Photoacoustic Imaging Market Report Scope & Overview:

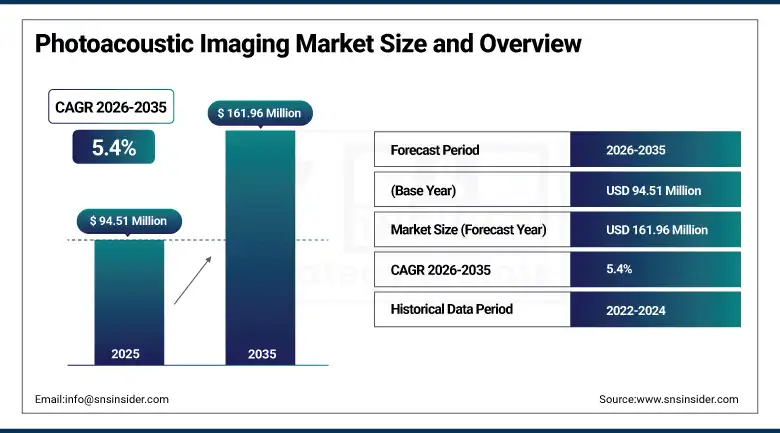

The Photoacoustic Imaging Market was valued at USD 94.51 Million in 2025 and is expected to reach USD 161.96 Million by 2035, growing at a CAGR of 5.4% from 2026–2035.

The global photoacoustic imaging market is advancing as a technically distinctive medical imaging modality that combines pulsed laser excitation with ultrasound detection to generate high-resolution images of tissue optical absorption in real time without ionising radiation. The technology delivers functional and molecular imaging information beyond what conventional ultrasound provides, while achieving centimetre-scale tissue penetration depth that optical-only techniques cannot reach. NIH funded biomedical imaging research at USD 1.4 billion in fiscal year 2023, up 5% year-on-year, creating the institutional investment environment that sustains photoacoustic system and transducer development.

In January 2024, a consortium of U.S. universities received a USD 5 million NIH grant to develop an intraoperative photoacoustic imaging platform for real-time tumour margin assessment during cancer surgery. The platform’s objective is to reduce positive margin rates that necessitate re-excision surgery in 20–30% of breast conservation procedures, demonstrating the high-value clinical application that could accelerate photoacoustic imaging’s transition from pre-clinical research tool to intraoperative clinical standard.

Market Size and Forecast

-

Market Size in 2026E: USD 99.62 Million

-

Market Size by 2035: USD 161.96 Million

-

CAGR: 5.4% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Photoacoustic Imaging Market - Request Free Sample Report

Photoacoustic Imaging Market Trends

-

Intraoperative photoacoustic imaging for real-time tumour margin guidance is emerging as a high-value clinical application whose positive margin reduction potential creates a compelling clinical and health-economic case for system adoption in surgical oncology.

-

Photoacoustic tomography system miniaturisation is enabling clinical form factors that can be integrated with existing ultrasound platforms, reducing adoption barriers by leveraging familiar clinical workflows and existing infrastructure investment.

-

Multi-wavelength photoacoustic imaging is enabling functional haemoglobin oxygen saturation mapping and vascular microstructure characterisation that creates quantitative biomarker capabilities for tumour hypoxia assessment and peripheral vascular disease monitoring.

-

AI-assisted photoacoustic image reconstruction is reducing data processing time from minutes to seconds, enabling near-real-time photoacoustic imaging workflows that are compatible with clinical time constraints in interventional and diagnostic settings.

-

Contrast agent development for targeted photoacoustic imaging, including nanoparticle and dye formulations activated by disease-specific molecular targets, is progressively enabling molecular imaging applications that complement structural vascular imaging in research settings.

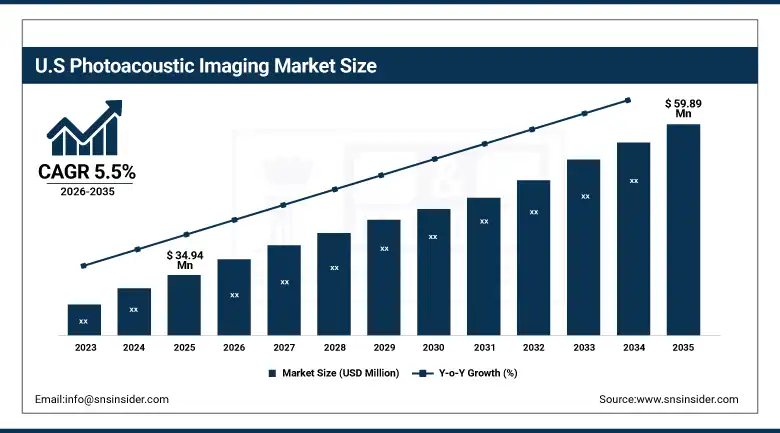

U.S. Photoacoustic Imaging Market Outlook

The U.S. Photoacoustic Imaging Market was valued at approximately USD 34.94 Million in 2025 and is expected to reach approximately USD 59.89 Million by 2035, growing at a CAGR of approximately 5.5%.

The U.S. is the world’s largest photoacoustic imaging market within the North America-dominant region. NIH biomedical research funding, the FDA’s regulatory pathway development for photoacoustic clinical systems, and the concentration of leading photoacoustic technology developers including Verasonics and Endra Life Sciences collectively create the research and commercial ecosystem sustaining market leadership. The USD 5 million NIH grant for intraoperative photoacoustic tumour margin assessment in January 2024 reflects the federal government’s recognition of photoacoustic imaging’s translational clinical potential whose successful realisation would substantially expand the market’s clinical adoption scope.

FUJIFILM VisualSonics expanded its Vevo LAZR-X photoacoustic imaging system capabilities in 2024 with enhanced multi-wavelength spectroscopic analysis features and improved real-time processing speed, enabling researchers to perform simultaneous structural and functional imaging of tumour vasculature, oxygenation, and perfusion in small animal models. The enhancement supports translational oncology research programmes whose pre-clinical photoacoustic validation is intended to inform future clinical photoacoustic imaging system design.

Photoacoustic Imaging Market Segment Analysis

-

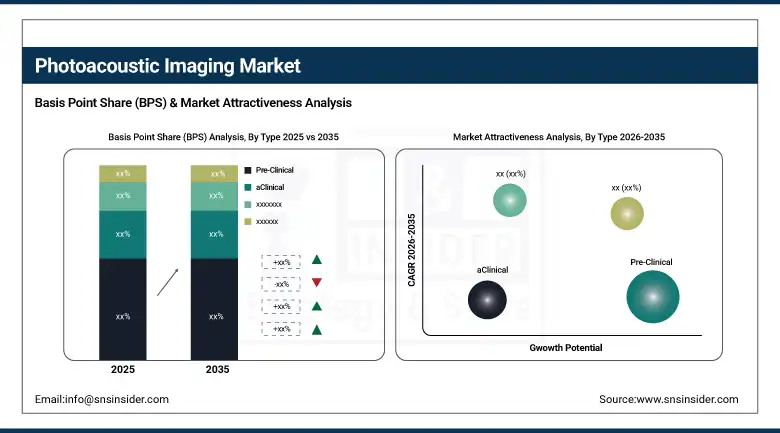

By Type, the Pre-Clinical segment dominated the Photoacoustic Imaging Market with approximately 78.00% share in 2025, while the Clinical segment is the fastest growing.

-

By Product, the Imaging Systems segment dominated the Photoacoustic Imaging Market with approximately 67.00% share in 2025, while the Transducers segment is the fastest growing.

-

By Technology, the Photoacoustic Tomography segment dominated the Photoacoustic Imaging Market with approximately 62.00% share in 2025, while the Photoacoustic Microscopy segment is the fastest growing.

-

By Application, the Oncology segment dominated the Photoacoustic Imaging Market with approximately 35.00% share in 2025, while the Cardiology segment is the fastest growing.

-

By End User, the Research Institutes segment dominated the Photoacoustic Imaging Market with approximately 57.00% share in 2025, while the Hospitals & Clinics segment is the fastest growing.

By Type, pre-clinical dominates, clinical grows fastest

Pre-clinical retained the dominant type position with approximately 78% of the photoacoustic imaging market in 2025. Its commercial primacy reflects the technology’s current developmental stage, where the majority of the installed system base supports biomedical research, pharmaceutical drug development, and translational science programmes in academic and commercial research settings. Pre-clinical photoacoustic imaging provides researchers with non-invasive longitudinal tumour microenvironment characterisation, vascular network mapping, and oxygen saturation monitoring in living small animal models that conventional histological analysis cannot provide from the same subject over time.

Clinical photoacoustic imaging is the fastest-growing type because the accumulation of pre-clinical research validation is progressively creating the clinical evidence base that supports regulatory submission and clinical adoption. FDA 510(k) clearances for clinically intended photoacoustic systems are creating the regulatory precedent that enables hospital and diagnostic centre procurement. Seno Medical’s Imagio breast imaging system, which combines photoacoustic and ultrasound for breast mass characterisation, represents the most commercially advanced clinical photoacoustic application whose regulatory approval and clinical deployment validates the transition pathway from research to clinical use that other photoacoustic applications are following.

By Application, oncology dominates, cardiology grows fastest

Oncology retained the dominant application position in the photoacoustic imaging market in 2025. Photoacoustic imaging’s ability to characterise tumour vasculature, map haemoglobin oxygen saturation as a marker of tumour hypoxia, and monitor anti-angiogenic therapy response creates a comprehensive functional oncology imaging toolkit whose translational value sustains the largest application-specific research and commercial investment in the market. Breast imaging, skin cancer characterisation, and intraoperative margin assessment represent the clinical oncology applications closest to widespread adoption, with pre-clinical models across pancreatic, prostate, and lung cancer creating the next wave of translational clinical application.

Cardiology is the fastest-growing application segment because photoacoustic imaging’s ability to characterise coronary artery plaque composition, assess peripheral arterial disease haemodynamics, and map myocardial perfusion using endogenous haemoglobin contrast offers diagnostic information that conventional ultrasound cannot provide without exogenous contrast agents. Intravascular photoacoustic imaging catheters for coronary plaque vulnerability assessment are advancing through translational research programmes whose clinical validation could create a substantial new interventional cardiology application for photoacoustic technology.

By Product, imaging systems dominate, transducers grow fastest

Imaging systems retained the dominant product position in the photoacoustic imaging market in 2025. System procurement represents the primary capital investment event whose specification drives the entire photoacoustic imaging programme’s clinical or research capability. Each institutional decision to adopt photoacoustic imaging begins with system selection whose capital cost, performance specification, and application compatibility determine the subsequent accessories, software, and service procurement that sustains ongoing market revenue. The imaging system’s laser, detector array, and processing unit collectively define the photoacoustic platform’s clinical and research capability.

Transducers are the fastest-growing product segment because the expanding application range of photoacoustic imaging is creating demand for specialised transducer configurations whose optimised geometry, frequency response, and sensitivity characteristics serve specific clinical and research use cases that general-purpose system transducers cannot address with equivalent performance. Intraoperative surgical transducers, intravascular photoacoustic catheters, and high-frequency dermatology transducers each represent application-specific product categories whose development is creating an expanding accessories market around the established system installed base.

By End User, research institutes dominate, hospitals grow fastest

Research institutes retained the dominant end user position in the photoacoustic imaging market in 2025. The majority of commercial photoacoustic systems are deployed in university biomedical research departments, cancer research centres, and pharmaceutical company pre-clinical imaging facilities whose research workflow requirements, long-duration experiments, and small animal model protocols align with the current commercial maturity level of photoacoustic imaging platforms. NIH grant-funded research programmes are the primary procurement mechanism for U.S. academic photoacoustic systems whose purchasing decisions are driven by specific research protocol requirements rather than clinical workflow efficiency.

Hospitals and clinics are the fastest-growing end user segment because clinical regulatory approvals and clinical validation publications are progressively creating the evidence base that hospital procurement decision-makers require before committing capital equipment investment to photoacoustic systems. Each clinical publication demonstrating photoacoustic imaging performance in diagnostic or intraoperative applications, and each regulatory clearance enabling clinical deployment, creates adoption momentum that compounds across the hospital market as early adopter clinical evidence accumulates.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Photoacoustic Imaging Market Insights

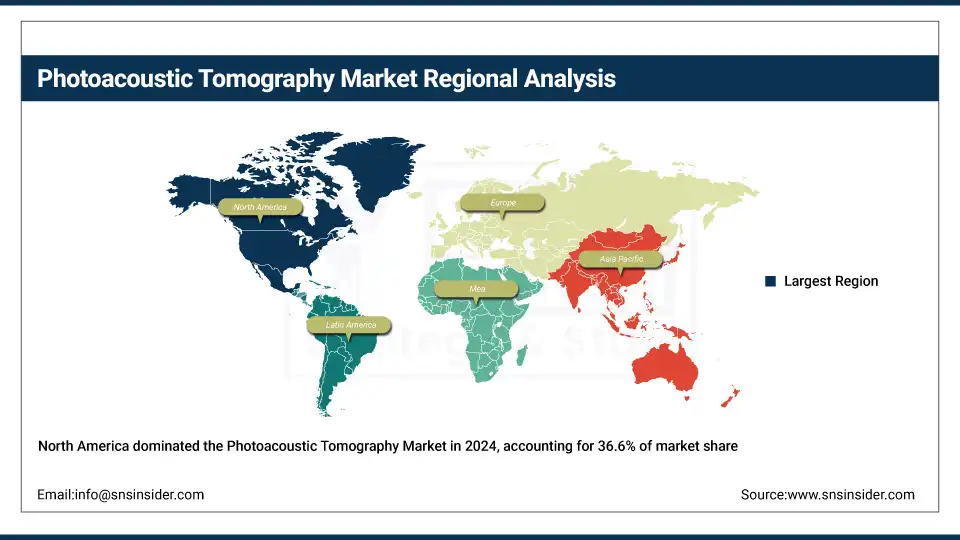

North America dominated the global photoacoustic imaging market in 2025 with approximately 42% of global revenues. The United States accounts for approximately 87.4% of North American revenues. NIH biomedical research funding creates the institutional procurement environment whose research grant-driven procurement sustains above-average photoacoustic system adoption rates relative to other global regions. The presence of Verasonics, Endra Life Sciences, and PhotoSound Technologies creates a domestic technology developer ecosystem whose commercial activity reinforces the market’s research institution procurement.

Canada contributes approximately 12.6% of North American revenues through its active biomedical research university system, CIHR-funded imaging research programmes, and photoacoustic research groups at University of Toronto, University of British Columbia, and Ryerson University whose equipment procurement and translational research activity sustain consistent market engagement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Photoacoustic Imaging Market Insights

Europe is a technically sophisticated photoacoustic imaging market where EU Horizon research funding, the active biomedical engineering research ecosystem across Germany, the Netherlands, and the United Kingdom, and the commercial presence of iThera Medical GmbH and Optosonics create a complete photoacoustic technology development and commercial adoption environment. Germany accounts for approximately 22.3% of European revenues through iThera Medical’s MSOT system commercial leadership in pre-clinical research, strong academic photoacoustic research programmes, and the DFG’s biomedical research funding that sustains photoacoustic system procurement.

The United Kingdom and the Netherlands are significant secondary markets where active photoacoustic research groups at King’s College London, University College London, and Erasmus MC have generated foundational photoacoustic technology innovation and created institutional procurement through their own research programmes whose external visibility attracts international research collaboration that sustains regional market development.

Asia Pacific Photoacoustic Imaging Market Insights

Asia Pacific is the fastest-growing regional photoacoustic imaging market, driven by rising healthcare expenditure, growing awareness of early disease detection importance, and government initiatives expanding biomedical research and healthcare infrastructure investment across China, Japan, South Korea, and India. China accounts for approximately 44.8% of Asia Pacific revenues through its expanding biomedical research university system, government-funded cancer research infrastructure, and the growing number of photoacoustic research groups whose pre-clinical imaging programme development creates structured equipment procurement.

Japan and South Korea represent technically sophisticated secondary markets whose pharmaceutical industry’s translational research investment and advanced academic biomedical engineering departments create consistent photoacoustic system procurement. Japan’s Canon and FUJIFILM VisualSonics’ photoacoustic programme development reflects the domestic technology investment in photoacoustic clinical system development whose commercialisation creates both domestic supply and export market opportunity.

MEA & Latin America Photoacoustic Imaging Market Insights

The Middle East and Africa and Latin America are emerging photoacoustic imaging markets where healthcare infrastructure development and growing research investment are creating early-stage structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through its Vision 2030 healthcare and research investment, King Abdullah University of Science and Technology’s biomedical research programme, and the private hospital sector’s growing diagnostic technology adoption.

Brazil leads Latin American revenues at approximately 44.2% through its university biomedical research infrastructure, FAPESP and CNPq research grant funding for imaging technology development, and the growing private healthcare sector’s diagnostic technology investment that is creating initial photoacoustic system adoption in leading cancer and cardiovascular centres.

Market Dynamics

Growth Drivers: NIH and government biomedical research funding and clinical oncology applications driving translational adoption

NIH and government biomedical research funding is the photoacoustic imaging market’s most commercially direct institutional growth driver. NIH’s USD 1.4 billion biomedical imaging research investment in fiscal year 2023 creates the grant-funded procurement mechanism that enables academic and research institution photoacoustic system acquisition. Each new NIH imaging grant that identifies photoacoustic technology as the appropriate tool creates a defined system procurement event whose commercial value is determined by the funded programme’s scale and duration. The structured nature of grant-funded procurement provides commercial predictability that complements the private hospital capital equipment market’s longer adoption cycle.

Clinical oncology application development is creating the translational commercial momentum that will define photoacoustic imaging’s market growth trajectory beyond the research institution installed base. The NIH’s USD 5 million grant for intraoperative tumour margin assessment, Seno Medical’s Imagio clinical breast imaging system, and the growing clinical publication volume in photoacoustic oncology collectively create the adoption infrastructure that hospital system procurement requires before committing to an emerging imaging modality. Each positive clinical study publication and each regulatory clearance event accelerates the adoption curve whose steepening creates above-linear market growth potential.

Restraints: Limited clinical regulatory clearances and high system cost relative to established imaging alternatives

Limited clinical regulatory clearances constrain photoacoustic imaging’s transition from research to clinical market. The regulatory pathway for photoacoustic clinical systems requires demonstration of safety, performance equivalency to predicate devices, and clinical utility that emerging technologies must establish through the submission process whose timeline extends commercial deployment beyond technology readiness. Each year of regulatory review that delays commercial clearance limits the clinical market’s development relative to the research market whose procurement does not require clinical device approval.

High photoacoustic system cost relative to the imaging alternatives clinicians can use for equivalent anatomical evaluation creates capital equipment procurement justification challenges. A hospital administrator comparing a USD 200,000-300,000 photoacoustic system to an existing ultrasound asset requires compelling clinical outcome evidence whose current accumulation in published literature is not yet sufficient to justify routine capital investment in most hospital procurement cycles. Cost reduction through photoacoustic module integration with existing ultrasound platforms is progressively addressing this barrier.

Opportunities: Intraoperative surgical guidance adoption and clinical reimbursement pathway development

Intraoperative surgical guidance represents the most commercially high-value clinical application whose adoption would most significantly accelerate photoacoustic imaging’s transition from niche research tool to mainstream clinical infrastructure investment. Positive surgical margin rates in breast conservation surgery of 20-30% create a quantifiable clinical quality problem whose resolution through intraoperative photoacoustic guidance would deliver measurable outcome improvement and health-economic return. The NIH’s USD 5 million research investment in intraoperative photoacoustic technology validates the application’s clinical priority and creates the institutional research programme whose evidence output will support subsequent commercial system development.

Clinical reimbursement pathway development represents the most commercially transformative institutional change that would accelerate photoacoustic imaging adoption in hospital and diagnostic centre settings. Once CMS and private payers establish reimbursement codes for photoacoustic imaging procedures in specific clinical indications, the revenue model that justifies hospital capital equipment investment becomes commercially viable. The pathway from regulatory clearance to reimbursement establishment, while lengthy, creates a structural commercial gateway whose crossing converts photoacoustic imaging from an uncompensated capability to a revenue-generating clinical service.

Recent Developments:

-

2024: A consortium of U.S. universities received a USD 5 million NIH grant in January 2024 to develop an intraoperative photoacoustic imaging platform for real-time tumour margin assessment during cancer surgery, targeting reduction of positive margin re-excision rates in breast conservation procedures through nanoscale-precision photoacoustic surgical guidance.

-

2024: FUJIFILM VisualSonics expanded Vevo LAZR-X capabilities in 2024 with enhanced multi-wavelength spectroscopic analysis and improved real-time processing speed, enabling simultaneous structural and functional imaging of tumour vasculature, oxygenation, and perfusion to support translational oncology research programmes.

-

2024: iThera Medical advanced its MSOT Acuity Echo clinical photoacoustic-ultrasound system in 2024 through additional clinical investigation programmes in inflammatory bowel disease and peripheral vascular disease assessment, generating clinical evidence supporting regulatory submissions for expanded clinical indication approval in European and U.S. markets.

Photoacoustic Imaging Market Key Players

-

Verasonics Inc.

-

Endra Life Sciences Inc.

-

FUJIFILM VisualSonics Inc.

-

iThera Medical GmbH

-

PhotoSound Technologies Inc.

-

Optosonics Ltd.

-

Seno Medical Instruments

-

TomoWave Laboratories

-

Kibero GmbH

-

PreXion Corporation

-

Cyberdyne Inc.

-

Aspect Imaging

-

GE Healthcare

-

Philips Healthcare

-

Canon Medical Systems

Photoacoustic Imaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 94.51 Million |

| Market Size by 2035 | USD 161.96 Million |

| CAGR | CAGR of 5.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Pre-Clinical, Clinical) • by Product (Imaging Systems, Transducers, Accessories & Software) • by Technology (Photoacoustic Tomography, Photoacoustic Microscopy) • by Application (Oncology, Cardiology, Neurology, Ophthalmology, Dermatology, Others) • by End User (Research Institutes, Hospitals & Clinics, Diagnostic Centres) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Verasonics Inc., Endra Life Sciences Inc., FUJIFILM VisualSonics Inc., iThera Medical GmbH, PhotoSound Technologies Inc., Optosonics Ltd., Seno Medical Instruments, TomoWave Laboratories, Kibero GmbH, PreXion Corporation, Cyberdyne Inc., Aspect Imaging, GE Healthcare, Philips Healthcare, Canon Medical Systems |

Frequently Asked Questions

The Photoacoustic Imaging Market is expected to grow at a CAGR of 5.4% from 2026 to 2035.

The Photoacoustic Imaging Market was valued at USD 94.51 Million in 2025.

NIH and government biomedical research funding creating institutional grant-funded procurement for pre-clinical photoacoustic systems, and clinical oncology application development including intraoperative tumour margin guidance translating pre-clinical platform maturity into high-value clinical adoption programmes.

Pre-Clinical dominated the Photoacoustic Imaging Market with approximately 78% share in 2025, while Clinical is the fastest-growing type.

North America dominated the Photoacoustic Imaging Market in 2025 with approximately 42% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch