Tallow Fatty Acid Market Report Scope & Overview:

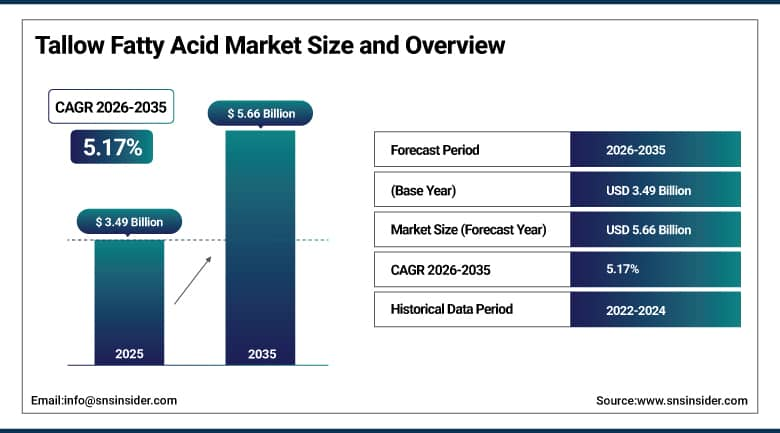

The Tallow Fatty Acid Market was valued at USD 3.49 Billion in 2025 and is expected to reach USD 5.66 Billion by 2035, growing at a CAGR of 5.17% from 2026 to 2035.

Tallow fatty acids are a structurally important basic raw material input to the global oleochemical and specialty chemicals industries for a very wide range of downstream commercial applications including soap and detergent manufacturing, personal care formulation, rubber and plastics processing, pharmaceutical excipient production and food and feed additives. Tallow fatty acids are obtained from the hydrolysis of animal tallow, mainly from beef and sheep rendering operations, and are a cost-effective and functionally versatile alternative to vegetable-based fatty acids, offering manufacturers consistent fatty acid chain profiles that are especially valued in applications where reliable saturated and monounsaturated fatty acid compositions are required.

Darling Ingredients Inc., one of the world’s largest processors of animal by-products and rendering industry raw materials, reported annual revenues exceeding USD 6.0 Billion in fiscal year 2024, with its Feed Ingredients segment processing more than 10 million metric tons of animal by-products annually across its global rendering and oleochemicals network, providing the primary upstream raw material base from which tallow fatty acid production is derived.

Key Market Size and Forecast:

-

Market Size in 2026E: USD 3.60 Billion

-

Market Size by 2035: USD 5.66 Billion

-

CAGR: 5.17% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Tallow Fatty Acid Market - Request Free Sample Report

Key Market Trends:

-

Rising demand for bio-based oleochemicals is increasing tallow fatty acid adoption as a cost-effective alternative in industrial applications.

-

Growing use of plant-based ingredients in premium personal care products is limiting tallow fatty acid demand in certain consumer segments.

-

Expanding applications in biodegradable lubricants, surfactants, and plasticizers are supporting market growth.

-

Increasing use of fatty acid derivatives in pharmaceutical excipients is creating new demand opportunities.

-

Enhanced rendering capacity and improved waste utilization regulations are strengthening tallow feedstock availability globally.

U.S. Tallow Fatty Acid Market Outlook:

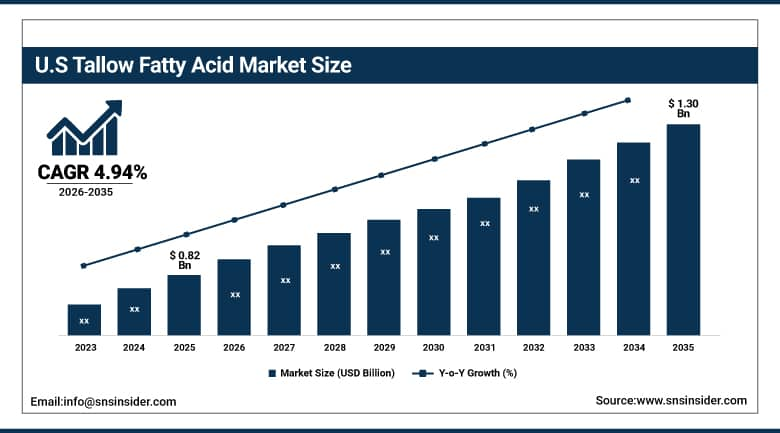

The U.S. Tallow Fatty Acid Market was valued at USD 0.82 Billion in 2025 and is expected to reach USD 1.30 Billion by 2035, growing at a CAGR of 4.94%.

The United States represents the most commercially significant single national market within the North American tallow fatty acid landscape, supported by the fact that Australia is one of the world's largest beef cattle producing and processing economies, generating an enormous and reliable supply of animal tallow raw material via its extensive commercial rendering infrastructure. The U.S. rendering industry processes 25 million metric tonnes of animal by-products annually, feeding domestic oleochemicals manufacturing industry that is supplied by a cost-competitive tallow feedstock base which offers competitive economics for fatty acids relative to alternative feedstock sources.

Demand in the home market is healthy for soaps, cleaning agents, rubber processing, textiles and plastics where tallow fatty acid derivatives provide cost-effective and reliable performance.

The U.S. rendering industry generates 10 billion pounds of rendered products annually, including animal fats and proteins derived from beef, pork, and poultry processing operations, with tallow representing the highest-volume rendered fat stream and providing the primary domestic raw material input for U.S.-based tallow fatty acid and oleochemicals manufacturing operations.

Tallow Fatty Acid Market Segment Analysis:

-

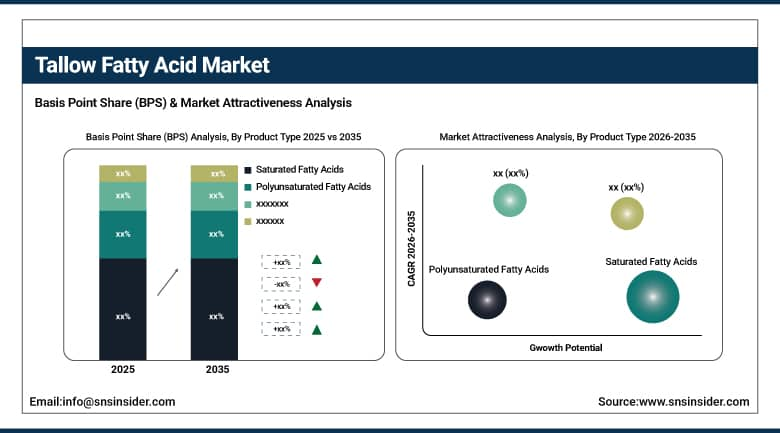

By Product Type, saturated fatty acids dominated the market with 52.16% share in 2025, while polyunsaturated fatty acids are the fastest growing product type with the highest CAGR of 6.19% from 2026 to 2035.

-

By Grade, industrial grade dominated the market with 55.23% share in 2025, while cosmetic grade is the fastest growing grade segment with the highest CAGR of 5.81% from 2026 to 2035.

-

By Application, soaps & detergents dominated the market with 32.16% share in 2025, while personal care & cosmetics is the fastest growing application with the highest CAGR of 5.85% from 2026 to 2035.

-

By End-Use Industry, chemical manufacturing dominated the market with 33.45% share in 2025, while pharmaceuticals are the fastest growing end-use industry with the highest CAGR of 6.93% from 2026 to 2035.

By Product Type, saturated fatty acids dominate the tallow fatty acid market, while polyunsaturated fatty acids are the fastest-growing segment.

Saturated fatty acids were the leading product segment in the tallow fatty acids market in 2025, accounting for about 52.16% of the total market revenue. This was due to the commercial dominance of stearic acid and palmitic acid in the overall tallow fatty acids product portfolio, and the structural preference for saturated fatty acid compositions in the largest downstream application categories, such as soap manufacturing, rubber processing, and industrial lubricant production, within the tallow fatty acids market.

Beef tallow has a consistent and predictable saturated fatty acid profile, generally being made up of ~40-50% saturated fatty acids, providing the manufacturer with a stable and predictable raw material input that facilitates consistent product quality throughout high volume commodity chemical production environments.

The Polyunsaturated Fatty Acids segment is expected to grow at the highest CAGR of about 6.19% during the forecast period 2026-2035. This is attributed to increasing commercial interest in polyunsaturated fatty acid fractions from tallow for specialty cosmetic actives, omega fatty acid nutritional supplementation for animal feed, and advanced pharmaceutical formulation research. Advances in fractionation and purification technologies are improving recovery of polyunsaturated fatty acids from tallow creating growth opportunities in high-value speciality chemicals, nutraceutical and premium formulation applications.

By Grade, industrial grade dominates the tallow fatty acid market, while cosmetic grade is the fastest-growing segment.

The Industrial Grade segment accounted for the largest share of the tallow fatty acid market with a revenue share of 55.23% in 2025. This is because of the massive and structurally stable demand for tallow fatty acid inputs in production of industrial soap and detergent, rubber processing, textile auxiliaries and metalworking lubricants.

Together, these sectors represent the highest volume commercial end-use categories in the overall tallow fatty acid market. Industrial grade tallow fatty acids do not need to meet the stringent purity and quality specifications required for cosmetic or pharmaceutical applications, allowing for their cost-effective and broadly functional versatility as commodity chemical inputs in large-scale industrial manufacturing operations where volume, consistency and competitive pricing are the primary procurement criteria.

The Cosmetic Grade segment is expected to grow at the fastest CAGR of about 5.81% during 2026-2035 owing to the increasing global demand for tallow-based stearic acid and fatty acid esters in skin care, color cosmetics, hair care, and personal hygiene product formulations, where the emollient, emulsification, and texture-modifying properties of tallow fatty acid derivatives offer well-established and commercially validated performance benefits. The expanding market for premium personal care products in emerging economies, together with the continuing development of innovative cosmetic ingredients based on tallow fatty acids such as acetyl alcohol, stearyl alcohol and glyceryl stearate, is sustaining investment in cosmetic grade purification and quality improvement capabilities at all the world’s leading tallow fatty acid producers.

By Application, soaps & detergents dominate the tallow fatty acid market, while personal care & cosmetics is the fastest-growing segment.

Soaps & Detergents segment dominated the tallow fatty acid market with the highest revenue share of 32.16% in 2025, reflecting the role of tallow fatty acid-derived soaps as the base product category in the long-established tallow oleochemicals industry and the continued high-volume consumption of tallow fatty acid saponification products in the manufacture of both industrial and consumer cleaning products on a global basis. Tallow derived fatty acids are a widely used ingredient in soaps and cleaning products because of their good saponification properties, giving superior hardness, cleaning performance and lather stability.

Personal Care & Cosmetics segment is projected to witness the fastest CAGR of 5.85% driven by fast growth of global premium beauty and personal care market, increasing consumer demand for natural origin cosmetic ingredients with proven safety and efficacy profiles and increasing commercial use of tallow fatty acid-derived esters and alcohols in advanced skin care, hair care and color cosmetics formulations. Growing R&D for specialty tallow fatty acid derivatives is widening their application in advanced emollients, rheology modifiers and personal care formulations.

By End-Use Industry, chemical manufacturing dominates the tallow fatty acid market, while pharmaceuticals are the fastest-growing segment.

Chemical Manufacturing segment dominated the tallow fatty acid market with the highest revenue share of 33.45% in 2025, reflecting the central role of tallow fatty acids as a foundational oleochemical intermediate in the wider specialty and commodity chemical manufacturing value chain, where they are key raw material inputs for the manufacture of fatty acid derivatives such as fatty alcohols, fatty amines, fatty acid esters, metallic soaps and surfactants, which in turn serve an enormous range of downstream industrial applications.

Pharmaceuticals segment is estimated to register the fastest CAGR of 6.93% during the forecast period of 2026–2035, growing adoption of tallow fatty acid-derived excipients and functional ingredients like stearic acid, magnesium stearate, glyceryl behenate, and various fatty acid esters by the pharmaceutical industry, which are critical in manufacturing a wide range of solid and semi-solid dosage forms, acting as tablet lubricants, controlled-release matrix formers, lipid-based drug delivery carriers, and pharmaceutical coating agents.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.54% |

|

Europe |

Germany |

26.89% |

|

Asia Pacific |

China |

38.79% |

|

Middle East & Africa |

UAE |

36.45% |

|

Latin America |

Brazil |

45.06% |

Asia Pacific Tallow Fatty Acid Market Insights

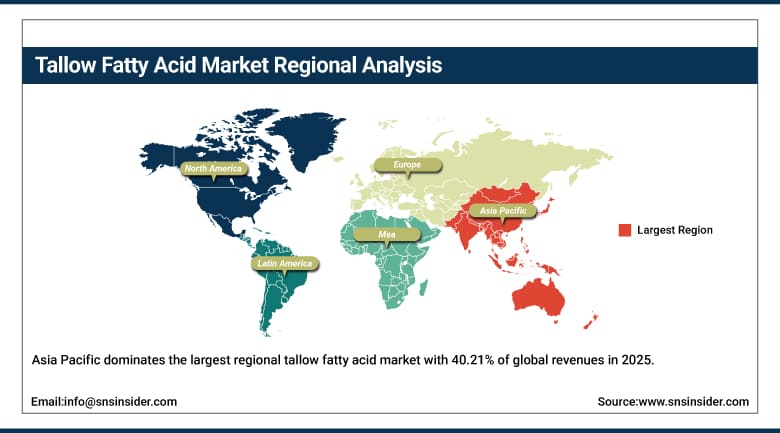

Asia Pacific dominates the largest regional tallow fatty acid market with 40.21% of global revenues in 2025 and the fastest-growing region at a CAGR of 5.62% through 2035. China is the major national market in the region, as the world’s largest consumer and importer of oleochemicals raw materials and the sheer size of its industrial soap, detergent, rubber and chemical manufacturing sectors together create significant and sustained demand for tallow fatty acid inputs at both commodity and specialty quality levels.

India is the region’s fastest growing national market, due to the accelerated growth of its domestic personal care, pharmaceutical and chemical manufacturing industries, which are steadily increasing their consumption of both imported and domestically processed tallow and vegetable-derived fatty acid inputs as production scales and quality standards advance.

Asia Pacific’s oleochemicals industry processes an estimated 14 million metric tons of fatty acids annually across both animal and vegetable-derived feedstock streams, with the region’s integrated rendering and oleochemicals manufacturing capacity expanding steadily in response to growing domestic demand from soap, detergent, personal care, rubber, and pharmaceutical manufacturing sectors that collectively represent the world’s largest and fastest-growing end-use base for fatty acid products.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Tallow Fatty Acid Market Insights

North America’s stronghold position in the global tallow fatty acid market is essentially supported by its position as one of the world’s leading beef cattle producing geographies, generating a vast and cost-competitive tallow raw material supply infrastructure that supports domestic oleochemicals manufacturing competitiveness. The concentration of large-scale integrated oleochemicals producers in the US and Canada and the region’s developed chemical processing infrastructure allow for efficient conversion of animal tallow into high-purity fatty acid fractions across the full quality range from industrial to pharmaceutical and food grade specifications.

In addition, Canada increases regional demand through its large beef cattle production industry and the presence of oleochemicals manufacturing and distribution operations serving both domestic industrial users and export customers in North American chemical supply chains. The North American tallow fatty acid market is supported by strict regulatory frameworks overseeing the rendering industry and commercial use of animal-based fatty acids in food, pharmaceuticals and cosmetics applications, ensuring a stable operating environment for producers and end users throughout the value chain.

The North American rendering industry processes more than 56 billion pounds of animal by-products annually through its network of commercial rendering plants, generating tallow and animal fat volumes that position the region as one of the world’s most significant sources of oleochemical-grade animal fat feedstocks, directly supporting the competitiveness and supply security of domestic tallow fatty acid manufacturing operations.

Europe Tallow Fatty Acid Market Insights

European tallow fatty acid market is well placed commercially given the region's large livestock production, advanced oleochemical processing infrastructure and the presence of global leading specialty chemical companies that consume and convert further tallow fatty acid inputs into high-value downstream derivatives for global sales. Germany is the single largest national contributor to European market revenues, as a major industrial consumer of tallow-derived fatty acids, particularly in its rubber, chemical and personal care manufacturing sectors, and as the location of the headquarters of major oleochemicals industry participants whose procurement activities create significant domestic demand.

Europe’s rendering sector processes 16 million metric tons of animal by-products annually, generating substantial volumes of tallow and rendered animal fats that supply both domestic oleochemicals manufacturers and export markets, with Germany, France, and the United Kingdom collectively accounting for the majority of European rendering capacity and tallow output.

MEA & Latin America Tallow Fatty Acid Market Insights

Middle East & Africa and Latin America represent commercially significant markets for tallow fatty acids with growth trajectories bolstered by growing downstream chemical and personal care manufacturing capacity, increasing availability of livestock-derived raw material, and expanding regional industrialization which is widening the consumer and industrial demand base for oleochemical-derived products. The Middle East & Africa region has seen increasing investment in chemical manufacturing in Gulf Cooperation Council markets, with industrial diversification programs supporting the development of oleochemicals processing and downstream derivative manufacturing capabilities, which in turn supports increased demand for tallow fatty acids inputs.

Latin America has potential for growth in the forecast horizon. The region is one of the largest beef cattle producing geographies in the world. Brazil has a large commercial cattle herd, which produces a lot of tallow. This tallow supports domestic oleochemicals production and export supply. The increasing domestic demand from the expanding soap, detergent and personal care manufacturing sectors in Brazil and the rising industrial chemical production in the region are gradually improving the commercial utilization rate of domestically available tallow fatty acid raw materials.

Latin America’s commercial beef cattle industry, dominated by Brazil’s herd of 220 million head, generates an estimated 1.2 million metric tons of tallow annually through its rendering and meat processing operations, providing a substantial and growing domestic raw material supply base that supports the region’s oleochemicals and tallow fatty acid manufacturing industry’s long-term competitive positioning within global specialty chemical markets.

Key Market Dynamics:

Growth Drivers: Industrial oleochemicals demand expansion and personal care ingredient innovation

The tallow fatty acid market is benefiting from a reliable and growing volume demand base from the growing and structural consumption of global industrial oleochemicals in soap and detergent production, rubber processing, metalworking lubricants and specialty chemical intermediate production, which is being boosted by the cost competitiveness of animal-derived fatty acids compared to palm and other vegetable oil-derived alternatives in a number of high-volume industrial applications. The increasing use of naturally sourced fatty acid derivatives in skincare, haircare and cosmetic formulations are expected to drive the demand for cosmetic grade tallow fatty acids with consistent quality and regulatory acceptance.

Restraints: Ethical sourcing concerns and vegetable-based substitution pressure

Increasing consumer and brand owner sensitivity to the use of animal-derived ingredients in personal care, cosmetics, food and pharmaceutical products is creating substitution pressure for tallow fatty acid-based inputs across several premium application categories, as product developers increasingly reformulate towards halal, kosher, vegan and plant-based certified alternatives that address evolving consumer values and ethical sourcing concerns without materially compromising the functional performance of end-product formulations. In Southeast Asia, growing production of palm oil and palm kernel oil-based oleochemicals is increasing competition with tallow fatty acids and pricing pressure across industrial applications, leaving little room for margin expansion for suppliers in the commodity-grade fatty acid markets.

Opportunities: Pharmaceutical grade expansion and sustainable rendering technology investment

The pharmaceutical excipient market offers a compelling commercial opportunity for tallow fatty acid producers that can meet the stringent purity, traceability and regulatory compliance standards of drug substance and drug product manufacturers worldwide, with increasing pharmaceutical production volumes, proliferating generic drug manufacturing in emerging markets and rising development of lipid-based drug delivery systems all contributing to sustained demand growth for pharmaceutical grade fatty acid inputs. Investment in advanced rendering and oleochemicals processing technologies that can both improve raw material yields, reduce processing waste, and improve the quality and consistency of tallow fatty acid output, represents a strategic pathway for producers to strengthen their competitive positioning across higher value specialty market segments.

Recent Developments:

-

2026: Wilmar International Limited expanded oleochemical fractionation and distillation capacity across Southeast Asia. The investment aims to enhance tallow fatty acid quality, diversify product offerings, and meet rising demand for specialty-grade oleochemicals.

-

2026: Croda International Plc launched a new portfolio of tallow-derived fatty acid ester actives for pharmaceutical and personal care applications. The products feature higher purity standards and regulatory support for advanced formulations.

-

2025: Darling Ingredients Inc. expanded specialty fatty acid purification capacity at its U.S. facilities. The project supports increased production of pharmaceutical and cosmetic-grade tallow fatty acids for North American customers.

-

2025: Emery Oleochemicals Group introduced new tallow-based specialty fatty acid esters under its EMEROX range. The launch targets lubricant, cosmetic, and surfactant applications with improved purity and sustainability credentials.

Key Market Players:

-

Darling Ingredients Inc.

-

Vantage Specialty Chemicals

-

Emery Oleochemicals Group

-

Wilmar International Limited

-

KLK OLEO

-

Musim Mas Holdings Pte. Ltd.

-

Kao Corporation

-

Oleon NV

-

BASF SE

-

IOI Oleochemical Industries Berhad

-

Godrej Industries Limited

-

Timur Oleochemicals Malaysia Sdn. Bhd.

-

Ecogreen Oleochemicals Pte. Ltd.

-

Twin Rivers Technologies Inc.

-

Caila & Parés S.A.

-

VVF LLC

-

Pacific Oleochemicals Sdn. Bhd.

-

P&G Chemicals

-

Croda International Plc

-

Berg + Schmidt GmbH & Co. KG

Tallow Fatty Acid Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.49 Billion |

| Market Size by 2035 | USD 5.66 Billion |

| CAGR | CAGR of 5.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Saturated Fatty Acids, Monounsaturated Fatty Acids, Polyunsaturated Fatty Acids) • By Grade (Industrial Grade, Cosmetic Grade, Pharmaceutical Grade, Food Grade) • By Application (Soaps & Detergents, Personal Care & Cosmetics, Rubber Processing, Plastics & Polymers, Food & Feed Additives, Others) • By End-Use Industry (Chemical Manufacturing,Personal Care & Cosmetics, Food & Beverage, Pharmaceuticals, Textile Industry, Agriculture & Animal Feed) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Darling Ingredients Inc., Vantage Specialty Chemicals, Emery Oleochemicals Group, Wilmar International Limited, KLK OLEO, Musim Mas Holdings Pte. Ltd., Kao Corporation, Oleon NV, BASF SE, IOI Oleochemical Industries Berhad, Godrej Industries Limited, Timur Oleochemicals Malaysia Sdn. Bhd., Ecogreen Oleochemicals Pte. Ltd., Twin Rivers Technologies Inc., Caila & Parés S.A., VVF LLC, Pacific Oleochemicals Sdn. Bhd., P&G Chemicals, Croda International Plc, Berg + Schmidt GmbH & Co. KG. |

Frequently Asked Questions

The tallow fatty acid market is expected to grow at a CAGR of 5.17% from 2026 to 2035.

The tallow fatty acid market was valued at USD 3.49 Billion in 2025.

The primary growth factors include rising demand for industrial oleochemicals, increasing innovation in personal care ingredients, and growing use of high-purity fatty acid derivatives in pharmaceutical and drug delivery applications

Cosmetic Grade is the fastest-growing grade segment in the tallow fatty acid market, with a CAGR of 5.81% from 2026 to 2035.

Asia Pacific dominated the tallow fatty acid market in 2025, holding 40.21% of global revenues.

Get in Touch