Analytical Instrumentation Market Report Scope & Overview:

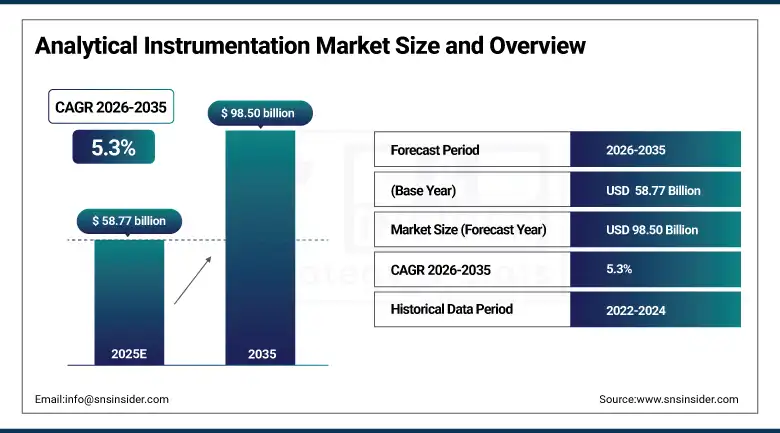

The Analytical Instrumentation Market was estimated at USD 58.77 Billion in 2025 and is expected to reach USD 98.50 Billion by 2035 and grow at a CAGR of 5.3% during 2026-2035.

Analytical Instrumentation Market growth is poised to maximize due to the modifiable nature of increasing R&D investments in pharmaceuticals & biotechnology, stringent regulatory requirements for quality control of food and environmental vaccines, and technological advancements enabling high sensitivity, automation, and seamless integration of data. Global demand for precision diagnostics, life sciences research and process analytical technology in diverse industry verticals will continue to drive uptake for spectroscopy, chromatography, PCR, and sequencing systems during the forecast period.

Market Size and Forecast:

-

Market Size in 2025: USD 58.77 Billion

-

Market Size by 2035: USD 98.50 Billion

-

CAGR: 5.3% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Analytical Instrumentation Market - Request Free Sample Report

Key Analytical Instrumentation Market Trends:

-

Accelerated adoption of high-throughput screening and automated systems in pharmaceutical and biotechnology R&D to reduce time-to-market for new therapies.

-

Increasing integration of artificial intelligence and machine learning for predictive analytics, instrument calibration, and real-time data interpretation.

-

Growing demand for portable, handheld analytical devices for on-site environmental monitoring, food safety testing, and point-of-care diagnostics.

-

Rise of multi-omics research (genomics, proteomics, metabolomics) driving advanced sequencing, spectrometry, and cytometry solutions.

-

Stringent global regulations regarding drug safety, food authenticity, and environmental pollution boosting investment in compliant analytical technologies.

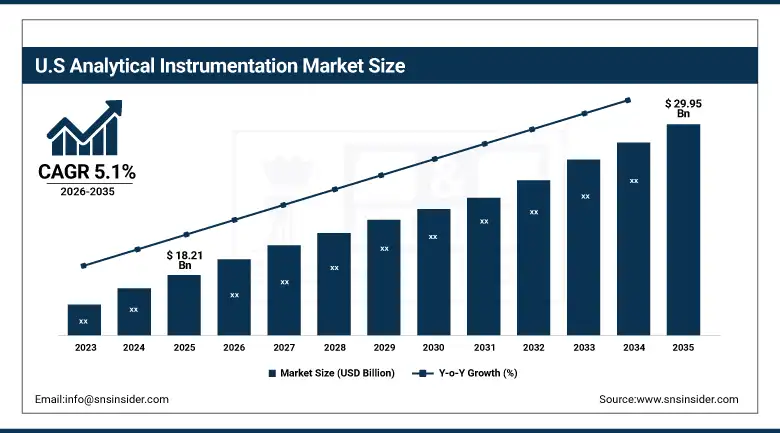

The U.S. Analytical Instrumentation Market is estimated at USD 18.21 Billion in 2025 and is projected to reach USD 29.95 Billion by 2035, growing at a CAGR of 5.1% during 2026-2035. The U.S. market is propelled by its leading position in pharmaceutical and biotech R&D, significant federal funding for life sciences, advanced healthcare infrastructure, and strong regulatory frameworks from the FDA and EPA mandating rigorous quality and safety testing.

Analytical Instrumentation Market Growth Drivers:

-

Rising Pharmaceutical and Biotech R&D Investments, Regulatory Compliance Mandates, and Technological Advancements in Automation and Precision Drive Market Growth

High R&D spending by pharmaceutical and biotechnology companies for drug discovery and development is one of the key factors driving the global Analytical Instrumentation Market, followed by quality control. The global pressure on various industries to comply with stringent regulatory standards concerning product safety in pharmaceuticals, food & beverages, and environmental monitoring is driving investments in reliable, high-performance analytical tools. Ongoing technological innovation in the form of increasingly automated, simple-to-use and connected instruments with higher sensitivity and throughput, continues to further reduce adoption barriers across academic, industrial and clinical laboratories, driving further market growth.

In 2024, pharmaceutical R&D spending surpassed USD 260 billion globally, with a significant portion allocated to advanced analytical technologies for characterizing complex biologics and ensuring regulatory compliance, directly fueling instrument demand.

Analytical Instrumentation Market Restraints:

-

High Capital and Maintenance Costs, Complexity of Operation, And Budget Constraints in Academic and Small Labs Restrain Widespread Market Penetration

The Analytical Instrumentation Market is likely to face restraints from the high cost of initial acquisition along with significant ongoing expenses for maintenance, reagents, and skilled personnel to operate advanced systems. Less sophisticated environments with low technical expertise may find this hard to adopt as the solution of high-end instruments can be very complex. Many academic institutions, small-to-medium enterprises (SMEs) and developing regions face budget constraints and thus act to recycle these instruments as slowly and with as much delay as possible, while the latest generations of an analytical solution sit and gather dust.

Analytical Instrumentation Market Opportunities:

-

Expansion Into Emerging Economies, Growth in Point-Of-Care and Portable Testing, And Convergence with IoT and Cloud Data Platforms Unlock New Revenue Streams

The growing healthcare and industrial infrastructure in emerging economies in Asia-Pacific, Latin America, and the Middle East, where rising local production and regulatory harmonization are generating demand, offer substantial market potential. Innovation in small, reliable, and networked point-of-care and portable analyzers for field applications is being fueled by the move toward decentralized testing. Additionally, remote monitoring, predictive maintenance, and collaborative data analysis are made possible by the integration of analytical tools with cloud-based data management platforms and Internet of Things (IoT) connectivity, creating new service-based and subscription income models for manufacturers.

The portable analytical instrument segment is projected to grow at a CAGR exceeding 7% through 2035, fueled by environmental monitoring mandates and the need for rapid on-site decision-making in sectors, such as agriculture and mining.

Analytical Instrumentation Market Segment Analysis:

-

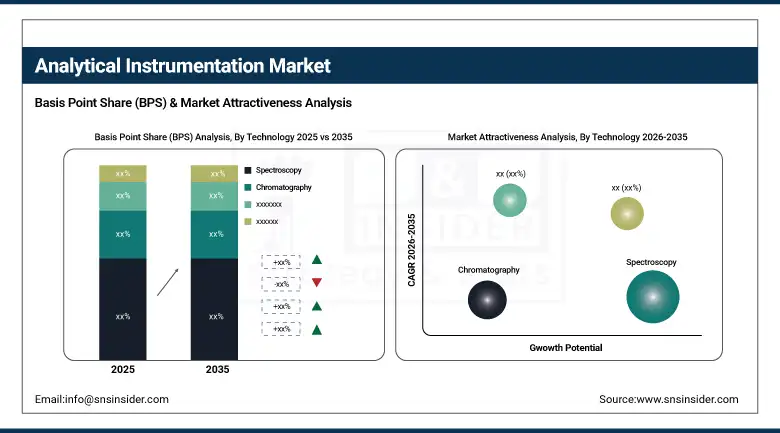

By Technology, Spectroscopy dominated with a 28.4% share in 2025, and Sequencing is expected to grow at the fastest CAGR of 7.1% from 2026 to 2035.

-

By Product, Instruments dominated with a 65.8% share in 2025, and Software & Informatics is expected to grow at the fastest CAGR of 6.9% from 2026 to 2035.

-

By Application, Life Sciences Research & Development dominated with a 35.7% share in 2025, and Clinical & Diagnostic Analysis is expected to grow at the fastest CAGR of 6.2% from 2026 to 2035.

By Technology, Spectroscopy Solutions Lead Market Share, While Sequencing Technology Exhibits Fastest Growth Driven by Genomics and Precision Medicine

Spectroscopy, including molecular and atomic techniques, holds the largest market share due to its versatile applications across pharmaceuticals, chemicals, and environmental testing for qualitative and quantitative analysis. The sequencing segment is expected to grow with the fastest CAGR during the forecast period, propelled by plummeting costs per genome, expanding applications in oncology, rare diseases, and infectious disease surveillance, and continuous innovation in next-generation and third-generation sequencing platforms.

By Product, Instruments Dominate Revenue, While Software and Informatics Solutions Experience Accelerated Growth Through Demand for Data Management and AI Integration

Instruments constitute the core revenue-generating product segment, encompassing the physical hardware for analysis. The Software & Informatics segment is expected to grow at the fastest growth during the forecast period, as laboratories increasingly require sophisticated data management, analysis, visualization, and compliance tools to handle the massive, complex datasets generated by modern instruments, integrating AI for deeper insights and workflow automation.

By Application, Life Sciences R&D Holds Largest Market, While Clinical and Diagnostic Analysis Shows Robust Growth Fueled by Personalized Medicine and Rapid Diagnostics

Life Sciences Research & Development remains the largest application area, due to a wide array of instruments for basic research, drug discovery, and development. The Clinical & Diagnostic Analysis segment is growing rapidly, driven by the global trend toward personalized medicine, which relies on advanced instrumentation for genetic, proteomic, and metabolomic profiling, and the ongoing need for rapid, accurate diagnostic testing in healthcare settings.

Regional Insights

North America Analytical Instrumentation Market Insights:

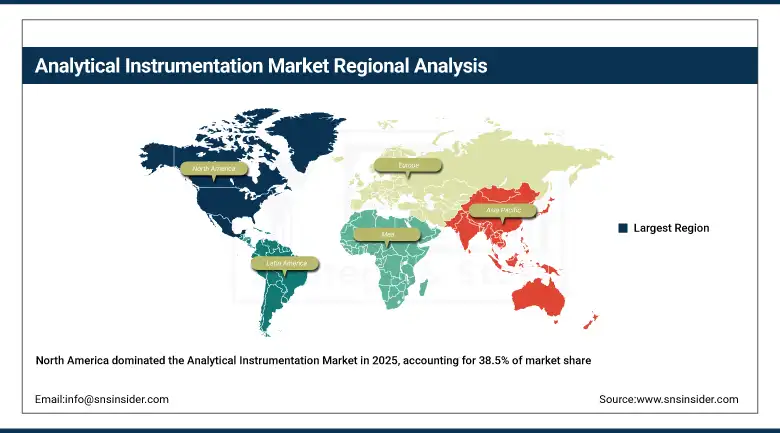

Due to the presence of significant pharmaceutical and biotech companies, top academic and research institutions worldwide, and stringent regulatory frameworks (FDA, EPA), North America is expected to hold a 38.5% market share for analytical instruments in 2025. Market leadership and innovation in precision analytical tools are maintained by high healthcare costs, early adoption of cutting-edge technology, and substantial venture capital funding in the life sciences.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Analytical Instrumentation Market Insights:

With more than 85% of the North American market, the U.S. is the dominant country. Strengths include a strong diagnostics industry, significant NIH and private funding, concentrated R&D hubs (San Diego and Boston), and expertise in creating high-throughput, AI-powered analytical platforms for commercial and research labs.

Europe Analytical Instrumentation Market Insights:

Europe holds a 29.2% market share for analytical instruments in 2025. Strong chemical and pharmaceutical manufacturing, strict EU regulations (REACH, EU MDR/IVDR), major environmental monitoring programs, and sophisticated healthcare systems that prioritize quality control and accurate diagnosis, particularly in Germany, the U.K., and Switzerland, all contribute to growth.

With its robust manufacturing sector, especially in chemicals and automobiles that require precise material analysis, extensive network of research institutes, such as Fraunhofer and Max Planck, and leadership from domestic instrument manufacturers, Germany is the largest market in Europe and is driving demand for high-precision laboratory and process analytical equipment.

Asia Pacific Analytical Instrumentation Market Insights:

Asia Pacific is the fastest-growing area in 2025, with a projected CAGR of 6.8% between 2026 and 2035. The expansion of biopharmaceutical production (particularly in China, India, and South Korea), growing government and private investments in healthcare infrastructure, growing concerns about food safety and the environment, and the growing outsourcing of R&D and clinical trials to the region are the main drivers of this growth.

China is driving APAC's growth with its "Made in China 2025" initiative, which encourages high-tech manufacturing, a sizable domestic pharmaceutical market, growing instrument production localization, and significant public investment in national genomics and precision medicine projects. These factors have created a huge demand for sophisticated analytical systems.

Latin America (LATAM) and Middle East & Africa (MEA) Analytical Instrumentation Market Insights

In 2025, LATAM and MEA hold a combined share of approximately 7.5%. The region’s growth is steady, driven by the developing healthcare infrastructure, investments in oil & gas and mining (requiring environmental and material analysis), and gradual strengthening of regulatory frameworks for food and drug safety, though adoption is often paced by economic and budgetary constraints.

Competitive Landscape:

Thermo Fisher Scientific Inc. was founded in 2006 through the merger of Thermo Electron and Fisher Scientific and is headquartered in the U.S. It is the undisputed global leader in the analytical instrumentation market, offering an unparalleled portfolio across chromatography, spectrometry, microscopy, and molecular spectroscopy. Its strength lies in providing integrated workflow solutions, from sample preparation to data analysis, serving pharmaceutical, biotech, academic, and industrial customers globally.

-

In February 2025, Thermo Fisher Scientific launched a new high-resolution orbitrap mass spectrometer with unprecedented sensitivity and speed, designed to accelerate proteomics and metabolomics research in complex biological samples.

Agilent Technologies, Inc. was spun off from Hewlett-Packard in 1999 and is headquartered in the U.S. A premier leader in life sciences, diagnostics, and applied chemical markets, Agilent is renowned for its chromatography (LC/GC), mass spectrometry, spectroscopy, and bioinformatics solutions. The company emphasizes innovation in workflows for pharma QA/QC, food testing, environmental analysis, and clinical research.

-

In January 2025, Agilent introduced an advanced gas chromatography system with intelligent pressure programming and enhanced connectivity features, targeting higher throughput and lower operational costs for petrochemical and environmental laboratories.

Danaher Corporation, through its operating company SCIEX and other subsidiaries, is a major force in the analytical instrument space. Danaher's business model focuses on strategic acquisitions and continuous operational improvement. SCIEX is a leader in capillary electrophoresis and mass spectrometry, particularly in the biopharmaceutical and clinical diagnostics markets, known for its high-performance quantification and characterization capabilities.

-

In March 2025, Danaher's SCIEX division released a new software suite integrating artificial intelligence to automate method development and anomaly detection in LC-MS workflows, significantly reducing hands-on time for analysts.

PerkinElmer, Inc. was founded in 1937 and is headquartered in the U.S. The company provides a broad portfolio focused on diagnostics, life sciences, and applied markets. It is a key player in areas such as sequencing preparation, liquid handling automation, molecular spectroscopy, and imaging. PerkinElmer has a significant presence in applied markets, such as food, environmental, and industrial quality control.

-

In February 2025, PerkinElmer launched a fully automated, high-throughput next-generation sequencing (NGS) library preparation system, aiming to streamline genomic workflows in large-scale population health and clinical research studies.

Analytical Instrumentation Market Key Players:

-

Thermo Fisher Scientific Inc.

-

Agilent Technologies, Inc.

-

Danaher Corporation

-

Waters Corporation

-

PerkinElmer, Inc.

-

Shimadzu Corporation

-

Bruker Corporation

-

Bio-Rad Laboratories, Inc.

-

JEOL Ltd.

-

Mettler-Toledo International Inc.

-

Illumina, Inc.

-

PacBio

-

Oxford Nanopore Technologies

-

Becton, Dickinson and Company (BD)

-

Sartorius AG

-

Eppendorf SE

-

F. Hoffmann-La Roche Ltd

-

Malvern Panalytical

-

ZEISS Group

-

Metrohm AG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 58.77 Billion |

| Market Size by 2035 | USD 98.50 Billion |

| CAGR | CAGR of 5.3% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Polymerase Chain Reaction, Spectroscopy, Microscopy, Chromatography, Flow Cytometry, Sequencing, Microarray, Others) • By Product (Instruments, Services, Software) • By Application (Life Sciences Research & Development, Clinical & Diagnostic Analysis, Food & Beverage Analysis, Forensic Analysis, Environmental Testing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Danaher Corporation, Waters Corporation, PerkinElmer, Inc., Shimadzu Corporation, Bruker Corporation, Bio-Rad Laboratories, Inc., JEOL Ltd., Mettler-Toledo International Inc., Illumina, Inc, PacBio, Oxford Nanopore Technologies, Becton, Dickinson and Company (BD), Sartorius AG, Eppendorf SE, F. Hoffmann-La Roche Ltd, Malvern Panalytical, ZEISS Group, Metrohm AG |

Frequently Asked Questions

Ans: High Capital and Maintenance Costs, Complexity of Operation, And Budget Constraints in Academic and Small Labs Restrain Widespread Market Penetration

Ans: The Instruments product segment dominated the Analytical Instrumentation Market in 2025.

Ans: The North American region dominated the Analytical Instrumentation Market in 2025.

Ans: The CAGR of the Analytical Instrumentation Market is 5.3% During the forecast period of 2026-2035.

Ans: The projected market size for the Analytical Instrumentation Market is USD 98.50 Billion by 2035.

Get in Touch