AI Infrastructure Market Report Scope & Overview:

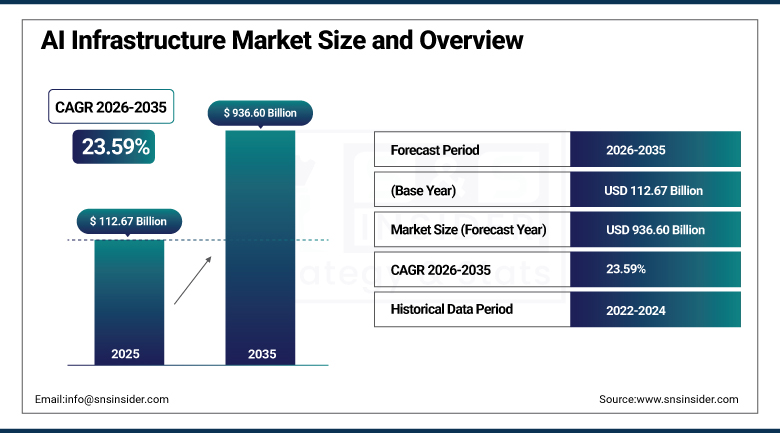

The AI Infrastructure Market size was valued at USD 112.67 Billion in 2025 and is expected to reach USD 936.60 Billion by 2035, growing at a CAGR of 23.59% from 2026 to 2035.

The AI Infrastructure Market continues to expand at a pace few technology categories have matched, as enterprises across healthcare, banking, retail, manufacturing, and automotive sectors race to build the computational foundation that generative and agentic AI workloads require. The entrenched CUDA software ecosystem and the sheer parallelism transformer model training demands continue keeping graphics processing units at the center of most infrastructure buildouts, even as field-programmable gate array and application-specific integrated circuit alternatives gain ground in inference workloads that prioritize energy efficiency and predictable latency over raw training throughput. Data-residency mandates and sector-specific regulatory frameworks continue anchoring a meaningful share of spending on-premises even as hyperscale cloud instances increasingly erode that advantage through favorable pay-per-inference economics.

Tata Consultancy Services introduced its Rapid Outcome AI platform in March 2026, a solution built on NVIDIA AI infrastructure designed to accelerate enterprise adoption of generative and agentic AI across industries including banking, retail, and manufacturing by compressing the time required to move from pilot projects to production deployment.

Market Size and Forecast

-

Market Size in 2026E: USD 139.25 Billion

-

Market Size by 2035: USD 936.60 Billion

-

CAGR: 23.59% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On AI Infrastructure Market - Request Free Sample Report

AI Infrastructure Market Trends

-

Hyperscale cloud providers are standardizing pay-per-inference pricing as multi-petaflop instances erode traditional on-premises capital expenditure advantages.

-

Financial institutions once committed to sovereign hosting are piloting confidential-compute enclaves that keep encryption keys under customer control.

-

Field-programmable gate array and application-specific integrated circuit alternatives are gaining share in inference workloads prioritizing energy efficiency.

-

Hybrid deployment patterns are proliferating as enterprises train sensitive models on-premises before shifting inference to geographic edge nodes.

-

Sovereign AI infrastructure programs are expanding rapidly as nations prioritize domestic computational independence for critical AI workloads.

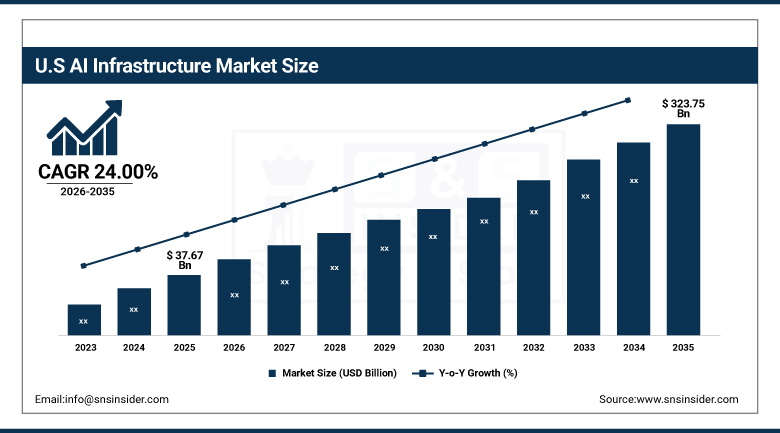

U.S AI Infrastructure Market Size Outlook

The U.S. AI Infrastructure Market was valued at USD 37.67 Billion in 2025 and is expected to reach USD 323.75 Billion by 2035, growing at a CAGR of 24.00% from 2026 to 2035.

The United States maintained a leading position in North American AI infrastructure demand, supported by the concentration of major hyperscale cloud operators, chip designers, and AI research institutions headquartered domestically. Continued enterprise capital expenditure on data center construction, combined with sustained federal and private investment in domestic semiconductor and AI infrastructure development, kept the country at the center of global AI infrastructure buildout throughout the year.

Microsoft announced an additional four billion dollar investment in September 2025 to build a second AI datacenter in Mount Pleasant, Wisconsin, bringing its total committed investment at the site to more than seven billion dollars and establishing what the company described as one of the largest and most sophisticated AI training facilities ever built, with the first facility expected to become operational in early 2026.

AI Infrastructure Market Segment Analysis

-

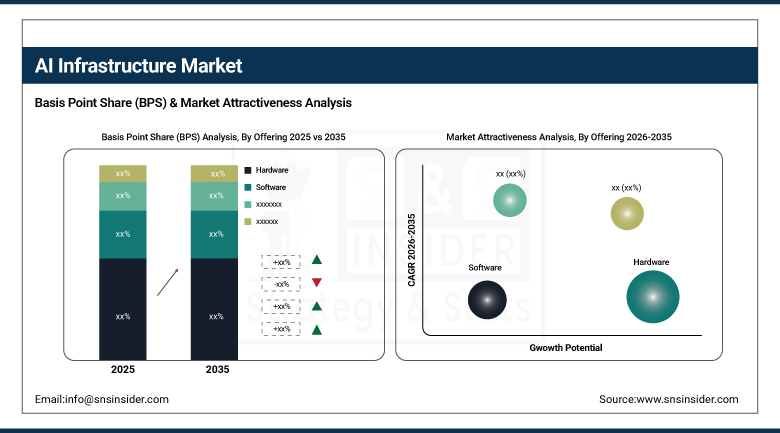

By Offering, the Hardware segment held approximately 62.40% share in 2025, while the Software segment is the fastest growing, with a CAGR of approximately 26.80%.

-

By Deployment, the On-premises segment held approximately 57.46% share in 2025, while the Cloud segment is the fastest growing, with a CAGR of approximately 15.76%.

-

By Processor Architecture, the GPU segment held approximately 88.82% share in 2025, while the FPGA and ASIC segment is the fastest growing, with a CAGR of approximately 16.89%.

-

By End Use, the Enterprises segment held approximately 54.30% share in 2025, while the Government Organizations segment is the fastest growing, with a CAGR of approximately 27.10%.

By Offering, Hardware led the market, Software grew fastest

The Hardware segment dominated the offering category in 2025, holding approximately 62.40% of total revenue, anchored by sustained enterprise capital expenditure on GPUs, specialized accelerators, and supporting server and networking equipment. The scale of physical infrastructure required to train and run large AI models keeps hardware the single largest cost component of nearly every AI infrastructure deployment, reinforcing this segment's leading position across the broader offering segmentation.

The Software segment is projected to grow at the fastest CAGR of approximately 26.80% during the forecast period, as orchestration platforms, model management tools, and AI-specific middleware increasingly determine how efficiently enterprises can extract value from their underlying hardware investment. Rising enterprise focus on shortening the path from pilot deployment to production is pushing software revenue ahead of the broader offering segmentation as buyers increasingly prioritize deployment speed alongside raw compute capacity.

By Deployment, On-premises led the market, Cloud grew fastest

The On-premises segment held the largest deployment share in 2025, at approximately 57.46%, driven by data-residency mandates and sector-specific regulatory frameworks including healthcare privacy requirements that continue favoring infrastructure kept within an organization's own physical control. Financial institutions and healthcare providers in particular continue prioritizing on-premises deployment for sensitive workloads even as cloud alternatives improve in both capability and cost efficiency.

The Cloud segment is projected to grow at the fastest CAGR of approximately 15.76% during the forecast period, as hyperscale providers deliver multi-petaflop performance at increasingly favorable economics through standardized pay-per-inference pricing models. Financial institutions that once insisted on sovereign hosting are now piloting confidential-compute enclaves that keep encryption keys under customer control, a development that continues reducing regulatory friction and pushing cloud deployment ahead of the broader deployment segmentation.

By Processor Architecture, GPU led the market, FPGA and ASIC grew fastest

The GPU segment held the largest processor architecture share in 2025, at approximately 88.82%, driven by the entrenched CUDA software ecosystem and the parallelism requirements that transformer model training fundamentally demands. That software ecosystem lock-in, built up over more than a decade of developer investment, continues keeping GPUs the default processor choice across the overwhelming majority of AI training and inference deployments worldwide.

The FPGA and ASIC segment is projected to grow at the fastest CAGR of approximately 16.89% during the forecast period, as inference workloads increasingly prioritize energy efficiency and predictable latency over the raw parallel throughput GPUs are optimized to deliver. Custom silicon developed by major hyperscalers specifically for their own inference workloads continues expanding this segment's footprint, pushing its growth rate well ahead of the broader processor architecture segmentation.

By End Use, Enterprises led the market, Government Organizations grew fastest

The Enterprise end-use type was leading in terms of end-use market share in 2025, having captured an approximately 54.30% end-use market share due to increasing awareness among organizations from healthcare, banking, retail, manufacturing, and automotive industries of the benefits associated with AI in terms of productivity improvement and innovation.

The Government Organizations end-use type will experience the highest CAGR of an approximately 27.10% during the forecast period due to increasing development of sovereign AI infrastructure projects, which is mainly due to growing concerns about computational independence in relation to crucial and defense-oriented AI workloads. Increasing investments into partnership projects between the public and private sector geared toward enhancing computational capacity within the national borders drives demand in the government sector above the others.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.60% |

|

Asia Pacific |

China |

37.90% |

|

Europe |

Germany |

27.40% |

|

Middle East & Africa |

UAE |

29.80% |

|

Latin America |

Brazil |

37.30% |

North America AI Infrastructure Market Insights

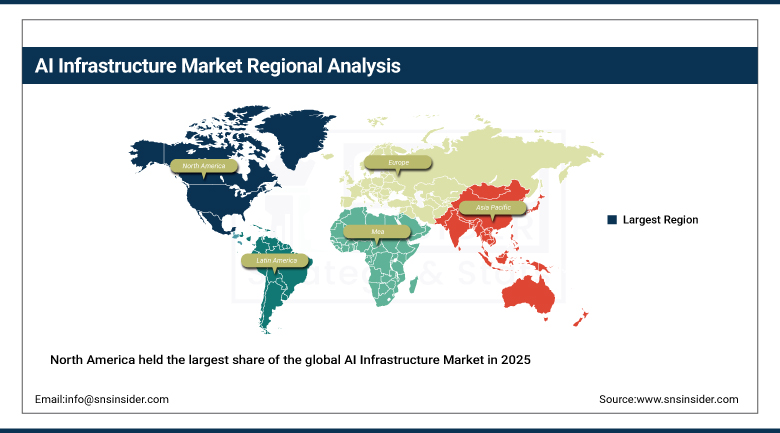

North America held the largest share of the global AI Infrastructure Market in 2025, at approximately 39.56%, supported by the region's concentration of major technology companies, hyperscale cloud operators, and AI research institutions. Substantial government initiatives supporting AI infrastructure development continued creating favorable conditions for market expansion, encouraging private sector investment while reinforcing national competitiveness in critical AI technologies.

The United States accounted for roughly 87.60% of regional revenue, reflecting its dense concentration of chip designers, hyperscale data center operators, and AI model developers. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding AI research ecosystem, keeping North America firmly ahead of every other region in this market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI Infrastructure Market Insights

Asia Pacific was the fastest-growing region in the global AI Infrastructure Market, with a CAGR near 16.44% through the forecast period, driven by aggressive government-backed AI infrastructure programs, expanding domestic semiconductor manufacturing capability, and rising enterprise AI adoption across China, Japan, and South Korea. Rapid growth in domestic cloud infrastructure investment continued driving regional demand at a pace considerably faster than more mature Western markets.

China accounted for roughly 37.90% of regional revenue, supported by aggressive national AI infrastructure policy and substantial domestic semiconductor investment aimed at reducing reliance on foreign chip suppliers. Japan and South Korea contributed significant additional regional demand through their own advanced semiconductor manufacturing and AI research sectors, reinforcing Asia Pacific's position as the clear growth leader in AI infrastructure adoption through the forecast period.

Europe AI Infrastructure Market Insights

The Europe region occupied a considerable market share of the global AI Infrastructure Market in 2025 due to increasing use of AI infrastructure by enterprises and increasing digital sovereignty initiatives among governments in the region. Germany occupied a share of 27.40% of revenue in the region due to presence of industrial manufacturing companies which have integrated AI infrastructure into next generation automation processes.

Similarly, France, UK and Nordic nations showed a somewhat parallel trend in terms of market share due to AI infrastructure investments being made across the biggest economies of the region through European Union. Increased focus on data sovereignty will continue driving European demand in future years.

MEA & Latin America AI Infrastructure Market Insights

The Middle East and Africa region recorded rapid growth in AI infrastructure adoption in 2025, driven by ambitious sovereign AI infrastructure programs and substantial government investment in computational capacity across the Gulf states in particular. The UAE accounted for roughly 29.80% of regional revenue, supported by national AI strategy investment and large-scale data center construction partnerships with leading global technology providers.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.30% of regional revenue, where growing enterprise cloud and AI adoption continued to support category growth. Mexico and Argentina followed a similar trajectory as regional digital infrastructure investment expanded further through the remainder of the forecast period.

Growth Drivers: Enterprise AI adoption and hyperscale capital expenditure

Rising enterprise adoption of generative and agentic AI continues to be the central force behind AI infrastructure market growth, as companies across virtually every industry sector transition AI from experimental pilot projects into core business infrastructure. The computational demands of large language models and other complex AI algorithms continue necessitating a fundamental shift away from general-purpose processors toward specialized GPUs and custom accelerators capable of the parallel processing deep learning requires.

Massive hyperscale capital expenditure commitments, spanning data center construction, power infrastructure, and chip procurement, continue reinforcing this growth trajectory at a scale few other technology categories have matched. Public-private partnerships aimed at expanding national computational resources continue accelerating infrastructure buildout, while government initiatives supporting domestic AI infrastructure development create favorable conditions that encourage sustained private sector investment across nearly every major economy.

Restraints: Power constraints and GPU supply limitations

Physical limitations of energy grids continue posing a genuine constraint on AI infrastructure buildout, as data center operators increasingly struggle to secure sufficient power capacity to match the pace of GPU procurement and deployment. That power bottleneck continues forcing operators to site new facilities in locations with available grid capacity rather than purely optimal locations from a latency or connectivity standpoint.

Persistent GPU supply constraints continue extending deployment timelines across the industry, compelling operators to shift focus toward compute-efficient architectures and edge AI strategies that reduce dependence on scarce, high-demand accelerator hardware. These combined power and chip supply constraints continue to concentrate the largest AI infrastructure buildouts among the best-capitalized hyperscale operators capable of securing both power and compute allocation ahead of smaller competitors.

Opportunities: Sovereign AI programs and inference-optimized architecture

Expanding sovereign AI infrastructure programs present substantial opportunity for infrastructure providers positioned to serve nations prioritizing domestic computational independence for critical and defense-related AI workloads. Government-backed AI infrastructure investment across multiple regions continues opening new addressable demand well beyond traditional enterprise and hyperscale cloud customer bases.

Continued growth in inference-optimized processor architecture, including custom silicon developed for specific workload types, presents a further significant opportunity for chip designers capable of delivering energy-efficient alternatives to general-purpose GPU deployment. Providers positioned to serve both training-intensive and inference-optimized workloads simultaneously stand to capture a growing share of demand across an increasingly diverse set of enterprise and government AI applications through 2035.

Recent Developments:

-

2025: NVIDIA and OpenAI announced a strategic partnership in September to deploy at least ten gigawatts of NVIDIA systems for OpenAI's next-generation AI infrastructure, with NVIDIA committing to invest up to one hundred billion dollars progressively as each gigawatt of capacity comes online.

-

2025: NVIDIA joined a consortium alongside Microsoft, BlackRock, and xAI in October to acquire Aligned Data Centers for forty billion dollars, in what was described as the largest global data center transaction to date.

-

2025: Oracle disclosed in a regulatory filing in June that it had signed a thirty billion dollar cloud services agreement with an unnamed partner, a single contract exceeding the company's total cloud revenue for the entire preceding fiscal year.

AI Infrastructure Companies are:

-

Advanced Micro Devices, Inc.

-

Intel Corporation

-

Google LLC

-

Amazon Web Services, Inc.

-

Microsoft Corporation

-

IBM Corporation

-

Hewlett Packard Enterprise Company

-

Cisco Systems, Inc.

-

Broadcom Inc.

-

Super Micro Computer, Inc.

-

Lenovo Group Limited

-

Huawei Technologies Co., Ltd.

-

Oracle Corporation

-

Meta Platforms, Inc.

-

Tata Consultancy Services Limited

-

Cerebras Systems Inc.

-

Graphcore Limited

-

SambaNova Systems, Inc.

AI Infrastructure Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 112.67 Billion |

| Market Size by 2035 | USD 936.60 Billion |

| CAGR | CAGR of 23.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Offering (Hardware, Software) • by Deployment (On-premises, Cloud, Hybrid) • by Processor Architecture (GPU, FPGA, ASIC) • by End Use (Enterprises, Government Organizations, Cloud Service Providers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Google LLC, Amazon Web Services, Inc., Microsoft Corporation, IBM Corporation, Dell Technologies Inc., Hewlett Packard Enterprise Company, Cisco Systems, Inc., Broadcom Inc., Super Micro Computer, Inc., Lenovo Group Limited, Huawei Technologies Co., Ltd., Oracle Corporation, Meta Platforms, Inc., Tata Consultancy Services Limited, Cerebras Systems Inc., Graphcore Limited, SambaNova Systems, Inc. |

Frequently Asked Questions

The AI Infrastructure Market is expected to grow at a CAGR of 23.59% from 2026 to 2035.

The AI Infrastructure Market was valued at USD 112.67 Billion in 2025.

Rising enterprise adoption of generative and agentic AI combined with massive hyperscale capital expenditure is the major growth factor.

The Hardware segment held approximately 62.40% share in 2025.

North America held the largest share of the AI Infrastructure Market in 2025, at approximately 39.56%, while Asia Pacific was the fastest-growing region.

Get in Touch