Anal Cancer Market Size & Trends:

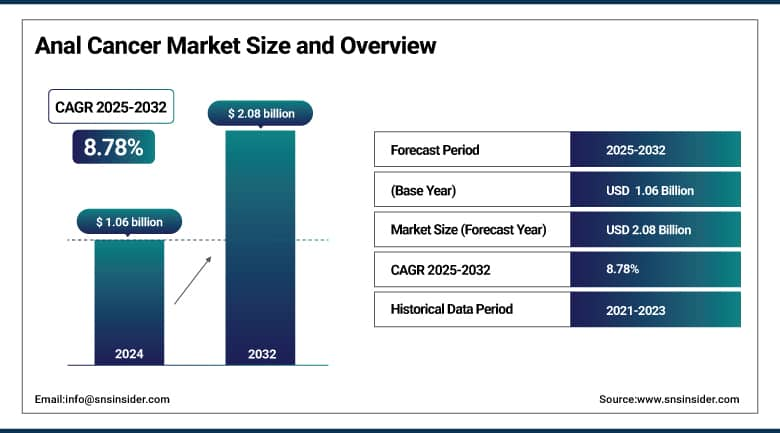

The Anal Cancer Market size was valued at USD 1.06 billion in 2024 and is expected to reach USD 2.08 billion by 2032, growing at a CAGR of 8.78% over 2025-2032.

The global anal cancer market is likely to shift due to an increasing burden of HPV-associated anal cancer, awareness growth and increased screening practices. The anal cancer market and demand for early awareness tools, including the broader utilization of Naveris’ NavDx liquid biopsy test for molecular residual disease monitoring are also driving the market. Approvals of new agents by the FDA, specifically the approval of Retifanlimab (Zynyz) in advanced disease, have and will continue to change treatment, showing a great deal of innovation in the immuno-oncology world. Market growth is further driven by new systemic therapy guidelines from ASCO (2025) for stages I-III, which promote standardization and increase the number of patients eligible for treatment.

Growth in R&D for biomarker discovery, particularly in HPV-positive patient populations such as MD Anderson’s Phase II study for predictive biomarkers, suggests a rich pipeline of innovation. Increased funding for preventive screening in high-risk populations, such as HIV+ MSM (men who have sex with men) highlighted in cost-effective analysis published on Medscape, also bolsters market analysis of anal cancer. Moreover, the market of anal cancer is growing due to expanding government and private financial support for diagnostics and immunotherapies.

June 2025 – A recent study found that broad based screening in high-risk groups such as HIV-positive population has the potential to decrease #analcancer mortality by 50%, further corroborating the increasing market needs in #anal cancerr for advanced early detection.

These major developments have been compounded by recent regulatory events. In the meantime, FDA approvals in 2024 and 2025, such as for Retifanlimab in both the monotherapy and combination settings, have confirmed the place of immunotherapy in first-line treatment for R/M disease. In the meantime, the screening landscape widens around the world in line with revised clinical guidance and risk-based modelling that broadens the target population. Advances coming from anal cancer companies such as Incyte (producer of Zynzy and Naveris — these are beginning to set the new standard in both treatment and diagnostics. Additionally, the anal cancer market is seeing increasing use of precision oncology treatment approaches, liquid biopsies, and AI-powered patient stratification, supporting clinicians in decisions and providing personalized therapies.

January 2025 -Significant milestone in increased coverage for testing with liquid biopsy, NavDx test, to include anal cancer monitoring- Highlights the R&D investment and diagnostic innovation that is underpinning and driving the growth of the anal cancer market size.

To Get More Information On Anal Cancer Market - Request Free Sample Report

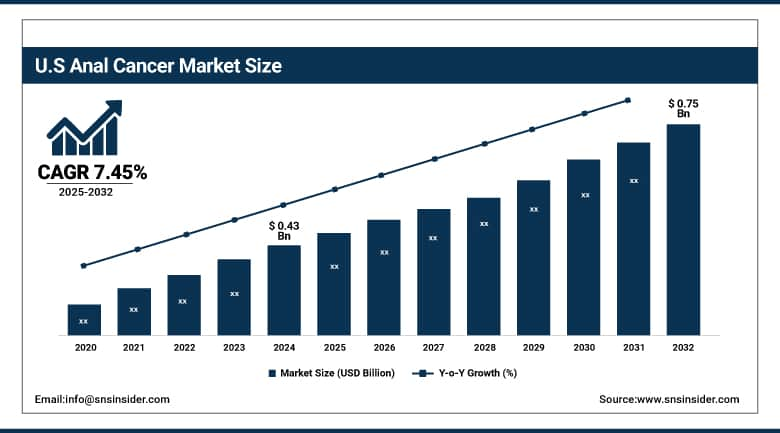

The U.S. Anal Cancer Market size was valued at USD 0.43 billion in 2024 and is expected to reach USD 0.75 billion by 2032, growing at a CAGR of 7.45% over 2025-2032.

Anal Cancer Market Dynamics:

Drivers:

-

Rising Therapeutic Innovation, Early Detection Focus, and Targeted Investments Propel Market Expansion

Growing research in the field of immune checkpoint inhibitors and biomarker-oriented therapies are the major support to drive the anal cancer market. New agents such as Taletrectinib (ROS1+ NSCLC) are part of a widening oncology pipeline that may be accessible to anal cancer on 'cohort' lines path which also drives innovation. Studies of immunotherapy are now largely focused on personalized medicine, and there are a large number of phase II/III trials investigating combinations with chemoradiotherapy. In addition, academic institutions and biotechs continue to invest in translational research – the NIH alone budgeted more than USD 20 billion for HPV-related cancer research in 2024.

On the screening side, new guidelines for high-resolution anoscopy (HRA) and AI-supported cytology tools are coming into clinical practice, improving diagnostic efficiency. The increasing frequency among immunodeficient patients becomes a requirement for customized treatment. Guidelines such as the NCCN guidelines have provided much more structured treatment pathways, making access and reimbursement easier for patients. Taken together, increased awareness, investment and policy are driving anal cancer market analysis and boosting overall trajectory.

Restraints:

-

Low Awareness, Late Diagnosis, and Clinical Trial Challenges Hinder Market Growth

Although there has been some movement, the market for anal cancer continues to encounter obstacles such as underdiagnosis and a lack of understanding beyond high-risk groups. More than 30% of cases are still diagnosed at regional or distant stage, with concomitantly poorer outcomes and higher costs of treatment. On the other hand, in low- and middle-income regions, the shortage of skilled personnel and resources (such as HRAs and molecular-based diagnosis) causes many people to lose opportunities for early diagnosis. Supply-side problems include lack of trial diversity and lack of efficient recruitment, with only a 2023 PubMed analysis finding that just 12% of anal cancer trials had participants of diverse races or ethnicity, restricting generalizability.

Regulatory hurdles also remain, especially for rare subtypes or coinfected (HIV) patients, which could delay the time to approval. Pharmaceutical capital for R&D is also often firmly focused on higher incidence cancers, which impacts R&D on anal cancer. These systemic deficiencies are stifling innovation and preventing the anal cancer market share from achieving maximum potential. Without greater funding, broader screening requirements will prevent market acceleration due to detection, equity, and access barriers.

Anal Cancer Market Segmentation Analysis:

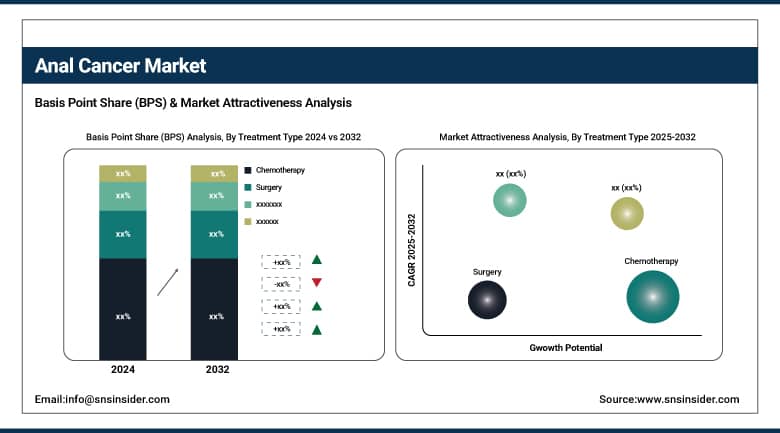

By Treatment Type

Chemotherapy continued to be the most-prescribed therapy in 2024 with a 49% market share for anal cancer, as its presence in chemoradiation regimens for locally advanced squamous cell carcinoma had become standard of care. Mitomycin and 5-fluorouracil are the standard agents for cytotoxic therapy throughout the world. The patient has been a clinical standard accepted for the extensive availability of wide practice, and in guidelines, chemotherapy is commonly the default option in resource-limited to high-income settings.

Immunotherapy is the fastest growing treatment segment, but it is keyed to a growing uptake of checkpoint inhibitors, specifically PD-1/PD-L1 antibodies, in the advanced or treatment-resistant setting. Late-stage trial data and growing regulatory approvals are driving its use as monotherapy and in combination therapy. Additionally, an enhanced patient selection based on personalized approaches with immune biomarker profiling is driving higher efficacy and less side effects, which is also accelerating the adoption and incorporation of immunotherapy in the anal cancer market share analysis.

By Type

In 2024, the anal cancer market was led by squamous cell carcinoma, which represented more than 60% of all diagnosed cases of the disease. Its incidence is highly associated with high-risk human papillomavirus (HPV) infections, especially HPV-16, and is predominantly observed in the HIV-positive population and men who have sex with men (MSM). This has resulted in specific screening programs and focused development of therapy, and is the main topic of clinical and basic research.

Conversely, adenocarcinoma is now the most rapidly growing segment, mainly due to better diagnostic imaging and molecular profiling, which in turn result in more accurate detection of malignancies in the anorectal transition zone. Greater attention to and recognition of the less-common histological subtypes in screening and research settings is contributing to its increasing rate of detection. Such developments have been helping enable better staging and personalization of treatment regimens, in turn, driving further growth in this submarket of the overall anal cancer market analysis.

By End-User

Hospitals & clinics dominated the market, accounting for more than 68% share in 2024, as they were the key centers of diagnosis, treatment, and post-treatment. These provide comprehensive cancer services, surgery, radiation, and multidisciplinary care and are the preferred option for the majority of patients. Their dominance is also reinforced by a centralization of expertise and state-of-the-art imaging facilities.

Research & Academic Institutes are anticipated to be the fastest-growing end-user, driven by a rise in translational research and clinical trials. Fueled by increased investment from governmental and private entities, these organizations are driving the creation of new diagnostics, immunotherapeutic techniques, and biomarker-guided treatments. Partnering with biotech companies and more government funding in HPV-related oncology research are stimulating innovation. Their influence in the global anal cancer market is growing at a meteoric rate, especially in early drug development and testing.

Anal Cancer Market Regional Insights:

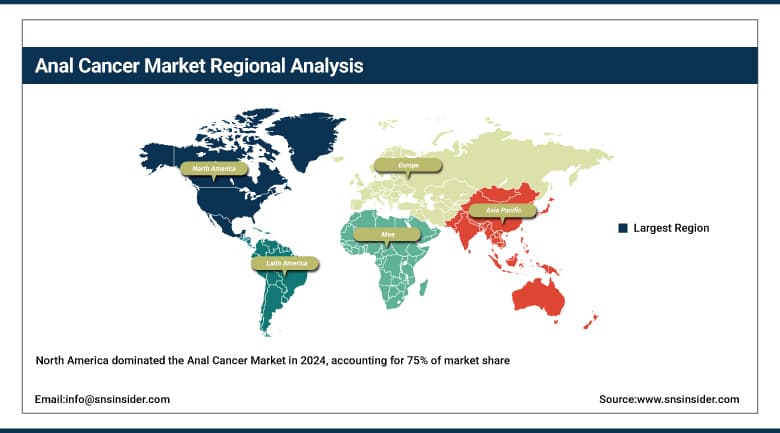

The global anal cancer market in 2024 was led by North America on account of high prevalence of disease, well developed healthcare infrastructure, and significant clinical research activities. The U.S is the dominating region with over 75% of the North America market share, which is backed by the extreme presence of the HPV screening programs, an increase in awareness, and a strong FDA pipeline for immunotherapy approvals such as Retifanlimab. Its dominance is reinforced by having the most elite academic cancer centers and high rates of health spending. The country with the fastest growth in the region was Canada, against a backdrop of a growing number of HPV-based screening strategies and the widening of public health funding for the detection of anal cancer in high-risk groups (especially HIV-positive individuals and MSM). Further, higher participation in global clinical trials is expanding access to new treatments, thereby enlarging the market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

The second largest market for anal cancer is the Europe, with domination being claimed by well-regulated cancer registries, screening programs and national guidelines. This is largely driven by proactive measures such as the National Anal Cancer Screening Programme for at risk groups and significant government funding toward HPV vaccination. There is also a lot of market activity seen in Germany and France through clinical research and the integration of immunotherapy into oncology care. The fastest-growing country in the region is Poland, where modernizing healthcare and enhanced involvement in EU-backed cancer trials are fuelling demand. Increased diagnostic reach and greater treatment penetration are driving anal cancer market growth in Western and Eastern Europe.

The fastest growing Asia Pacific is expected to be the fastest growing global anal cancer market driven by a growing cancer burden, growing access to healthcare and increasing acceptance of precision diagnostics. Japan is the regional leader in the market due to its aging patients, high testing of HPV and early introduction of screening for anal cancer among those prone to be immunocompromised. Japan’s robust pharmaceutical industry and nationwide insurance for the treatment of cancer help Japan maintain its supremacy over the market. India is a hot spot of cancer, growing at a brisk pace due to increasing awareness, burgeoning cancer infrastructure, and a rise in public-private participation in cancer treatment facilities. The increasing investment in HPV vaccination and cost-effective screening devices is speeding up market entry, particularly in cities, and fuelling the region’s strong growth trajectory.

Anal Cancer Market Key Players:

Leading anal cancer companies active in the market include Amgen, Eli Lilly, Bristol-Myers Squibb, Merck, Novartis, Celgene, Pfizer, Sanofi, GlaxoSmithKline, Johnson & Johnson, Roche, and Hospira.

Recent Developments in the Anal Cancer Market:

-

In June 2025, at ASCO 2025, Pfizer unveiled data across its cancer pipeline, including next-generation molecules poised to advance treatment options in rare and common tumor types.

-

In May 2025, Amgen’s Nplate (romiplostim) significantly reduced chemotherapy-induced thrombocytopenia, enabling 84% of patients to continue full-dose therapy compared to 36% on placebo, potentially transforming supportive care protocols in oncology.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.06 billion |

| Market Size by 2032 | USD 2.08 billion |

| CAGR | CAGR of 8.78% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Carcinoma In Situ, Squamous Cell Carcinoma, Melanoma, Adenocarcinoma, Basal Cell Carcinoma, and Others) • By Treatment Type (Chemotherapy, Surgery, Radiation Therapy, and Immunotherapy) • By End-User (Hospitals & Clinics, Research & Academic Institutes, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Amgen, Eli Lilly, Bristol-Myers Squibb, Merck, Novartis, Celgene, Pfizer, Sanofi, GlaxoSmithKline, Johnson & Johnson, Roche, and Hospira. |

Frequently Asked Questions

Ans: North America dominated the Anal Cancer market.

Ans: There has been some movement, the market for anal cancer continues to encounter obstacles such as underdiagnosis and a lack of understanding beyond high-risk groups.

Ans: Growing research in the field of immune checkpoint inhibitors and biomarker-oriented therapies are the major support to drive the anal cancer market.

Ans: The market is expected to reach USD 2.08 billion by 2032, increasing from USD 1.06 billion in 2024.

Ans: The Anal Cancer market is anticipated to grow at a CAGR of 8.78% from 2025 to 2032.

Get in Touch