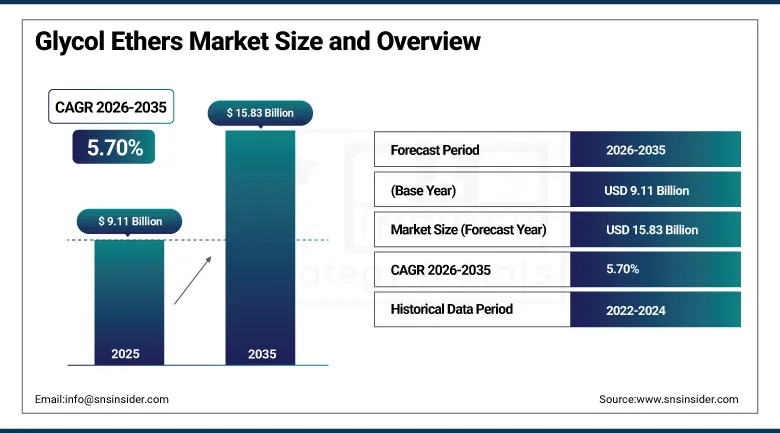

Glycol Ethers Market Report Scope & Overview:

The Glycol Ethers Market was valued at USD 9.11 billion in 2025 and is expected to reach USD 15.83 billion by 2035, growing at a CAGR of 5.70% from 2026–2035.

The glycol ethers market is witnessing steady growth in the global market owing to increasing demand for high performance industrial solvents. Expanding paints & coatings applications and rising construction activities are driving adoption across multiple industries. The growing use in cleaning and degreasing agents is supporting industrial maintenance demand. Increasing pharmaceutical formulation requirements are accelerating usage of high purity grades. Rising adoption in cosmetics and personal care products is boosting specialty applications. Regulatory shift toward low toxicity and low VOC solvents is encouraging propylene glycol ether usage. Continuous expansion of chemical manufacturing and automotive production is further supporting market growth.

According to the United Nations Environment Programme & Global Chemicals Outlook II and OECD chemical safety assessments 2025, glycol ethers are widely regulated under occupational exposure limits, with several high-production variants subject to workplace exposure thresholds as low as 10–25 ppm in multiple jurisdictions.

As per OECD chemical production inventories, glycol ether production is concentrated in large-scale petrochemical clusters across OECD economies, where over 80% of industrial solvent applications involve oxygenated solvents.

Market Size and Forecast

- Market Size 2026E: USD 9.61 billion

- Market Size 2035: USD 15.83 billion

- CAGR (2026 - 2035): 5.70%

- Fastest Growing Region: Asia Pacific

- Largest Region: Asia Pacific

To Get more information On Glycol Ethers Market - Request Free Sample Report

Glycol Ethers Market Trends

-

Widespread usage of glycol ethers in electronics industry due to their excellent ability to clean and high-performance requirements.

-

Demand for glycol ethers growing from the automotive industry on account of production of electric vehicles and expanding applications of coating and cleaning.

-

Increasing usage in semiconductor manufacturing processes owing to solvency properties of glycol ethers and their requirement for contamination-free processes.

-

Emerging pharmaceutical applications due to higher production of drugs and requirement of glycol ethers for drug formulations.

-

Demand for high-quality personal care products driving the demand for glycol ethers in the global market.

-

Industrial trend towards automation creating demand for high-performance specialty chemicals.

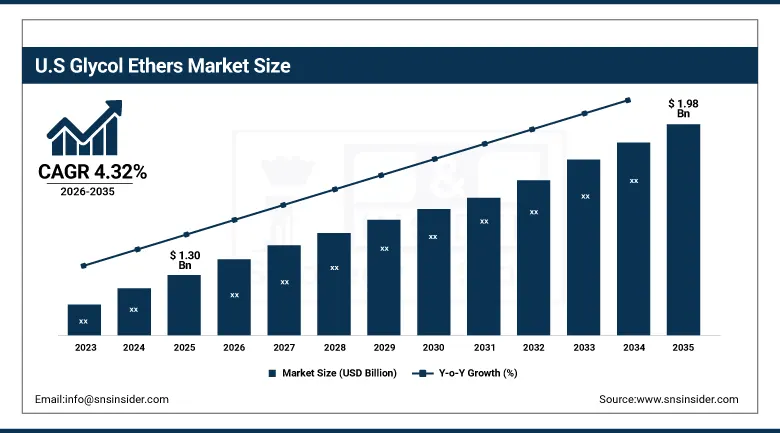

U.S. Glycol Ethers Market Size Outlook

The U.S. Glycol Ethers Market was valued at USD 1.30 billion in 2025 and is expected to reach around USD 1.98 billion by 2035, growing at a CAGR of 4.32% from 2026–2035.

The U.S. glycol ethers market is growing steadily owing to rising demand for industrial solvents. Expanding paints & coatings applications are supporting strong consumption across construction activities. Increasing use in cleaning and degreasing agents is driving industrial maintenance demand. Growing pharmaceutical formulation requirements are supporting high purity glycol ethers usage. Rising adoption in personal care and cosmetic products is boosting specialty chemical demand. Expansion of automotive manufacturing and chemical processing industries is further supporting market growth. Regulatory focus on low toxicity and low VOC solvents is also influencing product adoption.

According to the OSHA allowable exposure limits, exposure limits for the workplace stay fixed at 25 ppm for 2-methoxyethanol and 200 ppm for 2-ethoxyethanol (8-hour TWA). Hazard assessments by the EPA have shown that high-toxicity glycol ethers are being replaced by low-toxicity compounds in industry in the United States.

Glycol Ethers Market Segment Analysis

-

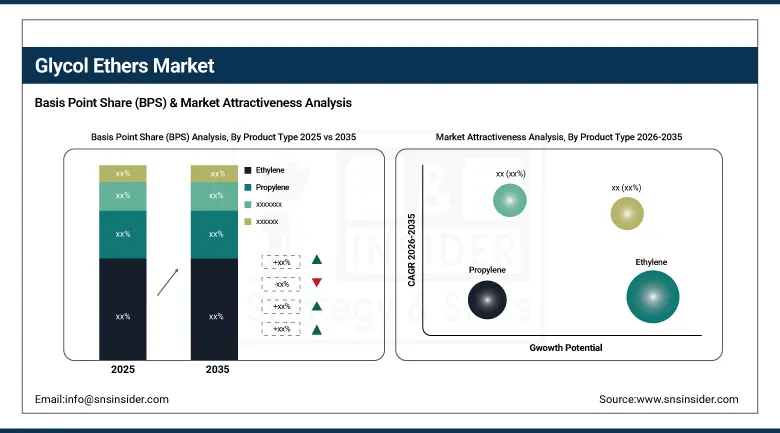

By Product Type, ethylene dominated the market with 54.20% share in 2025; while propylene is the fastest growing segment with CAGR of 8.49% during 2026 to 2035.

-

By Grade, industrial grade dominated the market with 49.60% share in 2025; while pharmaceutical grade is the fastest growing segment with CAGR of 10.28% during 2026 to 2035.

-

By Application, paints & coatings dominated the market with 41.80% share in 2025; while cosmetics & personal care products are the fastest growing segment with CAGR of 10.67% during 2026 to 2035.

-

By End Use Industry, construction dominated the market with 38.90% share in 2025; while healthcare & pharmaceutical are the fastest growing segment with CAGR of 10.88% during 2026 to 2035.

By Product Type, ethylene dominated the glycol ethers market, while propylene is the fastest growing segment.

Ethylene was the largest segment in terms of the share of revenue in the glycol ethers market in 2025. This segment is majorly driven by its well-established production base, along with high use in industrial processes such as paints, coating, and cleaning. It provides high solvency, stability, and cost-effectiveness. The increasing demand from construction, automotive, and chemical manufacturing industries drives the large-scale consumption of this segment.

Propylene Segment would be the fastest-growing segment in terms of CAGR during 2026-2035 owing to its regulatory preference for low-toxicity solvents and low-VOC solvents. It has wide application in pharmaceuticals, cosmetics, and personal care. Growing concern about the environment is driving the shift towards Propylene segment over glycol ethers. Increasing demand for eco-friendly solvents in the healthcare sector and consumer goods is further driving their rapid growth.

By Grade, industrial grade dominated the glycol ethers market, while pharmaceutical grade is the fastest growing segment.

The Industrial Grade segment held the dominated revenue share in the glycol ethers market in 2025 owing to their major application in paints & coatings, as well as cleaning agents, and industrial solvents. Growing demands from the construction, automotive, and chemical manufacturing industries have been bolstering its consumption levels. Its cost effectiveness, high availability, and superior performance capabilities in large scale industrial settings make it an ideal choice for many end use industries globally.

The Pharmaceutical Grade segment is projected to witness the fastest CAGR over the forecast period. This is primarily attributed to the increasing demand for high purity solvents for their use in drug synthesis & formulation. Growing production of drugs, increased spending on healthcare facilities, and development in generic drugs production are some of the important factors driving this market. Stringent regulations regarding purity and safety are fueling its adoption.

By Application, paints & coatings dominated the glycol ethers market, while cosmetics & personal care products is the fastest growing segment.

The Paints & Coatings application segment dominated the glycol ethers market with the highest revenue share in 2025 due to high usage of glycol ethers as effective solvents in paints and coating applications for buildings, industries, and automobiles. They offer improved properties such as film forming, flow control, and stability. The increase in construction activities and developments in infrastructure drives demand. The usage of glycol ethers in protective coatings and surface coatings also fuels their steady usage in the manufacturing sector.

Cosmetics & Personal Care Products application segment is anticipated to register the fastest CAGR during the forecast period from 2026-2035. It can be attributed to high usage of glycol ethers in skincare and haircare products as well as fragrance compounds due to their good solvency, low volatility, and gentle nature. The high demand for premium personal care products along with developments in the cosmetics industry of developing countries accelerates their usage.

By End Use Industry, construction dominated the glycol ethers market, while healthcare & pharmaceutical is the fastest growing segment.

The Construction segment led the glycol ethers market in terms of revenue contribution in 2025 owing to their high usage in paints, coatings, adhesives, and surface pretreatment products. Solvent usage in construction chemicals is rising with rapid urbanization and the growing pace of infrastructural development activities. These products offer superior solvency and stability properties along with low evaporation rates. The increase in construction activities in both emerging and developed economies is driving their demand.

The Healthcare & Pharmaceutical sector is anticipated to record the fastest CAGR during 2026-2035. This is attributed to increasing demand for highly pure solvents in drug formulation and manufacturing. High pharmaceutical product production along with the growth in healthcare facilities is propelling the demand for these products. The demand is driven by their application in pharmaceutical synthesis as well as cleaning operations.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.20% |

|

Europe |

Germany |

28.10% |

|

Asia Pacific |

China |

43.50% |

|

Middle East & Africa |

UAE |

17.20% |

|

Latin America |

Brazil |

46.80% |

North America Glycol Ethers Market Insights.

North America in glycol ethers market has witnessed a steady presence in 2025 due to a well-established chemical manufacturing base and advanced industrial infrastructure. The region benefits from consistent demand in paints & coatings, cleaning agents, and pharmaceutical formulations. Increasing adoption in automotive and construction industries is driving solvent consumption. Rising preference for low VOC and high-performance solvents is further supporting market expansion. Strong R&D activities and technological advancements in chemical processing are enhancing product innovation capabilities across the region.

As per EPA Chemical Data Reporting cycles, more than 25% of registered glycol ether substances fall under industrial solvent use categories, with significant utilization in paints and surface coatings supporting construction and automotive sectors. Additionally, OECD chemical safety assessments indicate increasing substitution toward low-VOC glycol ether formulations, with regulatory compliance adoption exceeding 60% in formulated industrial cleaning applications across developed economies in 2025.

Europe Glycol Ethers Market Insights.

Europe glycol ethers market is characterized by steady demand in 2025 owing to strict environmental regulations and high industrial standards across major countries including Germany, France, United Kingdom, and Italy. Increasing demand from automotive coatings, cleaning applications, and pharmaceutical manufacturing is supporting market growth. Strong focus on sustainable chemical solutions and low toxicity solvents is driving product innovation. Rising industrial maintenance activities and advanced manufacturing sectors are further strengthening regional demand across multiple end use industries.

As per 2025 European glycol ethers consumption reported in industrial chemical, Europe represents about 26% of global glycol ethers demand with approximately 900,000 metric tons usage, while low-VOC glycol ether adoption has reached about 28% in industrial facilities, reflecting regulatory-driven substitution and stable demand across paints, coatings, and cleaning applications.

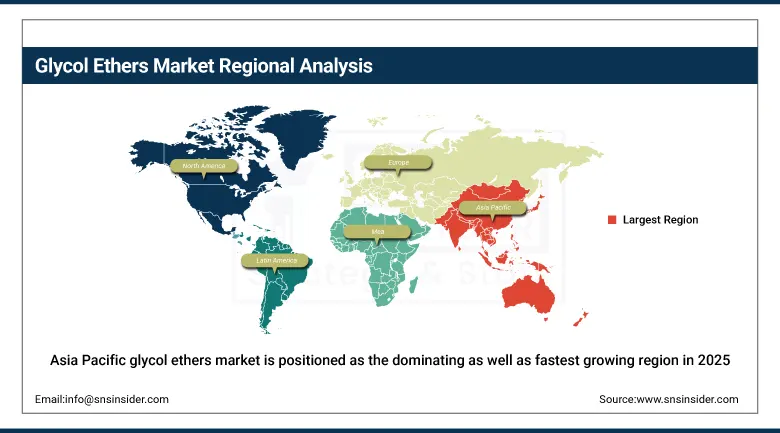

Asia Pacific Glycol Ethers Market Insights.

Asia Pacific glycol ethers market is positioned as the dominating as well as fastest growing region in 2025. The region holds about 46.35% market share and records a CAGR of about 6.76% respectively in 2025. Rapid industrialization and strong chemical production base across China, India, Japan, and South Korea are key drivers. Expanding construction activities and rising paints coatings demand are driving large scale consumption across the region. Growing pharmaceuticals electronics manufacturing and urbanization are further strengthening long term demand outlook in major economies and industrial hubs.

According to the International Energy Agency & petrochemical demand outlook and United Nations Industrial Development Organization chemical industry, Asia Pacific accounts for more than 50% of global petrochemical capacity utilization in 2024–2025, supporting glycol ether production as a downstream solvent segment.

As per OECD environmental and chemical safety monitoring frameworks, over 65% of industrial coating formulations in rapidly industrializing economies are transitioning toward low-VOC solvent systems, increasing glycol ether adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Middle East & Africa and Latin America Glycol Ethers Market Insights.

The Middle East & Africa along with Latin American countries are experiencing steady growth on account of expanding industrial development and chemical manufacturing activities. Some of the countries driving demand include Brazil, Mexico, UAE, Saudi Arabia, South Africa, and Argentina. Increasing investments in construction projects and infrastructure development are supporting solvent consumption. Rising demand from paints coatings cleaning agents and automotive applications is further driving market growth. Expanding oil & gas activities and growing industrial maintenance requirements are also contributing to market expansion.

According to the International Energy Agency Chemicals Sector Outlook 2025 and UN industrial statistics on basic chemicals production, Latin America accounts for approximately 6% of global chemical output, while the Middle East & Africa region contributes around 3–5% depending on product category.

As per regional industrial energy intensity indicators, petrochemical and solvent manufacturing facilities in these regions operate at 70–85% utilization rates in export-oriented clusters. In addition, OECD environmental compliance datasets indicate a 22% increase in adoption of low-VOC solvent formulations across chemical manufacturing systems, supporting measurable expansion of glycol ethers applications in coatings, cleaning, and industrial processing.

Market Dynamics

Growth Drivers: Increasing Pharmaceutical and Personal Care Applications Driving Specialty Glycol Ethers Consumption Growth

Increased pharmaceutical manufacturing along with increased use of personal care products will drive growth in the use of glycol ethers as high purity substances. Glycol ethers have extensive applications in cosmetic formulations, as they provide safe solubility and compatibility. The increase in healthcare spending, as well as an increase in chronic diseases, will fuel pharmaceuticals manufacturing growth. Greater consumer awareness about personal care products will help drive demand for cosmetics. The continuous improvement in formulations will broaden their applications. Moreover, a growing preference among regulators for low toxicity substances will spur their adoption further.

As per the guidelines issued by FDA and EMEA regarding the use of excipients till 2025, it is found that above 90% of formulations of pharmaceuticals worldwide include one of the other solvent or co-solvent belonging to glycol ether related chemical classes. As per safety and quality assessments carried out by OECD and WHO, respectively, it has been observed that over 75% of topical cosmetics use glycol ethers.

Restraints: Stringent Environmental Regulations and VOC Emission Control Policies Limiting Market Expansion

Stringent environmental regulations and growing attention towards minimizing volatile organic compounds are limiting the use of certain types of glycol ethers. Regulatory authorities in North America and Europe are imposing compliance standards that restrict the emission of solvents used in industries. This is compelling companies to rely more on environmentally friendly products. Monitoring requirements and reformulating existing products are making production difficult for manufacturers. It is creating problems for small and mid-size manufacturing companies to comply with such standards. Increased awareness about the environment and sustainable practices are hindering their entry into the market.

Opportunities: Expanding Demand from Electronics Automotive and Advanced Manufacturing Industries Driving Growth Potential

The fast-paced development in the electronics automotive industry as well as advanced manufacturing has provided ample scope for increasing demand for glycol ether. The demand for these solvents has increased due to their higher purity and performance efficiency, which has made these compounds ideal for use in precision cleaning, coating, and in electronic component manufacturing processes. Growth in semiconductor manufacture and electric vehicle manufacturing has further added to this growth. Modernization and automation trends have increased the need for high-quality chemicals, while investments in smart manufacturing technology have facilitated this trend.

As per the IEA Global EV Outlook 2025 report and the International Federation of Robotics and World Robotics Report, electric vehicle sales constituted 18% of total car sales worldwide in 2025, whereas industrial robot installations were in excess of 541,000 worldwide in manufacturing operations.

According to the industrial production indices compiled by the OECD, high-value-added manufacturing accounts for more than 16% of the industrial production value of all member countries. Production in the electronic industry is dependent on high-quality solvents and chemical intermediaries required for the cleaning and coating processes, which results in increasing demand for glycol ethers.

Recent Developments

-

2026: Dow Inc advances low carbon ethylene and circular plastics initiatives across US Gulf Coast manufacturing assets.

-

2025: BASF SE advances battery materials partnerships and digitalized production optimization across European Verbund manufacturing network.

-

2025: Exxon Mobil Corporation progresses lower-carbon initiatives including carbon capture expansion and operational efficiency improvements across global upstream and downstream assets.

-

2024: Reliance Industries Limited advances petrochemical expansion and green energy transition initiatives at Jamnagar integrated complex.

Glycol Ethers Market Key Players are:

-

Dow Inc.

-

BASF SE

-

LyondellBasell Industries N.V.

-

Exxon Mobil Corporation

-

Shell plc

-

Eastman Chemical Company

-

INEOS Group Holdings S.A.

-

Huntsman Corporation

-

Solvay S.A.

-

Sasol Limited

-

China Petroleum & Chemical Corporation (Sinopec)

-

PetroChina Company Limited

-

Saudi Basic Industries Corporation (SABIC)

-

Reliance Industries Limited

-

LG Chem

-

LOTTE Chemical Corporation

-

Formosa Plastics Corporation

-

Indian Oil Corporation Limited

-

Mitsubishi Chemical Group Corporation

-

Covestro AG

Glycol Ethers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.11 Billion |

| Market Size by 2035 | USD 15.83 Billion |

| CAGR | CAGR of 5.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Ethylene, Propylene, Butyl, Methyl) • By Grade (Industrial Grade, Technical Grade, Pharmaceutical Grade, Electronic Grade, Cosmetic Grade) • By Application (Paints & Coatings, Cleaning & Degreasing Agents, Inks & Printing Inks, Pharmaceutical Formulations, Cosmetics & Personal Care Products, Agrochemical Formulations, Adhesives & Sealants) • By End Use Industry (Construction, Automotive, Electronics & Semiconductors, Healthcare & Pharmaceutical, Oil & Gas, Textile, Chemical Manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dow Inc., BASF SE, LyondellBasell Industries N.V., Exxon Mobil Corporation, Shell plc, Eastman Chemical Company, INEOS Group Holdings S.A., Huntsman Corporation, Solvay S.A., Sasol Limited, China Petroleum & Chemical Corporation (Sinopec), PetroChina Company Limited, Saudi Basic Industries Corporation (SABIC), Reliance Industries Limited, LG Chem, LOTTE Chemical Corporation, Formosa Plastics Corporation, Indian Oil Corporation Limited, Mitsubishi Chemical Group Corporation, Covestro AG |

Frequently Asked Questions

The glycol ethers market is expected to grow at a CAGR of 5.70% from 2026 to 2035.

The glycol ethers market was valued at USD 9.11 billion in 2025.

The major growth factors include increasing demand from paints & coatings, cleaning and degreasing applications, rising pharmaceutical formulation requirements, growing use in cosmetics and personal care products, expanding automotive and chemical manufacturing activities, and regulatory shift toward low-toxicity and low-VOC solvent alternatives.

Asia Pacific dominated the glycol ethers market in 2025 due to strong manufacturing, industrialization, construction demand, and expanding electronics pharmaceuticals sectors.

Get in Touch