corporations that can absorb these high operational expenditures.

Sputter Coatings Industry Segmentation Analysis:

By Substrate

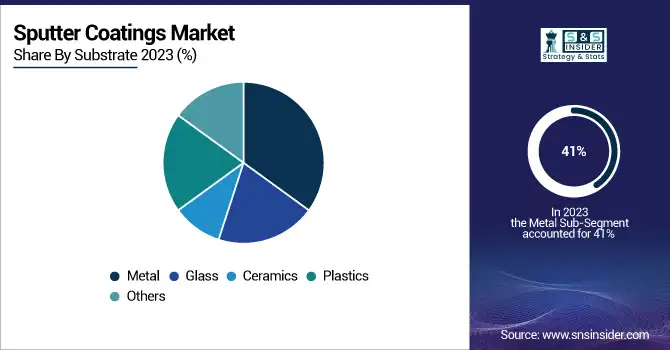

In 2023, the metal segment held the largest share of the sputter coating market, accounting for approximately 41% of the revenue. This dominance is driven by the extensive use of metal coatings in high-performance applications across a variety of industries, including electronics, aerospace, automotive, and optics. Metals such as gold, silver, platinum, and copper are commonly used in sputter coatings due to their exceptional corrosion resistance, thermal stability, and electrical conductivity. In the electronics industry, metal coatings are essential for semiconductors, solar cells, and displays, ensuring better efficiency and conductivity. Similarly, in aerospace and automotive applications, metal coatings enhance the durability and wear resistance of critical components like sensors, turbine blades, and fuel cells. The growing demand for metal sputter coatings in these industries has solidified its position as the largest segment in the market.

The glass segment is expected to be the fastest-growing in the sputter coating market from 2024 to 2032. This growth is driven by the increasing demand for architectural glass and display technologies, particularly in applications such as smart windows, solar panels, and touchscreens. Glass coatings enhance the properties of these surfaces, offering benefits like anti-reflective coatings, conductivity, and aesthetic finishes. The growing emphasis on sustainable building practices and energy-efficient solutions further fuels the demand for glass coatings, making it a key segment with robust expansion prospects in the coming years.

By Application

In 2023, the electronics segment dominated the sputter coating market, capturing approximately 45% of the total revenue. This significant share is largely due to the widespread application of sputter coatings in various electronic components, such as semiconductors, displays, and solar cells. Sputter coatings are essential for enhancing electrical conductivity, improving performance, and providing corrosion resistance in these components. In semiconductors, metal sputter coatings are crucial for the fabrication of microchips, ensuring efficient energy flow and reliability. The rise in smartphone production, consumer electronics, and solar energy technologies has contributed to the rapid growth in this segment. Additionally, sputter coatings are used in circuit boards and displays to enhance the durability and functionality of electronic devices. The electronics industry's continuous innovation and demand for more efficient and advanced materials make it the largest revenue-generating segment in the sputter coating market.

The architectural glass segment is projected to be the fastest-growing in the sputter coating market from 2024 to 2032. The market is growing due to the increasing demand for energy-efficient buildings and the rising adoption of smart windows. Sputter process coatings do improve building glass thermal insulation, UV protection, and optical property enhancement for modern building projects. The segment is also benefitting from the increasing emphasis on sustainable architecture and green building ratings, including LEED certification. With the goal of conserving energy through better regulated indoor temperatures, solar reflective coatings technology drives glass materials forward even more. The architectural glass segment will be the fastest growing segment of the sputter coating market owing to the rise in urbanization and demand for eco-friendly overhead buildings.

By Sputter Coatings

In 2023, the metal sputter coatings segment dominated the sputter coating market, accounting for around 50% of the total revenue. This dominance is driven by the widespread use of metal coatings in high-performance industries, such as electronics, automotive, aerospace, and optics. Metals like gold, silver, platinum, and titanium are favored for their electrical conductivity, thermal stability, corrosion resistance, and wear resistance. In the electronics sector, metal sputter coatings are essential for components like semiconductors, displays, and solar panels, ensuring improved durability and efficiency. In aerospace and automotive industries, metal coatings protect critical components from extreme conditions. The increasing demand for precision in optical lenses and mirror coatings further boosts the segment’s growth. As these industries expand and technology advances, metal sputter coatings remain central to innovations in high-performance applications.

The alloy sputter coatings segment is expected to be the fastest-growing over the forecast period from 2024 to 2032. This growth is driven by the increasing demand for advanced, high-performance materials in industries such as electronics, aerospace, and automotive. Alloy coatings offer superior durability, corrosion resistance, and thermal stability compared to pure metals, making them ideal for high-stress applications. They are particularly beneficial in electronics for microelectronics and semiconductors, where they ensure efficient functionality and longer product lifespans. Additionally, aerospace and automotive sectors rely on alloy coatings to protect components from extreme environments and enhance their performance. The growing adoption of these coatings in solar energy applications, along with customized alloys for specialized uses, positions the alloy sputter coatings segment for significant expansion during the forecast period.

Sputter Coatings Market Regional Analysis:

In 2023, the Asia-Pacific region held the largest share of the sputter coating market, accounting for approximately 40% of the total revenue. This dominance is driven by the region's rapid industrialization, significant presence of electronics, automotive, and aerospace sectors, and high demand for advanced coatings. Countries like China, Japan, and South Korea lead the way with cutting-edge manufacturing technologies, bolstering the demand for sputter coatings in semiconductors, solar panels, and electronics. Furthermore, the growing emphasis on clean energy solutions and innovative manufacturing processes in the region is fueling the market's growth. The region’s strong manufacturing base and increasing adoption of advanced materials make Asia-Pacific the dominant player in the sputter coating market, with continuous investment in high-tech industries driving further expansion.

North America is expected to be the fastest-growing region in the sputter coating market over the forecast period from 2024 to 2032. This growth is driven by the region's robust electronics and automotive industries, which demand advanced sputter coatings for high-performance applications. The United States and Canada are leading the charge with their significant investments in research and development and increasing adoption of innovative manufacturing techniques. In particular, the semiconductor industry, critical to North America's technological infrastructure, relies heavily on sputter coatings for the fabrication of integrated circuits and displays. Additionally, the growing emphasis on renewable energy technologies and advanced materials further supports the region’s expansion. North America's focus on sustainability, along with continuous advancements in coating technologies for various industries like aerospace, positions the region for significant growth throughout the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Sputter Coatings Market Key Players:

-

Materion Corporation (USA) - Sputtering Targets, Thin Film Materials, Bonding Materials, Optical Coatings

-

ULVAC, Inc. (Japan) - Vacuum Coating Systems, Sputtering Targets, Thin Film Deposition Equipment

-

JX Nippon Mining & Metal Corporation (Japan) - Sputtering Targets, Precious Metal Products, Electronic Materials

-

Heraeus Holding (Germany) - Sputtering Targets, Thin Film Materials, Metal Alloys, Thermocouples

-

Honeywell International Inc. (USA) - Advanced Materials, Thin Film Coatings, Semiconductor Materials

-

Umicore Group (Belgium) - Sputtering Targets, Advanced Materials for Electronics, Catalysts, Battery Materials

-

Praxair S.T. Technology, Inc. (USA) - Sputtering Targets, Thin Film Coatings, Industrial Gases

-

Tosoh SMD, Inc. (Japan) - Sputtering Targets, Thin Film Materials, Chemical Vapor Deposition Products

-

Soleras Advanced Coatings (USA) - Sputtering Targets, Coating Services for Electronics and Aerospace

-

China Rare Metal Material Co., Ltd. (China) - Sputtering Targets, Rare Metal Alloys, Metal Coatings

-

JIANGYIN ENTRET COATING TECHNOLOGY CO., LTD (China) - Sputtering Targets, Coating Materials for Electronics and Solar Panels

-

GRIKIN Advanced Materials Co., Ltd. (China) - Sputtering Targets, Thin Film Materials, Advanced Coatings for Semiconductor Industry

Some of the potential customer companies that use sputter coatings in various industries:

Electronics Industry

-

Intel Corporation (Semiconductor Manufacturing)

-

TSMC (Taiwan Semiconductor Manufacturing Company) (Semiconductor Manufacturing)

-

Samsung Electronics (Display Manufacturing, Consumer Electronics)

-

LG Display (Display Manufacturing)

Aerospace Industry

-

Boeing (Aircraft Manufacturing)

-

Airbus (Aircraft Manufacturing)

-

Lockheed Martin (Space and Defense Technologies)

-

SpaceX (Space Technologies)

Automotive Industry

-

General Motors (Automotive OEM)

-

Toyota Motor Corporation (Automotive OEM)

-

BMW (Automotive OEM)

-

Bosch (Automotive Electronics and Sensors)

-

Continental AG (Automotive Electronics and Sensors)

Medical Device Manufacturers

-

Medtronic (Medical Devices, Implants)

-

Johnson & Johnson (Medical Devices)

-

Stryker Corporation (Surgical Equipment)

-

Siemens Healthineers (Medical Imaging Equipment)

Optics and Optical Coatings

-

Nikon Corporation (Optical Lenses and Coatings)

-

Carl Zeiss AG (Optical Lenses and Coatings)

-

Edmund Optics (Optical Coating Services)

-

Optics Balzers (Optical Coatings)

Energy Sector

-

First Solar (Solar Panels Manufacturing)

-

SunPower (Solar Energy Solutions)

-

Tesla (Energy Storage and Solar Solutions)

-

LG Chem (Battery Solutions)

Research and Development Institutions

-

Massachusetts Institute of Technology (MIT)

-

Stanford University

-

California Institute of Technology (Caltech)

-

National Renewable Energy Laboratory (NREL)

Recent Development

-

January 1, 2024, Materion announced that SAE-AMS approved aerospace specification AMS4355 for SupremEX 225XE, a lightweight aluminum metal matrix composite with 25% ultrafine silicon carbide particles, enhancing strength and stiffness for aerospace applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 709 Million |

| Market Size by 2032 | USD 1121.6 Million |

| CAGR | CAGR of 5.23% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Substrate (Metal, Glass, Ceramics, Plastics, Others) • By Application(Electronics, Architectural glass, Automotive, Optics, Others) • By Sputter Coatings(Metal sputter coatings(Aluminum, Copper), Alloy sputter coatings(Stainless steel, Tungsten carbide), Ceramic sputter coatings, Compound sputter coatings, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Materion Corporation (USA), ULVAC, Inc. (Japan), JX Nippon Mining & Metal Corporation (Japan), Heraeus Holding (Germany), Honeywell International Inc. (USA), Umicore Group (Belgium), Praxair S.T. Technology, Inc. (USA), Tosoh SMD, Inc. (Japan), Soleras Advanced Coatings (USA), China Rare Metal Material Co., Ltd. (China), JIANGYIN ENTRET COATING TECHNOLOGY CO., LTD (China), and GRIKIN Advanced Materials Co., Ltd. (China). |

Frequently Asked Questions

North America dominated the Sputter Coatings Market in 2023.

The “Discrete Sensor Processor” segment dominated the Sputter Coatings Market.

Include the growing demand for advanced materials in electronics, aerospace, automotive, and medical industries, along with the rise of nanotechnology and the increasing adoption of sustainable coatings.

The Sputter Coatings Market was USD 709 Million in 2023 and is expected to Reach USD 1121.6 Million by 2032.

The Sputter Coatings Market is expected to grow at a CAGR of 5.23% during 2024-2032.

Get in Touch