Alumina Based Products Market Report Scope & Overview:

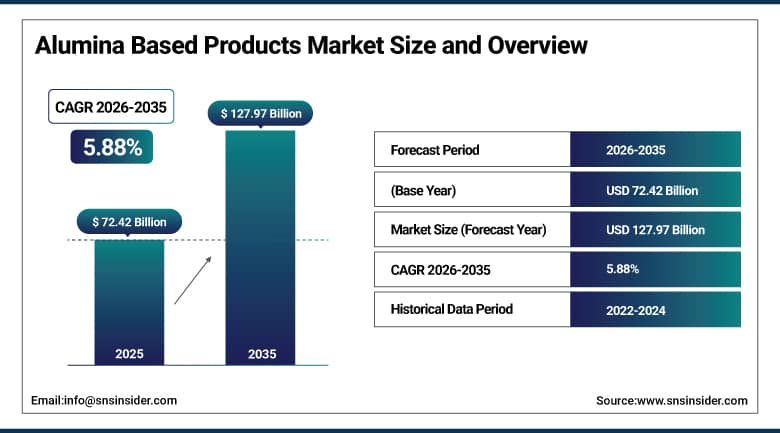

The Alumina Based Products Market was valued at USD 72.42 billion in 2025 and is expected to reach USD 127.97 billion by 2035, growing at a CAGR of 5.88% from 2026–2035.

The alumina based products market is witnessing steady growth in the global market owing to increasing demand from refractories and abrasives industries. Rising adoption in metallurgy, steel production, and high temperature industrial processes is supporting market expansion. Manufacturers are focusing on high purity alumina and advanced alumina composites. Growing use in electronics, semiconductors, and ceramics is creating new opportunities. Advancements in material processing technologies are improving product performance. Increasing investments in EV batteries and clean energy systems are further accelerating adoption of alumina-based products.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025, global bauxite production, the primary feedstock for alumina-based products, reached approximately 400 million metric tons, with Australia accounting for about 28% of output and Guinea exceeding 20% share.

According to International Aluminum Institute Sustainability Indicators 2025, more than 70% of alumina refinery capacity worldwide is located in Asia Pacific, whereas recycling of aluminum contributes about 34% of overall aluminum production, showing increased circularity within value chains of alumina based products. Moreover, efficiency gains of energy intensive Bayer process have also helped to decrease residue intensity by more than 10%.

Market Size and Forecast:

-

Market Size 2026E: USD 76.54 billion

-

Market Size 2035: USD 127.97 billion

-

CAGR (2026 - 2035): 5.88%

-

Fastest Growing Region:North America

-

Largest Region: Asia Pacific

To Get More Information On Alumina Based Products Market - Request Free Sample Report

Alumina Based Products Market Trends:

-

Fast penetration of electric vehicles creating need for high purity alumina for batteries and thermal insulation parts globally.

-

Increased investments in renewable energy creating increased use of alumina in solar and wind energy ceramics and refractories.

-

Development in semiconductor industry creating increased demand for ultra-high purity alumina for wafers and electronic substrates globally.

-

Increased rollout of 5G networks and smart devices creating demand for high performance alumina based electronic parts.

-

Strict governmental policies regarding clean energy leading to increased adoption of alumina materials in EV and energy storage systems globally.

-

Increased innovations in high performance ceramics leading to increased use of alumina across electronic, automotive, and industrial manufacturing industries.

U.S. Alumina Based Products Market Outlook:

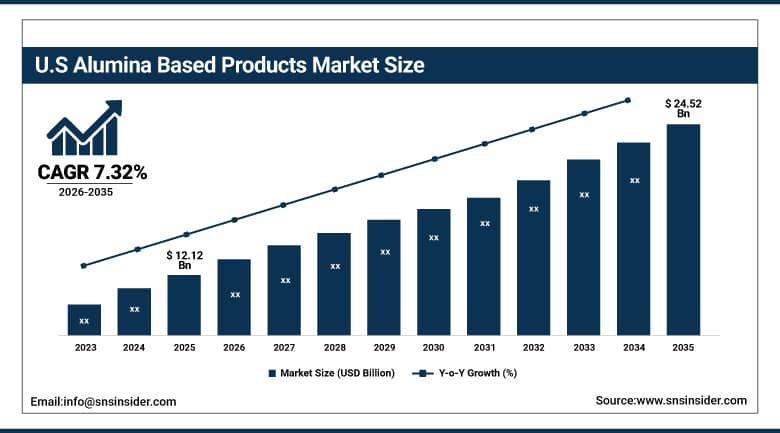

The U.S. Alumina Based Products Market was valued at USD 12.12 billion in 2025 and is expected to reach around USD 24.52 billion by 2035, growing at a CAGR of 7.32% from 2026–2035.

The U.S. alumina based products market is growing steadily owing to rising demand from refractories, abrasives, and advanced ceramics applications. Strong adoption in metallurgy, automotive, and aerospace industries is supporting stable industrial consumption. The use of alumina in electronics, semiconductors, and high purity applications has contributed to market expansion. Increasing focus on EV battery materials and clean energy technologies has generated higher demand. Development of advanced refining technologies and high-performance alumina composites is further driving market expansion.

According to the U.S. Geological Survey Mineral Commodity Summaries 2025, the U.S. alumina production remains limited, with the country relying on imports for over 95% of alumina feedstock used in aluminum and advanced ceramic applications.

According to the U.S. Environmental Protection Agency & Sustainable Materials Management guidelines, all such plants engaged in the processing of industrial minerals have to follow particulate emissions regulations based on the Clean Air Act, with 100% coverage of major refining and downstream processing of alumina. Moreover, DOE advanced materials programs state that over 70% of the U.S. high-performance ceramic and catalyst uses include alumina-based compounds.

Alumina Based Products Market Segment Analysis:

-

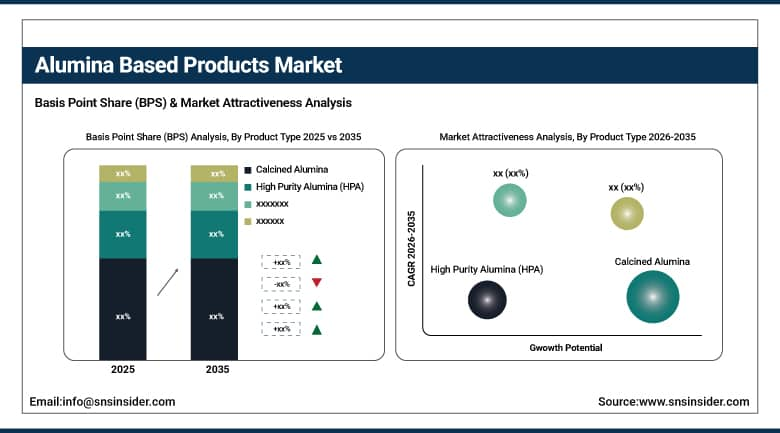

By Product Type, calcined alumina dominated the market with 38.45% share in 2025; while high purity alumina (HPA) is the fastest growing segment with CAGR of 13.07% during 2026 to 2035.

-

By Application, refractories dominated the market with 36.80% share in 2025; while electronics & semiconductors are the fastest growing segment with CAGR of 11.53% during 2026 to 2035.

-

By End Use Industry, metallurgy & steel dominated the market with 39.60% share in 2025; while electronics & electrical are the fastest growing segment with CAGR of 10.71% during 2026 to 2035.

By Product Type, calcined alumina dominated the alumina based products market, while high purity alumina (HPA) is the fastest growing segment.

The calcined alumina segment led the alumina based products market by revenue share in 2025 due to its widespread usage in the refractories, abrasives, and ceramics sectors. It is popularly used in high temperature industrial applications. It provides great thermal stability, economical prices, and excellent performance. Its high usage in the metal and steel manufacturing sectors is another driving factor. The presence of a well-established supply chain and industry acceptance further enhances its dominance in the market.

The high purity alumina (HPA) segment will witness the fastest CAGR during the forecast period owing to rising demand in the electronics, semiconductor, and lithium-ion batteries industry. It is required for LED lights and sapphire substrates. Growing usage of electric cars and energy storage devices is increasing its demand. Its superior purity and material quality make it an appropriate choice for performance-driven applications. Rapid advancements in technology and investments in clean energy industry will further fuel its growth in the market.

By Application, refractories dominated the alumina-based products market, while electronics & semiconductors are the fastest growing segment.

Refractories segment has been the dominated segment in alumina based products market with the highest share in terms of revenue in 2025. The reason behind this is their extensive application in high temperature industrial processes. They find applications in the furnaces of steel, cement kilns, and glass manufacturing units. Rising demand from metallurgy and steel industry contributes to their consumption. These materials have high thermal resistance and are very durable as well as economical; hence their significance in heavy industries. Industrial expansion also aids in their demand.

Electronics & Semiconductors segment has the fastest CAGR from 2026 to 2035 owing to the rising demand for electronics. Increasing usage of semiconductors in electric vehicles, smartphones, and smart devices leads to their increasing applications. High purity aluminum is crucial for LEDs substrates and battery separators. Development in the infrastructure of 5G network and artificial intelligence further increases their demand. Investments in high performance electronic devices help in their expansion.

By End Use Industry, metallurgy & steel dominated the alumina based products market, while electronics & electrical are the fastest growing segment.

Metallurgy & steel accounted for the largest market revenue share of the alumina based products market in 2025. The growing use of alumina products for steel manufacturing process and high temperature refractories is expected to boost the market growth. High use of alumina in blast furnaces, ladles and kilns is driving the market. Increased demand from construction, infrastructure and manufacturing industries is boosting the market growth in global regions. Continued industrialization is fueling the market demand.

Electronics & electrical is estimated to hold the fastest growing CAGR from 2026 to 2035. The growing demand for highly purified alumina in semiconductors, LED lights and electrical parts is driving the market growth. The increasing demand in the manufacture of electric vehicles, renewable energy systems and consumer electronic equipment is driving the market growth. Growing trend of miniaturized devices is further fuelling the demand in the market.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.20% |

|

Europe |

Germany |

28.70% |

|

Asia Pacific |

China |

44.90% |

|

Middle East & Africa |

UAE |

19.10% |

|

Latin America |

Brazil |

48.30% |

North America Alumina Based Products Market Insights.

North America is emerging as the fastest growing region in the Alumina Based Products Market during the forecast period, with an estimated growth rate of 7.47% in 2025. This growth is due to rapid expansion in advanced manufacturing and high value material applications. The region benefits from strong demand in metallurgy, aerospace, automotive, and electronics industries. Increasing use of high purity alumina in semiconductors and EV batteries is driving significant market acceleration across the United States and Canada. Rising adoption of advanced ceramics and refractory materials is further supporting growth momentum. Strong R&D investments are enhancing innovation capabilities in alumina based technologies.

As per the U.S. Geological Survey Mineral Commodity Summaries 2025, North America is a major consumer of alumina, whereby the United States does not have any full-capacity operating primary aluminum smelters and has to import over 80% of alumina. As per Natural Resources Canada mineral statistics, Canada mined over 3 million metric tons of aluminum, with over 90% being exported. The OECD industrial materials statistics indicate rising usage of alumina-based ceramics and catalysts in over 65% of refining and environmental applications in North American industries in 2025.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Alumina Based Products Market Insights.

Europe alumina based products market is characterized by steady growth in 2025 owing to strict environmental regulations and rising demand for sustainable industrial materials. The major countries contributing towards demand include Germany, France, United Kingdom, and Italy. Rising demand for automotive manufacturing and industrial ceramics is fueling market growth. Increased use of alumina in refractories and catalysts is propelling usage rate. Strong focus on decarbonization and circular economy policies is supporting market expansion.

As per the Raw Materials Scoreboard and Industrial Production statistics 2025 of the European Commission, EU imports more than 90% of its needs for bauxite and alumina, which suggests that there is high dependence on external sources for the production of alumina products. According to the Sustainability Indicators of the European Aluminum Association, recycling rates of aluminum packaging in Europe is above 75%.

Asia Pacific Alumina Based Products Market Insights.

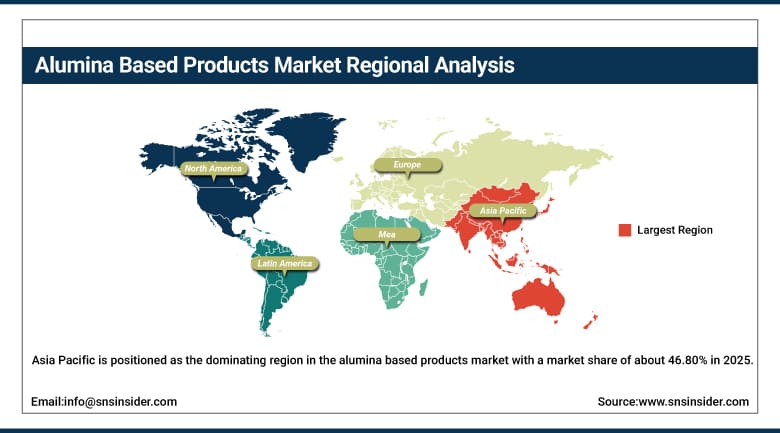

Asia Pacific is positioned as the dominating region in the alumina based products market with a market share of about 46.80% in 2025. Rapid industrial expansion and increasing steel production are driving strong demand across China, India, Japan, South Korea, and Southeast Asia. Expanding electronics manufacturing and automotive production are significantly boosting adoption. Growing demand for cost effective industrial materials is further accelerating market growth. Large scale investments in infrastructure and manufacturing support strong regional outlook.

According to the US Geological Survey Mineral Commodity Summaries 2025, China makes up 55% and more of the world’s alumina production; in addition, the Asia Pacific region as a whole serve as the leading refinement center for aluminum and alumina materials.

According to the International Aluminum Institute 2025, the worldwide alumina refinery production surpassed 140 million tons, in which China, Australia, and India were the major contributors. Moreover, more than 70% of the alumina production in the Asia Pacific region goes into the primary aluminum smelting process, whereas other industrial uses such as refractories and catalysts constitute a lower but steadily increasing portion.

Middle East & Africa and Latin America Alumina Based Products Market Insights.

The Middle East & Africa along with Latin American regions are experiencing steady growth due to expanding industrialization and increasing infrastructure development. Key contributing countries include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Investments in construction, steel production, and chemical industries are supporting market growth. Rising demand for durable refractory materials and industrial alumina is driving adoption. Growth in oil & gas and emerging manufacturing sectors is further strengthening demand across both regions.

According to the World Bank’s industrialization, the manufacturing value added for Latin America makes up about 12-13% of GDP, whereas in Sub-Saharan Africa, it is less than 10%, signifying different downstream demand intensities for the products derived from alumina. Besides, OECD Material Flow Statistics reveal rising alumina consumption along with more than 70% dependency of aluminum production on refined alumina.

Market Dynamics:

Growth Drivers: Increasing adoption of high purity alumina in electronics, EV batteries, and semiconductor applications globally

The fast development in electronic manufacturing and electric vehicles is fueling the need for high purity alumina on an international scale. HPA has applications in lithium-ion batteries, LEDs, and semiconductor substrates because of its high resistance to heat. The development of 5G technology and smart gadgets has further increased the requirement for the material. There are several emerging trends in automotive industry related to electric vehicles that have increased the use of the material in EVs and energy storage systems.

As per the International Energy Agency and Global Critical Minerals Outlook 2025 and U.S. Geological Survey Mineral Commodity Summaries 2025, there has been an exponential increase in the demand of minerals for batteries with the installation of Lithium-Ion batteries in electric cars which is over 14 million units, resulting in an increasing demand for high purity alumina required for separators and coatings. The IEA reports that EV sales constituted 18% of total car sales globally, and semiconductor manufacturing utilization in Asia was over 75%.

Restraints: Supply chain disruptions and raw material dependency creating volatility in alumina based products market

The alumina oxide-based products industry has great dependence on bauxite mines and refining plants, which are situated in certain geographic locations only. Perturbations in the processes of mining, geopolitics, and international trade affect the availability of supply across the globe. Logistical issues can have an effect on timely transportation of the raw material to consumer firms. Importing dependency in many countries leaves the industry vulnerable to price fluctuations. Environmental restrictions limit possibilities for expanding supplies.

Opportunities:Expansion of electric vehicles and renewable energy infrastructure creating strong alumina demand opportunities

As electric vehicles and renewable sources of energy are rapidly being adopted, there emerge numerous opportunities for the application of pure alumina. High-purity alumina is required as an insulation material in technologies such as batteries in electric vehicles, energy storage, and power electronics. Development and construction of installations related to solar and wind energy contribute to an increase in the application of ceramic and refractory products. There are also certain governmental policies promoting the adoption of clean energy.

As per the International Energy Agency & Global EV Outlook 2025, there has been a marked increase in the number of electric vehicles to over 40 million units globally, which accounts for more than 20% of annual sales volume in 2024, with further expected growth in 2025. As per the U.S. Geological Survey Mineral Commodity Summaries 2025 report, the production of alumina is concentrated globally, wherein China accounts for over 50% of the total alumina produced.

Recent Developments:

-

2026: Rio Tinto commissions $1.5 billion low-carbon aluminum expansion in Quebec, boosting capacity and advancing ELYSIS-based emissions reduction technology.

-

2025: Norsk Hydro reduced capital expenditure plans and optimized alumina sourcing strategy while improving upstream refinery performance and cost competitiveness.

-

2026: Rio Tinto announced 40% alumina output reduction at Yarwun refinery to extend asset life and manage tailings capacity.

-

2024: Hindalco Industries Limited expanded aluminium recycling capacity through Novelis investments supporting circular economy and low carbon production.

Alumina Based Products Market Key Players are:

-

Alcoa Corporation

-

Rio Tinto

-

United Company RUSAL

-

Norsk Hydro ASA

-

China Hongqiao Group Limited

-

Aluminum Corporation of China Limited (CHALCO)

-

Hindalco Industries Limited

-

Emirates Global Aluminium

-

South32 Limited

-

Alumina Limited

-

Altech Chemicals Limited

-

Almatis GmbH

-

Nabaltec AG

-

Imerys S.A.

-

Saint-Gobain

-

3M Company

-

Kyocera Corporation

-

Nippon Light Metal Holdings Company

-

Resonac Holdings Corporation

-

UBE Corporation

Alumina Based Products Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 72.42 Billion |

| Market Size by 2035 | USD 127.97 Billion |

| CAGR | CAGR of 5.88% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Calcined Alumina, Activated Alumina, Tabular Alumina, Fused Alumina, Hydrated Alumina, Alumina Trihydrate, High Purity Alumina (HPA)) • By Application (Refractories, Abrasives, Catalysts, Ceramics, Water Treatment, Polishing & Surface Finishing, Electronics & Semiconductors) • By End Use Industry (Metallurgy & Steel, Oil & Gas, Chemical & Petrochemical, Automotive, Electronics & Electrical, Water Treatment Industry, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alcoa Corporation, Rio Tinto, United Company RUSAL, Norsk Hydro ASA, China Hongqiao Group Limited, Aluminum Corporation of China Limited (CHALCO), Hindalco Industries Limited, Emirates Global Aluminium, South32 Limited, Alumina Limited, Altech Chemicals Limited, Almatis GmbH, Nabaltec AG, Imerys S.A., Saint-Gobain, 3M Company, Kyocera Corporation, Nippon Light Metal Holdings Company, Resonac Holdings Corporation, UBE Corporation |

Frequently Asked Questions

The alumina based products market is expected to grow at a CAGR of 5.88% from 2026 to 2035.

The alumina based products market was valued at USD 72.42 billion in 2025.

Major growth factors include rising demand from refractories and abrasives, metallurgy and steel production, electronics and semiconductors, EV batteries, clean energy applications, and advancements in high purity alumina and ceramics technologies.

Calcined Alumina dominated the market in 2025 due to wide use in refractories, abrasives, ceramics, and high temperature industrial applications.

Asia Pacific dominated the alumina based products market in 2025 due to strong industrial growth, steel production, electronics, and manufacturing expansion.

Get in Touch