Wearable AI Market Report Scope & Overview:

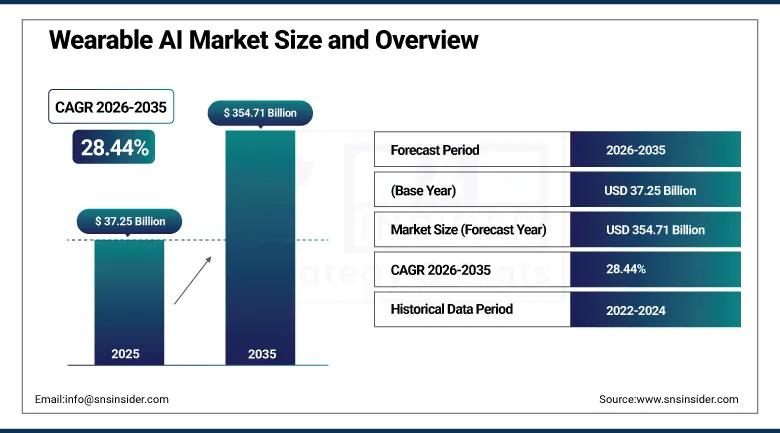

The Wearable AI Market was valued at USD 37.25 Billion in 2025 and is expected to reach USD 354.71 Billion by 2035, growing at a CAGR of 28.44% from 2026 to 2035.

AI in Wearable Devices: AI based health monitoring capabilities especially those that measure heart rate, SpO2 and sleep, are more in use in North America and Europe, although there is also a fast-developing market in Asia Pacific. Voice activation features in wearables such as smartwatches and earbuds are gaining traction because of natural language processing technologies advances. The report will introduce you to the trends in emotion detection using AI, gesture control technologies and AI assistants integration into next generation of wearables.

In September 2024, Apple introduced the Apple Watch Series 10 with new depth and water temperature sensors, enhancing its suitability for water activities and extending AI powered health monitoring capability to new underwater sports and recreational swimming use cases. The product launch demonstrates Apple's continued investment in expanding the application scope of wearable health monitoring sensors, where each new sensor modality creates additional data collection capability that supports more comprehensive AI powered health insight delivery to consumers.

Market Size and Forecast

-

Market Size in 2026E: USD 47.84 Billion

-

Market Size by 2035: USD 354.71 Billion

-

CAGR: 28.44% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Wearable AI Market - Request Free Sample Report

Wearable AI Market Trends

-

AI-powered health monitoring capabilities, including ECG, blood oxygen measurement, sleep analysis, and personalized wellness insights, are accelerating adoption of wearable AI devices.

-

Smart earwear with AI-enabled voice assistants, real-time language translation, and biometric sensing is expanding beyond audio applications into everyday productivity and health monitoring.

-

Generative AI integration, gesture recognition, and emotion detection technologies are enhancing user interaction and enabling more intelligent, context-aware wearable experiences.

-

Enterprise adoption of wearable AI is increasing for workforce safety, hands-free communication, productivity enhancement, and industrial monitoring applications.

-

Smart rings and smart patches are emerging as high-growth wearable AI categories, offering discreet continuous health monitoring and advanced sensor-based analytics.

The U.S. Wearable AI Market Outlook

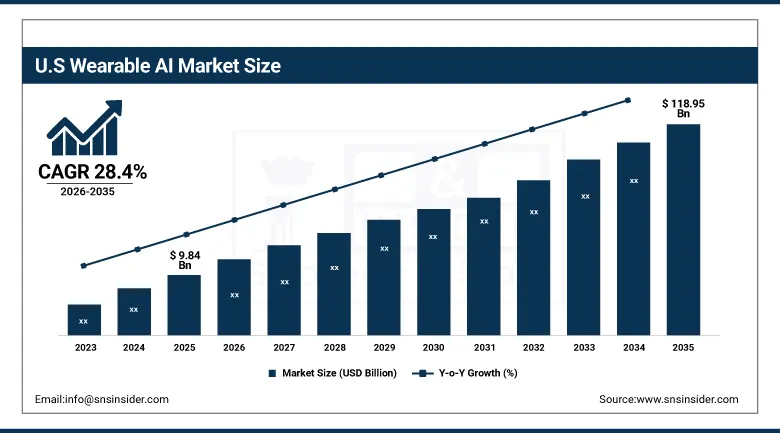

The U.S. Wearable AI Market was valued at approximately USD 9.84 Billion in 2025 and is expected to reach approximately USD 118.95 Billion by 2035, growing at a CAGR of approximately 28.4% during the forecast period.

The U.S. Wearable AI Market is among the biggest in the country due to the presence of leading wearable AI players such as Apple, Google, and Fitbit, high tech penetration rate among consumers, and increased health awareness among consumers. The area will be aided by good connectivity infrastructure, increased use of AI in healthcare gadgets, and increased adoption by enterprises for productivity and health tracking purposes. The huge investments being made by the US government in AI infrastructure as seen through the CHIPS and Science Act has strengthened semiconductor production for better AI processor inclusion in wearables.

Meta collaborated with Oakley in 2024 to launch the Oakley Meta HSTN smart glasses featuring hands-free 4K camera, open ear audio, water resistance, and built-in Meta AI functionalities. The collaboration shows the growing commercial ecosystem that is forming in relation to AI enabled smart glasses. This occurs through a combination of consumer lifestyle product collaborations and AI platform functionality to create high-end wearables that can be used for photography, communication, and AI assistance purposes.

Wearable AI Market Segment Analysis

-

By Product Type, the smartwatches & fitness bands segment led the wearable ai market and held approximately 32.0% revenue share in 2025, while the smart earwear segment is projected to register the fastest CAGR from 2026 to 2035.

-

By Component, the Sensors segment dominated the Wearable AI Market and accounted for approximately 41.6% revenue share in 2025, while the processor segment is projected to register the fastest CAGR from 2026 to 2035.

-

By Operations, the cloud-based ai segment dominated the wearable ai market and accounted for approximately 57.8% revenue share in 2025, while the on-device ai segment is projected to register the fastest CAGR from 2026 to 2035.

-

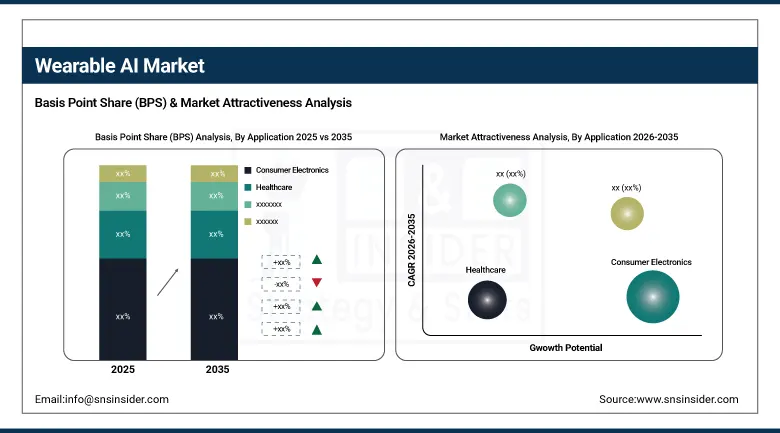

By Application, the consumer electronics segment dominated the wearable ai market and accounted for approximately 39.0% revenue share in 2025, while the healthcare segment is projected to register the fastest CAGR from 2026 to 2035.

By Product Type, smartwatches and fitness bands dominate, smart earwear grows fastest

Fitness trackers and smartwatches were the pioneers in the field of wearable AI devices and had a market revenue share of 32% in 2025, as a result of their wide range of functionalities in areas of health monitoring, communication, and notifications powered by AI. The increasing level of health consciousness among consumers, fitness fad, and regular upgrades such as ECG, blood oxygen monitoring, and AI-powered workout sessions helped to retain the leadership of the segment in the market. Their integration with voice assistants and app ecosystem further enhanced their market demand. Every active individual who seeks to buy a smartwatch in order to achieve fitness goals or monitor their health helps the segment to dominate in the market.

Smart earwear is projected to register the fastest CAGR from 2026 to 2035, fueled by surging consumer interest in AI enabled voice assistants, real time language translation, and immersive audio experiences. Rapid growth is being fueled by increased demand for hands-free calling capabilities, AI-enabled health tracking using biosensors, and compatibility with other wellness and productivity applications. Every individual who generates demand for hands-free access to an AI assistant increases smart earwear sales, which build on top of the real-time translation use case that allows cross-language communications in both consumer and enterprise settings.

By Application, consumer electronics dominates, healthcare grows fastest

Consumer electronics dominated the wearable AI market and accounted for 39% of revenue share in 2025, driven by the growing adoption of AI enabled smartwatches, earwear, and fitness bands for personal health, entertainment, and communication. Growing number of smartphones, need for lifestyle gadgets, and integration of artificial intelligence-based voice assistants gave an extra edge to their market supremacy. Growing health consciousness among consumers and preference for wearable technology has made it mandatory to have AI-powered wearables in daily tech environment. Innovation in products and compatibility with mobile environments maintain their dominant market share.

Healthcare is projected to register the fastest CAGR from 2026 to 2035, driven by increasing demand for AI enabled health monitoring and diagnostics through wearable devices. The expansion of remote patient monitoring, telehealth integration, and chronic disease management applications creates structured healthcare channel procurement whose clinical validation requirements and regulatory approval processes create barriers that sustain premium pricing for medical grade wearable AI devices. Each healthcare system deployment of wearable AI for continuous patient monitoring creates procurement that compounds with the broader shift toward proactive, data driven health management.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Wearable AI Market Insights

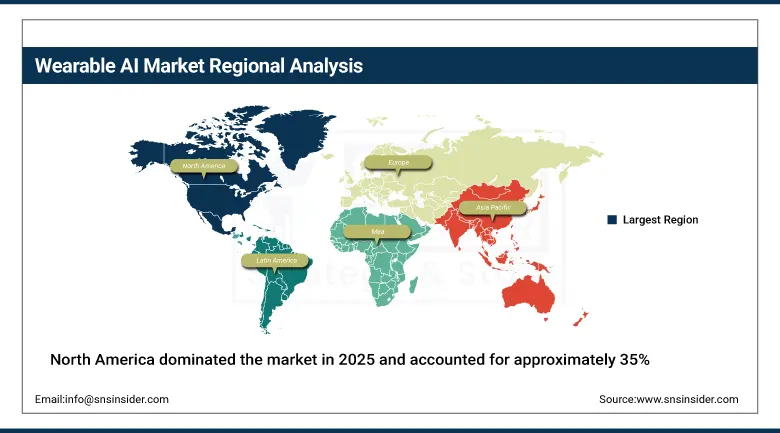

North America dominated the market in 2025 and accounted for approximately 35% of revenue share in 2025. This is driven by high consumer tech adoption rates, strong presence of major wearable AI brands such as Apple, Google, and Fitbit, and growing health-conscious consumer behavior. The region also benefits from the advanced connectivity infrastructure, rising AI integration in healthcare devices, and an increasing enterprise adoption for productivity and wellness monitoring.

The United States accounts for approximately 87.4% of North American revenues through these dominant technology companies.

Canada contributes complementary North American revenue through its growing consumer wearable technology adoption and expanding enterprise health and safety monitoring wearable deployment across industrial and healthcare sectors.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Wearable AI Market Insights

Europe is a technically sophisticated wearable AI market where GDPR data protection compliance requirements and growing health technology investment create structured institutional demand.

Germany accounts for approximately 22.3% of European revenues through its strong consumer electronics market and growing digital health technology adoption across the country's healthcare and industrial sectors.

The United Kingdom and France are significant secondary markets where strong digital health infrastructure and growing enterprise wearable technology adoption create consistent procurement. Major global wearable technology brands maintain substantial European commercial operations sustaining regional market development.

Asia Pacific Wearable AI Market Insights

The Asia Pacific region is expected to register the fastest CAGR of approximately 28.4% during 2026–2035 in the wearable AI market. This surge is fueled by a rapidly growing middle class, booming smartphone and wearable device penetration, increasing fitness awareness, and strong investments in AI driven consumer electronics across China, India, Japan, and South Korea. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary consumer electronics manufacturing base and rapidly growing domestic wearable technology consumer market.

India represents the most commercially dynamic emerging market within Asia Pacific where government national digital transformation initiatives and growing health awareness are creating above average regional adoption growth for wearable AI devices, with local as well as global players focusing on these emerging markets through affordable device offerings tailored for price sensitive consumers.

MEA & Latin America Wearable AI Market Insights

The UAE leads MEA revenues through its growing technology adoption and expanding healthcare digitalization investment supporting wearable AI device adoption across both consumer and clinical settings and enterprise wellness monitoring programs. Saudi Arabia's Vision 2030 digital economy program adds substantial complementary regional demand across multiple verticals.

Brazil tops Latin American revenues with an increase in consumer electronics sales and the use of health technologies by the urban middle-class population in Brazil. Mexico’s growing penetration in smartphones and Argentina’s rise in technological innovation keep the regional markets growing up to 2035.

Market Dynamics

Growth Drivers: AI-powered health monitoring demand and ecosystem integration

Growing consumer focus on health and wellness, combined with advancements in AI powered health monitoring features, is significantly driving the wearable AI market. Advanced features that have been incorporated in smartwatches and other wearable devices include electrocardiograms (ECG), monitoring of blood oxygen levels, stress measurement, and AI-powered personalized coaching. Wearable technology is increasingly being used by consumers for health purposes. Thanks to AI, the devices can predict certain outcomes, thus making them essential in health practices.

The expanding AI applications in healthcare wearables for remote monitoring and chronic disease management offer major growth potential. This rising adoption across fitness enthusiasts and health-conscious users globally is creating robust demand for innovative, AI driven wearable devices. Each patient whose chronic condition management is supported by continuous AI powered monitoring creates structured healthcare procurement that complements the consumer market demand.

Restraints: Data privacy concerns and high device costs

Privacy and security issues continue to be a major barrier towards the complete utilization of wearable AI technology. This is because the wearable devices keep collecting sensitive data such as health, location, and activities of the users, and in case of mismanagement, privacy infringement may occur. The complicated nature of the algorithms used in the process of AI and cloud computing only heightens the danger of being hacked.

The high cost of advanced wearable AI devices poses a challenge to market penetration, particularly in price sensitive regions. AI technology requires efficient processors, good-quality sensors, and advanced software applications, increasing costs in manufacturing and selling these products. In addition to that, AI-powered analytics and constant health tracking consume a lot of energy from the battery very quickly, reducing the usability of devices and requiring frequent charging.

Opportunities: Healthcare remote monitoring expansion and enterprise adoption

An expansion of uses for AI in health wearables through remote monitoring and chronic condition management has tremendous potential growth, with healthcare providers coming to realize the benefits that continuous biometric data collection can provide. Wearable AI technology allows for early detection of diseases, personalized treatment, and less need for hospital visits when managing chronic conditions, thus making this clinical adoption sustainable, ensuring the premium purchase of wearable AI products.

Integration of wearable AI into enterprise environments for worker safety monitoring, productivity enhancement, and hands-free communication creates additional commercial opportunity beyond the consumer market. Industrial applications, healthcare worker monitoring, and military and defense deployments collectively represent structured B2B procurement channels whose technical specifications and regulatory requirements create premium market opportunities distinct from consumer-oriented product categories.

Recent Developments:

-

2026: Apple Inc. expanded its AI-powered wearable ecosystem by introducing enhanced on-device health intelligence and personalized wellness features across its latest smartwatch portfolio.

-

2026: Samsung Electronics Co., Ltd. launched next-generation Galaxy wearable devices with advanced Galaxy AI capabilities, enabling improved health monitoring, sleep analysis, and real-time fitness coaching.

-

2026: Meta Platforms, Inc. expanded its AI-enabled smart glasses portfolio with enhanced multimodal AI assistant features, supporting real-time translation, visual recognition, and hands-free interaction.

-

2026: Qualcomm Incorporated introduced a new generation of Snapdragon wearable platforms featuring on-device generative AI processing, improved power efficiency, and advanced connectivity for next-generation AI wearables.

Wearable AI Market key players are:

-

Apple Inc.

-

Samsung Electronics Co., Ltd.

-

Alphabet Inc. (Google/Fitbit)

-

Meta Platforms, Inc.

-

Garmin Ltd.

-

Oura Health Oy

-

Amazfit (Zepp Health)

-

Huawei Technologies Co., Ltd.

-

Xiaomi Corporation

-

WHOOP Inc.

-

Withings SA

-

Fossil Group, Inc.

-

Jabra (GN Audio A/S)

-

Sony Group Corporation

-

Microsoft Corporation

-

Qualcomm Incorporated

-

Snap Inc.

-

Vuzix Corporation

-

RayNeo (TCL Electronics)

-

RealWear, Inc.

Wearable AI Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.25 Billion |

| Market Size by 2035 | USD 354.71 Billion |

| CAGR | CAGR of 28.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Smartwatches & Fitness Bands, Smart Eyewear, Smart Earwear, Smart Clothing, Others) • By Component (Processor, Connectivity IC, Sensors) • By Operations (On-Device AI, Cloud-based AI) • By Application (Consumer Electronics, Healthcare, Automotive, Military and Defense, Media and Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Apple Inc., Samsung Electronics Co., Ltd., Alphabet Inc. (Google/Fitbit), Meta Platforms, Inc., Garmin Ltd., Oura Health Oy, Amazfit (Zepp Health), Huawei Technologies Co., Ltd., Xiaomi Corporation, WHOOP Inc., Withings SA, Fossil Group, Inc., Jabra (GN Audio A/S), Sony Group Corporation, Microsoft Corporation, Qualcomm Incorporated, Snap Inc., Vuzix Corporation, RayNeo (TCL Electronics), RealWear, Inc. |

Frequently Asked Questions

Rising consumer demand for AI powered health and fitness monitoring fueling rapid adoption of wearable AI devices.

The Market was valued at USD 37.25 Billion in 2025.

The Market is expected to grow at a CAGR of 28.44% from 2026 to 2035.

North America dominated the Wearable AI Market with 35% of revenue share in 2025.

Smartwatches and Fitness Bands dominated the Wearable AI Market with a 32% revenue share in 2025.

Get in Touch