Underwater Robotics Market Report Scope & Overview:

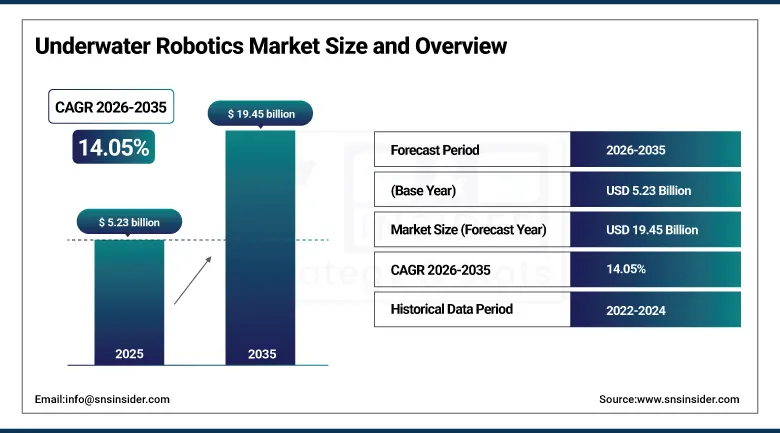

The Underwater Robotics Market size was valued at USD 5.23 billion in 2025 and is expected to reach USD 19.45 billion by 2035, growing at a CAGR of 14.05% from 2026-2035.

The Underwater Robotics Market is booming with growth because of high utilization of underwater robotics in offshore oil and gas exploration, maritime defense, scientific research and recently started utilizing renewable energy sectors. Robotic vehicles, especially Remotely Operated Vehicles (ROVs) and Autonomous Underwater Vehicles (AUVs) have become invaluable for performing complex tasks at great ocean depths with high accuracy and low risk to human lives. Rapidly developing artificial intelligence, machine learning, and real-time data analytics capabilities are revolutionizing the operational capabilities of underwater robotic systems, allowing longer autonomous mission durations and improved navigation around dynamic seabed terrains.

Furthermore, the growing importance of government-backed scientific programs to both stimulate the incorporation of AUVs into scientific studies and subsequently help refine the technology is strongly highlighted here, with developments in AI-enabled autonomous underwater vehicles focused on marine conservation to survey species distributions and their ecosystem dynamics being funded by the U.S. National Science Foundation (NSF).

In addition, increasing offshore energy leasing activity by the U.S. Bureau of Ocean Energy Management (BOEM) has further fuelled demand for ROV–based inspection, maintenance, and repair services at deep-water installations. BOEM's offshore wind leasing program across massive ocean areas of the U.S. outer continental shelf is creating a new, long-term need for underwater robotic support services for renewable energy infrastructure management.

Market Size and Forecast:

-

Market Size in 2025: USD 5.23 Billion

-

Market Size by 2035: USD 19.45 Billion

-

CAGR: 14.05% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Underwater Robotics Market - Request Free Sample Report

Underwater Robotics Market Trends:

-

Growing deployment of AI-powered AUVs for long-duration autonomous ocean monitoring, scientific research, and environmental data collection is reshaping industry capabilities.

-

Rising offshore wind energy infrastructure development globally is creating sustained demand for ROV-based subsea inspection, installation, and maintenance services.

-

Integration of advanced sonar, LiDAR, and high-definition imaging technologies in underwater robots is significantly improving seabed mapping precision and operational efficiency.

-

Increasing defense and naval investment in autonomous underwater systems for mine detection, surveillance, and anti-submarine warfare is driving specialized AUV development.

-

Adoption of swarm robotics and multi-vehicle coordination systems is enabling more complex and comprehensive underwater survey and monitoring operations.

-

Development of energy-harvesting underwater vehicles that leverage ocean currents and wave energy is extending operational endurance for remote mission profiles.

U.S. Underwater Robotics Market Size Outlook:

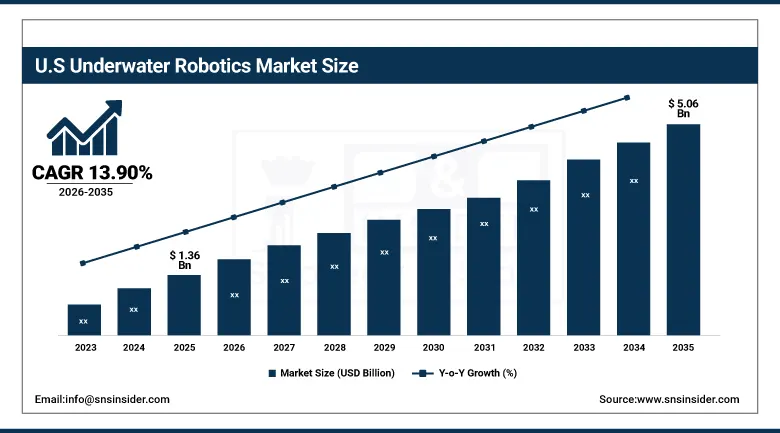

The U.S. Underwater Robotics Market was valued at USD 1.36 billion in 2025 and is expected to reach USD 5.06 billion by 2035, growing at a CAGR of 13.90% from 2026-2035. The U.S. Underwater Robotics Industry is supported just as much by large federal funding into national security and naval defense systems, offshore energy infrastructure and services, and oceanographic research. The domestic demand base remains strong in the U.S. with the U.S. Navy making continued purchases of advanced underwater unmanned vehicles for mine countermeasures, intelligence gathering, and undersea domain awareness programs.

Supporting this, the U.S. Navy's Unmanned Maritime Systems program has made large-displacement unmanned undersea vehicles (LDUUVs) with long-range autonomy a priority for development and acquisition, suggesting continued defense-sector interest in sophisticated autonomous undersea vehicle technology. Since becoming a strategic priority of the U.S. Department of Defense (DoD), funding for undersea warfare capabilities providing a direct line of support to underwater robotics technology development and domestic industry growth has steadily increased.

Underwater Robotics Market Segment Highlights:

-

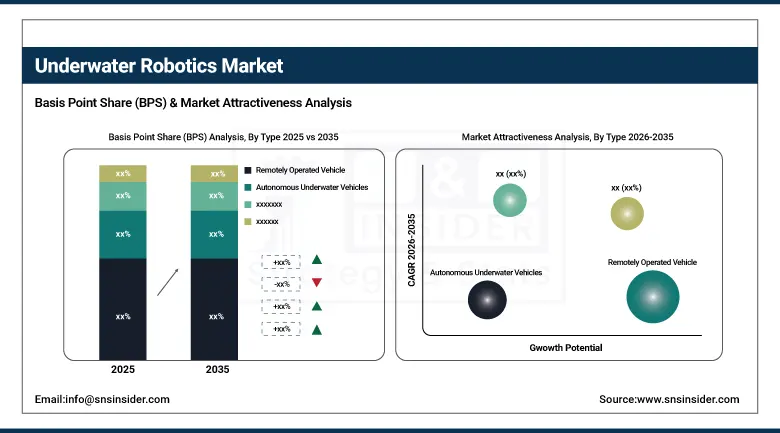

By Type, ROV segment dominated with 79% share in 2025; AUV segment expected to grow fastest (CAGR 17.82% through 2035).

-

By Application, Commercial Exploration dominated with 42% share in 2025; Scientific Research segment expected to grow fastest (CAGR 16.07%).

By Type, ROV segment dominates the Underwater Robotics Market, AUV segment expected to grow fastest

The Underwater Robotics Market was dominated by the Remotely Operated Vehicle (ROV) segment, capturing around 79% share in the year 2025. ROVs are still the mainstay of the subsea industry, providing an essential real-time visual inspection, manipulation and intervention tool for offshore oil and gas, subsea cable maintenance and marine construction projects. They are the natural choice for complex, high-risk intervention activities at depth due to a combination of their ability to carry a range of specialist tooling and operate continuously under direct human control. ROV operators in turn have the most entrenched market position globally across the commercial offshore and defence sectors due coming with an established industry infrastructure of vessels, training programs, and support vessels.

the Autonomous Underwater Vehicle (AUV) segment is anticipated to account for the fastest CAGR of around 17.82% over the forecast period. AUVs are becoming more favoured in applications where long endurance and operational independence from surface support vessels are vital, thus they are being used as a popular platform for large-scale survey missions, environmental monitoring, scientific data collection, and military reconnaissance applications. AUV operational range and mission complexity is rapidly being extended through advances in battery technology, AI-based navigation, and acoustic communication systems. The falling costs of units together with increasing commercial applications (e.g., offshore wind surveying, pipeline inspection, seabed mapping) are driving AUV adoption to an ever-more diverse variety of industry sectors and geographic markets.

By Application, Commercial Exploration segment dominates the Underwater Robotics Market, Scientific Research segment expected to grow fastest

In 2025, the Commercial Exploration application segment accounted for the largest share of about 42% due to continuous offshore oil and gas exploration activity, feasibility study into deep-sea mining, as well as renewable energy infrastructure development. Unmanned underwater vehicles have arisen as key methods for completing Inspection, maintenance and repair activities at depths that prohibit human dive access in an economical and effective manner. The segment's supremacy signifies the paramount operating dependence of offshore energy industries globally on ROV and AUV functionalities for routine maintenance as well as emergency intervention operations.

The Scientific Research segment is anticipated to grow at the fastest CAGR during the forecast periodThe post Global Ocean Research Market Insights, Outlook, and Revenue, Forecast to 2035 appeared first on Research Nester. AUVs are now being used by scientific institutions to collect high-resolution data on ocean chemistry, temperature, biodiversity and seafloor geology in remote ocean environments. Some of the growth drivers for these robots are complex international cooperation at large scale ocean science programs and the deep-sea research initiatives increases which are now being conducted due to regulatory agencies such as NOAA, the European Marine Observation and Data Network (EMODnet), and respective organizations in Asia Pacific.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

82% |

|

Europe |

Norway |

30% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

55% |

Europe Underwater Robotics Market Insights

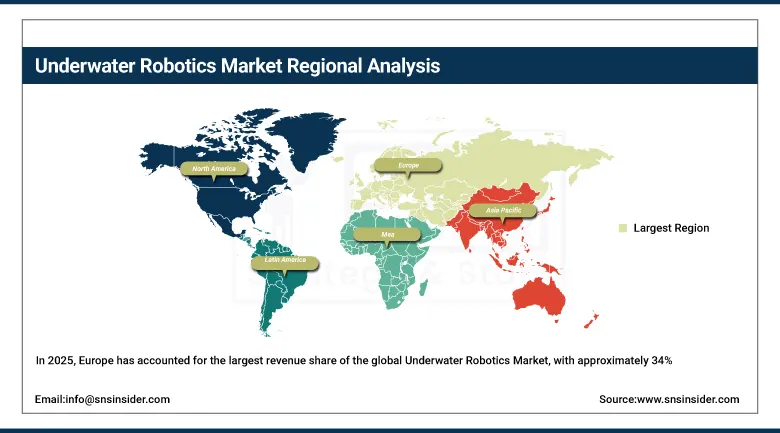

In 2025, Europe has accounted for the largest revenue share of the global Underwater Robotics Market, with approximately 34%, owing to a strong offshore oil and gas in the North Sea, booming maritime defense capabilities coupled with the growing offshore wind energy sector in the region. The deep-water robotics markets of Norway, the United Kingdom, France, Germany, and the Netherlands embody the core of underwater robotics adoption in Europe A mature ROV services industry in Norway is maintained with a large backlog of deepwater petroleum production infrastructure, whilst increasing offshore wind capacity in the UK is offering high demand for new long-term AUV survey and inspection contracts.

In support of this position, the European Commission states in its Strategic Plan for the Blue Economy that investment in maritime technology, especially underwater robotics, is a significant growth area that will enable sustainable management of ocean resources, subsea energy production, and marine environmental monitoring across EU member states.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Underwater Robotics Market Insights

North America is a key market within the Underwater Robotics Market, fueled by the competing front of commercial offshore energy activity in the Gulf of Mexico and large U.S. federal defense and oceanographic research investment. The area already has a developed subsea services sector, an active technology development environment, and existing local ROV operator networks that support deepwater production. Canada's already growing offshore energy sector and expanding Arctic research programs are examples of more gradual regional growth.

Asia Pacific Underwater Robotics Market Insights

The Asia Pacific region is forecast to achieve the highest CAGR of approximately 17.03% during 2026-2035, driven by rapidly expanding offshore energy development, rising defense investment in undersea capabilities, and growing oceanographic research programs. China, Japan, South Korea, India and Australia are the main growth markets. China The aggressive ramp-up of deep-sea research capabilities, including state-funded development of advanced AUVs for ocean exploration and resource assessment, positions China as the most important growth driver in the regional market.

Chinese Ministry of Natural Resources recently introduced targeted plans to develop deep-sea exploration technologies, with ocean depth autonomous underwater vehicles (AUV) placed optimally at the intersection of domestic ability and exportal work abroad as they directly facilitate support with massive and/or niche manufacturing capacity development and the broader scaling of underwater robotic-related applications in scientific and strategic efforts.

Middle East & Africa and Latin America Underwater Robotics Market Insights:

The increasing interest in marine resource management. This is followed by Brazil (dominates Latin American adoption) with Petrobras's extensive deep-water pre-salt exploration and production operations requiring sophisticated ROV capabilities. Offshore energy activities and national maritime defense modernization programs are driving MEA regional growth markets in the UAE and Saudi Arabia.

Underwater Robotics Market Growth Drivers:

-

Expanding offshore oil, gas, and renewable energy infrastructure creating sustained demand for ROV and AUV inspection, maintenance, and survey operations globally

The ongoing expansion in deepwater and ultra-deepwater energy production infrastructure, as well as the global build-out of offshore wind energy installations, creates structurally growing demand for underwater robotic services. With ageing offshore assets, and as regulatory requirements tighten regarding inspections frequency, the ROV service hour requirements over key offshore energy producing regions are set to rise. At the same time, the proliferation of offshore wind development across Europe, the U.S., and Asia Pacific is opening up a nascent and soon to be sizable market for AUV-based cable route surveys, foundation inspections and environmental monitoring programs— all of which require high-endurance robotic platforms at a price point within budget.

Offshore wind capacity additions are accelerating around the world as clean energy transition commitments gather pace, and the International Energy Agency (IEA) shows offshore wind as one of the largest sources of power generation by 2040 directly driving long-term demand for underwater robotic support services in installation, maintenance and inspection applications.

Underwater Robotics Market Restraints:

-

High maintenance and operational costs in extreme underwater environments limiting adoption among cost-constrained operators and emerging market industries

The environment and harsh conditions to which underwater robots are subjected impose high operational and maintenance cost burdens on the end users, constraining the growth of market as a whole, especially for smaller operators and industries which are within cost-sensitive markets. Robotic systems driven deep-ocean are subjected to high-wear rates from pressures and corrosive environments as well as biofouling and mechanical stresses arising from repeated deployments, requiring high-maintenance cycles and carbon component replacements. The recovery and repair of out of service systems in deep waters often necessitates the use of costly specialist vessels and extended shutdown periods, which has the potential to accrues significant costs to a project, reducing its overall commercial viability, and discouraging take-up amongst less capital-strong Operators.

Underwater Robotics Market Opportunities:

-

Rapid advancement of AI-enabled autonomous systems and expanding deep-sea research programs creating significant new growth avenues for underwater robotics across scientific, commercial, and defense applications

The combination of AI, advanced sensor technologies and energy systems is radically widening the operational scope and economic feasibility of autonomous underwater vehicles for an expanding number of applications. External image / image: Adaptive gateway AI-enabled adaptive navigation, real-time anomaly seafloor activity detection, and multi-vehicle coordination are enabling AUVs to conduct complex, long-duration missions with minimal surface support and fundamentally changing the economics of large-scale ocean data collection. With increasing government investment in ocean research infrastructure, growing commercial interest in the assessment of deep-sea mineral resources, and rising defense interest in autonomous undersea systems, there is a healthy and diversified demand environment that will continue to sustain market growth through 2035.

Recent Developments:

-

2025: Komatsu unveiled an autonomous underwater robot for construction tasks at CES 2025, designed to perform complex structural operations in deep underwater environments, reflecting the expanding application scope of underwater robotics beyond traditional oil and gas and defence markets.

-

2024: Beam introduced the first AI-powered autonomous underwater vehicle specifically designed for offshore wind farm inspection in September 2024, improving operational efficiency and significantly reducing inspection costs compared to conventional ROV-based methods.

-

2024: SLB, Subsea7, and C-Power formed a strategic partnership to explore ocean energy powering of subsea operations, testing C-Power's SeaRAY autonomous offshore power system at the PacWave South site enabling persistent, low-carbon powered underwater robotic deployments.

-

2024: NSF-funded researchers developed advanced AI-driven AUVs for marine conservation, capable of autonomously mapping species distribution and ecosystem dynamics across large marine areas, demonstrating the expanding scientific application of underwater robotic platforms.

-

2023: Oceaneering International expanded its fleet of electric work-class ROVs, investing in next-generation e-ROV technology designed to deliver reduced environmental impact, lower operational costs, and improved performance in deep-water offshore energy applications.

-

2022: Kongsberg Maritime advanced its HUGIN Superior AUV platform with enhanced endurance and payload capacity, targeting deepwater survey, seabed mapping, and environmental monitoring applications across global offshore energy and scientific research markets.

Underwater Robotics Companies are:

-

Saab AB

-

TechnipFMC plc

-

Kongsberg Maritime

-

Teledyne Marine

-

General Dynamics Mission Systems, Inc.

-

ECA GROUP

-

Atlas Elektronik GmbH

-

Hydroid, Inc. (Kongsberg)

-

Soil Machine Dynamics Ltd.

-

Forum Energy Technologies, Inc.

-

VideoRay LLC

-

Subsea 7 S.A.

-

DOF Subsea AS

-

International Submarine Engineering Limited

-

Deep Ocean Engineering, Inc.

-

ATLAS MARIDAN Aps

-

Perry Slingsby Systems

-

Eddyfi Technologies

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.23 Billion |

| Market Size by 2035 | USD 19.45 Billion |

| CAGR | CAGR of 14.05% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Remotely Operated Vehicle (ROV), Autonomous Underwater Vehicles (AUV)) • By Application (Defense & Security, Commercial Exploration, Scientific Research, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Oceaneering International, Inc.; Saab AB; TechnipFMC plc; Kongsberg Maritime; Teledyne Marine; Fugro N.V.; General Dynamics Mission Systems, Inc.; ECA GROUP; Atlas Elektronik GmbH; Hydroid, Inc. (Kongsberg); Soil Machine Dynamics Ltd.; Forum Energy Technologies, Inc.; VideoRay LLC; Subsea 7 S.A.; DOF Subsea AS; International Submarine Engineering Limited; Deep Ocean Engineering, Inc.; ATLAS MARIDAN Aps; Perry Slingsby Systems; Eddyfi Technologies. |

Frequently Asked Questions

Ans: Asia Pacific is the fastest-growing region in the Underwater Robotics Market.

Ans: North America dominated the Underwater Robotics Market in 2025.

Ans: The ROV segment dominated the Underwater Robotics Market with approximately 79% share in 2025.

Ans: The Underwater Robotics Market was valued at USD 5.23 billion in 2025.

Ans: The Underwater Robotics Market is expected to grow at a CAGR of 14.05% from 2026 to 2035.

Get in Touch