Acoustic Insulation Market Report Scope & Overview:

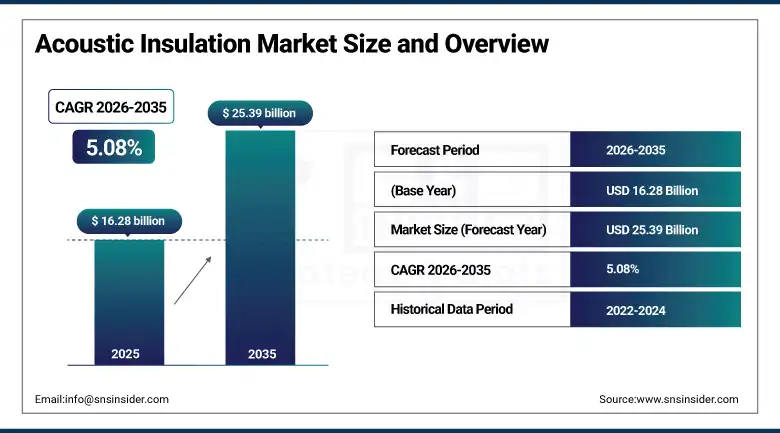

The Acoustic Insulation Market was valued at USD 16.28 Billion in 2025 and is expected to reach USD 25.39 Billion by 2035, growing at a CAGR of 5.08% from 2026 to 2035.

Acoustic insulation encompasses the full range of materials and engineered systems designed to reduce, absorb, block, or dampen sound transmission between spaces, whether airborne noise propagating through air gaps and structural pathways, or impact noise transmitted through building structures as vibration. The commercial imperative driving acoustic insulation investment has intensified across multiple simultaneously expanding demand fronts. Urbanization concentrating larger populations in denser residential environments where noise from neighbors, traffic, and urban infrastructure directly affects sleep quality, cognitive performance, and psychological wellbeing creates strong consumer demand for acoustic comfort that building codes are progressively formalizing into mandatory minimum acoustic performance standards.

In October 2024, Knauf Insulation opened a new glass wool production facility in Poland, expanding its manufacturing capacity in Eastern Europe to serve the growing demand from residential and commercial construction markets across Poland, the Czech Republic, and the wider Central and Eastern European region. The investment demonstrated Knauf Insulation's strategic commitment to production proximity to growth markets whose increasing building activity, strengthening acoustic performance building standards, and growing green building adoption are creating sustained above-average acoustic insulation demand growth relative to Western European market rates.

Market Size and Forecast

-

Market Size in 2026E: USD 17.11 Billion

-

Market Size by 2035: USD 25.39 Billion

-

CAGR: 5.08% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get more information On Acoustic Insulation Market - Request Free Sample Report

Acoustic Insulation Market Trends

-

Rising electric vehicle adoption is increasing demand for advanced acoustic insulation to reduce cabin noise from road, wind, and drivetrain sources.

-

Growing use of sustainable and bio-based insulation materials is supporting environmentally friendly construction practices.

-

Thin, high-performance acoustic membranes and composite panels are gaining popularity in space-constrained retrofit projects.

-

Smart acoustic solutions combining active noise control with passive insulation are emerging in premium building applications.

-

Integration of acoustic insulation requirements into BIM-based design workflows is improving building sound-performance planning and optimization.

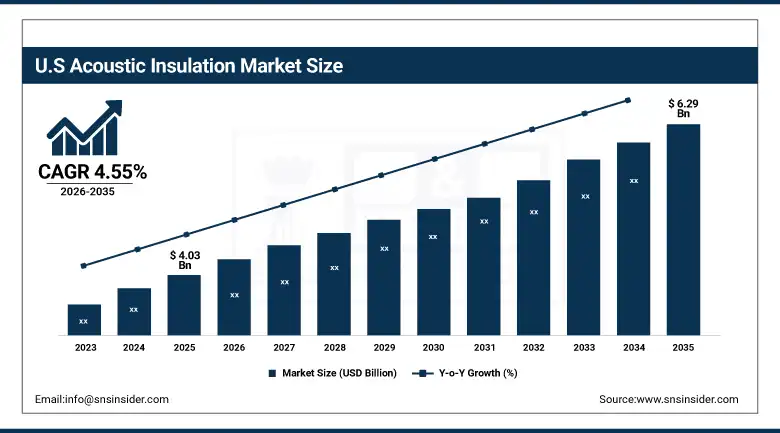

The U.S. Acoustic Insulation Market Outlook

The U.S. Acoustic Insulation Market was valued at approximately USD 4.03 Billion in 2025 and is expected to reach approximately USD 6.29 Billion by 2035, growing at a CAGR of approximately 4.55%. Europe is the largest regional acoustic insulation market, while Asia Pacific is growing fastest, with a CAGR of 7.5% documented in the forecast period, driven by rapid construction activity and tightening building codes.

The United States acoustic insulation market is driven by the renovation and retrofit of its large existing building stock whose acoustic performance does not meet contemporary standards, the stringent acoustic requirements of healthcare facility construction under guidelines that address patient sleep quality and clinical privacy, and the growing multifamily residential construction segment whose shared-wall and floor-ceiling assemblies require careful acoustic insulation specification to comply with ICC and IBC building code minimum sound transmission class requirements. The U.S. transportation sector's acoustic insulation demand from both automotive OEM production and aircraft cabin lining applications sustains a significant non-construction acoustic insulation market segment whose technical specifications and material performance requirements differ substantially from building construction applications.

In January 2025, Armacell partnered with a Middle Eastern construction firm to supply acoustic and thermal insulation for large-scale infrastructure projects in Saudi Arabia, demonstrating the growing demand for specialised insulation solutions in the Gulf region's ambitious construction programme. Armacell's elastomeric foam acoustic insulation products were specified for HVAC duct and pipe acoustic insulation across multiple commercial building projects whose open-plan office and hospitality function requirements demand HVAC system noise control that standard fibre insulation cannot achieve within the mechanical plant space constraints of modern commercial building design.

Acoustic Insulation Market Segment Analysis

-

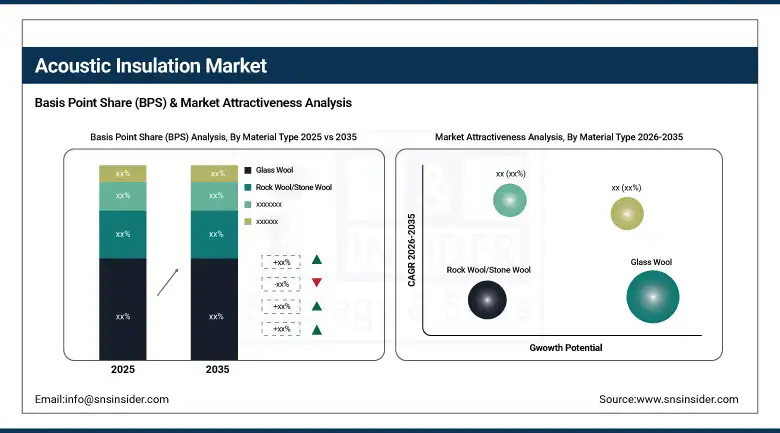

By Material Type, glass wool segment dominated the acoustic insulation market with approximately 34% market share in 2025, while the foamed plastics segment is projected to be the fastest-growing material type, registering a CAGR of around 6.9% during 2026–2035.

-

By End-Use Industry, building & construction segment dominated the acoustic insulation market with the largest share in 2025, while the transportation segment is the fastest growing end-use industry during the forecast period.

-

By Application, the walls & partitions segment dominated the acoustic insulation market in 2025, while the HVAC ducts & pipes segment is the fastest growing application during 2026 to 2035.

By Material Type, glass wool dominates, foamed plastics grow fastest

Glass wool generated the dominant material type revenue in 2025, reflecting its unmatched combination of cost-effectiveness, acoustic performance across the mid-frequency range where human speech and HVAC system noise concentrate, ease of installation in standard wall cavity and ceiling plenum applications, and broad compatibility with conventional building framing systems that make it the default acoustic insulation specification for residential and commercial construction across North American and European building markets. Glass wool's fibrous structure, whose randomly oriented glass filaments create tortuous air paths that dissipate sound energy through viscous friction, provides excellent sound absorption coefficients at the wall cavity thicknesses that standard building framing spaces accommodate.

Foamed plastics are growing fastest, driven by automotive requirements for thin, lightweight, moisture-resistant acoustic materials that mineral wool's hygroscopic characteristics and bulk density cannot satisfy within vehicle door cavity and underbody packaging constraints. Polyurethane foam, melamine foam, and elastomeric foam products serve specific automotive, HVAC, and industrial applications whose performance requirements favor polymer foam chemistry's tunable density, closed-cell moisture resistance, and fabrication flexibility. The HVAC industry's growing use of elastomeric foam pipe and duct insulation for combined thermal and acoustic management creates a commercially significant polymer foam growth category whose demand tracks commercial building construction activity.

By End-Use Industry, building & construction dominates, transportation grows fastest

Building and construction generated the dominant end-use industry revenue share in 2025, accounting for the majority of global acoustic insulation consumption across its residential, commercial, industrial, and institutional sub segments whose combined demand for wall, floor, ceiling, and mechanical system acoustic insulation makes this the foundational market segment. Residential construction's requirement for party wall, floor-ceiling, and external facade acoustic insulation is governed by mandatory building code requirements whose compliance is non-negotiable and whose specification detail directly drives insulation product selection and specification. Commercial office, hospitality, healthcare, and educational building construction each contribute significant acoustic insulation demand whose open-plan office and patient privacy requirements specify acoustic insulation performance beyond minimum code compliance, driving premium product adoption that sustains above-commodity segment pricing.

Transportation is growing fastest, driven by automotive OEM investment in NVH (noise, vibration, and harshness) improvement programmes whose acoustic comfort targets are simultaneously becoming more stringent under consumer quality expectations and more technically challenging as electric vehicle elimination of engine noise masking requires acoustic insulation performance improvements across every vehicle interior surface. Each electric vehicle model generation's NVH programme represents a significant acoustic insulation content increase per vehicle relative to equivalent ICE model specifications, creating a structurally growing per-vehicle acoustic insulation value that multiplies with EV production volume growth to create one of the most commercially dynamic acoustic insulation demand growth vectors through the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Europe |

Germany |

28.47% |

|

North America |

United States |

82.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Acoustic Insulation Market Insights

North America held a significant share of global acoustic insulation revenues in 2025. The United States accounts for approximately 82.47% of regional revenue through its large multifamily residential construction market, stringent healthcare and educational facility acoustic requirements, and the automotive OEM acoustic insulation demand from domestic vehicle production. Building code requirements under the International Building Code and International Residential Code establish minimum sound transmission class ratings for party walls and floor-ceiling assemblies in multifamily construction whose compliance creates non-discretionary acoustic insulation procurement across every new residential unit built. Canada contributes supplementary demand through its growing multifamily residential construction, green building investment, and its alignment with U.S. building code acoustic requirements whose application across the shared North American building products market sustains common product specification.

Europe Acoustic Insulation Market Insights

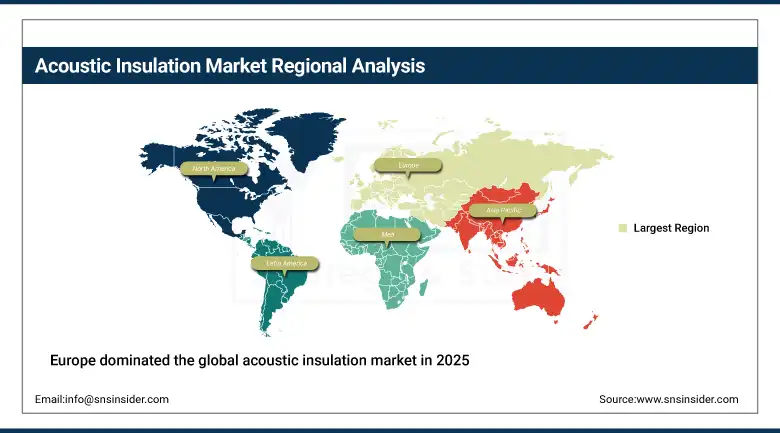

Europe dominated the global acoustic insulation market in 2025, holding the largest regional revenue share of approximately 37%. The region's market leadership reflects its comprehensive regulatory framework requiring acoustic performance documentation for residential, healthcare, and educational building categories, the mature green building certification ecosystem whose BREEAM and DGNB credit structures award acoustic comfort performance, and the high building renovation activity across the EU's energy and acoustic performance improvement programmes. Germany accounts for approximately 28.47% of European revenues through its large construction sector, automotive manufacturing acoustic insulation demand from premium OEM production, and the presence of major acoustic insulation manufacturers including Knauf, Saint-Gobain, and ROCKWOOL whose European headquarters and manufacturing operations concentrate regional market activity.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Acoustic Insulation Market Insights

Asia Pacific is the fastest-growing regional acoustic insulation market, with the region achieving a CAGR of approximately 7.50% through 2035, driven by rapid urbanization creating dense residential construction whose acoustic performance requirements are progressively formalised by tightening building regulations across China, India, Japan, South Korea, and Southeast Asia. China accounts for approximately 38.47% of Asia Pacific revenues through its enormous residential construction volume, industrial facility acoustic insulation requirements, and the rapidly expanding domestic automotive manufacturing sector whose NVH improvement investment is creating growing technical acoustic insulation demand from both domestic and international OEM customers.

MEA & Latin America Acoustic Insulation Market Insights

Middle East and Latin America are growing Acoustic Insulation markets where expanding construction activity, industrial facility development, and growing consumer awareness of acoustic comfort in residential and hospitality construction are creating increasing commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its world-class commercial and residential construction programme, the acoustic insulation requirements of its luxury hospitality sector whose brand standards demand acoustic privacy performance well above building code minimums, and the industrial acoustic insulation demand from its petrochemical processing and logistics facility sectors.

Market Dynamics

Growth Drivers: Stricter building codes mandating acoustic performance standards and the electric vehicle transition increasing per-vehicle acoustic insulation

The acoustic insulation market's growth is powered by two complementary regulatory and technological forces operating simultaneously. Building codes across major economies are progressively incorporating minimum acoustic performance requirements for residential, healthcare, and educational construction that previously were either absent or unenforceable, creating compliance-driven demand for acoustic insulation specification whose non-discretionary nature provides structural market stability through economic cycles. The electric vehicle transition is simultaneously creating a technology-driven demand growth vector as each additional percentage point of vehicle electrification increases the per-vehicle acoustic insulation content requirement, multiplying the commercial impact of EV adoption rates across the automotive industry's annual production volumes. Together, these demand forces create a market whose growth is driven by converging regulatory and technology forces independent of cyclical construction market fluctuations.

Restraints: High-performance acoustic insulation costs and installation complexity limit adoption above minimum code compliance levels

The cost premium of high-performance acoustic insulation products including aerogel composites, dense-pack mineral wool, and multi-layer acoustic membrane systems over standard building code-compliant alternatives creates a value-engineering pressure in residential and commercial construction that consistently reduces acoustic insulation specification to minimum compliance levels rather than optimal acoustic comfort performance. Professional acoustic insulation installation requires specialist knowledge of flanking transmission paths, acoustic bridge identification, and continuity detailing that building contractors without acoustic insulation training frequently overlook, creating performance gaps between design specification and installed performance that damage the market's reputation for reliability in delivering promised acoustic performance improvements.

Opportunities: Building retrofit acoustic improvement programmes and automotive NVH innovation for electric vehicles represent high-value commercial growth frontiers for acoustic insulation manufacturers

The vast global stock of existing buildings whose acoustic performance falls below contemporary standards represents a retrofit acoustic improvement market whose scale substantially exceeds new construction acoustic insulation demand in mature markets. European and North American governments are increasingly coupling energy efficiency retrofit grant programmes with acoustic improvement requirements whose implementation creates bundled energy and acoustic insulation project opportunities for contractors and product suppliers. Each kWh of energy saving achieved through building envelope upgrade creates a co-installation opportunity for acoustic insulation whose marginal cost within an active renovation project is substantially below the cost of a standalone acoustic retrofit. Automotive NVH innovation programmes whose engineering investment in multi-material acoustic systems, tunable damping composites, and distributed noise absorption technologies create a premium acoustic insulation product development market that rewards technical performance differentiation with above-commodity pricing.

Recent Developments:

-

2025: Armacell partnered with a Middle Eastern construction firm to supply elastomeric foam acoustic and thermal insulation for large-scale Saudi Arabian infrastructure projects, expanding Armacell's commercial presence in the Gulf region's rapidly growing construction and industrial sectors.

-

2024: Knauf Insulation opened a new glass wool production facility in Poland to strengthen manufacturing capacity in Eastern Europe, responding to growing demand from Central and Eastern European residential and commercial construction markets whose building code tightening and green building adoption are driving above-average acoustic insulation demand growth.

-

2023: Kingspan Group completed the acquisition of a majority stake in Steico SE, a German natural and wood-based insulation manufacturer, expanding Kingspan's portfolio into sustainable bio-based acoustic insulation products and strengthening its competitive position in the growing green building materials segment.

Acoustic Insulation Market Key Players are:

-

Saint-Gobain SA

-

ROCKWOOL International AS

-

Owens Corning

-

Knauf Insulation GmbH

-

Armacell International SA

-

Kingspan Group PLC

-

Johns Manville (Berkshire Hathaway)

-

Recticel NV

-

Fletcher Insulation Pty Ltd.

-

Cellecta Ltd.

-

International Cellulose Corporation

-

Acoustafoam Ltd.

-

Acoustical Surfaces Inc.

-

Paroc Group Oy (Owens Corning)

-

Isover (Saint-Gobain)

-

BASF SE

-

Huntsman Corporation

-

Illinois Tool Works Inc.

-

Nichias Corporation

-

Autex Industries Ltd.

Acoustic Insulation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.28 Billion |

| Market Size by 2035 | USD 25.39 Billion |

| CAGR | CAGR of 5.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Glass Wool, Rock Wool/Stone Wool, Foamed Plastics, Elastomeric Foam, Natural Fibre Insulation, Others) • By End-Use Industry (Building & Construction, Transportation, Oil & Gas, Energy & Utilities, Industrial & OEM) • By Application (Walls & Partitions, Floors & Underlayments, Roofs & Ceilings, HVAC Ducts & Pipes, Automotive & Transportation Interiors, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Saint-Gobain SA, ROCKWOOL International A/S, Owens Corning, Knauf Insulation GmbH, Armacell International SA, Kingspan Group PLC, Johns Manville (Berkshire Hathaway), Recticel NV, Fletcher Insulation Pty Ltd., Cellecta Ltd., International Cellulose Corporation, Acoustafoam Ltd., Acoustical Surfaces Inc., Paroc Group Oy (Owens Corning), Isover (Saint-Gobain), BASF SE, Huntsman Corporation, Illinois Tool Works Inc., Nichias Corporation, and Autex |

Frequently Asked Questions

The acoustic insulation market is expected to grow at a CAGR of 5.08% from 2026 to 2035.

The acoustic insulation market was valued at USD 16.28 Billion in 2025.

Stricter building acoustic regulations, increasing electric vehicle production, expanding green building certification programs, growing awareness of noise pollution impacts, and rising automotive NVH (noise, vibration, and harshness) investments are driving acoustic insulation market growth.

The glass wool segment dominated the acoustic insulation market in 2025 due to its cost-effectiveness, broad acoustic performance, and compatibility with standard building framing systems across residential and commercial construction.

Europe dominated the acoustic insulation market in 2025, holding the largest regional revenue share through its comprehensive building acoustic regulatory framework.

Get in Touch