Virus Filtration Market Report Scope & Overview:

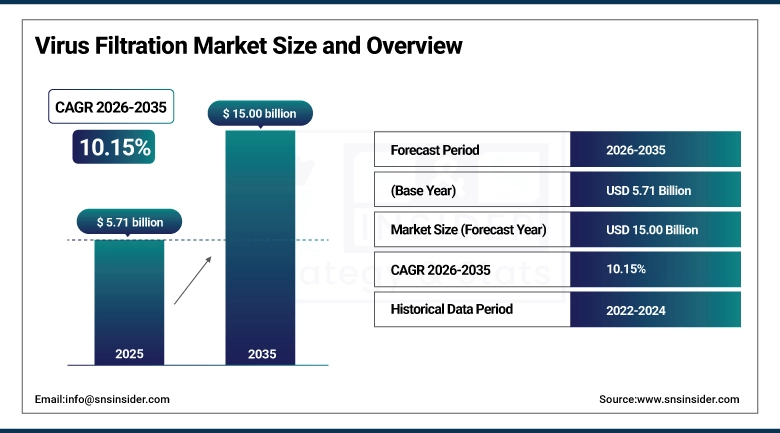

The Virus Filtration Market was valued at USD 5.71 Billion in 2025 and is expected to reach USD 15.00 Billion by 2035, growing at a CAGR of 10.15% from 2026–2035.

Virus filtration technology serves as a critical safety checkpoint in the manufacture of Virus filtration technology provides an essential safeguard in the production of biologicals, vaccines, blood components, and advanced therapy medicinal products, filtering out or inactivating any possible viral contaminants in order to prevent them from reaching patients. The increasing demand from the biopharmaceutical and biotechnology companies for effective solutions in the area of viral clearance is driving the market growth in conjunction with the heightened regulatory focus on viral clearance validation by such agencies as the FDA, EMA, and ICH. The growing application of single-use bioprocessing equipment and continuous manufacturing technologies has added to the demand for both virus-retentive filter membranes and viral clearance through chromatography as the companies seek validated and scalable solutions for growing volumes of biologics production.

The approval of a total of 73 novel biologics and biosimilar products in 2024 by the United States Food and Drug Administration was a new record for the agency and created direct and visible demand for viral clearance validation services and virus-retentive filtration consumables among the United States-based contract development and manufacturing organizations.

Market Size and Forecast

-

Market Size in 2026E: USD 6.29 Billion

-

Market Size by 2035: USD 15.00 Billion

-

CAGR: 10.15% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Virus Filtration Market - Request Free Sample Report

Virus Filtration Market Trends

-

Adoption of single-use virus filtration assemblies in biopharmaceutical manufacturing continues to rise, reducing cross-contamination risk, cleaning validation burden, and overall production timelines.

-

Virus-retentive nanofiltration membranes are increasingly integrated with downstream bioprocessing workflows, supporting higher-throughput viral clearance with consistent log reduction values above 4.0 log10 for parvoviruses.

-

Expansion of continuous bioprocessing models is driving demand for inline viral filtration modules capable of supporting real-time process monitoring and automated flow control.

-

Growing application of virus filtration in cell and gene therapy manufacturing, including lentiviral and adeno-associated virus vector production, is accelerating adoption of specialized hollow-fiber filtration technology.

-

Rising regulatory emphasis on adventitious agent testing and viral clearance studies for biologics continues to accelerate uptake of GMP-grade filtration consumables and third-party validation services.

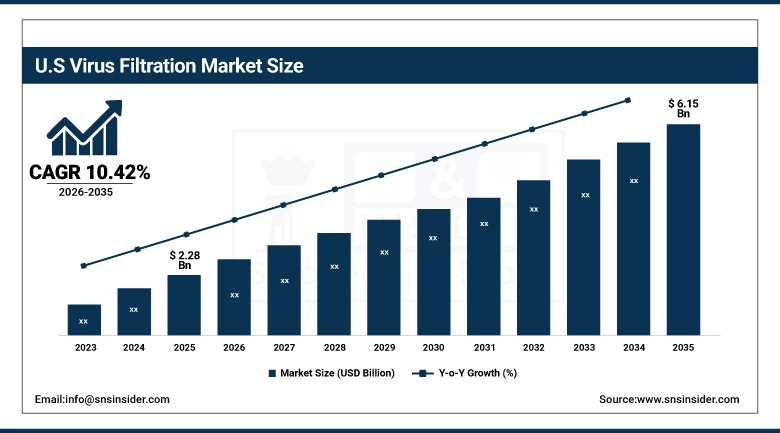

U.S. Virus Filtration Market Outlook

The U.S. Virus Filtration Market was valued at approximately USD 2.28 Billion in 2025 and is expected to reach approximately USD 6.15 Billion by 2035, growing at a CAGR of approximately 10.42%.

The US takes the largest percentage of the worldwide virus filtration market, due to the advanced biopharmaceuticals industry in the US, stringent guidelines for viral safety by FDA, and high investment in biologics and cell/gene therapy R&D. A large concentration of contract development and manufacturing organizations, academic institutions, and biotech companies within the major biopharmaceutical clusters, as well as high NIH spending on infectious disease/vaccine R&D, has been a driving factor behind the increased use of virus filtration technology in the country.

In March 2024, revenue from global biological drugs exceeded $420 billion, with virus filtration consumables making up 18% of the total downstream bioprocessing supply costs of the top twenty pharmaceutical companies. This number demonstrates the huge and increasing percentage of the total biologics manufacturing cost associated with virus filtration technology, which is due to increased regulation as well as increased applications for the technology in different types of biologics products.

Virus Filtration Market Segment Analysis

-

By Product, the Consumables segment dominated the Virus Filtration Market with approximately 57.42% share in 2025, while the Services segment is the fastest growing with a CAGR of approximately 11.23%.

-

By Technology, the Filtration segment dominated the Virus Filtration Market with approximately 61.85% share in 2025, while the Chromatography segment is the fastest growing with a CAGR of approximately 11.47%.

-

By Application, the Biologicals segment dominated the Virus Filtration Market with approximately 64.32% share in 2025 and is also expected to register the fastest growth with a CAGR of approximately 11.06%.

-

By End-Use, the Biopharmaceutical & Biotechnology Companies segment dominated the Virus Filtration Market with approximately 54.71% share in 2025, while the Contract Research Organizations segment is the fastest growing with a CAGR of approximately 11.84%.

By Product, consumables dominate, services grow fastest

Consumables comprised about 57.42% share of the market in 2025, driven by stable and repetitive demands for virus retention membrane filters, kits and reagents, and disposable filtration assemblies in biologics manufacturing process. The demand for consumables will be constant and mostly immune from underlying capital equipment purchasing trends because batch process cycles for manufacturing monoclonal antibodies and plasma derived products often exceed equipment replacement cycle.

The services segment is expected to be the fastest growing segment with the CAGR of 11.23% during the forecast period, fueled by the trend toward outsourcing of viral clearance validation studies, filter performance qualification, and other regulatory services to contract testing facilities. Stringent regulations along with requirement of biosafety level-2 facilities continue to bolster this trend.

By Technology, filtration dominates, chromatography grows fastest

Filtration technology held approximately 61.85% of the market in 2025, supported by its broad applicability across biologics manufacturing, blood fractionation, and plasma processing, where virus-retentive nanofiltration membranes deliver high log reduction values against both enveloped and non-enveloped viruses. Continued improvements in membrane chemistry, pore size uniformity, and pre-validated filter formats have further reinforced this segment's leading market position.

The chromatography segment is expected to register the fastest growth, at approximately 11.47% CAGR, driven by its increasing incorporation into biologic purification platforms as an orthogonal viral clearance step. Anion exchange and mixed-mode chromatography resins offering flow-through viral clearance properties are seeing particularly strong adoption within next-generation monoclonal antibody and gene therapy purification platforms.

By Application, biologicals leads and registers the fastest growth

The biologicals segment constituted about 64.32% of the market in 2025, which is due to the high demand from vaccine and therapeutics manufacturing, plasma-based biologicals, and increasing applications in cellular and gene therapy. The regulations calling for multi-pass virus clearance in all biologicals create continuous demand for filter consumables in this field of application.

Cellular and gene therapy is the fastest-growing sub-segment of the biologicals segment, because of the scale-up of viral vector production, as well as commercializing platforms for ex vivo cell therapy manufacturing. Applications in medical devices grow owing to increased need for validation of virus removal during device manufacturing; water purification and air purification applications bring additional growth to the whole market.

By End-Use, biopharmaceutical and biotechnology companies lead, contract research organizations grow fastest

Biopharmaceutical and biotechnology companies accounted for approximately 54.71% of the market in 2025, driven by large-scale in-house biologics production and the corresponding requirement for validated viral clearance within GMP-compliant manufacturing environments. These organizations represent the largest purchasers of high-value filtration equipment, including filtration assemblies and validation tools, reinforcing their leading position within the end-use landscape.

Contract research organizations are projected to register the fastest growth, at approximately 11.84% CAGR, as an increasing number of pharmaceutical companies outsource viral safety testing, clearance study development, and regulatory support to specialized providers. This trend reflects a broader industry shift toward outsourced research and development models that allow biopharmaceutical companies to access specialized viral safety expertise without maintaining extensive in-house capability.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.0% |

|

Europe |

Germany |

25.0% |

|

Asia Pacific |

China |

39.0% |

|

Middle East & Africa |

UAE |

29.0% |

|

Latin America |

Brazil |

37.0% |

North America Virus Filtration Market Insights

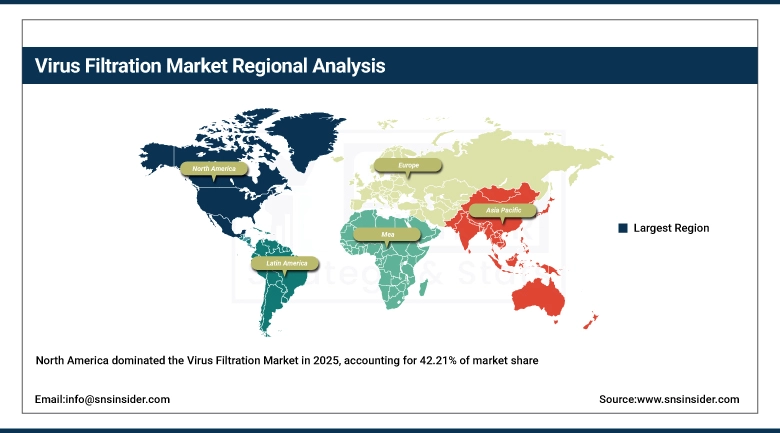

North America accounted for the largest virus filtration market in 2025 with a market share of over 42.21%. This dominance in the market can be attributed to factors including the biopharmaceutical industry presence in the region, stringent requirements of viral safety testing by the FDA, and presence of many biological drugs manufacturers and CDMOs in the United States. The growing capacity for production of mRNA vaccines and increasing capacity for plasma fractionation, along with advanced therapy medicinal products manufacturing infrastructure in California, keeps driving the need for virus-retentive filtration systems.

The United States is the major commercial center in the region, driven by the presence of major pharmaceutical companies headquartered globally in the Northeast and West Coast regions. Canada has seen growth in its biotechnology sector in recent years, adding to the demand in the region incrementally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Virus Filtration Market Insights

Asia Pacific holds the highest growth potential within the virus filtration market, with a projected CAGR of approximately 12.35% through the forecast period, driven by expanding biopharmaceutical manufacturing capacity across China, India, South Korea, and Japan. Government-backed initiatives, including China's Fourteenth Five-Year Plan for biopharmaceutical manufacturing, India's National Biopharma Mission, and South Korea's K-Bio strategy, are directing substantial investment toward domestic biopharmaceutical manufacturing infrastructure.

A growing number of biosimilar manufacturers across the region are pursuing regulatory approval both domestically and internationally, while expanded vaccine production mandates stemming from the COVID-19 pandemic and a rising number of regional contract research and manufacturing organizations continue to support strong growth within the regional virus filtration market.

Europe Virus Filtration Market Insights

Europe is considered the second largest regional market for virus filtration, thanks to the presence of guidelines on viral safety from the European Medicines Agency, existing plasma fractionation industries in Germany, France, and the UK, as well as growing research and development in the advanced therapies space. EMA’s guidance on the evaluation of viral safety, CPMP/BWP/268/95, together with the need to eliminate adventitious agents in biological products, will help to continue supporting the demand for efficient virus filtration and chromatography equipment within the region.

Harmonization of cross-border production due to EU pharmaceutical legislation, together with the development of biopharmaceutical hubs in Northern and Eastern Europe, will create considerable potential for the region. These factors are likely to ensure sustainable market growth in the coming years.

MEA & Latin America Virus Filtration Market Insights

Latin America is adopting virus filtration technology through national biological manufacturing programs and growing integration with contract development and manufacturing organizations targeting regulated export markets. Key demand drivers within the region include continued investment in plasma fractionation infrastructure and efforts toward vaccine manufacturing self-sufficiency across major economies.

The United Arab Emirates and Saudi Arabia are emerging as regional biopharmaceutical manufacturing hubs within the Middle East and Africa, supported by healthcare investment programs aligned with Vision 2030 and rising demand for GMP-grade virus filtration consumables to support regional biologics production facilities. Expanding internet infrastructure across Sub-Saharan Africa is also supporting incremental growth in basic plasma safety filtration investment across the continent.

Market Dynamics

Growth Drivers: Rising biologics production and viral safety regulation sustain steady demand

The expanding global market for monoclonal antibodies, recombinant proteins, vaccines, and plasma-derived products represents the principal driver of virus filtration market growth. Regulatory bodies including the FDA, EMA, and World Health Organization have consistently emphasized the necessity of robust viral clearance studies as a prerequisite for biological product approval, sustaining consistent demand for virus-retentive filters, validation test kits, and downstream chromatography products across the industry.

Continued growth in biosimilar development represents an additional meaningful driver, as does the ongoing expansion of mRNA vaccine technology following its accelerated development during the COVID-19 pandemic. As biologic drug revenues continue to expand and virus filtration consumables account for a growing share of downstream bioprocessing expenditure among leading pharmaceutical manufacturers, this structural demand is expected to remain a durable growth driver throughout the forecast period.

Restraints: High validation costs and limited specialized workforce constrain broader adoption

The expensive nature of the validation process with regard to the capital costs involved with the model virus testing, laboratory setup at BSL-2 facility and regulatory matters poses a considerable challenge, especially for small and mid-size biopharmaceutical firms and academia due to their limited budgets. The cost of conducting one viral clearance validation test can be estimated between USD 150,000 and USD 400,000, and this can considerably hinder entry into the market for the smaller firms.

The scarcity of bioprocess engineers with relevant expertise in assessing viral safety and GMP filtration technology is another factor, especially in developing countries where the biopharmaceutical sector is at an early stage of development.

Opportunities: Cell and gene therapy manufacturing expansion presents substantial growth potential

Rapid growth in cell and gene therapy development pipelines represents a substantial opportunity for virus filtration technology suppliers. Manufacturing processes for adeno-associated virus and lentiviral vectors require specialized tangential flow filtration and depth filtration products to ensure appropriate concentration, purity, and clearance of adventitious agents. With more than 3,500 active gene therapy trials currently underway and over 40 gene therapy products approved or under rolling regulatory review, demand for specialized virus filtration capability continues to accelerate.

According to the Alliance for Regenerative Medicine, global cell and gene therapy investment reached USD 9.8 billion in 2023, with viral vector manufacturing infrastructure accounting for over 31 percent of total facility capital expenditures within the sector. Continued investment in specialized viral vector contract development and manufacturing organizations, along with the expansion of academic spin-out manufacturing facilities, is directly expanding the addressable market for virus filtration products and platforms.

Recent Developments:

-

2024: In April 2024, Cytiva introduced a next-generation Ultipor VF Grade DV20 filter with enhanced non-enveloped virus retention performance and a 30% improvement in filtrate flux, targeting high-throughput plasma and biologic purification applications.

-

2024: In September 2024, Sartorius AG expanded its BioStat STR bioreactor line with an integrated downstream viral filtration module, enabling seamless end-to-end bioprocessing from cell culture through viral clearance within a single automated platform for monoclonal antibody manufacturers.

-

2025: In February 2025, Merck KGaA launched an enhanced Viresolve Pro filtration platform featuring improved flux performance and a pre-validated, audit-ready viral clearance data package designed to reduce regulatory submission timelines for biopharmaceutical manufacturers.

Virus Filtration Market Key Players

-

Merck KGaA

-

Sartorius AG

-

Cytiva

-

Pall Corporation

-

Thermo Fisher Scientific Inc.

-

Asahi Kasei Medical Co., Ltd.

-

Charles River Laboratories International, Inc.

-

Lonza Group AG

-

Repligen Corporation

-

3M Purification Inc.

-

Parker Hannifin Corporation

-

Bio-Rad Laboratories, Inc.

-

Meissner Filtration Products, Inc.

-

WuXi Biologics

-

Entegris, Inc.

-

Cobetter Filtration Equipment Co., Ltd.

-

Novasep Holding SAS

-

Agilent Technologies, Inc.

-

Eurofins Scientific SE

-

Clean Harbors, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.71 Billion |

| Market Size by 2035 | USD 10.15 Billion |

| CAGR | CAGR of 18.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Consumables [Kits and Reagents, Others], Instruments [Filtration Systems, Chromatography Systems], Services) • by Technology (Filtration, Chromatography) • by Application (Biologicals, Medical Devices, Water Purification, Air Purification) • by End-Use (Biopharmaceutical & Biotechnology Companies, Contract Research Organizations, Medical Device Companies, Academic Institutes & Research Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Merck KGaA, Sartorius AG, Cytiva, Pall Corporation, Thermo Fisher Scientific Inc., Asahi Kasei Medical Co., Ltd., Charles River Laboratories International, Inc., Lonza Group AG, Repligen Corporation, 3M Purification Inc., Parker Hannifin Corporation, Bio-Rad Laboratories, Inc., Meissner Filtration Products, Inc., WuXi Biologics, Entegris, Inc., Cobetter Filtration Equipment Co., Ltd., Novasep Holding SAS, Agilent Technologies, Inc., Eurofins Scientific SE, Clean Harbors, Inc. |

Frequently Asked Questions

North America dominated the Virus Filtration Market in 2025 with more than 42.21% market share, while Asia Pacific is the fastest-growing region.

The Virus Filtration Market is expected to grow at a CAGR of 10.15% from 2026 to 2035.

The Virus Filtration Market was valued at USD 5.71 Billion in 2025.

Rising biologics production combined with strict regulatory requirements for viral safety validation across biopharmaceutical manufacturing.

Get in Touch