Virtual Fitness Market Report Scope & Overview:

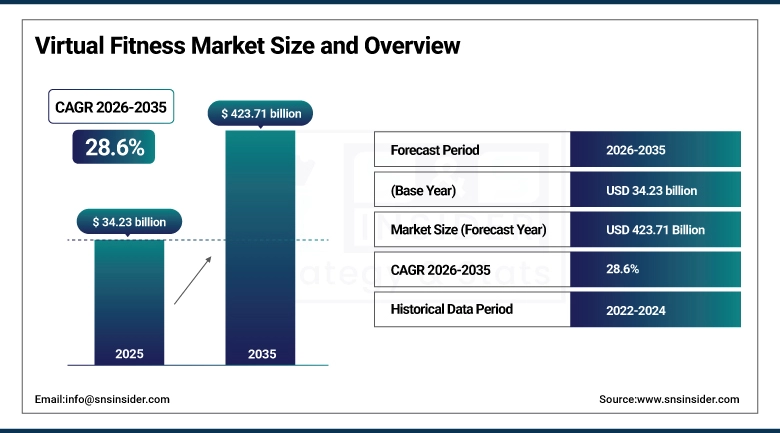

The Virtual Fitness Market size was estimated at USD 34.23 billion in 2025 and is expected to reach USD 423.71 billion by 2035 and grow at a CAGR of 28.6% over the forecast period of 2026-2035.

The growth of the virtual fitness industry can be attributed to the adoption of health technology platforms, rapid technology advancements in streaming technologies and wearables, and an ever-increasing preference for working out from home. Millions of people around the world use fitness programs which deliver live and on-demand fitness content to devices (smartphones, smart televisions, tablets, laptops etc.) as part of their health regimes.

Many more people today have access to high-speed internet with abundant 5G connections and broadband filling over 80% of households in developed economies which have enhanced both streaming experience quality and interactivity. Additionally, the rise of lifestyle diseases like obesity which affects over 650 million on earth and heart diseases which kill 17.9 million people a year have played a huge role in the expansion of the virtual fitness industry.

Virtual Fitness Market Size and Forecast:

-

Market Size in 2025: USD 34.23 billion

-

Market Size by 2035: USD 423.71 billion

-

CAGR: 28.6% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Virtual Fitness Market - Request Free Sample Report

Virtual Fitness Market Trends:

-

Fast adoption of AI-based personalized virtual fitness services, providing customized training sessions, instant correction, and adaptive complexity, resulting in an increase in retention rate by 38%.

-

Faster deployment of wearable technology, including such devices as smartwatches and heartrate sensors, allowing biofeedback coaching and synchronization with exercise performance.

-

Increasing use of gamification in fitness apps, including leaderboards and challenges that ensure 52% increased user activity during the month.

-

Increasing popularity of corporate wellness segment, where enterprises spend ~USD 762 per employee each year, resulting in B2B subscriptions growth.

-

Increasing integration of virtual reality technology in fitness content with a 120% increase in VR app downloads (in terms of 2023–2024).

-

Increasing number of hybrid fitness services, whereby users take both gym memberships and virtual subscriptions (for North America & Europe, 2024), and their share amounts to 34%.

-

Increasing demand for instructor-led live streaming for fitness workouts such as HIIT, yoga, and spinning, with annual growth rates of 31%.

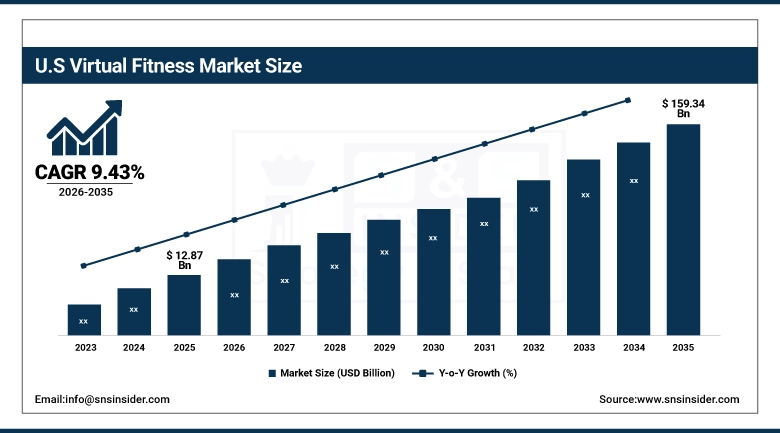

The U.S. Virtual Fitness Market was valued at USD 12.87 billion in 2025 and is projected to reach USD 159.34 billion by 2035, growing at a CAGR of 28.4% from 2026–2035. With high digital literacy rates, smartphone penetration above 91% and strong wellness spend of approximately USD 1,432 per capita per year, the United States remains the largest individual country level market by far.

Market growth is supported by global brand recognition, the Affordable Care Act suggesting more workplace wellness initiatives, and strong demand for paid subscriptions. Strategic partnerships with insurer companies such as Aetna, UnitedHealth group, and Cigna will further accelerate penetration in the market via cost sharing mechanisms and incentive-based user engagement strategies.

Virtual Fitness Market Growth Drivers:

- Surging Demand for Convenient, Accessible, and Cost-Effective Fitness Solutions is Fueling Virtual Fitness Market Expansion

The movement towards home fitness and hybrid fitness options from traditional gym-based exercise forms the major factor responsible for the growth of the virtual fitness industry. While regular gym membership in the USA costs USD 507 annually, virtual fitness plans cost between USD 96 and USD 468, providing equally good or better quality content than the traditional form of membership.

The urbanized lifestyle that involves hectic schedules, such as an average commuting time of 54 minutes a day for US employees, along with the growing trend of working remotely beyond 22%, as observed by 2024, have forever changed the way individuals workout. Virtual platforms allow for the elimination of commuting time and scheduling conflicts, making it possible to exercise during any fragmented time period available.

Virtual Fitness Market Restraints:

- High Platform Churn Rates and Subscription Fatigue are Constraining Virtual Fitness Market Revenue Stability

Despite the rapid addition of users, virtual fitness apps have high churn (35 to 50%), which makes income streams less stable and costs of customer acquisition higher. The rise in competition is contributory to subscription fatigue, with folks brining an average of 4.7 subscriptions in the air, before cutting engagement with fitness subscriptions during periods of disuse.

Other contributing factors include a lack of self motivation and accountability when exercising at home, with data showing that 61% of users have reduced the frequency of their sessions by 50% within 90 days. Although enterprises have built artificial intelligence-enabled engagement features for retention and community building, the operational cost associated with it is a barrier.

Virtual Fitness Market Opportunities:

- Integration of Artificial Intelligence, Extended Reality Technologies, and Emerging Market Penetration are Generating Substantial Growth Opportunities for the Virtual Fitness Market

Real integrated value in the virtual fitness Industry comes from an amalgamation of AI-driven coaching, real-time biometrics from wearables, and XR environments. The niche application of AI to personalize workouts by analysing real-time health parameters, recovery metrics, and performance records to modify the intensity, approach, and duration of workouts is attracting a 28% reduction in churn while driving up premium subscriptions by 19%.

Furthermore, there is growth potential in developing markets in Latin America, South Asia, and Sub-Saharan Africa, thanks to mobile fitness apps with 40%+ CAGR adoption in Brazil, Indonesia, Nigeria and Vietnam. Localized content, coaches in regional languages, and micro subscriptions, with prices between USD 2 and USD 8 per month are propelling this trend.

Virtual Fitness Market Segment Analysis:

-

By session type, group sessions accounted for the largest share of approximately 57.43% in 2025, while the solo segment is expected to register the fastest growth with a CAGR of 29.8% over the forecast period.

-

By streaming type, on-demand streaming dominated the market with nearly 64.72% share in 2025, whereas live streaming is anticipated to witness the highest growth with a CAGR of 30.4%.

-

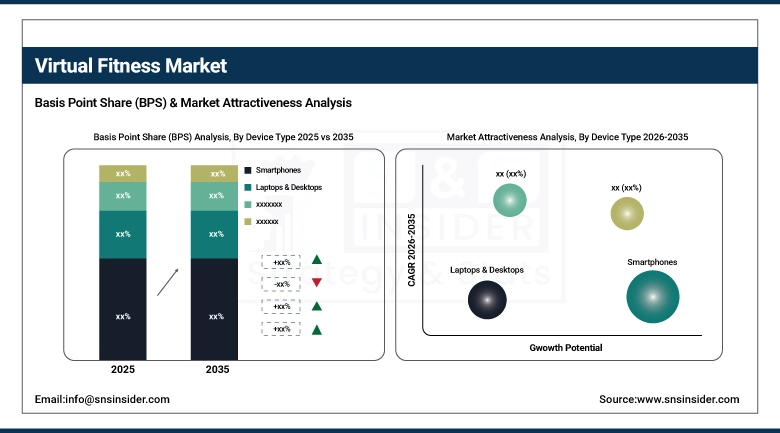

By device type, smartphones led the market with approximately 42.16% share in 2025, while smart TVs are projected to register the fastest growth with a CAGR of 31.7%.

By Device Type, Smartphones Lead, While Smart TVs Register the Fastest Growth

Smartphones dominate due to widespread availability, advanced camera features for motion tracking and form analysis, and ease of use for on-the-go workouts. Smart TVs are the fastest-growing segment, driven by demand for immersive large-screen fitness experiences, with US connected TV households reaching 115 million in 2024.

By Session Type, Group Sessions Lead the Market, While Solo Sessions Are the Fastest Growing

The Group Sessions segment is dominating the market, given the social accountability-motivation-community niche characteristics (similar to some components of live classes). The platforms for live and pre-recorded sessions that include biking, yoga, HIIT, dance cardio, and strength training are showing an average 74% session retention compared to 58% for solo sessions.

The solo session segment is the fastest-growing category. The key factors contributing to the rapid growth of this market include AI-Driven personalisation, increased interest in online classes and integration of biometrics from built-in fitness trackers. It gives users tailored workout plans depending on how users performed and recovered, just like personal trainers do.

By Streaming Type, On-Demand Dominates, While Live Streaming Registers Rapid Growth

On-demand streaming has become the most popular format due to its convenience regarding scheduling and its broad range of classes, which often exceeds 10,000 for one platform. It can be a perfect choice for people with unpredictable schedules because it allows everyone to choose their level and purpose of workout during a paid subscription.

Live streaming is a rapidly developing type due to social aspects, including live competition through leaderboards and instructor feedback. Live feedback from trainers makes workouts more engaging, thus helping users stay more committed and have a higher net promoter score.

Virtual Fitness Market Regional Highlights:

North America Virtual Fitness Market Insights:

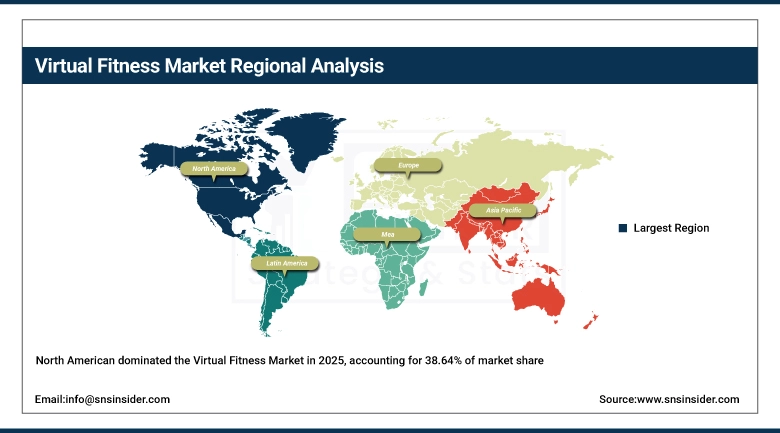

The virtual fitness market was dominated by North America with a share of 38.64% in 2025. Digital home fitness spending per capita is highest in the region, with U.S. consumers spending around USD 312 annually on subscription and connected fitness hardware. As of 2024, 83% of large U.S. employers still are providing some form of employer wellness integration, which protects against consumer-based churn for platform revenues. Approximately 9% of regional revenue comes from Canada, assisted by provincial digital health initiatives and French Canadian adoption supported through the addition of bilingual content.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Virtual Fitness Market Insights:

The Asia Pacific region will witness the highest CAGR of 30.2% during the forecast period owing to the addressable population of higher than 2.8 billion total in China, India, Japan, South Korea, and Southeast Asia. By 2024, 420 million people use virtual fitness apps in China, with companies including Keep, Lefit, and SuperMonkey distributing content via their apps. For fitness apps by fastest-growing on a countries basis, India runs away with 487 million downloads in 2024, a year-on-year change of 62% highlighted by the explosive adoption of low-cost $2.10 monthly high-speed 5G data plans and median age of 28.4 years.

Europe Virtual Fitness Market Insights:

Europe was the second-biggest player in the virtual fitness market in 2025, grabbing about 26.18% of the global share. The UK, Germany, France, and the Netherlands delivered over 64% of the region’s revenue. GDPR keeps a tight grip on how biometric and health data gets handled—consent models matter. In Germany and Scandinavia, corporate wellness requirements push B2B uptake; German enterprise deals average roughly €1.2 million a year.

Latin America (LATAM) and Middle East & Africa (MEA) Virtual Fitness Market Insights:

The LATAM region and the MEA market are both developing economies, and they’re growing fast—with an overall CAGR of 27% to 29%. Take Brazil, the biggest market in Latin America. It had around 89 million fitness app users and virtual fitness subscribers in 2024, pulling in USD 1.4 billion in revenue. That kind of traction comes from a couple of things: high social engagement around fitness activities and a freemium model that actually works. Over in the MEA market, the UAE and Saudi Arabia are the key players. Saudi Vision 2030 alone has poured more than USD 750 million into digital health and fitness infrastructure.

Virtual Fitness Market Competitive Landscape:

Peloton Interactive, Inc., founded in 2012, is a leading player in the connected virtual fitness market, integrating proprietary hardware such as bikes and treadmills with a subscription-based digital platform offering live and on-demand classes across cycling, running, strength, yoga, and meditation. Its hardware-independent Peloton App tier has expanded total addressable market beyond device owners.

- In January 2025: Peloton launched an AI-powered coaching feature delivering real-time personalized workout recommendations using performance, recovery, and goal-based data, improving 90-day subscriber retention by 21% in the U.S.

iFIT Health & Fitness, Inc., established in 1977 and rebranded to reflect its digital-first strategy, operates connected fitness brands including NordicTrack and ProForm, serving 6M+ global subscribers across cardio equipment. Its iFIT platform delivers trainer-led immersive outdoor workouts globally.

- In March 2025: iFIT introduced Google Maps-integrated route streaming across 50 new destinations and expanded multilingual content in Mandarin, Spanish, and Portuguese to drive growth in Asia Pacific and Latin America.

Les Mills International Ltd., founded in 1968, is a global leader in group fitness content via its Les Mills+ platform, licensed across 21,000+ fitness clubs in 100 countries. Its portfolio includes BODYPUMP, BODYCOMBAT, RPM, and SPRINT in live and on-demand formats.

- In February 2025: Les Mills launched LES MILLS+ Live with 60+ weekly live classes across major regions, reaching 1.4M live attendances within eight weeks.

Virtual Fitness Market Key Players:

-

Peloton Interactive, Inc.

-

iFIT Health & Fitness, Inc. (NordicTrack, ProForm)

-

Apple Fitness+ (Apple Inc.)

-

Les Mills International Ltd.

-

Beachbody, LLC (BODi)

-

ClassPass, Inc. (Mindbody)

-

Zwift, Inc.

-

Tonal Systems, Inc.

-

Hydrow, Inc.

-

Echelon Fitness Multimedia, LLC

-

FitOn Health, Inc.

-

Obé Fitness, Inc.

-

Daily Burn, Inc.

-

Strava, Inc.

-

Nike Training Club (Nike, Inc.)

-

Technogym S.p.A.

-

Noom, Inc.

-

Whoop, Inc.

-

Centr (Chris Hemsworth Enterprises Pty Ltd)

-

Future Fit Training, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 34.23 Billion |

| Market Size by 2035 | USD 423.71 Billion |

| CAGR | CAGR of 28.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Session Type (Group, Solo) • By Streaming Type (Live, On-demand) • By Device Type (Smart TV, Smartphones, Laptops & Desktops, Tablets) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Peloton Interactive Inc., iFIT Health & Fitness Inc. (NordicTrack, ProForm), Apple Fitness (Apple Inc.), Les Mills International Ltd., Beachbody LLC (BODi), ClassPass Inc. (Mindbody), Zwift Inc., Tonal Systems Inc., Hydrow Inc., Echelon Fitness Multimedia LLC, FitOn Health Inc., Obé Fitness Inc., Daily Burn Inc., Strava Inc., Nike Training Club (Nike, Inc.), Technogym S.p.A., Noom Inc., Whoop Inc., Centr (Chris Hemsworth Enterprises Pty Ltd), Future Fit Training Inc. |

Frequently Asked Questions

The Virtual Fitness Market was valued at USD 34.23 billion in 2025 and is projected to reach USD 423.71 billion by 2035, growing at a CAGR of 28.6% during 2026-2035, driven by rising digital health adoption and home-based workout trends.

The Virtual Fitness Market is expanding due to increased demand for convenient and cost-effective fitness solutions, growing adoption of wearables and AI-based platforms, and rising lifestyle diseases encouraging digital fitness engagement.

In the Virtual Fitness Market, on-demand streaming leads with around 64.72% market share in 2025, while group sessions dominate by session type with over 57% share due to higher engagement and retention rates.

North America dominates the Virtual Fitness Market with a 38.64% share in 2025, supported by high digital penetration, strong wellness spending, and widespread adoption of subscription-based fitness platforms.

Key trends in the Virtual Fitness Market include AI-powered personalized training, rapid growth in wearable integration, gamification features increasing engagement, and rising adoption of virtual reality-based fitness experiences.

Get in Touch