Ultra Capacitors Market Size

Get More Information on Ultra Capacitor market - Request Sample Report

Ultra Capacitors Market Overview

The Ultra Capacitors Market Size was USD 2.75 Billion in 2023 & expects a good growth by reaching USD 9.62 billion till end of year2032 at CAGR about 15.04% during forecast period 2024-2032

The increasing popularity of electric vehicles is driving a spike in the need for ultracapacitors. These high-powered capacitors are great at providing quick and strong energy bursts, which perfectly work alongside the continuous power supply from batteries in electric vehicles. Picture yourself speeding up your electric vehicle onto a crowded freeway. The ultra capacitor is responsible for providing the initial burst of power needed to merge into traffic. It adds a burst of power to the battery, providing you with a quick response. When you decelerate at a red light, the ultra capacitor effortlessly collects the braking energy via regeneration, saving it for future consumption. The collaboration of the battery and ultra capacitor enhances vehicle acceleration and performance while decreasing strain on the battery, which may prolong its lifespan. A new study emphasizes this collaborative relationship. The study suggests an energy management system for a hybrid system that combines a solar-powered battery with an ultra capacitor, mirroring the collaboration seen in electric vehicles. The research shows that this system effectively cuts down on power surges by 26% during acceleration and recovers braking energy twice as quickly as some methods. These results confirm the increasing significance of ultra capacitors in electric vehicles, serving as a crucial element in maintaining the effectiveness, speed, and durability of EVs.

The distinctive sound of IndyCar motors is soon going to be mixed with an electric thrill. After years of progress, IndyCar will introduce its new hybrid engine system this weekend, signaling a major move towards eco-friendly racing technology. This new system uses ultra capacitors, which are recognized for their capacity to supply brief surges of energy, to add 120 horsepower to the current engines, increasing the overall output to over 800 horsepower for the first time in years.

Picture a driver exiting a bend quickly, requiring an added advantage to pass their rival. That is when the ultra capacitor comes into play. It releases a sudden increase in power, providing the driver with essential acceleration for an exciting overtaking maneuver. This technology is not only focused on speed but also opens the door to a more strategic and energy-saving future for Indy Car racing. Motorists will need to learn new methods to control their battery levels and strategically utilize the ultra capacitor's power surge for maximum efficiency. The implementation of ultra capacitors in the IndyCar hybrid system showcases how they can transform multiple industries dependent on intense energy spikes, leading to a future where efficiency and performance are closely linked.

Market Dynamics

Drivers

-

Ultra capacitor are fueling a more environmentally friendly future for industry.

The global push to reduce industrial CO2 emissions is creating significant opportunities for growth within the ultra capacitor sector. Nations face demands to embrace more environmentally friendly technologies while striving to meet ambitious net-zero goals outlined in agreements such as the Paris Agreement, which seeks to cut current CO2 emissions by 80% by 2050 to cap global warming at 1.5°C. Traditional UPS systems often rely on lead-acid batteries that play a major role in carbon emissions throughout their manufacturing and disposal processes. Ultra capacitor-based UPS systems offer a greener alternative by providing backup power without causing the environmental harm associated with lead-acid batteries. Fluctuations in voltage and power supply can disrupt industrial automation, leading to energy wastage and hindering a smooth and efficient production process. Ultracapacitors act as buffers, quickly absorbing and releasing energy to keep a steady power supply for machinery and improve manufacturing efficiency. This leads to reduced energy consumption and a decline in CO2 emissions. With sustainability becoming an increasing focus worldwide and more regulations being introduced, industrial businesses are actively seeking methods to decrease their carbon footprint. Ultra capacitors are well-placed to seize the growing market opportunity in the fight against climate change by enhancing energy efficiency and reducing reliance on less environmentally friendly alternatives.

-

Energy Chameleons, ultracapacitors adjust to meet constantly changing power requirements.

Quick reaction picturing a factory with constantly changing power needs. Ultra capacitors function similar to lightning rods, absorbing extra energy spikes and promptly releasing them when necessary. This quick ability to store and release energy guarantees a constant stream of power, avoiding interruptions and maximizing the efficiency of equipment. Enduring stamina and durability provide an additional benefit. While batteries deteriorate with frequent charging, ultracapacitors are designed to last a long time. They are able to endure multiple cycles without experiencing a significant decrease in capacity, reducing maintenance expenses and ensuring consistent performance over the long term. Ultra capacitors are a game-changer for energy management in different industries due to their quick response and long-lasting endurance. These adaptable energy chameleons are ready to be crucial in shaping a more flexible and effective future in various sectors, from industrial automation to renewable energy integration.

Restraints

-

Competitive pricing

The primary obstacle preventing ultra capacitors from being widely used is their expensive current cost. Ultra capacitors can cost a lot more than traditional capacitors and batteries. This could be a make-or-break situation for numerous sectors, particularly those operating on restricted budgets. Picture a manufacturer considering different choices for emergency power in a crucial production line. Although ultra capacitors provide quicker response times and extended lifespans, the initial expense could be a barrier when compared to a simpler battery setup. Efforts are being made to narrow the cost difference, which is a good development. Researchers are concentrating on enhancing manufacturing techniques and delving into novel materials. Improving production methods can result in cost reduction by achieving economies of scale. Moreover, by utilizing advanced materials that offer increased capacitance per volume, it may be possible for ultra capacitors to become smaller in size while still maintaining the same energy ability, leading to a greater competitive edge in terms of cost.

-

Ultracapacitor strive to achieve the optimal equilibrium of energy density

They provide brief, intense outbursts of energy, ideal for tasks such as regenerative braking in electric cars. Energy density is their weak point - they hold much less energy per size unit than batteries. Picture embarking on a lengthy journey in an electric car fueled exclusively by ultra capacitors. Stopping every few miles to "refuel" would make the journey far from smooth. This restriction on energy density prevents ultra capacitors from being the only power source in applications that need long distances, such as electric vehicles for long journeys. Nevertheless, scientists are working tirelessly to close this divide. They are researching new materials and electrode designs to potentially boost the energy density of ultra capacitors while maintaining their current strengths.

Ultra Capacitors Market Segment Analysis

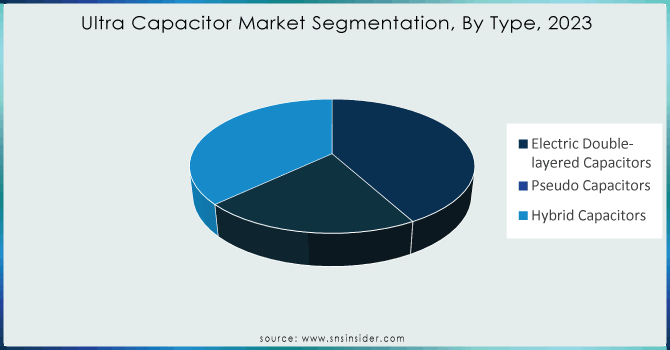

By Type

Electric Double-layered Capacitors hold the largest segment in Ultracapacitor market share with 42% in 2023, EDLCs provide a well-developed and advanced technology, supported by companies such as Maxwell Technologies, a key player in the ultracapacitor sector. They brag about benefits such as high power density for quick bursts of energy, and a long lifespan which ensures reliability and cost-effectiveness in the future. EDLCs are well-suited for a variety of applications due to these features. Picture a hybrid electric bus navigating through a crowded urban street. EDLCs are able to supply the rapid surges of energy necessary for accelerating at bus stops, leaving the battery to handle extended periods of power. Their strong construction means they are able to handle the challenges of regular stops and starts, making them a dependable option for public transportation. EDLCs are expected to uphold their dominant position in the ultra capacitors market as it expands, thanks to their established track record of effectiveness and adaptability.

Need any customization research on Ultra Capacitor market - Enquiry Now

By Industry

In 2023, the automotive Industry is at the forefront of integrating ultra capacitors, with a significant 40% market share. This is not solely focused on electric cars (EVs). Ultra capacitors are increasing efficiency in all areas. Picture a car accelerating seamlessly–that additional surge of power could be provided by an ultra capacitor supporting the battery. They additionally harness braking energy, lessening burden on the battery and potentially elongating its lifespan. Tesla (formerly Maxwell Technologies) and Eaton are creating ultra capacitors tailored for automobiles that are small and can endure harsh environments. It's not only electric vehicles. Another field where ultra capacitors are having an impact is in start-stop systems, which stop the engine automatically while idling to conserve fuel. As the electric vehicle movement gains momentum and the need for eco-friendly transportation increases, the automotive sector will continue to lead the way in advancing the ultra capacitor market.

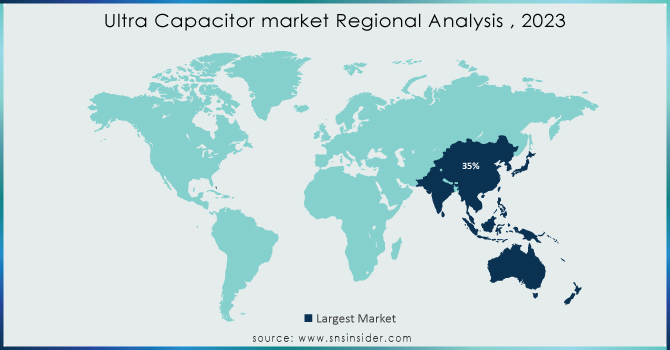

Ultra Capacitors Market Regional Analysis

Asia Pacific dominates the ultra capacitor market in 2023 with a 35% share, and this can be attributed to various factors. The increasing industrialization and urbanization in countries like China, Japan, and South Korea are driving the need for reliable energy storage solutions. Ultra capacitors are well-suited for industrial purposes due to their ability to deliver quick bursts of power and endure a high volume of charge cycles. The government's initiatives to promote renewable energy and sustainable transportation are creating a favorable setting for the usage of ultra capacitors. These energy storage systems can easily link up with green energy sources like solar and wind power, helping to stabilize the power grid by managing changes in electricity. Ultra capacitors are being combined with batteries in Asia's expanding electric vehicle sector to boost power and assist in regenerative braking operations. The large amount of top manufacturers in the region is fueling the growth, promoting innovation and technological advancements in ultra capacitors.

In 2023, North America is becoming a rapidly expanding area in the ultra capacitor market, securing a notable 25% portion. This increase can be credited to a coming together of various factors. The growing emphasis on updating the grid and securing energy is leading to a need for dependable energy storage options. Ultra capacitors are perfect for stabilizing the grid and ensuring a steady power supply due to their capacity to swiftly address changes in power demand. Picture scorching summer temperatures leading to a spike in power consumption.

Key Players

Some of the major players are CAP-XX Limited, Nippon Chemi-Con Corp., Panasonic, Maxwell Technologies, Eaton Corporation, Ls Mtron, Cornell-Dubilier Electronics, Inc., Ioxus Inc, Nawa Technologies, Paper Battery Company, Skeleton Technologies & Others players.

Recent Development in Ultra Capacitors Market

-

In Sept 2022, GODI India, the first Indian company to get BIS certification to sell lithium-ion cells made with home grown technology, has manufactured India’s first 3000F high-power supercapacitors at its Hyderabad facility.

-

In July 2023 Musashi Energy Solutions Co.,Ltd. Hybrid supercapacitors receive UL certification

| Report Attributes | Details |

| Market Size in 2023 | US$ 2.75 Billion |

| Market Size by 2032 | US$ 9.62 Billion |

| CAGR | CAGR of 15.04% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Electric Double-layered Capacitors ,Pseudo Capacitors ,Hybrid Capacitors) • By Power Type (Less than 10 Volts Modules ,10 Volts to 25 Volts Modules ,25 Volts to 50 Volts Modules ,50 Volts to 100 Volts Modules, Above 100 Volts Modules ) • By End User (Automotive ,Industrial ,Consumer Electronics ,Energy & Utilities ,Others (Aerospace & Defense, Metal & Mining, etc.)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | CAP-XX Limited ,Nippon Chemi-Con Corp. ,Panasonic ,Maxwell Technologies ,Eaton Corporation ,Ls Mtron ,Cornell-Dubilier Electronics, Inc. ,Ioxus Inc ,Nawa Technologies ,Paper Battery Company,Skeleton Technologies & Others |

| Key Drivers | • Ultra capacitors are fueling a more environmentally friendly future for industry. • Energy Chameleons, ultracapacitors adjust to meet constantly changing power requirements. |

| RESTRAINTS | • Competitive pricing • Ultracapacitors strive to achieve the optimal equilibrium of energy density |

Frequently Asked Questions

Ans. Asia Pacific is to hold the largest market share in the Ultra Capacitor market during the forecast period.

Ans. The Electric Double-layered Capacitors is leading in the market revenue share in 2023.

Ans. North America region to record the fastest growing in the Ultra Capacitor market.

Ans. The Ultra Capacitors market size was USD 2.75 Billion in 2023 & expects a good growth by reaching USD 9.62 billion till end of year2032 at CAGR about 15.04% during forecast period 2024-2032

Ans. The Ultracapacitor market is driven by demand in electric vehicles, focus on efficient energy management, and growing need for renewable energy integration.

Get in Touch