Autonomous Underwater Vehicle (AUV) Market Report Scope & Overview:

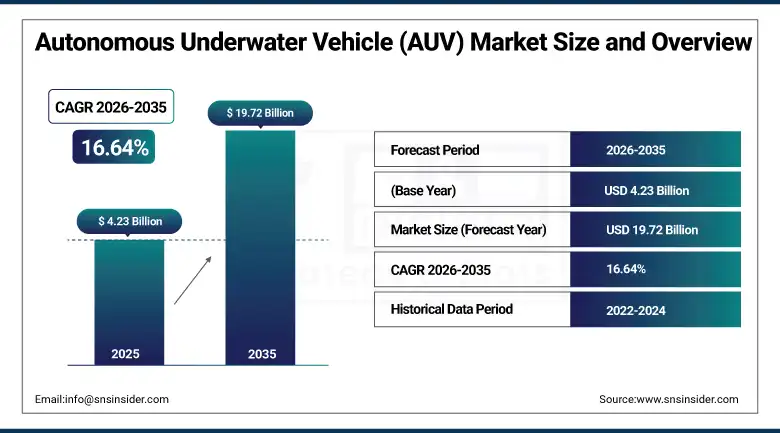

The Autonomous Underwater Vehicle (AUV) Market was valued at USD 4.23 Billion in 2025 and is expected to reach USD 19.72 Billion by 2035, growing at a CAGR of 16.64% from 2026 to 2035.

The global autonomous underwater vehicle market is growing rapidly as advancements in artificial intelligence, underwater navigation, sensor technology, and wireless acoustic communication. The market is driven by escalating global defense investment in naval surveillance, mine countermeasures, and anti-submarine warfare capability that creates structured government procurement for military-grade AUV systems, growing oil and gas pipeline and infrastructure inspection requirements that demand cost-effective automated survey alternatives to expensive diver and ROV inspection programmes, and the expanding scientific and environmental monitoring community whose climate change research, ocean acidification monitoring, and marine biodiversity assessment missions create sustained demand for autonomous deep-sea survey platforms.

In 2023, Boeing expanded its Echo Voyager Extra Large Unmanned Undersea Vehicle series by launching an upgraded version with enhanced endurance and AI-driven navigation for military reconnaissance applications. The Echo Voyager's modular payload design, able to accommodate sensor packages demonstrates the commercial direction of large-displacement military AUV development toward multi-mission platform architectures that reduce per-mission procurement cost through mission equipment substitution rather than dedicated single-emission vehicle procurement.

Market Size and Forecast

-

Market Size in 2025E: USD 4.93 Billion

-

Market Size by 2035: USD 19.72 Billion

-

CAGR: 16.64% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Autonomous Underwater Vehicle (AUV) Market - Request Free Sample Report

Autonomous Underwater Vehicle (AUV) Market Trends

-

AI-powered mission planning enables AUVs to autonomously adjust routes based on real-time environmental and sensor data.

-

Multi-AUV swarm operations are improving efficiency in mine countermeasures, surveillance, and underwater infrastructure inspection missions.

-

Advanced lithium batteries and hydrogen fuel cells are extending AUV endurance for long-duration underwater operations.

-

Acoustic communication networks are enabling near real-time underwater data transmission between AUVs and surface assets.

-

Miniaturized AUVs are expanding adoption in harbor security, coastal monitoring, and shallow-water infrastructure inspection applications.

The U.S. Autonomous Underwater Vehicle (AUV) Market Outlook

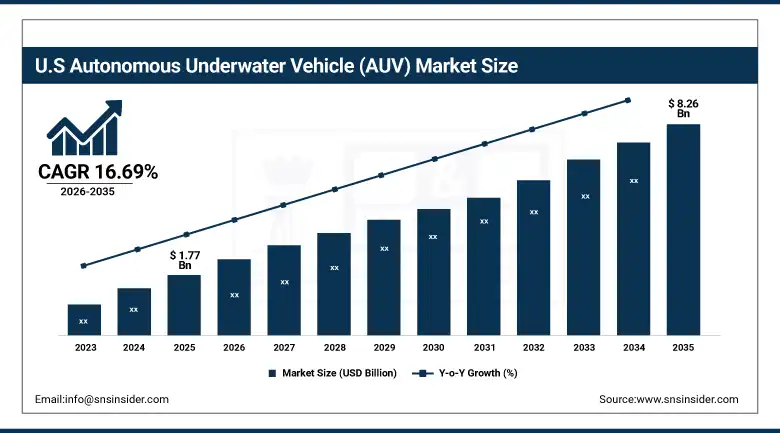

The U.S. Autonomous Underwater Vehicle (AUV) Market is the world's largest national AUV market, valued at approximately USD 1.77 Billion in 2025 and expected to reach approximately USD 8.26 Billion by 2035, growing at a CAGR of approximately 16.69%.

The U.S. is the dominant global AUV market through the extraordinary scale of U.S. Navy and DARPA AUV development and procurement investment, the offshore oil and gas industry's pipeline inspection demand, and the NOAA and academic oceanographic community's scientific survey programme. Teledyne Marine, Hydroid (Kongsberg Maritime), L3Harris Technologies, Boeing Defense, Exail Technologies, and Bluefin Robotics (General Dynamics Mission Systems) collectively define the domestic commercial AUV landscape. The U.S. Navy's Large Displacement Unmanned Undersea Vehicle programme, the Orca Extra Large UUV procurement from Boeing, and the Research Acequia AUV development programme create structured defense procurement that sustains domestic AUV manufacturer revenue independent of commercial market cycles. NOAA's ocean observation network investment creates additional civilian government AUV procurement.

In 2023, Kongsberg Maritime launched an advanced HUGIN Endurance AUV designed for deep-sea exploration and long-duration oceanographic missions, incorporating an enhanced energy system enabling mission endurance exceeding 72 hours at survey speed, high-resolution multibeam sonar, and AI-powered adaptive survey mode. The HUGIN Endurance targets the growing market for extended-endurance scientific survey AUVs whose mission duration advantage over conventional battery-limited platforms creates survey area coverage that cannot be achieved within the operational window of standard AUV mission profiles.

Autonomous Underwater Vehicle (AUV) Market Segment Analysis

-

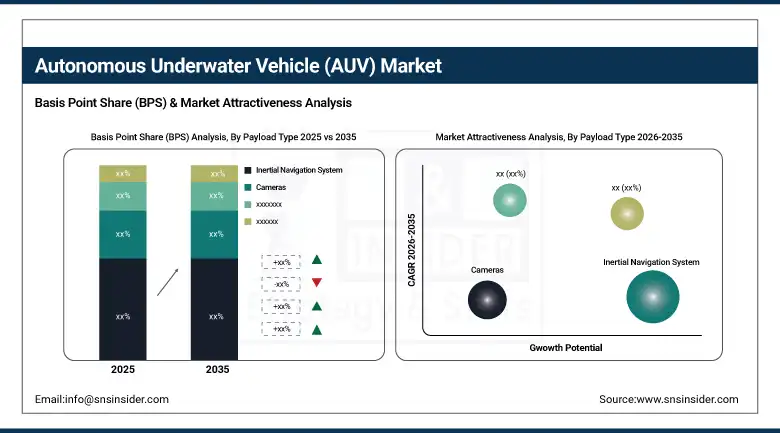

By Payload Type, the inertial navigation system segment dominated the market with the largest share in 2025, while the cameras segment is the fastest growing.

-

By Shape, the torpedo-shaped segment dominated the market with the largest share in 2025, while the multi-hull vehicle segment is the fastest growing.

-

By Technology, the navigation segment dominated the market with the largest share in 2025, while the collision avoidance segment is the fastest growing.

-

By Application, the defense segment dominated the market with the largest share in 2025, while the scientific research segment is the fastest growing.

By Payload, inertial navigation system dominates, cameras grow fastest

Inertial navigation systems retained the dominant payload position in the AUV market in 2025. The fundamental operational requirement for accurate position knowledge throughout GPS-denied underwater missions makes INS the mandatory foundational payload for every AUV regardless of primary mission purpose. Each AUV survey mission whose data geo-referencing requires position accuracy at the sub-meter level creates INS procurement whose performance specification determines the quality and scientific or operational value of all sensor data collected during the mission. Teledyne Marine's TSS inertial navigation systems and Kongsberg Maritime's high-performance INS solutions collectively demonstrate the commercial scale of navigation system procurement in AUV build programmes.

Cameras are the fastest growing payload because high-resolution visual inspection capability is becoming a standard AUV payload requirement across pipeline inspection, harbor security, coral reef monitoring, and archaeological site documentation missions that previously required expensive diver or ROV-based survey. Sonardyne International's compact high-resolution underwater camera with AI-powered image processing and Blue Robotics' upgraded low-light underwater camera collectively demonstrate the commercial development investment in AUV-integrated visual payload systems whose computational capability and optical sensitivity at depth create inspection quality previously only achievable at significantly higher operational cost.

By Application, defense dominates, scientific research grows fastest

Defense retained the dominant application position in the AUV market in 2025. The extraordinary per-unit commercial value of military-grade AUV systems, whose advanced sonar, AI autonomy, and endurance specifications create per-vehicle procurement values ranging from several million to tens of millions of dollars, creates defense application revenue dominance despite lower unit volumes relative to commercial alternatives. Mine countermeasures AUV procurement, whose replacement of dangerous manned mine hunting operations with autonomous survey vehicles creates humanitarian and operational motivation simultaneously, defines the most established defense AUV application.

Scientific research is the fastest growing application because the global recognition of climate change as an urgent research priority, the expansion of international ocean observation programme funding, and the oceanographic community's adoption of AUV technology as the standard deep-ocean survey platform creates structured institutional procurement growth. Each new oceanographic research vessel that deploys AUVs as its standard survey tool, each climate research programme that deploys AUV arrays for ocean heat content monitoring, and each marine biodiversity conservation programme that uses AUV visual surveys to assess reef ecosystem health creates AUV procurement whose commercial aggregate grows with international science funding allocation to ocean research.

By Shape, torpedo dominates, multi-hull grows fastest

Torpedo-shaped AUVs retained the dominant shape position in 2025. The hydrodynamic efficiency of streamlined cylindrical form factors whose low drag coefficient enables high-speed transit between survey areas with minimal energy consumption creates the operational range and endurance advantage that makes torpedo-shaped vehicles the preferred architecture for long-distance defense and scientific missions. Each military AUV programme that requires transit to a distant operational area before beginning survey operations creates a performance specification that torpedo-shaped vehicles’ transit efficiency advantage satisfies over competing multi-hull alternatives.

Multi-hull AUVs are the fastest growing shape because the stable platform advantage of catamaran and trimaran hulled AUV configurations creates superior sensor data quality during low-speed survey operations where platform motion disturbs acoustic, optical, and geophysical sensor measurements in ways that torpedo-shaped vehicles’ lower lateral stability exacerbates. Pipeline inspection, seabed habitat mapping, and archaeological documentation missions whose data quality requirements prioritize stability over transit speed create growing multi-hull procurement. Wave Glider-inspired designs and dedicated inspection AUV architectures from Saab, Fugro, and Ocean Infinity demonstrate the growing commercial investment in multi-hull AUV development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Norway |

28.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Autonomous Underwater Vehicle (AUV) Market Insights

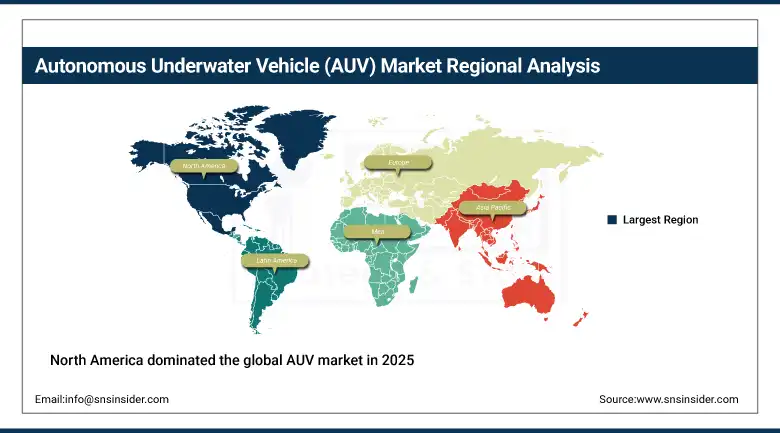

North America dominated the global AUV market in 2025 through the U.S. Navy's extraordinary AUV procurement investment, NOAA's oceanographic survey fleet, and the Gulf of Mexico offshore oil and gas industry's pipeline inspection demand. The United States accounts for approximately 87.4% of North American revenues through Teledyne Marine, Hydroid (Kongsberg), L3Harris Technologies, and Boeing Defense's commercial operations that define global AUV technology standards.

Canada contributes approximately 12.6% of North American revenues through the Department of National Defense's naval AUV investment, DFO's oceanographic research fleet AUV deployment, and the offshore energy sector's pipeline inspection programme in the Newfoundland Labrador basin.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Autonomous Underwater Vehicle (AUV) Market Insights

Europe is a technically sophisticated AUV market where NATO's undersea warfare modernization, North Sea oil and gas pipeline inspection, and the European scientific oceanographic community's survey fleet create structured institutional demand. Norway accounts for approximately 28.4% of European revenues through Kongsberg Maritime's global AUV leadership and the Norwegian offshore energy sector's subsea inspection investment. Saab's Swedish operations and ECA Group's French military AUV systems sustain European defense AUV supply.

The United Kingdom, France, and Germany are significant secondary markets where Royal Navy mine countermeasures AUV investment, French Navy GESMA underwater research, and the German Navy's Baltic and North Sea surveillance requirements create consistent defense procurement alongside commercial offshore and scientific survey demand.

Asia Pacific Autonomous Underwater Vehicle (AUV) Market Insights

Asia Pacific is the fastest growing regional AUV market, driven by escalating naval AUV investment from China, Japan, South Korea, Australia, and India whose strategic interest in undersea domain awareness and submarine detection creates growing defense AUV procurement, and the region's expanding offshore energy sector's pipeline inspection demand. China accounts for approximately 44.8% of Asia Pacific revenues through the People's Liberation Army Navy's AUV development investment, the CNOOC offshore oil and gas inspection programme, and academic oceanographic institute survey operations.

Australia represents a commercially significant market within Asia Pacific where the Royal Australian Navy's Ghost Bat and MQ-28 drone programme's undersea equivalent ambitions, the Australian Signals Directorate's maritime surveillance investment, and the offshore energy sector's deepwater pipeline inspection create structured AUV procurement growth.

MEA & Latin America Autonomous Underwater Vehicle (AUV) Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Saudi Aramco's offshore pipeline inspection programme, the Royal Saudi Naval Forces’ maritime surveillance investment, and the Red Sea undersea infrastructure monitoring creating structured AUV procurement. The UAE's ADNOC offshore operations and Israel's naval AUV programme add complementary demand.

Brazil leads Latin American revenues at approximately 44.2% through Petrobras’ deepwater pre-salt pipeline inspection programme and the Brazilian Navy’s submarine and mine countermeasure AUV investment. Chile’s scientific oceanographic community and Colombia’s offshore energy development collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Escalating naval AUV procurement for undersea domain awareness and offshore oil and gas automation of subsea inspection

Escalating global naval investment in AUV capability for mine countermeasures, anti-submarine warfare, and intelligence surveillance reconnaissance is the AUV market's most commercially certain structural growth driver. NATO member states’ commitment to undersea warfare modernization, the U.S. Navy's Large Displacement UUV programme, and Indo-Pacific naval powers’ investment in autonomous undersea sensor networks collectively create structured multi-year defense procurement whose total programme values create above-commercial-market commercial certainty. Each new naval AUV programme that transitions from manual mine hunting operations to autonomous AUV survey creates procurement whose scale reflects the human diver and MCM vessel replacement value that AUV technology enables.

Offshore oil and gas pipeline and infrastructure inspection automation represents the most commercially accessible near-term AUV market expansion opportunity whose total addressable market reflects the cost and safety risk of equivalent diver and ROV inspection methods. Each offshore operator that deploys AUVs for annual pipeline inspection creates above-ROV cost efficiency from reduced surface vessel charter time, operator crew size, and weather window dependency that AUV's pre-launched autonomous survey profile eliminates relative to vessel-deployed ROV inspection alternatives.

Restraints: High manufacturing cost and underwater communication bandwidth limitations

High manufacturing and maintenance costs for advanced AUV systems whose AI navigation, precision sonar, and pressure-resistant structural materials create per-unit costs ranging from USD 500,000 to over USD 10 million for military-grade large-displacement vehicles create adoption barriers for cost-sensitive commercial and research operators whose programme economics require demonstrated ROI justification before AUV investment approval. Deep-sea repair logistics, whose AUV recovery and servicing in remote ocean environments creates above-commercial-standard maintenance cost, adds operational cost beyond initial vehicle procurement.

Underwater communication bandwidth limitations, whose acoustic modem data rate typically peaks at 100 kilobits per second versus gigabit-per-second surface wireless alternatives, constrains real-time high-definition video transmission and large dataset relay from AUV missions to surface operators. Each mission that generates terabytes of sonar and imagery data that can only be retrieved at end-of-emission vehicle recovery creates operational constraints that reduce AUV utility in time-sensitive defense and safety applications requiring real-time data access.

Opportunities: Climate research AUV fleet expansion and multi-AUV swarm deployment

Climate change research AUV fleet expansion represents the most commercially significant science-driven market opportunity whose institutional funding from national science agencies, the European Research Council, and international ocean observation programme investment creates structured government-funded AUV procurement. Each new ocean observation initiative that deploys AUV arrays for temperature, salinity, oxygen, and chemical tracer profiling creates procurement whose mission criticality motivates multi-vehicle redundancy that multiplies per-programme commercial value beyond single-vehicle survey missions.

Multi-AUV cooperative swarm deployment creates the most commercially transformative operational capability advance whose coordinated survey coverage, acoustic communication network, and distributed sensor fusion enable mission types that single-AUV operation cannot achieve within acceptable time or cost constraints. Each mine hunting programme that deploys an AUV swarm for coordinated area coverage creates procurement of multiple vehicles whose collective survey efficiency justifies above-single-vehicle cost through mission area completion time reduction that has direct operational value in military and emergency response contexts.

Recent Developments:

-

2026: Kongsberg Discovery announced the start of HUGIN AUV production in the United States to strengthen domestic manufacturing capacity and support growing demand from U.S. Navy, defense, and commercial subsea customers.

-

2026: Anduril Industries was selected by the U.S. Navy and Defense Innovation Unit for the Combat Autonomous Maritime Platform (CAMP) program, advancing deployment of its Dive-XL autonomous underwater vehicle for extended-range undersea missions.

-

2025: Anduril Industries unveiled the Copperhead family of autonomous underwater vehicles, designed for intelligence, surveillance, infrastructure inspection, and collaborative deployment from larger Dive-XL and Dive-LD platforms.

-

2025: Ocean Infinity expanded deployment of HUGIN 6000 autonomous underwater vehicles for deep-sea survey and search operations, supporting large-scale subsea mapping and offshore exploration activities.

Autonomous Underwater Vehicle (AUV) Market Key Players are:

-

Kongsberg Maritime AS (HUGIN Series)

-

Teledyne Marine (Gavia, Sentry)

-

L3Harris Technologies Inc.

-

Boeing Defense, Space & Security (Echo Voyager)

-

General Dynamics Mission Systems (Bluefin Robotics)

-

Saab AB (Sabertooth)

-

ECA Group

-

HII Mission Technologies (REMUS Series)

-

Fugro N.V.

-

Ocean Infinity Ltd.

-

Exail Technologies SA

-

Sonardyne International Ltd.

-

Liquid Robotics Inc. (Boeing)

-

Riptide Autonomous Solutions

-

Atlas Elektronik GmbH

-

BAE Systems plc

-

Thales Group SA

-

Anduril Industries

-

Ocean Aero, Inc.

-

MSubs Ltd.

Autonomous Underwater Vehicle (AUV) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.23 Billion |

| Market Size by 2035 | USD 19.72 Billion |

| CAGR | CAGR of 16.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Payload Type (Cameras, Sensors, Inertial Navigation System, Others) • By Shape (Torpedo, Streamlined Rectangular Style, Laminar Flow Body, Multi-hull Vehicle) • By Technology (Collision Avoidance, Navigation, Imaging, Communication, Propulsion) • By Application (Scientific Research, Defense, Oil & Gas Industry) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Kongsberg Maritime AS (HUGIN Series), Teledyne Marine (Gavia, Sentry), L3Harris Technologies Inc., Boeing Defense, Space & Security (Echo Voyager), General Dynamics Mission Systems (Bluefin Robotics), Saab AB (Sabertooth), ECA Group, HII Mission Technologies (REMUS Series), Fugro N.V., Ocean Infinity Ltd., Exail Technologies SA, Sonardyne International Ltd., Liquid Robotics Inc. (Boeing), Riptide Autonomous Solutions, Atlas Elektronik GmbH, BAE Systems plc, Thales Group SA, Anduril Industries, Ocean Aero, Inc., MSubs Ltd. |

Frequently Asked Questions

The Autonomous Underwater Vehicle (AUV) Market is expected to grow at a CAGR of 16.64% from 2026 to 2035.

The Autonomous Underwater Vehicle (AUV) Market was valued at USD 4.23 Billion in 2025.

Escalating global naval AUV procurement investment for mine countermeasures, anti-submarine warfare, and undersea surveillance creating structured multi-year defense procurement.

Inertial Navigation System dominated the AUV Market with the largest share in 2025.

North America dominated the Autonomous Underwater Vehicle Market in 2025.

Get in Touch