Water Pump Market Report Scope & Overview:

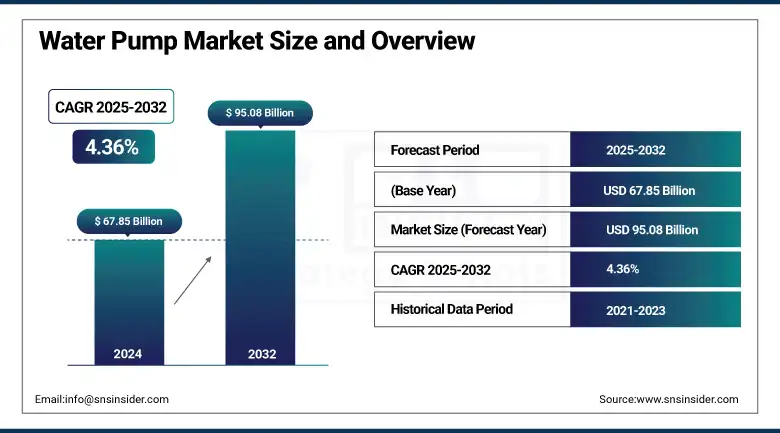

The water pump market size was valued at USD 67.85 billion in 2024 and is expected to reach USD 95.08 billion by 2032, growing at a CAGR of 4.36% over the forecast period of 2025-2032.

The global water pump market growth is driven by the demand for efficient water management systems across the agriculture, industrial, and municipal sectors. Trends are determined largely through technological advancements, increasing urbanization, and infrastructure development. The report further provides a thorough Water Pump Market Analysis of this business sphere, alongside emerging opportunities, competitive landscape, and innovations around energy-efficient and sustainable water solutions.

To Get more information On Water Pump Market - Request Free Sample Report

“For instance, in February 2024, KSB is adding high-efficiency water pumps to its portfolio, improving performance in water supply and pressure boosting applications for municipal and industrial customers.”

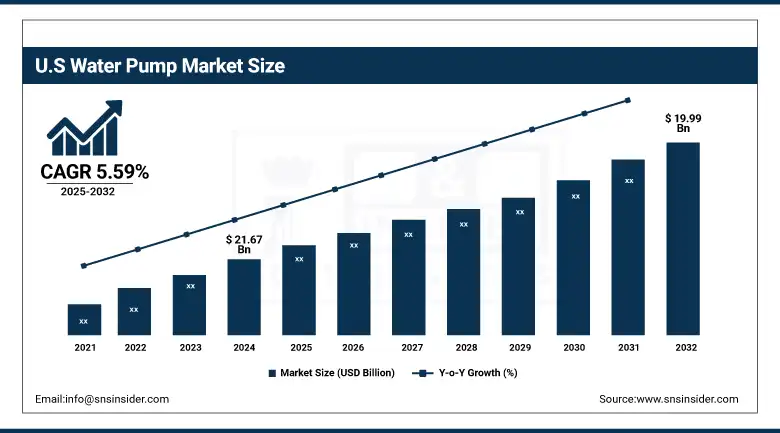

The U.S. water pump market size was valued at USD 21.67 billion in 2024 and is expected to reach USD 19.99 billion by 2032, growing at a CAGR of 5.59% over the forecast period of 2025-2032.

The trends in the U.S. water pump market signify an increasing implementation of energy-efficient and smart pump systems in agriculture, construction, and municipal sectors. The increasing demand, owing to rising infrastructure upgrades, concerns over water procession and sustainability, promulgating green building mandates are prompting key companies to engage in innovation to come up with effective water pumps solutions.

Water Pump Market Dynamics:

Drivers:

-

Increasing Adoption of Smart Irrigation Systems and Infrastructure Modernization Drives the Water Pump Market Growth

Smart irrigation technologies are expected to be integrated into agriculture, along with modernization plans of municipal infrastructure that are playing an important role in driving the growth of the market. Efficient water management systems are being pursued by governments globally, particularly in developing regions, which are expected to drive the demand for water pumps. Electric water pumps provide energy efficiency, high reliability, and low maintenance costs, which is driving the popularity of electric water pumps in the market. These developments are in line with the water pump market trends that are obtained through the help of stages of sustainable water use. The growing trend provides high scope for water pump companies to expand their portfolio and exploit developing Technology.

“In March 2025, Flowserve introduces next-generation energy-efficient and high-performance water pumps for municipal and industrial applications to support clean water needs and sustainability targets globally.”

-

Rising Industrialization and Demand for High-Efficiency Pumping Solutions Accelerate the Centrifugal Water Pump Industry

Increased industrialization within various sectors, comprising manufacturing, mining, and construction, has propelled the demand for effective water handling systems. As this demand boom occurs, the centrifugal water pump industry profits also benefit, due to rising demand for quality solutions that can handle different flow rates and types of brittle fluid. This is especially the case in areas with growing industrial landscapes and water-dependent uses. The clean water delivery systems are also being upgraded, adding centrifugal pumps for operational sustainability and reliability. Considering the trends of global industrial pumps usage, the continued technological innovations and cost-effective pumping solutions will be the foundation for ongoing adoption, as revealed by the water pump market analysis.

Restraints:

-

High Operational and Maintenance Costs of Advanced Pumping Systems May Hinder Market Expansion in Developing Regions

Even with new advancements in technology that allow for lower power water pumping systems, the cost of development and then ongoing systems are still high, putting a barrier to entry for large-scale plants in price-sensitive markets. In developing countries where the budgets are tight and there is not much technical infrastructure, deployment of complex solutions usually takes a long time. This hinders penetration in the market and slows down the general adoption. In addition, skilled manpower required for the operations and maintenance of these systems is not always available easily. Together, these drivers affect the overall market growth, and while there is a push for modernization and sustainability on the global stage, it proves difficult for water pump companies to penetrate new and emerging economies.

Water Pump Market Segmentation Outlook:

By Type

In 2024, the Centrifugal Pumps segment generated the highest revenue share of approximately 65.22% in the water pump market as they are simple and efficient, and they can manage high flow rates, which makes them the most preferred kind of pumps in residential, agricultural, and municipal sectors. Since centrifugal pumps are indispensable components of clean water delivery systems and they provide constant water flow at lower operational costs. In addition, water pump companies have more rapidly optimized centrifugal pumps in response to growing demands for sustainable and cost-effective pumping technologies.

The positive displacement pumps segment is expected to grow at a considerable CAGR of nearly 4.27% over 2025–2032. The slip ring market is benefiting from expanded demand in applications that revolve around dealing with viscous, abrasive, or chemically reactive fluids, such as the pharmaceuticals, oil & gas sectors. But it also includes pumps designed to achieve precise flow control irrespective of pressure differences, which are vital in complex systems. The typology is moving toward electric water pumps as a result of technological advancements and the desire for high-functioning solutions in niche applications.

By Business

The pumps segment accounted for the largest revenue share, being 59% in 2024 as water pumps find extensive applications in major end-use industries such as agriculture, residential, and utilities. The companies in the water pumps market are pushing for the development of variations of electric water pumps for improved efficiency, reliability, and sustainability. In addition to proving that they dominate the market with the fact that they can easily be directly used in the clean water delivery systems, which will lend itself to their domination in markets in North America that are facing water shortages or markets needing irrigation solutions, or even wastewater management solutions.

The aftermarket segment is expected to experience rapidly expanding growth from 2025–2032. This growth is supported by the expanding installation base of water pumps, which creates demand for maintenance, parts replacements, and upgrades as they age. With aging systems, efficiency decreases while the need for retrofit solutions increases. End users are focusing on operational continuity and energy savings, leading to growth in the aftermarket as per a water pumps market analysis. Increasing environmental regulations will drive the demand for sustainable electric water pumps, which in turn will spur aftermarket services.

By Distribution Channel

Direct sales generated the most revenue in 2024. With this channel, water pump companies can sell customized solutions, exercise better price control, and provide timely technical support. Project-specific electric water pump delivery creates a solid customer base, brand value, and loyalty. In particular, clean water delivery systems projects require a high level of technical accuracy and need on-the-spot guidance to ensure the success of the project and the sustained, reliable performance over time.

Distributor sales segment to grow fastest by 2025–2032. The growing demand for water pumps in rural and emerging markets has helped the water pumps to grow. With the growing infrastructure development in remote and rural areas, localized distribution networks enable greater product availability and faster delivery, as suggested by water pump market trends. Distributors, similarly, provide local education, increasing adoption rates. Distributor partnerships will be essential for water pump companies to reach the underserved regions of the globe where they are expanding.

By End-Use

As of 2024, the largest revenue share of the water pump market was held by the agriculture sector. This dominance is mainly attributed to the importance of water pumps to irrigation and drainage systems. As the world is increasingly emphasising food security along with water conservation, farmers are now leaning towards Electric water pumps for optimum water usage. Water pump companies have started catering to this segment by providing high-durable, energy-efficient, clean water/drought delivery systems, which are getting more attention, especially in water-stressed areas.

The Industrial vertical is anticipated to register a healthy CAGR over 2025-2032. The reason for this growth is attributed to the increasing demand for water in the manufacturing, energy, and chemical processing sectors. Increasing industrial infrastructure development across the globe, especially in the Asia Pacific and North America region, is anticipated to boost the demand for its manufacturing sector. The water pump market analysis shows that electric water pumps are increasingly adopted, especially automated and smart electric water pumps, which help in increasing the efficiency of the process and minimizing the downtime. As industries turn towards more sustainable operational models, the need for efficient pumping systems will continue to grow steadily.

Water Pump Market Regional Analysis:

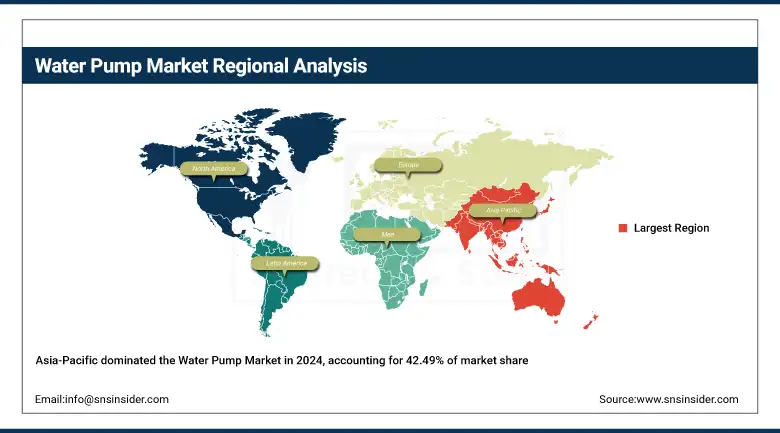

The Asia Pacific water pump market accounted for the largest revenue share, approximately 42.49%, which can be attributed to the rapid urbanization, growth in cultivation, and large-scale infrastructure development in countries including China, India, and the regional nations of Southeast Asia. Pump ownership and adoption have rapidly increased since the Indian government launched local-level groundwater governance initiatives linking water conservation with irrigation planning. Moreover, the high availability of essential water pump companies and increased demand for clean water delivery systems and electric water pumps from residential and industrial end-users are further factors enabling the region to retain its leading position in the global water pumps market.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is expected to register a relatively steady CAGR of approximately 5.95%, owing to the growing investments in the refurbishment of aged water infrastructure, surging industrial activities across the region, and a growing focus on energy-efficient technologies. High focus on sustainable solutions has propelled the growth of advanced electric water pumps in the region. North America is experiencing a similar upward trend, with a growing inclination toward automation and smart pumping systems, along with government regulations on clean water access and improved industrial efficiency.

Rising demand for energy-efficient solutions & sustainable clean water delivery systems is fuelling the growth of the European water pump market. The region itself is led by none other than Germany, thanks to its sophisticated industrial plant. For instance, one of the inventions is the Electric water pumps, which are smart and use the IOT to connect and monitor performance remotely, providing a quick solution to improve operational efficiency in municipal and industrial applications.

Key Players in Water Pump Market are:

The major companies operating in the market are KSB SE & Co. KGaA, Flowserve, ITT Inc., Gorman-Rupp, Pentair, Xylem, WILO SE, Grundfos, EBARA CORPORATION, ANDRITZ AG.

Recent Developments:

-

July 2024 - Grundfos launched an innovative solar-powered water ATM solution in India, providing clean drinking water through smart dispensing technology to underserved communities, supporting sustainability and improving access to safe water.

-

January 2025 - Pentair was honored for innovation by the Business Intelligence Group, recognizing its advanced water solutions and commitment to sustainability in the water pump market.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 67.85 Billion |

| Market Size by 2032 | USD 95.08 Billion |

| CAGR | CAGR of 4.36% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Centrifugal Pumps, Positive Displacement Pumps) • By Business (Pumps, Aftermarket [Parts & Components, Repair & Maintenance]) • By Distribution Channel (Direct Sales, Distributor Sales, Online Sales & E-Commerce) • By End Use (Municipal, Construction, Agriculture, Mining, Oil & Gas, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | KSB SE & Co. KGaA, Flowserve, ITT Inc., Gorman-Rupp, Pentair, Xylem, WILO SE, Grundfos, EBARA CORPORATION, ANDRITZ AG |

Frequently Asked Questions

Ans: Asia-Pacific dominated the Water Pump Market in 2024.

Ans: The Centrifugal Pumps segment dominated the Water Pump Market.

Ans: The major growth factor of the Water Pump Market is the increasing demand for energy-efficient and sustainable water management solutions across agriculture, industry, and urban infrastructure.

Ans: The Water Pump Market size was USD 67.85 billion in 2024 and is expected to reach USD 95.08 billion by 2032.

Ans: The Water Pump Market is expected to grow at a CAGR of 4.36% from 2025-2032.

Get in Touch