Wind Turbine Pitch and Yaw Drive Market Report Scope & Overview:

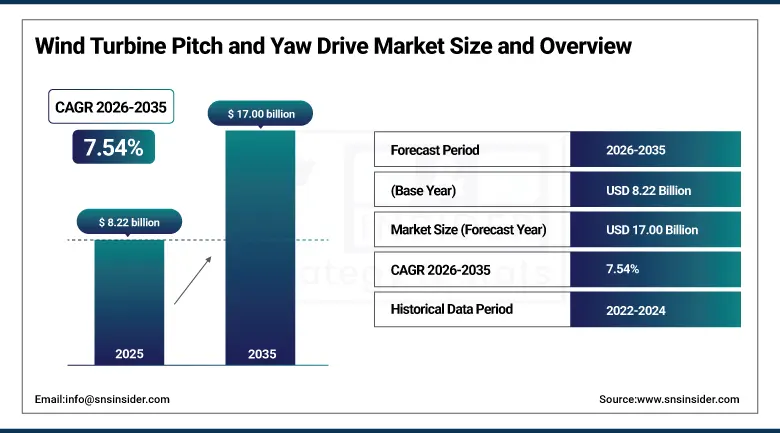

The Wind Turbine Pitch and Yaw Drive Market was valued at USD 8.22 billion in 2025 and is expected to reach USD 17.00 billion by 2035, growing at a CAGR of 7.54% from 2026–2035.

The wind turbine pitch and yaw drive market is undergoing a transformative growth phase, going through a phenomenal growth stage amidst the global energy transition from fossil fuel-based sources of power to renewable ones Pitch and yaw drive systems are essential electromechanical parts of contemporary wind turbines, pitch drives precisely adapt blade angles with respect to incoming wind direction to maximize energy conversion or withstand extreme loads whilst yaw drives orient a turbine nacelle with respect the incoming winds so as to optimize rotor action. The design features pitch and yaw drive systems, which require mechanical and electronic capabilities that are pushed to utmost limits as wind turbine sizes grow larger, more powerful and in harsher offshore environments, accelerating innovations in drive design, materials science, sensor integration and predictive maintenance algorithms.

Multi-decade tailwinds across every major geography driven by the global energy sector's commitment to net-zero targets and regulatory framing around deals like the EU Green Deal, U.S. Inflation Reduction Act and China's Dual Carbon Policy as well as sustainable demand for advanced pitch and yaw drive systems for both onshore and offshore wind turbine installations.

As the world installs progressively larger, more powerful wind turbines in increasingly demanding offshore environments, the pitch and yaw drive systems responsible for optimising every megawatt-hour of energy generation become correspondingly more sophisticated, more mission-critical, and more valuable, creating a compounding technology upgrade cycle that sustains premium revenue growth for leading drive system manufacturers through the entire forecast horizon.

Market Size and Forecast

-

Market Size in 2025: USD 8.22 Billion

-

Market Size by 2035: USD 17.00 Billion

-

CAGR: 7.54% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Wind Turbine Pitch and Yaw Drive Market - Request Free Sample Report

Wind Turbine Pitch and Yaw Drive Market Trends

-

Accelerating global shift toward electric pitch and yaw drive systems over hydraulic and mechanical alternatives, driven by superior efficiency, lower maintenance costs, faster response times, and compatibility with digital turbine control architectures.

-

Rising deployment of offshore wind farms — particularly in Europe, China, and the U.S. East Coast — demanding more robust, high-torque, corrosion-resistant pitch and yaw drives capable of operating reliably in marine environments.Integration of IoT sensors, edge computing, and AI-based predictive maintenance algorithms into pitch and yaw drive systems, enabling real-time condition monitoring, early fault detection, and significant reductions in unplanned downtime.

-

•Rapid growth in wind turbine capacity ratings — with next-generation offshore turbines exceeding 15–20 MW — requiring proportionally more powerful pitch and yaw drive systems and driving significant technology advancement cycles.

-

Increasing focus on turbine repowering and component retrofitting programmes across aging onshore wind fleets in Europe and North America, creating substantial aftermarket demand for upgraded pitch and yaw drive systems.

-

Adoption of direct-drive turbine architectures and permanent magnet generators is reshaping pitch drive requirements, encouraging manufacturers to develop more compact, lightweight, and efficient drive solutions.

-

Growing use of composite materials, advanced lubrication systems, and modular drive designs to reduce weight, enhance reliability, and lower total cost of ownership across both onshore and offshore turbine platforms.

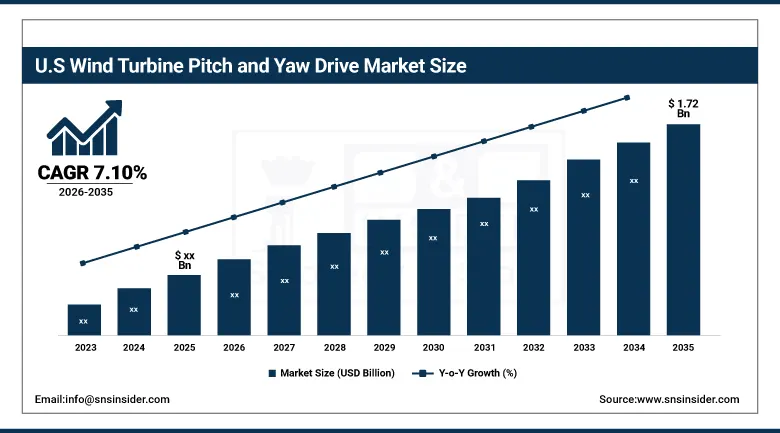

U.S. Wind Turbine Pitch and Yaw Drive Market is expected to reach USD 1.72 billion by 2035, registering a CAGR of 7.10% during 2026–2035.

The North American wind turbine pitch and yaw drive market is led by the U.S., fueled by aggressive federal and state renewable energy targets, an established onshore wind turbine fleet needing component upgrades and repowering investment due to aging turbines, as well as burgeoning offshore wind project backlogs across the Atlantic Seaboard and in the Gulf of Mexico. The production-based tax credits and investment tax credits from the Inflation Reduction Act are driving historical investments in wind energy due to robust policy backing, while government-sponsored grid-modernization programs are increasing demand for advanced pitch and yaw drive assemblages of turbines with newer and more sophisticated control systems. Fairly established by-wind-energy states Texas, Iowa, Oklahoma, Kansas and California persist to grow next-installed capacity even as new markets along with New York, New Jersey, Massachusetts along with Virginia are rising main offshore trend development centers alongside high-performance ability results able of meeting bottom-high-quality performance career setting conditions..

The April 2025 agreement between GE Vernova, a General Electric company, and BBWind to supply 6.0 MW onshore wind turbines for community wind projects in Germany The twentieth BBWind partnership of GE Vernova exemplifies our growth rate regarding the need for technology-intensive turbines which are relying on sophisticated pitch and yaw drive systems that maximise energy yield in complicated wind resource environments, while at the same time–the parallel expansion of thenegligible offshore wind programme fromGE Vernova in U.S.shows us the growing premium revenue opportunity over emerging and established countries addressing next-generation drive systems across the windshedding communities.

Wind Turbine Pitch and Yaw Drive Market Segment Insights

-

Based on Type, >3000 W accounted for the largest market share (67.2%) in 2025; 1000 W–3000 W expected to be the fastest-growing segment (CAGR).

-

Based on Pitch System, Electric accounted for the largest market share (57.4%) in 2025; Electric segment expected to maintain the fastest CAGR.Based on Pitch System,

-

Based on Size, Medium turbines accounted for the largest market share (46.6%) in 2025; Large turbines expected to be the fastest-growing segment (CAGR).

-

Based on End Use, Onshore accounted for the largest market share (71.5%) in 2025; Offshore expected to be the fastest-growing end-use segment (CAGR).Based on End Use,

Wind Turbine Pitch and Yaw Drive Market Segment Analysis

By Type: >3000 W dominates, 1000 W–3000 W expected to grow fastest

The >3000 W segment dominated the Global Wind Turbine Pitch and Yaw Drive Market in 2025, commanding approximately 67.2% of total market revenue. This commanding market position reflects towards high-capacity wind turbines, particularly multi-megawatt offshore platforms where proportionally strong pitch and yaw drive systems are essential to manage the vast aerodynamic forces which are applied to progressively larger rotor blades. It is also worth noting that the technical requirements for turbine drive systems operating at greater than 3,000 W of rated power are much more stringent. These large torque ratings requiring advanced thermal management and structural durability and integrated digital control systems make such high-capacity drive systems inherently costlier in dollar terms, as well as contributing greater revenue per unit when compared to their smaller-capacity counterparts. With the latest generations of turbines demanding increasingly sophisticated pitch and yaw drive assemblies, leading manufacturers of large-capacity turbines such as Siemens Gamesa, Vestas, GE Renewable Energy, and Dongfang Electric are specifying the advanced systems required to power them.

The 1000 W–3000 W segment is projected to record the highest CAGR during 2026–2035, owing to increasing demand for economic medium-capacity wind turbines which are ideal for economical onshore wind development in developing markets in Asia Pacific, Latin America, and the Middle East and Africa. With governments in these regions implementing more aggressive renewable energy targets and local supply chains for wind energy technology, medium-size machines are the sweet-spot between power output, installation cost and technical complexity by generating continuing demand growth of the pitch-to-yaw drive systems that form the basis of their capabilities. While the expansion of distributed wind energy projects and community wind schemes in established markets is further supporting the growth trend for medium-capacity segment through the forecast period.

By Pitch System: Electric dominates and grows fastest

Electric pitch and yaw drive systems dominated the market with a 57.4% revenue share in 2025 and are simultaneously projected to achieve the highest CAGR from 2026 to 2035, driven by a decisive technology transition within the wind turbine drive system industry. Electric systems have clear operational advantages over hydraulic and mechanical alternatives — higher efficiency, far less maintenance (no hydraulic fluid management needed), faster and more accurate blade angle change response times, lower risk of contamination from hydraulic fluid leaks, fully compatible with state-of-the-art digital turbine controls and predictive maintenance platforms. Progressive electrification of turbine pitch systems is closely in line with industry trends towards digital, data-driven turbine operations allowing electric drive manufacturers to target an expanding premium market segment.

Hydraulic pitch systems, while facing increasing displacement by electric alternatives, retain meaningful market positions in specific applications — particularly large offshore turbines where their high torque density and proven reliability in extreme environmental conditions remain valuable. However, the long-term structural trend strongly favours continued electric system market share gains through the forecast period, supported by ongoing improvements in electric motor technology, battery backup systems for emergency pitch operations, and the declining cost premium of electric systems relative to hydraulic alternatives as production volumes scale.

By Size: Medium turbines dominate, Large turbines accelerate fastest

Medium-sized wind turbines commanded the largest share of the Wind Turbine Pitch and Yaw Drive Market in 2025, contributing approximately 46.6% of global revenues. The segment's dominance illustrates the proliferation of 2–5 MW capacity class turbines the workhorses of the global onshore wind market in mature and developing markets worldwide, where these medium-capacity platforms provide the best cost-effective balance between energy production, installed price per kW, and logistical manageability. Medium turbines, with established supply chains for components, proven turbine designs and large operational experience remain dominant in the utility-scale onshore wind space across Europe, North America and rising in AsiaPacific and Latin America.

Large wind turbines are projected to record the highest CAGR during 2026–2035, due to continued scale up of turbine capacity ratings & speed in offshore wind worldwide. As offshore wind projects move further out into deeper waters and more energetically lucrative sites, turbine developers are increasingly offering larger rotor diameters (RD) and hub heights (HD) to optimize power output on next generation platforms routinely quantified with rated capacities of 12–20 MW. Such ultra-large turbines will naturally need relatively complex, high-torque pitch and yaw drive systems that can handle the unprecedented aerodynamic forces of rotors 200 metres in diameter or more which should provide lucrative revenue opportunities for drive system manufacturers sitting at the leading edge of technology within their sector.

By End Use: Onshore dominates, Offshore expected to grow fastest

Onshore wind energy retained the dominant position in the Wind Turbine Pitch and Yaw Drive Market in 2025, accounting for approximately 71.5% of total end-use revenues. The onshore segment's market leadership reflects its substantial installed base advantagethe global onshore wind fleet comprises the vast majority of all installed wind capacity —combined with the continued rapid expansion of new onshore projects, particularly across Asia Pacific, North America, and emerging markets with favourable wind resources and improving regulatory environments. Onshore wind benefits from significantly lower installation and infrastructure costs compared to offshore alternatives, making it the economically preferred option for many utility and independent power producers, thereby sustaining high volumes of pitch and yaw drive demand across the forecast period.

The offshore wind segment is projected to grow at the highest CAGR during 2026–2035, supported by a record high global pipeline of new offshore wind projects in European waters, the U.S. Atlantic coast and along China's coastal provinces, as well as developing markets in South Korea, Japan, India and Brazil. Value of offshore wind strong, more consistent wind resources lead to higher capacity factors and have comparatively few visual impact challenges; site large turbines and you'll not worry about road transport. Compared to onshore applications, the technical requirements of offshore environments directly impact the mechanical demands placed upon pitch and yaw drive systems including increased corrosion resistance, a higher level of sealing against marine ingress, longer maintenance intervals and greater structural reliability all adding up to an order-of-magnitude increase in revenue intensity per installed unit over onshore alternatives.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

35% |

|

Europe |

Germany |

37.7% |

|

Asia Pacific |

China |

46% |

|

Middle East & Africa |

UAE |

28% |

|

Latin America |

Brazil |

42% |

Europe Wind Turbine Pitch and Yaw Drive Market Insights

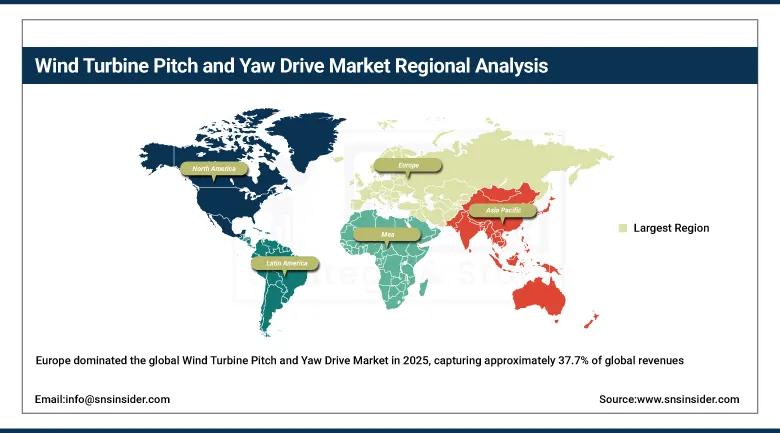

Europe dominated the global Wind Turbine Pitch and Yaw Drive Market in 2025, capturing approximately 37.7% of global revenues the highest regional share of any geography. Europe's market leadership is rooted in its decades-long commitment to wind energy development, its world-leading installed wind energy capacity, and the presence of the industry's most technologically advanced wind turbine manufacturers and component suppliers including Siemens Gamesa, Vestas, Nordex, Enercon, and Senvion. The European Union's ambitious renewable energy targets including a target of 42.5% renewable energy share by 2030 under REPowerEU are sustaining exceptionally high levels of wind turbine investment across the continent, while the rapid expansion of offshore wind capacity in the North Sea, Baltic Sea, and Atlantic Ocean is creating premium demand for the most advanced large-capacity pitch and yaw drive systems. Germany, Denmark, the United Kingdom, the Netherlands, and Spain represent the continent's largest individual wind energy markets, each characterised by extensive existing capacity requiring component upgrades and active new project pipelines.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Wind Turbine Pitch and Yaw Drive Market Insights

Asia Pacific is projected to record the highest regional CAGR of 8.4% during 2026–2035, representing an unprecedented level of wind energy expansion in China, India and Southeast Asia. Even a single country, China alone contained more than 400GW of installed capacity (largest wind market in the world) and maintains quasi-monopoly or market-leader status in Global markets sustained through its Dual Carbon targets comprising peak carbon emissions as early as before 2030 with set to achieve net-zero carbon neutrality by 2060. The government of India has set a goal of 500 GW of non-fossil fuel capacity by 2030 and this will come across many sectors, with wind energy contributing a sizeable and growing part as India becomes one of the major growth engines. Southeast Asia markets from Vietnam, the Philippines, and Indonesia are in earlier stages of wind development, but quickly accelerating growth driven by strengthening policy frameworks, cost-competitive turbine prices and high electricity demand growth. Asia Pacific's wind energy ambitions manifest on a scale that catalyzes exceptional long-duration demand from the world's most competitive manufacturing ecosystem for pitch and yaw drive systems.

North America Wind Turbine Pitch and Yaw Drive Market Insights

The Inflation Reduction Act's extension and enhancement of production and investment tax credits through the early 2030s providing never-before-seen policy certainty for wind energy investors which is already driving a multi-year wave of new onshore and offshore wind project development. The U.S. demand landscape is a diverse intermingling of demand drivers: utility-scale wind farm construction across the Great Plains and nascent offshore markets; repowering programs that augment the life and energy yield of existing onshore turbines in mature locations; and grid modernization investments incorporating sophisticated turbine control systems. Canada provides significant market volume through large wind resource and development programs in Ontario, Quebec, as well as potentially increasing interest in offshore wind potential developments particularly in the Atlantic Provinces.

Middle East & Africa and Latin America Wind Turbine Pitch and Yaw Drive Market Insights

The Middle East & Africa and Latin America regions are emerging as important growth markets for wind turbine pitch and yaw drive systems, driven by good wind resources, falling renewable energy costs and aggressive national clean energy programmes. As the demand for high performance turbine components including drive systems continues to expand, Saudi Arabia's NEOM and Vision 2030 projects are being developed as well as South Africa's REIPPP programme, an extensive wind energy development pipeline from Morocco. The UAE is the largest market for wind energy-related revenues in the region, accounting for almost 28% of total MEA revenues, benefiting from its position as a regional clean energy technology hub and ambitious targets for national energy diversification. In Latin America, Brazil represents around 42% of regional revenue, supported by one of the largest onshore wind energy markets in the world with over 27GW installed capacity and an active pipeline for new development across both Northeast and South regions. Chile, Argentina, Mexico and actually Colombia also are becoming large wind development markets with improving environment.

Market Growth Drivers:

Global renewable energy acceleration and offshore wind expansion creating sustained structural demand for advanced pitch and yaw drive systems: The most fundamental growth driver of the Wind Turbine Pitch and Yaw Drive Market is unprecedented global commitment to renewable energy deployment a fundamentally structural, policy-driven, and economics-driven transformation that is creating decades of increasing wind turbine installation demand. More than 90% of global GDP is covered by governments that have pledged to get to net-zero and wind power has been positioned, along with solar photovoltaics, as one of the two pillar technologies for the energy transition. Wind power continues to see year-on-year acceleration in added capacity globally with the Global Wind Energy Council showing over 680 GW of installations projected from just 2025–2028 alone, wherein each megawatt of installed windpower needing pitch and yaw drive systems for controlling blade angle as well as rotor facing, across a working lifespan often exceeding 25 years. The surge in offshore wind, with turbines larger (often previously untested), more technically advanced, and demanding a more complex and expensive drive system than onshore equivalents is fuelling growth of volume and value to market as offshore drive systems typically achieve substantially higher average selling prices than their land-based counterparts.

UKA has agreed to take up 80 Nordex turbines totaling 540 MW for 15 German projects with service contracts stretching over 20 years that highlights the compounding long-term revenue model around wind turbine drive system deployed in the modern mature markets where an initial components supply is followed by multiple decades worth of maintenance, monitoring and upgrade services to generate recurring revenue streams for manufacturers working at the system integration frontier of decarbonization.

Market Restraints

Supply chain constraints, raw material dependencies, and grid infrastructure bottlenecks limiting market growth velocity: Complex interaction of varying supply chain constraints, raw material price fluctuation risks and grid-related practical limitations are major threats for any wind energy project development timeline and component procurement cycle thereby limiting the potential as well as timing-based demand for Wind turbine pitch and yaw drive Market. Rare earth elements for permanent magnets in electric drives, high-grade steel for structural components and specialised bearings and gearbox assemblies are critical materials on which wind turbine drive systems depend heavily, each facing risks of concentration from supply and geopolitical trade tensions that create cost and availability volatility. In one switch, sizeable carry out delays due to grid connection backlogs in key global marketplaces which includes the UK, Germany and squeeze-producing access in the direction of program new turbines and attached pitch & yaw travel demand. In addition, the capital-intensive profile of offshore wind project development (since each individual project requires multi-billion-dollar capital investments and complex, multi-party financing structures) means that market activity is sensitive to interest rate environments, insurance costs, and availability of long-term power purchase agreements underpinning project economics.

Market Opportunities

Repowering programmes, predictive maintenance services, and emerging market wind energy development: The confluence of advanced digital drive system technologies and repowering programmes for ageing turbines presents perhaps the largest immediate market opportunity point in terms of years as well as potential value within the Wind Turbine Pitch & Yaw Drive Market framework. With tens of thousands of wind turbines across Europe and North America at or near the end of their original design lives (20-25 years), this represents a multi-billion dollar component replacement and performance upgrade programme. First-generation pitch and yaw drive systems were typically mechanical designs with limited digital connectivityModern pitch and yaw drive systems deliver significantly improved efficiency, reliability, and digital connectivity compared to first-generation drives from the ground up, providing strong economic cases for operators to retrofit outdated technology into existing turbines aimed at extending operational lifetimes along with improving energy yields while minimizing maintenance costs. As AI-driven predictive maintenance platforms are gaining traction, they are connecting with their respective drive systems allowing manufacturers to bundle up the initial equipment sales into recurring services revenue streams which will enhance predictability and deepen customer relationships. At the same time, large scale wind energy markets opening in India, Southeast Asia, Latin America, Middle East and Sub-Saharan Africa add significant greenfield growth opportunities for manufacturers whose drive solutions are competitively priced with locally adapted functions specified to meet emerging market applications based on local wind resource characteristics and project economics.

Recent Developments:

-

April 2025: GE Vernova and BBWind signed their 20th wind turbine supply agreement, committing three 6.0 MW turbines for community wind projects in North Rhine-Westphalia, Germany — demonstrating the continued scaling of turbine capacity in established European markets and the growing premium demand for high-performance pitch and yaw drive systems in next-generation onshore platforms.

-

December 2025: UKA placed a landmark order for 80 turbines from Nordex Group totalling 540 MW across 15 German projects, accompanied by a 20-year full-scope service contract — illustrating the compounding long-term revenue model now characterising the wind drive component sector, where decades of maintenance services follow initial equipment supply.

-

2025: Siemens Gamesa advanced the development of its next-generation offshore wind platform incorporating enhanced electric pitch drive systems with improved reliability metrics for deployment in the North Sea and Baltic Sea, targeting installation in the 2026–2028 project pipeline as European offshore wind capacity expands rapidly.

-

2025: Vestas announced expanded manufacturing capacity for pitch and yaw drive components at its European facilities, responding to accelerating offshore wind order intake and increasing aftermarket demand from its global installed base of more than 170 GW of wind turbines under service contracts.

-

2025: ZF Friedrichshafen expanded its wind energy drivetrain portfolio with enhanced yaw drive systems optimised for the structural and environmental demands of floating offshore wind platforms — positioning the company for a segment expected to grow rapidly as floating wind projects advance from demonstration scale to commercial deployment across European, Asian, and U.S. markets.

Wind Turbine Pitch and Yaw Drive Market Key Players

-

Siemens Gamesa Renewable Energy

-

Vestas Wind Systems A/S

-

GE Vernova (GE Renewable Energy)

-

Nordex SE

-

Suzlon Energy Limited

-

Mitsubishi Heavy Industries, Ltd.

-

Senvion GmbH

-

Dongfang Electric Corporation

-

Hansen Transmissions International NV

-

ZF Friedrichshafen AG

-

Bonfiglioli Riduttori S.p.A.

-

Comer Industries S.r.l.

-

Schaeffler Group

-

ABM Greiffenberger Antriebstechnik GmbH

-

Enercon GmbH

-

Rexnord Corporation

-

Moog Inc.

-

Mita-Teknik A/S

-

DEIF A/S

-

Bosch Rexroth AG

Wind Turbine Pitch and Yaw Drive Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.22 Billion |

| Market Size by 2035 | USD 17.00 Billion |

| CAGR | CAGR of 7.54% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (1000 W, 1000 W - 3000 W, and >3000 W) • BY Pitch System (Electric, Mechanical, and Hydraulic) • By Size (Small, Medium, and Large) • By End Use (Onshore and Offshore) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, GE Vernova (GE Renewable Energy), Nordex SE, Suzlon Energy Limited, Mitsubishi Heavy Industries, Ltd., Senvion GmbH, Dongfang Electric Corporation, Hansen Transmissions International NV, ZF Friedrichshafen AG, Bonfiglioli Riduttori S.p.A., Comer Industries S.r.l., Schaeffler Group, ABM Greiffenberger Antriebstechnik GmbH, Enercon GmbH, Rexnord Corporation, Moog Inc., Mita-Teknik A/S, DEIF A/S, Bosch Rexroth AG. |

Frequently Asked Questions

Ans: Europe dominated the Wind Turbine Pitch and Yaw Drive Market in 2025, accounting for approximately 37.7% of global market revenue, driven by the world's most mature wind energy ecosystem, ambitious renewable energy targets, extensive offshore wind development pipelines, and the concentration of leading turbine OEMs and component suppliers across Germany, Denmark, the United Kingdom, Spain, and the Netherlands.

Ans: The >3000 W segment dominated the Wind Turbine Pitch and Yaw Drive Market in 2025, holding approximately 67.2% of global revenue, driven by the widespread deployment of high-capacity turbines for offshore wind farms and large-scale onshore installations requiring powerful, reliable drive systems.

Ans: The primary growth driver is the accelerating global demand for larger, more efficient wind turbines — particularly offshore platforms — driven by net-zero commitments, renewable energy mandates, and the declining levelised cost of wind energy, which collectively are generating sustained, multi-decade demand for advanced pitch and yaw drive systems across all major geographies.

Ans: The Wind Turbine Pitch and Yaw Drive Market was valued at USD 8.22 billion in 2025.

Ans: The Wind Turbine Pitch and Yaw Drive Market is expected to grow at a CAGR of 7.54% from 2026 to 2035.

Get in Touch