Ultra-Low Temperature Freezers Market Report Scope & Overview:

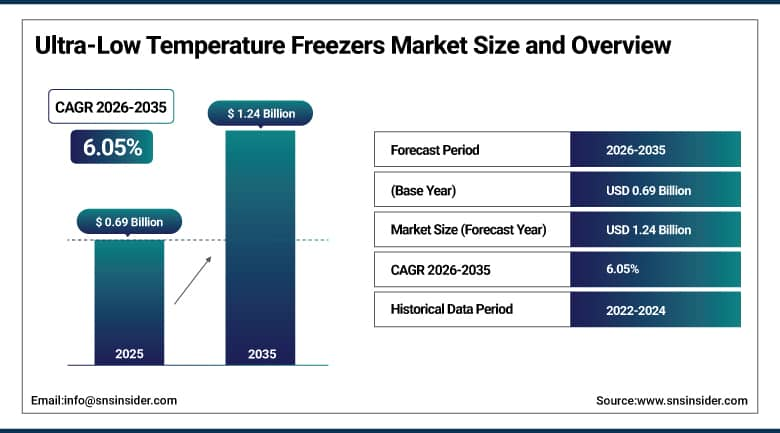

The Ultra-Low Temperature (ULT) Freezers Market was valued at USD 0.69 billion in 2025 and is expected to reach USD 1.24 billion by 2035, growing at a CAGR of 6.05% from 2026–2035.

Ultra-Low Temperature Freezers work in an environment that is between -40°C and -86°C. These machines are necessary in preserving samples of biological nature, vaccines, and medicinal substances. Materials that need to be preserved include DNA, RNA, stem cells, plasma, enzymes, and mRNA vaccine samples. The number of biobanks worldwide is increasing annually by more than 8%. This trend has resulted in increased demand for ultra-low temperature freezers. Since the outbreak of the novel Coronavirus, there has been heightened concern about the need for such storage facilities. The COVID-19 mRNA vaccines must be preserved from -70°C to -80°C throughout their production and even delivery. Research in personalized medicine and genomics is creating huge volumes of samples that need preservation.

The global biobank count is increasing by over 8% annually. This growth is directly driving demand for ultra-low temperature storage infrastructure that maintains sample integrity at temperatures as low as -86°C.

Market Size and Forecast

- Market Size in 2026E: USD 0.73 Billion

- Market Size by 2035: USD 1.24 Billion

- CAGR: 6.05% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Ultra-Low Temperature Freezers Market - Request Free Sample Report

Ultra-Low Temperature Freezers Market Trends

- Energy-efficient natural refrigerant ULT freezers are replacing older HFC cascade systems. Hydrocarbon-based refrigerants reduce energy consumption by 20 to 40% versus conventional cascade technology.

- Automated sample management systems are becoming standard in high-throughput biobank environments. AI-driven inventory tracking and retrieval automation reduce sample handling errors and storage loss.

- Freezer-as-a-service models are enabling capital-light access to ULT storage capacity. Subscription-based contracts allow smaller institutions to scale storage without large upfront equipment investment.

- IoT connectivity and remote monitoring are transforming ULT freezer fleet management. Real-time temperature alarms, performance dashboards, and predictive maintenance reduce sample loss risk significantly.

- mRNA platform expansion is driving sustained demand for -80°C storage infrastructure globally. Personalized vaccine and cell therapy pipelines require growing ULT storage capacity at every supply chain stage.

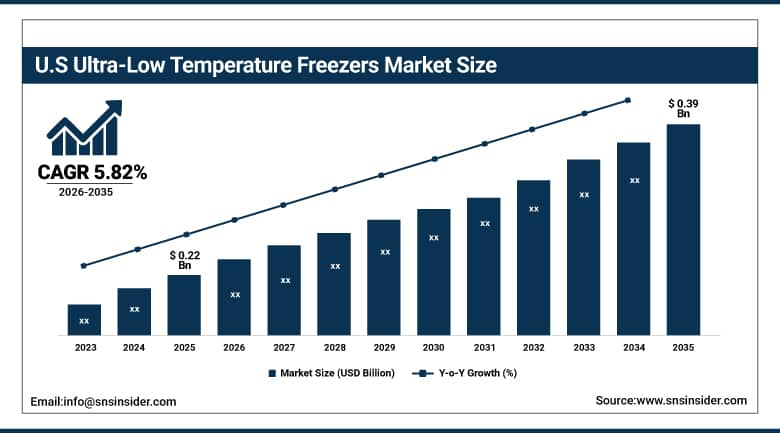

The U.S. Ultra-Low Temperature Freezers Market Outlook

The U.S. Ultra-Low Temperature Freezers Market was valued at approximately USD 0.22 billion in 2025 and is expected to reach approximately USD 0.39 billion by 2035, growing at a CAGR of 5.82%.

The United States holds the position of the world's leading national ULT freezer market by revenue. This is due to the presence of the largest number of R&D centers in this area in the country. Over USD 200 billion are invested in biomedical research involving cold storage each year by the National Institutes of Health (NIH) and private companies. The United States owns the largest system of academic biobanks, which store specimens related to genomics and clinics. The logistics associated with the COVID-19 vaccine delivery have contributed to the implementation of large-scale -80°C ULT storage in the United States. Cold storage regulations issued by the Food and Drug Administration (FDA) include strict temperature conditions for pharmaceuticals. ENERGY STAR Version 2.0 standards promote the implementation of efficient ULT freezers. Such renowned manufacturers as Thermo Fisher Scientific, Eppendorf, and Helmer Scientific have large shares in the US market. The development of cell and gene therapy research leads to an increase in demand for ULT freezers.

ENERGY STAR Version 2.0 ULT freezer standards that came into effect in 2023 are obligatory for the federally funded institutes in the United States.

Ultra-Low Temperature Freezers Market Segment Analysis

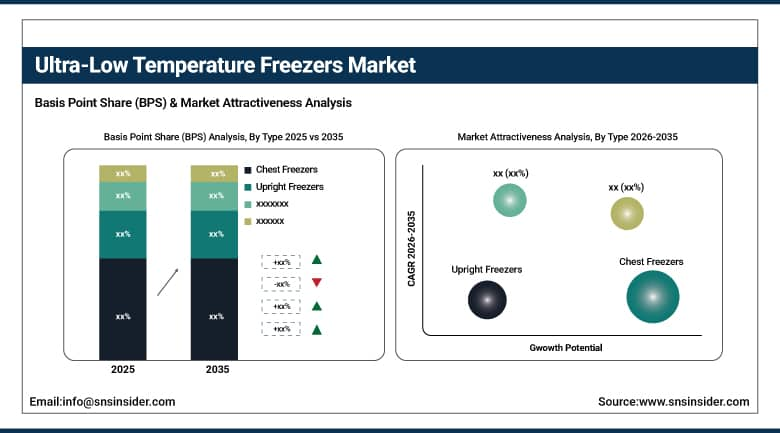

- By Type, chest freezers led the market with a share of 55.04% in 2025 through superior temperature uniformity and energy efficiency for long-term biobank storage. Upright freezers are the fastest-growing at a CAGR of 6.80% through space optimization and ease of sample access in high-throughput laboratory environments.

- By Technology, automated systems led with 60.24% share in 2025 through precise temperature control, barcode-integrated sample tracking, and remote monitoring capabilities. Semi-automated systems are growing through their cost-accessibility for medium-scale laboratory and hospital deployments.

- By Capacity, 501–700 litres dominated in 2025 as the most versatile range for pharmaceutical and biobank applications balancing capacity and footprint. Below 300 litres is growing through demand from smaller research laboratories and clinical sites requiring compact ULT solutions.

- By End-User, Pharmaceutical & Biotechnology companies dominated through master cell bank, stability testing, and biologic sample archiving requirements; Biobanks are the fastest-growing end-user through rapidly expanding national and institutional specimen collection programmes globally.

By Type, chest freezers dominate, upright freezers are expected to grow fastest

The dominant position was maintained by the chest freezers segment with approximately 55.04% revenue share of the ULT freezers market in 2025. The ability of the chest freezer to maintain naturally cold air due to the settling down of cold air to the bottom on the opening of the door makes them more energy efficient and more capable of maintaining uniform temperatures compared to the upright freezer. Genomic population and clinical specimen studies require highly accurate and uniform temperature control that can be provided only by the chest freezer segment. This is because of the higher density of samples they provide based on the floor space available in the freezer room.

Upright Freezers emerge as the most rapidly growing category, with a Compound Annual Growth Rate (CAGR) of 6.80% up to 2033. The upright design, which comes with vertical shelving, facilitates quick access and retrieval of samples without moving around heavy containers required when accessing samples using the chest freezer design. Sample management processes in high-throughput laboratories for pharmaceutical quality control, drug discovery, and clinical trials are designed with the upright design in mind because of its convenience from the aspect of ergonomics and speed. In the case of the modern upright ultra-low temperature (ULT) freezers, multiple zone temperature control systems, cascaded, or natural refrigeration systems and magnetic door seals have narrowed the efficiency gap compared to their counterparts in the chest freezer category.

By End-User, pharmaceutical & biotechnology dominates, biobanks are expected to grow fastest

Pharmaceutical and Biotechnology companies retained the dominant end-user position with approximately 44.23% of revenues in 2025. The pharmaceutical sector's regulatory obligation to store reference and retention samples at validated temperatures throughout drug development and post-approval stability monitoring programmes creates inelastic ULT freezer demand that is minimally sensitive to economic cycles. Master cell bank storage for biologic drug manufacture, where the working cell bank and master cell bank are stored at separate ULT freezer locations as redundancy against catastrophic storage failure, creates baseline ULT demand at every biologic manufacturing facility globally. The explosive growth of mRNA therapeutics, cell therapy, and gene editing pipeline compounds whose molecular stability requires continuous -70°C to -80°C storage is further expanding pharmaceutical sector ULT capacity requirements above historical rates.

Biobanks are the fastest-growing end-user through their rapidly expanding national and institutional specimen collection programmes. National biobanks including the UK Biobank, Estonian Biobank, and NIH All of Us Research Programme are systematically collecting and storing millions of biological specimens from population cohorts whose genomic and phenotypic data will support decades of precision medicine research. Each new biobank participant represents years of longitudinal specimen storage at ULT temperatures across blood, DNA, and tissue sample types. The proliferation of disease-specific biobanks for cancer, cardiovascular, neurological, and autoimmune conditions is creating additional institutional ULT storage demand beyond national population biobank programmes.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.3% |

|

Europe |

Germany |

24.7% |

|

Asia Pacific |

China |

42.6% |

|

Middle East & Africa |

UAE |

27.3% |

|

Latin America |

Brazil |

43.8% |

North America Ultra-Low Temperature Freezers Market Insights

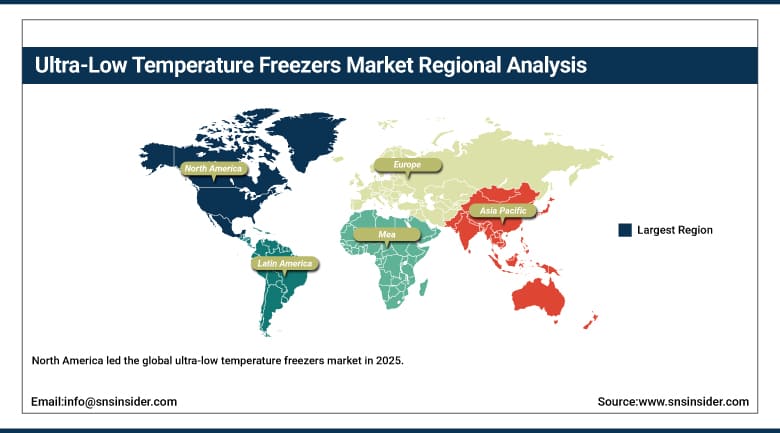

North America led the global ultra-low temperature freezers market in 2025. The U.S. accounts for approximately 85.3% of North American revenues. The region benefits from the world's highest concentration of pharmaceutical, biotechnology, and academic research facilities. Federal research funding through NIH, BARDA, and DoD creates consistent institutional ULT procurement demand. COVID-19 vaccine infrastructure investment permanently expanded the country's -80°C cold chain network. ENERGY STAR regulatory standards are systematically driving the replacement cycle toward energy-efficient modern units. The U.S. cell and gene therapy clinical pipeline is one of the fastest-growing sources of new ULT storage demand globally. Canada contributes through its strong academic biomedical research sector and expanding national biobank programmes.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Ultra-Low Temperature Freezers Market Insights

Europe is a technically advanced ULT freezers market with strong institutional and regulatory demand drivers. Germany accounts for approximately 24.7% of European revenues through its large pharmaceutical manufacturing and academic research base. The EU's Horizon Europe research funding programme sustains institutional biobank and genomic research specimen storage investment. UK Biobank's scale, now exceeding 500,000 participants, requires ongoing ULT capacity expansion as longitudinal collection continues. Nordic countries demonstrate above-average ULT adoption through their population biobank programmes and pharmaceutical R&D concentration. EU F-gas regulations restricting HFC refrigerant use are accelerating the transition to natural refrigerant ULT systems across the European market.

Asia Pacific Ultra-Low Temperature Freezers Market Insights

Asia Pacific is the fastest-growing ULT freezers market globally. China accounts for approximately 42.6% of Asia Pacific revenues through its rapidly expanding pharmaceutical manufacturing and biomedical research infrastructure. Chinese government investment in precision medicine and genomic research is creating large and growing biobank storage requirements. India's pharmaceutical manufacturing growth and expanding clinical research sector are driving ULT adoption in research and quality control applications. Japan and South Korea maintain sophisticated domestic pharmaceutical and biotechnology research sectors with consistent ULT storage requirements. The region's combination of growing R&D investment and expanding health infrastructure will sustain above-average market growth throughout the forecast period.

MEA & Latin America Ultra-Low Temperature Freezers Market Insights

The Middle East and Africa and Latin America are growing ULT freezers markets. UAE leads MEA revenues at approximately 27.3% through its world-class hospital infrastructure and growing pharmaceutical manufacturing ambitions. Saudi Arabia's Vision 2030 healthcare investment programme is expanding clinical research and biobank infrastructure requiring ULT storage. Brazil leads Latin American revenues at approximately 43.8% through its large university hospital research network and pharmaceutical manufacturing sector. Growing clinical trial activity in Latin America is creating new investigational site ULT storage demand. National vaccination programme storage requirements across both regions are sustaining demand for -70°C to -80°C cold chain equipment.

Market Dynamics

Growth Drivers: Expanding biobanks, growing mRNA platform investment, and rising pharmaceutical R&D are driving the ultra-low temperature freezers market growth globally.

Global biobank expansion at over 8% annually is the most structurally consistent ULT freezer demand driver. Each new biobank participant contributes years of longitudinal specimen storage requirements at ULT temperatures. The mRNA therapeutics and vaccine platform revolution has created a permanent step-change in -80°C cold chain infrastructure investment. Cell therapy and gene editing clinical pipelines require ULT storage at every stage from development through commercial manufacturing. Rising global pharmaceutical R&D expenditure, exceeding USD 250 billion annually, sustains continuous ULT procurement by drug developers and contract research organizations. COVID-19 permanently elevated institutional awareness of cold chain infrastructure vulnerability and investment priority. Government-funded genomic research programmes across the U.S., UK, China, and India are systematically expanding national biobank storage requirements.

Restraints: High equipment cost, significant energy consumption, and technical maintenance requirements are restraining ultra-low temperature freezers market adoption among smaller institutions.

Premium ULT freezers represent a significant capital expenditure for smaller research institutions and clinical sites. Operating energy costs at -80°C are substantially higher than conventional laboratory refrigeration, adding to total cost of ownership. Technical maintenance requirements for cascade refrigeration systems demand specialized engineering expertise. Unexpected temperature excursions can cause catastrophic irreplaceable sample loss, creating operational risk anxiety. Supply chain constraints for precision refrigeration components have periodically extended equipment lead times. Regulatory validation requirements for pharmaceutical ULT installations add significant time and cost to new unit deployment. Natural refrigerant conversion requires staff safety training and building code compliance investment that can delay transitions.

Opportunities: mRNA vaccine pipeline growth, cell therapy expansion, and natural refrigerant innovation create substantial ultra-low temperature freezers market opportunities globally.

The global mRNA therapeutics pipeline, with hundreds of clinical-stage programmes in cancer, infectious disease, and rare genetic conditions, represents the most commercially significant new ULT demand source of the current decade. Cell and gene therapy commercialization at scale requires ULT cold chain infrastructure across manufacturing, distribution, and hospital administration sites. Natural refrigerant ULT systems offer manufacturers premium differentiation through energy efficiency and environmental credentials that align with institutional sustainability commitments. Emerging market biobank development in China, India, and Brazil creates new geographic expansion opportunities for established Western ULT manufacturers. Freezer-as-a-service models unlock the smaller institution market segment previously constrained by capital budget limitations.

Recent Developments:

- 2025: Thermo Fisher Scientific launched its next-generation TSX Series ULT freezers with 35% improved energy efficiency and integrated IoT sample monitoring. The system provides real-time temperature mapping and remote alert capabilities for laboratory managers.

- 2025: Eppendorf expanded its CryoCube F570h ULT freezer range with new natural refrigerant variants meeting EU F-gas regulations. The HC-based refrigerant system achieves Class A energy performance under the EU Ecodesign framework.

- 2025: Haier Biomedical launched an AI-powered ULT freezer management platform integrating predictive maintenance alerts with laboratory information management systems. The platform serves its growing installed base across Asia Pacific research institutions.

Ultra-Low Temperature Freezers Market Key Players are:

- Thermo Fisher Scientific Inc.

- Eppendorf SE

- Haier Biomedical

- PHC Holdings Corporation

- Helmer Scientific

- Stirling Ultracold (Global Cooling Inc.)

- Arctiko A/S

- Bionics Scientific Technologies (P) Ltd.

- BINDER GmbH

- Esco Micro Pte. Ltd.

- Azbil Corporation

- Evermed S.r.l.

- Avantor Inc. (VWR International)

- Labcold Ltd.

- Vestfrost Solutions A/S

- LabRepCo LLC

- CryoScientific Inc.

- So-Low Environmental Equipment Co.

- Continental Scientific

- Nor-Lake Inc.

Ultra-Low Temperature Freezers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.69 Billion |

| Market Size by 2035 | USD 1.24 Billion |

| CAGR | CAGR of 6.05% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Chest Freezers, Upright Freezers) •By Technology (Automated, Semi-Automated) •By Capacity (Below 300 L, 300–500 L, 501–700 L, Above 700 L) •By End-User (Pharmaceutical & Biotechnology, Academic & Research Laboratories, Hospitals & Blood Centers, Biobanks, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Eppendorf SE, Haier Biomedical, PHC Holdings Corporation, Helmer Scientific, Stirling Ultracold (Global Cooling Inc.), Arctiko A/S, Bionics Scientific Technologies (P) Ltd., BINDER GmbH, Esco Micro Pte. Ltd., Azbil Corporation, Evermed S.r.l., Avantor Inc. (VWR International), Labcold Ltd., Vestfrost Solutions A/S, LabRepCo LLC, CryoScientific Inc., So-Low Environmental Equipment Co., Continental Scientific, Nor-Lake Inc. |

Frequently Asked Questions

Get in Touch