AI Chip Market Size & Trends Analysis:

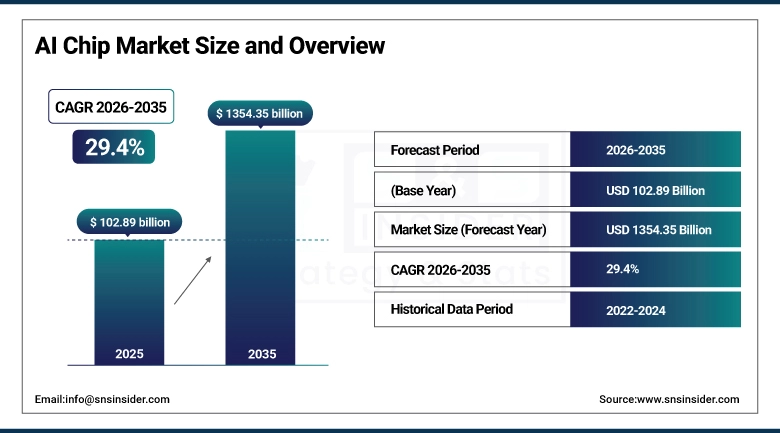

The AI Chip Market Size was valued at USD 102.89 Billion in 2025 and is expected to reach USD 1354.35 Billion by 2035 and grow at a CAGR of 29.4% over the forecast period 2026-2035.

The market for AI chips is witnessing rapid growth due to the increasing adoption of artificial intelligence technology in industries like healthcare, automotive, finance, and retail. The rising requirement for high-performance computing, increased data centers, and cloud-based AI services is also driving the market. The increased use of edge devices, autonomous systems, and generative AI applications is also contributing to the growth of the AI chips market. The constant improvements in semiconductor technology and increased investment in AI chips by governments and tech companies are also contributing to the market.

AI Chip Market Size and Growth Projection:

-

Market Size in 2025: USD 102.89 Billion

-

Market Size by 2035: USD 1354.35 Billion

-

CAGR: 29.4% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on AI Chip Market - Request Free Sample Report

Key AI Chip Market Trends:

-

Rising demand for generative AI, machine learning, and deep learning applications is driving the AI chip market.

-

Growing adoption of GPUs, ASICs, and NPUs for high-performance computing and data center acceleration is boosting market growth.

-

Expansion of edge AI across smartphones, IoT devices, and autonomous systems is fueling demand for specialized AI chips.

-

Increasing focus on energy-efficient and high-speed processing capabilities is shaping adoption trends.

-

Advancements in semiconductor technologies, including smaller nodes and heterogeneous computing architectures, are enhancing chip performance.

-

Rising investments by governments and tech companies in AI infrastructure and chip development are supporting market expansion.

-

Collaborations between semiconductor manufacturers, cloud providers, and AI firms are accelerating innovation and large-scale deployment.

U.S AI Chip Market Size Outlook:

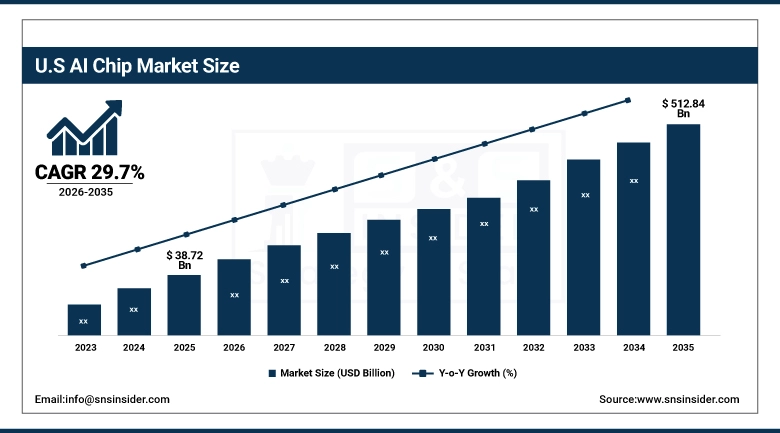

The United States AI Chip Market Size was valued at approximately USD 38.72 Billion in 2025 and is expected to reach around USD 512.84 Billion by 2035, growing at a CAGR of 29.7% over the forecast period 2026–2035. The US market for AI chips is influenced by robust market need for advanced computing capabilities across data centers, cloud environments, and business applications. The rapid acceptance of generative AI, machine learning, and autonomous technologies has created a strong need for advanced chipsets. The presence of prominent technology players and chipmakers has helped accelerate market development. Moreover, growing support for AI technologies, investments in chip manufacturing within the country, and growing edge AI applications are fueling market development.

AI Chip Market Key Drivers:

-

Rapid adoption of artificial intelligence across industries is fueling demand for high-performance AI chips globally in various computing applications

The rising adoption of AI technologies in various industries such as healthcare, automobiles, finance, retail, and manufacturing is one of the significant factors propelling the market for AI chips. The rising adoption of data centers, cloud computing, and high-performance computing is also one of the factors propelling the market. The rising advancements in machine learning, deep learning, and generative AI are also propelling the market. Furthermore, the rising investments in AI infrastructure by governments and prominent technology companies are also propelling the market.

AI Chip Market Key Restraints:

-

High development costs and complex semiconductor manufacturing processes are limiting the growth of the AI chip market globally

The process of designing and manufacturing AI chips requires substantial capital investment, sophisticated semiconductor fabrication facilities, and intricate supply chains. Such factors create entry barriers for new players in this market. Variability in semiconductor supply and dependence on a few semiconductor fabrication plants are some factors that affect AI chip production. High power consumption and thermal issues are challenges in designing high-performance AI chips. Government regulations and export restrictions are also factors that impact AI chip supply and hence its market growth.

AI Chip Market Key Opportunities:

-

Growing demand for edge AI and customized AI processors is creating opportunities for innovation and strategic collaborations worldwide

The trend of AI being deployed at the edge enabled via smartphones, IoT and self-driving cars is opening new doors towards the AI chip industry. The chips designed for a particular application are energy-efficient, which drives companies to develop them to meet energy needs across industries. New product development in AI chips is driven by growing investments in AI startups and investments in semiconductor technologies. Moreover, the strengthening of alliances among chipmakers, cloud providers, and enterprises to complement the growth of the AI Chip Industry will also create new market opportunities at its nascent stages.

AI Chip Market Segments:

-

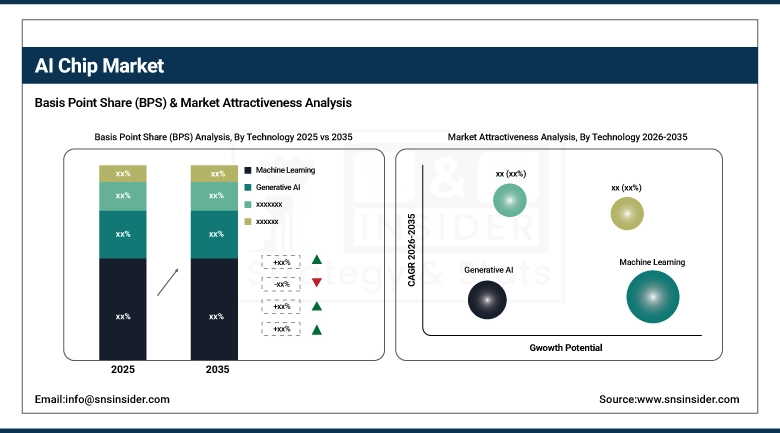

By Technology: In 2025, Machine Learning dominated with 38% share; Generative AI fastest growing segment during 2026–2035

-

By Chip Type: In 2025, GPU dominated with 46% share; ASIC fastest growing segment during 2026–2035

-

By Function: In 2025, Training dominated with 55% share; Inference fastest growing segment during 2026–2035

-

By End-User: In 2025, Data Center dominated with 49% share; Consumer fastest growing segment during 2026–2035

By Technology, Machine Learning segment dominates the Market, Generative AI segment expected to grow fastest

Machine Learning segment had the biggest share of the AI Chip Market, by revenue, in 2025. Machine learning workloads are standard in numerous sectors, from healthcare and finance to retail and manufacturing. Such demand for AI chips is continuous in nature and has assisted machine learning segment to maintain its market hold till now on global AI Chip Market.

Generative AI holds the highest CAGR during the forecast period of 2026-2035 for the AI Chip Market. The growing adoption of large language models, images, and AI-generated content has created a strong demand for AI chips. This segment of the AI Chip Market requires a high amount of computational power, which has increased the adoption of GPUs.

By Chip Type, GPU segment dominates the Market, ASIC segment expected to grow fastest

The GPU segment had the highest revenue share in the AI Chip Market in 2025. GPUs are popularly used in parallel processing and are very efficient in handling AI-related tasks. This segment is also driven by strong adoption in data centers, cloud computing, and high-performance AI-related tasks.

The ASIC segment is expected to grow at the highest CAGR in the AI Chip Market during 2026-2035. ASIC chips are specifically designed to perform AI-related tasks in an efficient manner with low power consumption. They are more efficient compared to other chips in handling AI-related tasks. In addition to this, the increasing demand for application-specific chips is also driving this market.

By Function, Training segment dominates the Market, Inference segment expected to grow fastest

Training segment dominated the AI Chip Market in 2025, as the high computational power is required in the training of AI models. High computational power is needed in processing high amounts of data in data centers, which has led to the dominance of the training segment.

Inference segment is expected to grow at the highest CAGR in the AI Chip market from 2026-2035. With AI applications being implemented in real-time environments, there is a high requirement for inference chips.

By End-User, Data Center segment dominates the Market, Consumer segment expected to grow fastest

Data Center segment had the highest market share in the AI Chip Market in 2025, due to the increase in the deployment of AI workloads in cloud infrastructure and enterprise systems. The requirement for high-performance computing and huge data processing is fueling investments in AI-enabled data centers.

Consumer segment is expected to have the highest CAGR in the AI Chip Market in the range of 2026 to 2035. The increase in the use of AI-enabled products like smartphones, wearables, and smart home is driving the AI chip market in consumer electronics.

AI Chip Market Regional Analysis:

North America AI Chip Market Insights:

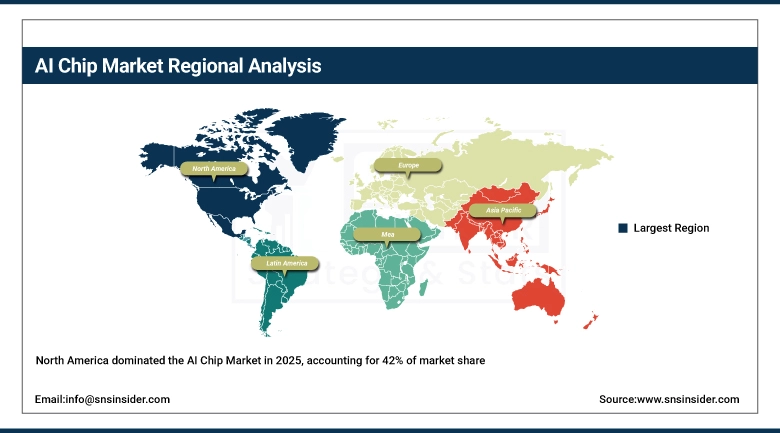

North America Global Artificial Intelligence Chip Market is having largest market share in 2025 of 42% region wise. Dan Ives, managing director for equity research at Wedbush Securities, attributes this dynamic to the presence of large tech players, semiconductor manufacturers, and cloud service providers like NVIDIA, Intel and Google, to name a few. Rising investments in artificial intelligence research, data centers, and advanced computing infrastructure, along with rapid adoption of generative artificial intelligent and machine learning technologies, are contributing to the growth of the market. Local market growth is also driven by government initiatives aimed at enhancing local semiconductor manufacturing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific AI Chip Market Insights:

The Asia-Pacific segment is expected to register the highest CAGR of 31.2% from 2026 to 2035 due to high digitalization and AI adoption in the region. Many countries in the region, including China, India, Japan, and South Korea, are investing heavily in semiconductor technology and AI innovation. Increasing demand for consumer electronics and growing 5G network infrastructure are driving growth in the region. In addition, edge AI device adoption is also driving growth in the region.

Europe AI Chip Market Insights:

The Europe AI chip market is growing steadily, with emphasis on AI sovereignty and semiconductor independence driving the market. The presence of key players and the European Union's initiatives to boost domestic chip production are contributing to the growth of the AI chip market in Europe. Investments in AI research, AI in automobiles, and industrial automation are contributing to the growth of the AI chip market in the region. AI chip uptake in manufacturing, healthcare, and automotive industries is contributing to the growth of the AI chip market in Europe.

Latin America AI Chip Market Insights:

Latin America’s AI Chip Market is growing at a steady pace due to the increasing adoption of AI technologies. Brazil and Mexico are increasingly investing in cloud computing, data centers, and AI-based applications. The growing need for smart gadgets and the improvement of IT infrastructure are factors that are helping the AI chip market grow.

Middle East & Africa (MEA) AI Chip Market Insights:

The Middle East & Africa region is experiencing steady growth in the AI Chip Market due to increasing digital transformation and government initiatives to promote AI Chip technology. The United Arab Emirates and Saudi Arabia are investing in smart city projects and AI Chip technology. Cloud infrastructure growth and interest in automation are driving growth in the AI Chip Market in this region.

AI Chip Market Competitive Landscape:

NVIDIA Corporation is a prominent semiconductor company that specializes in graphics processing units and artificial intelligence computing technologies. NVIDIA plays a vital role in the development of artificial intelligence chipsets. NVIDIA's graphics processing units are used to accelerate machine learning, deep learning, and other high-performance computing applications. NVIDIA's platforms are utilized to support data center, autonomous vehicles, and generative AI workloads. NVIDIA is a prominent company that specializes in artificial intelligence acceleration and parallel computing technologies.

-

2026: NVIDIA continued to expand its AI dominance with next-generation GPU architectures and increased data center revenue driven by generative AI demand.

Intel Corporation is a multinational technology company based in Santa Clara, California. The company specializes in designing and developing CPUs, AI accelerators, and semiconductors. Intel is working hard to become a strong player in the AI chips market by developing innovative AI chips, data center chips, and edge computing chips. Intel is focusing on developing AI chips that can be integrated into all Intel products to serve enterprise, cloud, and industrial markets.

-

2026: Intel accelerated its AI strategy with advancements in AI-enabled processors and expansion of its semiconductor manufacturing capabilities under its IDM 2.0 initiative.

Headquartered in San Jose, California, Xilinx Inc. is a leader in adaptive computing and FPGA innovations (now part of AMD). Engagement in numerous AI apps which requires programmable logic solution such as for involvement, edge computing and datacenter acceleration. Xilinx solutions are scalable and efficient, and flexible enough for a wide variety of AI applications.

-

2026: AMD continued integrating Xilinx capabilities to enhance its AI and adaptive computing portfolio, expanding FPGA adoption in AI-driven workloads and data centers.

Top AI Chip Companies are:

-

NVIDIA Corporation

-

Intel Corporation

-

Xilinx Inc.

-

Samsung Electronics Co., Ltd.

-

Qualcomm Technologies

-

IBM Corporation

-

Google Inc.

-

Microsoft Corporation

-

Apple Inc.

-

Amazon Web Services (AWS)

-

Advanced Micro Devices, Inc.

-

General Vision

-

Mellanox Technologies

-

Huawei Technologies Co. Ltd.

-

Fujitsu

-

Wave Computing

-

Mythic Inc.

-

Adapteva

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 102.89 Billion |

| Market Size by 2035 | USD 1354.35 Billion |

| CAGR | CAGR of 29.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Generative AI, Machine Learning, Natural Language Processing, Computer Vision) • By Chip Type (CPU, GPU, ASIC, FPGA, Others) • By Function (Training, Inference) • By End-User (Consumer, Data Center, Government Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, Intel Corporation, Xilinx Inc., Samsung Electronics Co., Ltd., Micron Technology, Qualcomm Technologies, IBM Corporation, Google Inc., Microsoft Corporation, Apple Inc., Amazon Web Services (AWS), Advanced Micro Devices, Inc., Graphcore, General Vision, Mellanox Technologies, Huawei Technologies Co. Ltd., Fujitsu, Wave Computing, Mythic Inc., Adapteva. |

Frequently Asked Questions

Ans: The AI Chip Market is expected to grow at a CAGR of 29.4% during 2026–2035.

Ans: The AI Chip Market Size was valued at USD 102.89 Billion in 2025 and is expected to reach USD 1354.357 Billion by 2035.

Ans: Key drivers include rising adoption of AI technologies, increasing demand for high-performance computing, and advancements in semiconductor technologies.

Ans: The GPU segment dominated the AI Chip Market during the projected period.

Ans: North America dominated the AI Chip Market in 2025.

Get in Touch