Timing Devices Market Report Scope & Overview:

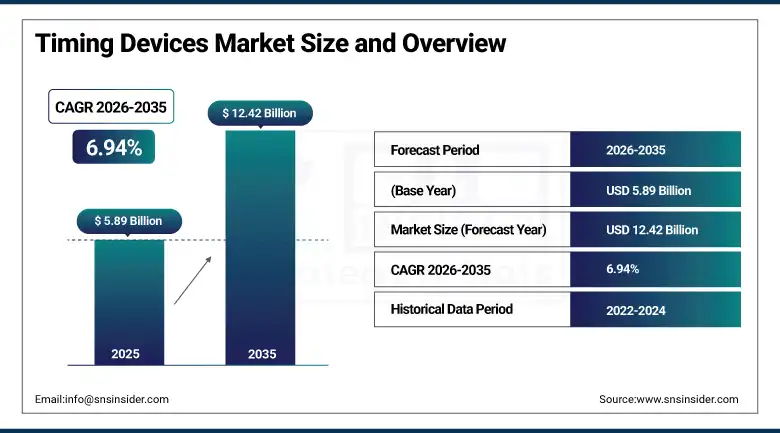

The Timing Devices Market was valued at USD 5.89 Billion in 2025 and is expected to reach USD 12.42 Billion by 2035, growing at a CAGR of 6.94% from 2026–2035.

The global timing devices market is growing at a sustained and commercially broad-based pace. The market encompasses oscillators, clock generators, clock buffers, resonators, jitter attenuators, and real-time clocks whose collective deployment spans consumer electronics, telecommunications, automotive, industrial automation, aerospace, and healthcare. The proliferation of 5G networks, autonomous vehicles, AI-enabled data centers, and IoT-connected devices is propelling demand for high-precision, low-jitter, and energy-efficient timing solutions. Innovation in MEMS-based oscillators and integrated clock system-on-chip architectures is improving performance while reducing board space requirements, creating new adoption opportunities in miniaturized and power-constrained applications.

In April 2024, SiTime Corporation launched the Chorus clock-system-on-a-chip portfolio for AI data centers, offering ten times higher performance than standalone oscillators and clocks in half the board space. The launch reflects the commercial recognition that AI infrastructure’s extraordinary precision timing requirement, whose GPU compute node synchronization demands femtosecond-level jitter performance, creates a premium timing device category whose performance specification creates commercial differentiation that conventional crystal oscillator alternatives cannot satisfy.

Market Size and Forecast

-

Market Size in 2026E: USD 6.30 Billion

-

Market Size by 2035: USD 12.42 Billion

-

CAGR: 6.94% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Timing Devices Market - Request Free Sample Report

Timing Devices Market Trends

-

MEMS oscillators grow due to superior vibration resistance, temperature range, and compact size versus quartz crystal oscillators.

-

AI data centers require ultra-low jitter timing devices enabling precise GPU cluster synchronization and high-performance computing accuracy.

-

5G networks drive demand for Precision Time Protocol compliant oscillators ensuring accurate fronthaul and backhaul synchronization.

-

Automotive ADAS and V2X systems increase need for AEC-Q100 qualified timing devices with high temperature and vibration tolerance.

-

Integrated timing ICs combine multiple functions, reducing components while improving system-level synchronization and precision efficiency.

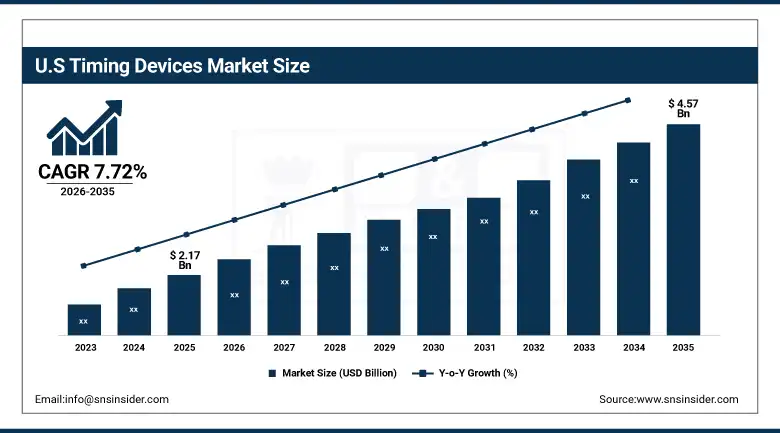

The U.S. Timing Devices Market Outlook

The U.S. Timing Devices Market was valued at approximately USD 2.17 Billion in 2025 and is expected to reach approximately USD 4.57 Billion by 2035, growing at a CAGR of approximately 7.72%.

The U.S. is the world’s most commercially significant timing devices market within North America’s dominant revenue position. SiTime Corporation, Microchip Technology, Integrated Device Technology (Renesas), Texas Instruments, and Analog Devices’ U.S. operations collectively define the North American timing device commercial and technology landscape. The extraordinary AI data center infrastructure buildout creates above-average premium timing device procurement for GPU compute node synchronization. 5G network infrastructure deployment’s backhaul timing precision requirement, the automotive ADAS adoption creating AEC-Q100 oscillator demand, and the aerospace and Defense sector’s radiation-hardened timing device procurement collectively sustain the U.S. as the highest-value per-unit timing device market globally.

Microchip Technology launched its DSC8001 series of ultra-low jitter MEMS oscillators in 2024, targeting 5G base station, optical networking, and high-speed serial link applications requiring femtosecond jitter performance in AEC-Q100 and industrial temperature-qualified packages. The product’s MEMS technology architecture delivers industry-leading jitter performance with superior vibration resistance relative to traditional quartz crystal alternatives, creating performance differentiation whose quantifiable signal integrity improvement justifies premium pricing in 5G infrastructure and precision measurement applications.

Timing Devices Market Segment Analysis

-

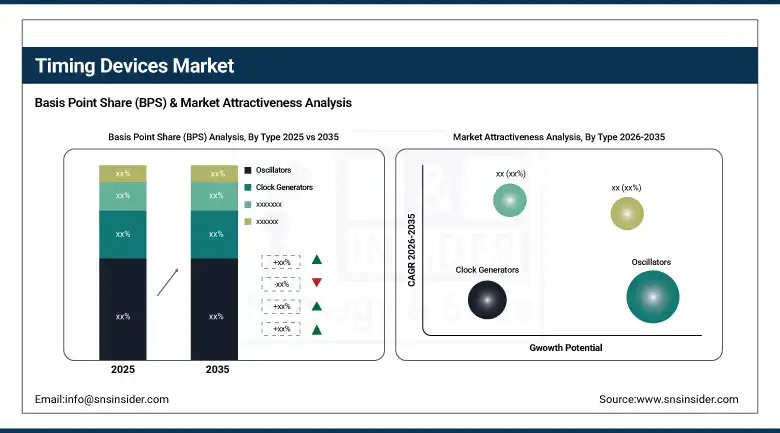

By Type, the oscillators segment dominated the market with approximately 25% share in 2025, while the clock generators segment is the fastest growing.

-

By Material, the crystal/quartz segment dominated the market with approximately 48% share in 2025, while the MEMS/silicon segment is the fastest growing.

-

By Application, the consumer electronics segment dominated the market with approximately 35% share in 2025, while the automotive segment is the fastest growing.

-

By End User, the consumer electronics segment dominated the market with approximately 32% share in 2025, while the IT & telecom segment is the fastest growing.

By Type, oscillators dominate, clock generators grow fastest

Oscillators retained the dominant type position with approximately 25% of the timing devices market in 2025. Oscillators’ commercial primacy reflects their foundational role as the primary frequency reference in every electronic system whose stable oscillation creates the fundamental timing signal from which all other clocked operations derive. Each smartphone, laptop, IoT device, and base station contains one or more oscillators whose aggregate across global electronics production creates the most commercially significant timing device type procurement volume. MEMS oscillators’ progressive adoption in performance-demanding environments where quartz’ vibration sensitivity creates system performance limitations sustains oscillator category revenue growth above the commodity quartz unit volume trajectory.

Clock generators are the fastest-growing type because AI infrastructure’s multi-GPU synchronization requirement, 5G base station’s multi-frequency clock distribution need, and high-speed computing’s processor-memory-I/O clock domain management create sophisticated clock generation and distribution requirements that standalone oscillators cannot satisfy without additional clock management circuitry. SiTime’s Chorus ClkSoC’s commercial launch demonstrates the premium market segment where integrated clock generation with femtosecond jitter performance commands above-standard pricing whose commercial value per device substantially exceeds commodity oscillator economics.

By Material, crystal dominates, MEMS grows fastest

Crystal and quartz material timing devices retained the dominant material position with approximately 48% of the timing devices market in 2025. Quartz’ piezoelectric resonance property, whose mechanical vibration at stable resonant frequency creates the electrical oscillation that timing circuits exploit, has defined electronic timing for over seven decades whose accumulated manufacturing expertise, supply chain infrastructure, and application knowledge create commercial entrenchment that alternative technologies progressively displace in performance-critical applications while volume consumer electronics applications sustain quartz’ aggregate dominance.

MEMS and silicon-based timing devices are the fastest-growing material category because silicon MEMS technology’s advantages in vibration immunity, extended temperature range, rapid startup, and smaller package size create performance advantages in demanding applications. Automotive ADAS’ vibration environment, 5G base station’s outdoor installation requiring -40°C to +85°C operation, and AI server’s femtosecond jitter requirement collectively create specification environments where MEMS timing devices’ performance advantages sustain the technology’s rapid adoption in premium market segments whose per-unit commercial value substantially exceeds commodity quartz crystal alternatives.

By End User, consumer electronics dominates, IT & Telecom grows fastest

Consumer electronics retained the dominant end-user position with approximately 32% of the timing devices market in 2025. Apple, Samsung, Xiaomi, and the global consumer electronics OEM ecosystem’s aggregate production creates the most commercially significant timing device procurement customer base by volume. Each new consumer electronics product generation’s additional timing function requirements create per-device content growth whose commercial impact compounds with production volume.

IT and Telecom is the fastest-growing end user because 5G network infrastructure’s backhaul synchronisation requirement and AI data centre’s GPU compute cluster timing precision create the most commercially premium timing device procurement of any end-user category. Each AI GPU server rack’s femtosecond jitter synchronisation requirement creates clock generator and jitter attenuator procurement whose precision specification and system-level impact create above-commodity pricing that sustains IT and Telecom’s fastest-growing commercial momentum.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Timing Devices Market Insights

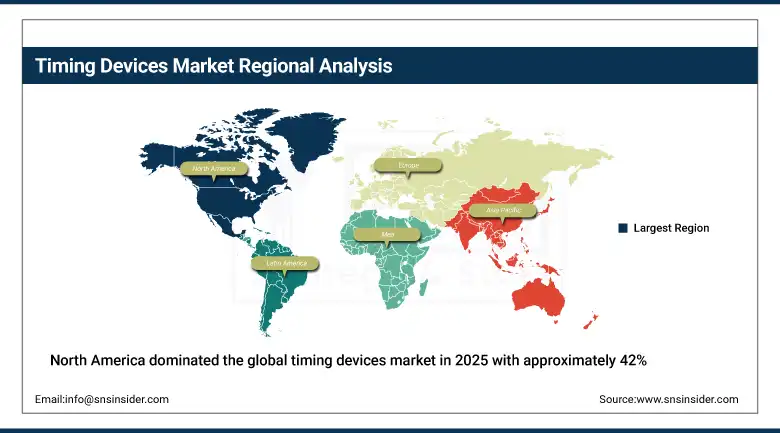

North America dominated the global timing devices market in 2025 with approximately 42% of global revenues. The United States accounts for approximately 87.4% of North American revenues through SiTime, Microchip Technology, Renesas Electronics, Texas Instruments, and Analog Devices’ commercial dominance whose combined product portfolio defines the North American timing device technology standard. The AI data center investment, 5G network infrastructure deployment, and aerospace and Defense programme’s precision timing procurement collectively sustain North America’s above-average per-unit commercial value.

Canada contributes approximately 12.6% of North American revenues through its telecommunications infrastructure investment, the growing technology sector’s computing infrastructure, and Rakon’s NewSpace timing technology development whose GNSS receiver timing products represent commercially advanced precision timing innovation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Timing Devices Market Insights

Europe is a technically sophisticated timing devices market where the automotive industry’s AEC-Q100 qualified oscillator procurement, IQD Frequency Products’ UK operations, and the telecommunications infrastructure’s precision timing investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive manufacturing sector’s timing device procurement, Infineon Technologies’ timing IC development, and the industrial automation sector’s precision timing requirement.

The United Kingdom, France, and Switzerland are significant secondary markets where aerospace and Defense timing device procurement, telecommunications infrastructure investment, and research institute precision instrumentation create consistent above-average per-unit timing device specification that sustains premium commercial relationships.

Asia Pacific Timing Devices Market Insights

Asia Pacific is the fastest-growing regional timing devices market, driven by China’s extraordinary consumer electronics and telecommunications infrastructure production, Japan’s semiconductor timing component manufacturing leadership through Seiko Epson, Murata, and Nihon Dempa Kogyo, South Korea’s Samsung and LG’s consumer electronics timing procurement, and Taiwan’s TXC Corporation’s crystal oscillator production. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world’s largest consumer electronics manufacturing location whose timing device procurement creates the most commercially significant regional volume demand globally.

India’s rapidly growing electronics manufacturing sector and the expanding 5G network deployment, combined with Southeast Asia’s consumer electronics and automotive manufacturing growth, create above-average emerging market timing device demand whose structural growth compounds with the region’s industrial development pace.

MEA & Latin America Timing Devices Market Insights

UAE leads MEA revenues at approximately 38.4% through its technology sector’s electronics infrastructure, 5G network deployment creating telecommunications timing procurement, and the growing data center sector’s precision timing investment. Brazil leads Latin American revenues at approximately 44.2% through its consumer electronics market, telecommunications infrastructure, and the growing automotive manufacturing sector’s timing device procurement.

Saudi Arabia’s Vision 2030 technology investment and South Africa’s telecommunications infrastructure create significant MEA secondary markets whose timing device procurement reflects the progressive digital infrastructure development across both national markets.

Market Dynamics

Growth Drivers: 5G infrastructure deployment and AI data center expansion creating premium precision timing demand

5G network infrastructure deployment is one of the timing devices market’s most commercially certain structural growth drivers. Each 5G base station’s fronthaul and backhaul synchronization requirement for sub-microsecond timing accuracy that IEEE 1588v2 Precision Time Protocol compliance demands creates OCXO and MEMS oscillator procurement whose per-unit commercial value substantially exceeds consumer electronics commodity oscillators. The global 5G base station installation programme, whose cumulative installations are projected to exceed 10 million units by 2030, creates aggregate premium timing device procurement whose commercial scale compounds with each successive year of network build-out investment.

AI data center infrastructure’s GPU compute cluster synchronization requirement is creating the most commercially premium new timing device application category in the market’s history. SiTime’s Chorus ClkSoC launch demonstrates the femtosecond jitter performance specification that AI training and inference clusters require, whose premium pricing reflects the system-level performance impact that timing accuracy has on GPU cluster throughput efficiency.

Restraints: MEMS oscillator adoption creating pricing pressure on established crystal oscillator suppliers and semiconductor supply chain concentration

MEMS oscillator technology’s progressive performance improvement is creating competitive pricing pressure on established crystal oscillator suppliers whose quartz-based product margins are being compressed by MEMS alternatives’ competitive total cost of ownership in performance-demanding applications. Each application segment that migrates from crystal to MEMS oscillators creates revenue pressure for traditional crystal oscillator manufacturers whose manufacturing infrastructure investment was sized for crystal technology economics. The long-term transition creates competitive dynamics that sustain innovation investment but moderate overall market ASP growth.

Semiconductor supply chain geographic concentration in Taiwan, Japan, and South Korea creates geopolitical procurement risk whose impact on timing device availability was demonstrated during COVID-19’s semiconductor shortage.

Opportunities: IoT proliferation creating volume MEMS timing demand and space and Defense precision timing premium market

IoT proliferation creating 40+ billion connected devices by 2030 represents the most commercially significant volume timing device demand expansion opportunity. Each IoT device category—from smart home sensor through industrial condition monitoring through wearable health tracker—contains timing devices whose aggregate across 40 billion units creates extraordinary volume procurement. The IoT application’s power constraint creates demand for ultra-low-power oscillators and real-time clocks whose energy efficiency innovation sustains above-commodity pricing despite the IoT market’s cost sensitivity.

Space and Defense precision timing represents the most commercially premium timing device opportunity whose radiation hardening, extreme temperature operation, and high reliability requirements create per-unit commercial value that substantially exceeds terrestrial commercial applications. Rakon’s November 2024 GNSS Receiver TIMING launch for NewSpace applications demonstrates the commercial momentum in the growing commercial space sector’s precision timing procurement whose CubeSat, LEO constellation, and satellite payload timing requirements create structured premium demand.

Recent Developments:

-

2026: Microchip Technology advanced automotive-grade oscillators meeting AEC-Q100 standards for ADAS, EV, and V2X communication timing accuracy requirements.

-

2025: Texas Instruments enhanced clock generator ICs supporting 5G infrastructure timing synchronization and IEEE 1588 Precision Time Protocol applications.

-

2025: SiTime expanded MEMS timing portfolio for AI data centers, improving ultra-low jitter performance for high-performance computing synchronization systems.

Timing Devices Market key players are:

-

SiTime Corporation

-

Microchip Technology Inc.

-

Qorvo Inc.

-

Texas Instruments Inc.

-

Analog Devices Inc.

-

Seiko Epson Corporation

-

TXC Corporation

-

Murata Manufacturing Co., Ltd.

-

Kyocera Corporation

-

IQD Frequency Products Ltd.

-

Nihon Dempa Kogyo Co., Ltd. (NDK)

-

Rakon Limited

-

Abracon LLC

-

Bliley Technologies Inc.

-

CTS Corporation

-

Crystek Corporation

-

Silicon Laboratories Inc.

-

NXP Semiconductors

-

Infineon Technologies AG

-

Daishinku Corporation

Timing Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.89 Billion |

| Market Size by 2035 | USD 12.42 Billion |

| CAGR | CAGR of 6.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Oscillators, Clock Generators, Clock Buffers, Resonators, Jitter Attenuators, Real-Time Clocks) • By Material (Crystal/Quartz, MEMS/Silicon, Ceramic) • By Application (Consumer Electronics, Telecommunications, Automotive, Industrial Automation, Aerospace & Defense, Medical & Healthcare, Computing & Data Centers) • By End User (Consumer Electronics, IT & Telecom, Automotive, Industrial, Aerospace & Defense, Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SiTime Corporation, Microchip Technology Inc., Qorvo Inc., Texas Instruments Inc., Analog Devices Inc., Seiko Epson Corporation, TXC Corporation, Murata Manufacturing Co., Ltd., Kyocera Corporation, IQD Frequency Products Ltd., Nihon Dempa Kogyo Co., Ltd. (NDK), Rakon Limited, Abracon LLC, Bliley Technologies Inc., CTS Corporation, Crystek Corporation, Silicon Laboratories Inc., NXP Semiconductors, Infineon Technologies AG, Daishinku Corporation |

Frequently Asked Questions

The Timing Devices Market is expected to grow at a CAGR of 6.94% from 2026 to 2035.

The Timing Devices Market was valued at USD 5.89 Billion in 2025.

5G network infrastructure deployment creating above-average premium timing device procurement for base station synchronization.

Oscillators dominated the Timing Devices Market with approximately 25% share in 2025, while the Clock Generators segment is the fastest growing.

North America dominated the Timing Devices Market with approximately 42% of global revenues in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch