Artificial Intelligence (AI) In Diagnostic Imaging Market Report Scope & Overview:

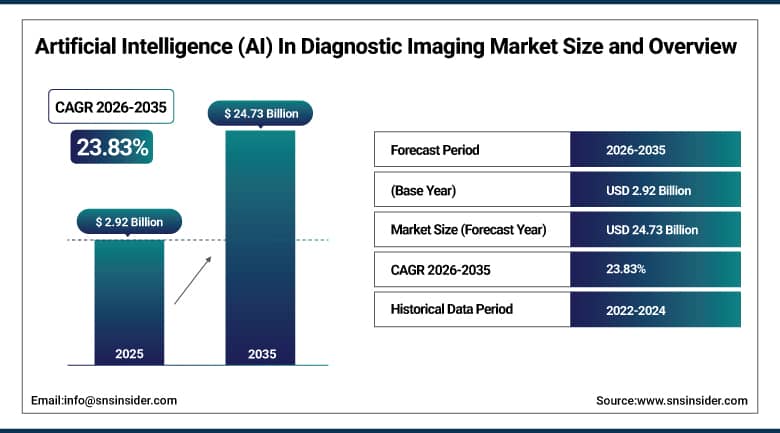

The Artificial Intelligence (AI) In Diagnostic Imaging Market was valued at USD 2.92 Billion in 2025 and is projected to reach USD 24.73 Billion by 2035, expanding at a CAGR of 23.83% during the forecast period 2026–2035.

The global Artificial Intelligence (AI) in Diagnostic Imaging market is experiencing a substantial growth acceleration due to the increasing integration of AI-enabled diagnostic algorithms, increasing workloads for imaging across healthcare systems, and the rising adoption of cloud-based radiology workflows. Hospitals and suppliers of diagnostic imaging are increasingly employing deep learning software, automated platforms for image interpretation and AI-assisted systems for workflow management, to enhance diagnostic accuracy, reduce the burden on radiologists and improve clinical productivity. Further expansion of the smart hospital ecosystems, digital healthcare infrastructure and AI-integrated imaging platforms are also further supporting long-term market commercialization across developed and emerging healthcare markets.

Several healthcare technology providers expanded commercialization of generative AI-supported radiology workflow systems integrated with real-time diagnostic decision support and automated image prioritization platforms in 2025-2026.

Market Size and Forecast:

-

Market Size 2026E: USD 3.61 Billion

-

Market Size 2035: USD 24.73 Billion

-

CAGR6: 23.83% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Artificial Intelligence (AI) In Diagnostic Imaging Market - Request Free Sample Report

Artificial Intelligence (AI) In Diagnostic Imaging Market Trends:

-

Rising adoption of AI-powered radiology workflow automation systems across healthcare facilities.

-

Increasing commercialization of cloud-based diagnostic imaging analytics platforms.

-

Growing deployment of AI-enabled oncology and cardiovascular imaging solutions globally.

-

Expansion of smart hospital infrastructure integrated with predictive imaging technologies.

-

Increasing integration of deep learning algorithms for automated disease detection and clinical decision support.

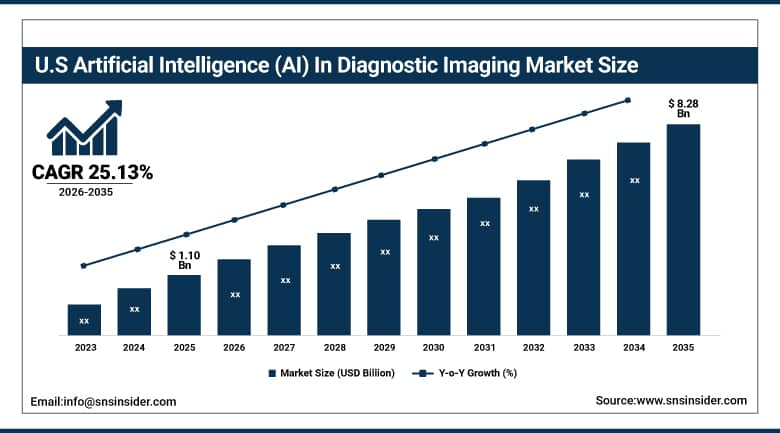

U.S. Artificial Intelligence (AI) In Diagnostic Imaging Market Size Outlook:

The U.S. Artificial Intelligence (AI) In Diagnostic Imaging Market was valued at USD 1.10 billion in 2025 and is expected to reach approximately USD 8.28 billion by 2035, expanding at a CAGR of 25.13% during 2026–2035.

The U.S. is a huge market for Artificial Intelligence (AI) in Diagnostic Imaging because of the quick adoption of AI-assisted radiology technologies, good healthcare IT infrastructure, and growing demand for workflow optimization in imaging centers and hospitals. Healthcare providers are increasingly adopting cloud-enabled imaging analytics platforms, AI-enabled disease detection software, and predictive diagnostic systems for improving operational efficiency and reducing diagnostic turnaround time. Commercial adoption is also being fueled by growing investments in precision medicine, enterprise imaging infrastructure and digital health transformation programmers across the country.

Several vendors of AI-enabled healthcare products in the U.S. augmented their rollouts of radiology reporting systems that leverage generative AI and are tied to image analysis automation and platforms that streamline clinical workflows in 2026.

Artificial Intelligence (AI) In Diagnostic Imaging Market Segment Analysis:

-

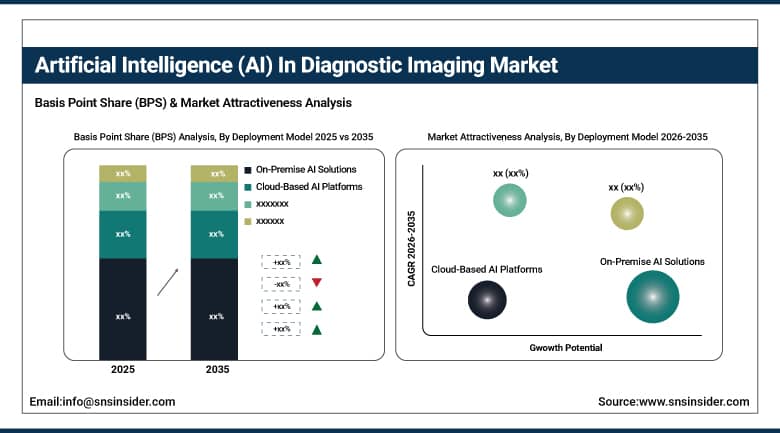

By Deployment Model, on-premise AI solutions dominated the market with 52.00% share in 2025, while cloud-based AI platforms are projected to witness the fastest growth with 28.25% CAGR during the forecast period.

-

By Imaging Modality, computed tomography (CT) dominated the market with 38.00% share in 2025, while X-ray & mammography is projected to witness the fastest growth with 24.86% CAGR during the forecast period.

-

By Application, oncology imaging dominated the market with 42.00% share in 2025, while cardiology & other imaging applications are projected to witness the fastest growth with 24.60% CAGR during the forecast period.

-

By End User, hospitals & health systems dominated the market with 58.00% share in 2025, while diagnostic imaging centers are projected to witness the fastest growth with 25.24% CAGR during the forecast period.

By Deployment Model, on-premise AI solutions dominated, while cloud-based AI platforms are fastest-growing.

The on-premise AI solutions segment accounted for the largest revenue share of 52.00% in 2025 and is expected to maintain its dominant position while registering strong growth over the forecast period. The growth of this segment is mainly due to the increasing preference of hospitals, diagnostic imaging centers, and integrated healthcare networks to have secure in-house imaging analytics infrastructure that offers higher control over patient data, workflow customization, and cyber security management. Big healthcare providers are still trying to deploy AI-powered diagnostic imaging software within their own corporate IT environments to comply with strict rules around healthcare data privacy and imaging governance.

The cloud-based AI platforms are expected to witness the fastest CAGR of 28.25% over the forecast period, driven by the increasing commercialization of scalable healthcare AI deployment models and the rising demand for remote imaging analytics across distributed healthcare environments. Healthcare providers are increasingly adopting cloud-native AI imaging platforms to facilitate multi-site radiology collaboration, centralized diagnostic interpretation and enterprise-wide imaging data access. Cloud deployment allows radiologists and imaging specialists to access advanced AI-powered imaging tools remotely, enhances interoperability across healthcare systems and lowers upfront infrastructure investments.

By Application, oncology imaging dominated, while cardiology & other imaging applications are fastest-growing.

The oncology imaging segment accounted for the largest revenue share of 42.00% in 2025 owing to the rapid increase in global cancer incidence rate, growing demand for early-stage disease detection, and rising implementation of AI-powered diagnostic imaging technologies across oncology care pathways. Healthcare providers and cancer treatment centers are increasingly adopting deep learning-based imaging analytics platforms in radiology workflows to improve tumor detection accuracy, lesion characterization, and treatment response monitoring. AI-assisted oncology imaging solutions are being widely used across CT, MRI, PET, and mammography systems to support precision oncology initiatives and reduce diagnostic interpretation variability among radiologists.

The cardiology & other imaging applications are estimated to witness the highest CAGR of 24.60% during the forecast period due to the rising prevalence of cardiovascular diseases, increasing demand for early detection of cardiac risk, and growing adoption of AI assisted cardiovascular imaging analytics in hospitals and specialty cardiac centers. Healthcare providers are now increasingly using AI-powered echocardiography, cardiac MRI, CT angiography, and ultrasound imaging platforms to enhance diagnostic accuracy and automate image interpretation. The increasing integration of machine learning algorithms with cardiovascular imaging systems is allowing physicians to identify abnormalities such as coronary artery disease, heart failure, arrhythmias, and structural cardiac disorders.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

92.00% |

|

Europe |

Germany |

28.00% |

|

Asia Pacific |

China |

24.00% |

|

Middle East & Africa |

UAE |

4.00% |

|

Latin America |

Brazil |

3.00% |

North America Artificial Intelligence (AI) In Diagnostic Imaging Market Insights

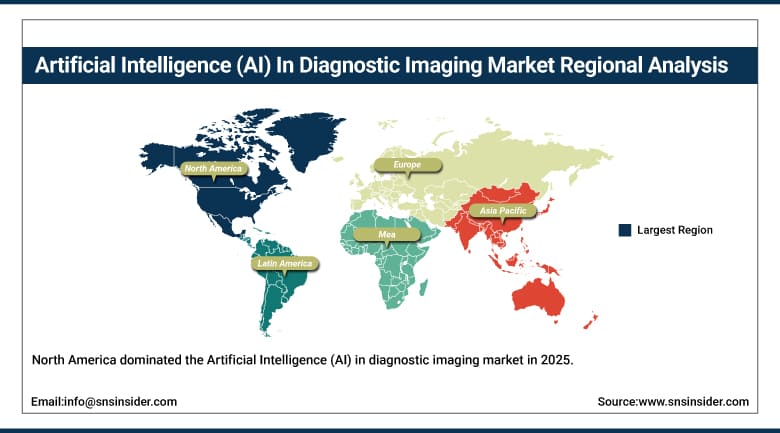

North America dominated the Artificial Intelligence (AI) in diagnostic imaging market in 2025, holding approximately 41.00% revenue share. This dominance is attributed to the presence of advanced healthcare IT infrastructure, rapid commercialization of AI-powered imaging platforms, and the widespread adoption of enterprise radiology automation technologies across the United States and Canada. Hospitals, imaging centers and integrated healthcare networks are spending more on AI-assisted diagnostic interpretation systems, predictive imaging analytics and cloud-based radiology workflow optimization platforms to improve clinical productivity and reduce diagnostic turnaround times. Additionally, increasing deployment of deep learning imaging tools across oncology, cardiology and neurology applications further boosts market growth.

In 2026, a number of North American healthcare technology companies introduced new AI-powered radiology workflow platforms with integrated automated diagnostic prioritization, intelligent image triaging and generative clinical reporting systems to boost radiologist productivity and imaging efficiency.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Artificial Intelligence (AI) In Diagnostic Imaging Market Insights

Europe held a market share of nearly 28.00% in 2025 due to the growing adoption of AI-assisted diagnostic imaging systems, increasing healthcare digitalization initiatives and surging investments in precision radiology infrastructure in Germany, France, the UK and other key European healthcare markets. Healthcare providers across the region are adopting AI-enabled imaging analytics, automated disease detection technologies and cloud-integrated radiology workflow platforms to enhance diagnostic accuracy, patient management efficiency and imaging workflow optimization. Higher government support for digital transformation and modernization of hospital imaging infrastructure in healthcare is further accelerating regional market expansion.

During 2025-2026, several European healthcare organizations increased the deployment of AI-assisted oncology imaging systems that were coupled with predictive clinical decision support and intelligent radiology automation tools.

Asia Pacific Artificial Intelligence (AI) In Diagnostic Imaging Market Insights

The Asia Pacific region is expected to register the highest CAGR of 27.45% during the forecast period, owing to the rapid modernization of healthcare infrastructure, increasing volumes of diagnostic imaging procedures, and growing adoption of AI-based healthcare technologies in China, Japan, South Korea, India, and South-east Asia. The growing shortage of radiologists is pushing healthcare systems to adopt cloud-based imaging analytics platforms, to improve clinical efficiency. The region is experiencing significant commercial growth opportunities in smart hospitals, digital healthcare ecosystems, and precision medicine initiatives. Healthcare providers are increasingly deploying AI-powered imaging systems integrated with predictive analytics, automated reporting platforms and intelligent workflow management.

In 2026, several Asia Pacific healthcare providers ramped up commercialization of AI-powered radiology automation platforms, incorporating predictive imaging, workflow orchestration, and cloud-connected clinical analytics technologies to drive efficiency in imaging and enhance diagnostic performance.

Middle East & Africa and Latin America Artificial Intelligence (AI) In Diagnostic Imaging Market Insights

The Middle East & Africa market is witnessing moderate growth due to increasing digitalization of healthcare initiatives, rising investments in smart hospital infrastructure, and increasing deployment of AI-assisted diagnostic imaging systems across UAE, Saudi Arabia, and South Africa. Healthcare providers are adopting cloud-enabled radiology platforms, AI-driven disease detection systems and automated clinical imaging analytics to boost diagnostic efficiency, improve workflow management and enhance patient care results. Governments in the region are backing the healthcare infrastructure modernization through investments in digital health transformation and intelligent medical technologies. Besides, the expansion of private healthcare networks and rising demand for advanced diagnostic capabilities are driving the market.

Latin America held close to 4.00% market share in 2025 owing to increasing adoption of digital healthcare technologies, increasing imaging infrastructure modernization, and growing implementation of AI-powered clinical workflow optimization systems in Brazil, Mexico and Argentina. Healthcare facilities throughout the region are expanding their investments in predictive imaging analytics, cloud-connected diagnostic systems and AI-assisted radiology platforms to improve clinical productivity and diagnostic accuracy. The regional market is also expanding as there is increasing emphasis on healthcare accessibility and operational efficiency.

Market Dynamics:

Growth Drivers: Increasing adoption of AI-enabled imaging analytics and smart healthcare infrastructure.

The global Artificial Intelligence (AI) in Diagnostic Imaging market is witnessing significant growth owing to the increasing adoption of AI-enabled imaging analytics platforms and smart healthcare technologies. Hospitals, imaging centers and integrated healthcare systems are embracing automated image interpretation software, predictive diagnostic analytics and deep learning-based radiology platforms to enhance clinical accuracy, operational efficiency and diagnostic turnaround times. As imaging workloads increase, a shortage of radiologists grows, and demand for precision diagnostics rises, the commercial deployment of AI-assisted imaging solutions is accelerating across healthcare environments globally. AI-driven clinical workflows are enabling healthcare providers to streamline radiology operations, improve disease prioritization, and boost diagnostic consistency in high-volume imaging departments.

Several healthcare technology providers commercialized advanced generative AI imaging platforms supporting automated radiology reporting, intelligent workflow prioritization and predictive clinical analytics capabilities in 2025–2026, in an attempt to improve healthcare productivity and diagnostic performance.

Restraints: Challenges in Healthcare AI Implementation such as high implementation costs and regulatory complexities.

However, the rapid technological developments, high implementation costs of AI-enabled imaging infrastructure, software integration complexities and stringent healthcare data governance requirements have limited the market penetration in smaller hospitals and independent imaging facilities. However, deploying enterprise-grade AI imaging systems typically demands substantial investment in advanced computing infrastructure, cloud storage capacity, cybersecurity infrastructure, and integration with legacy hospital information systems for interoperability. Operational and financial barriers for healthcare organisations adopting AI-powered diagnostic imaging technologies are also regulatory approval requirements, imaging algorithm validation processes and cyber security compliance standards.

2026 Several healthcare regulatory agencies issue updated guidance frameworks for AI validation protocols, imaging algorithm transparency, cyber security compliance, and risk management standards for diagnostic imaging software platforms deployed across healthcare systems.

Opportunities: Growth of cloud-connected diagnostic ecosystems and predictive imaging analytics platforms.

Increased investments in cloud-based healthcare ecosystems and predictive imaging technologies are opening up tremendous growth opportunities for Artificial Intelligence (AI) in diagnostic imaging vendors worldwide. Healthcare organizations are rapidly adopting cloud-native imaging workflows, enterprise AI analytics platforms, and predictive clinical decision-support systems to increase scalability, imaging accessibility and operational efficiency in distributed healthcare environments. The increasing commercialization of precision medicine programmers, and automated diagnostic ecosystems are expected to further augment the long-term market growth. Imaging infrastructure connected to the cloud enables radiologists and other healthcare professionals to remotely access real-time diagnostic insights, centralized imaging databases, and AI-assisted interpretation tools, thereby improving healthcare coordination and clinical productivity.

In 2025, several healthcare AI companies introduced cloud-connected imaging analytics ecosystems that include predictive disease detection, intelligent clinical reporting, and automated radiology workflow optimization technologies.

Recent Developments:

-

2026: GE HealthCare expanded commercialization of AI-enabled imaging workflow automation platforms integrated with predictive diagnostic analytics systems.

-

2026: Siemens Healthineers introduced upgraded cloud-connected radiology AI software supporting automated image prioritization and clinical decision support.

-

2025: Philips Healthcare accelerated deployment of AI-powered MRI workflow optimization technologies integrated with smart imaging analytics platforms.

-

2025: Canon Medical Systems expanded its AI-assisted oncology imaging portfolio with advanced automated lesion detection and diagnostic reporting capabilities.

Artificial Intelligence (AI) In Diagnostic Imaging Market Key Players are:

-

GE HealthCare

-

Siemens Healthineers AG

-

Koninklijke Philips N.V.

-

Canon Medical Systems Corporation

-

Fujifilm Holdings Corporation

-

IBM Corporation

-

NVIDIA Corporation

-

Aidoc Medical Ltd.

-

Arterys Inc.

-

Qure.ai Technologies Pvt. Ltd.

-

Zebra Medical Vision Ltd.

-

Viz.ai Inc.

-

Lunit Inc.

-

Infervision Medical Technology Co., Ltd.

-

PathAI Inc.

-

Agfa-Gevaert Group

-

Hologic Inc.

-

Samsung Medison Co., Ltd.

-

Riverain Technologies LLC

-

Subtle Medical Inc.

Artificial Intelligence (AI) In Diagnostic Imaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.92 Billion |

| Market Size by 2035 | USD 24.73 Billion |

| CAGR | CAGR of 23.83% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Retail Automation Assessment, Smart Checkout Technology Trends, AI-Enabled Retail Infrastructure Analysis, DROC & SWOT Analysis, Investment Trends, Supply Chain Evaluation, Consumer Transaction Technology Assessment, and Future Market Opportunity EvaluationChain Evaluation, Industrial Packaging Demand Analysis, Sustainability Assessment, DROC & SWOT Analysis, Regulatory Framework Analysis, Innovation Benchmarking, and Future Market Opportunity Evaluation |

| Key Segments | • By Deployment Model (On-Premise AI Solutions, Cloud-Based AI Platforms, Hybrid Deployment Models) • By Imaging Modality (Computed Tomography (CT), Magnetic Resonance Imaging (MRI), X-ray & Mammography) • By Application (Oncology Imaging, Neurology Imaging, Cardiology & Other Imaging Applications) • By End User (Hospitals & Health Systems, Diagnostic Imaging Centers, Research & Academic Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GE HealthCare, Siemens Healthineers AG, Koninklijke Philips N.V., Canon Medical Systems Corporation, Fujifilm Holdings Corporation, IBM Corporation, NVIDIA Corporation, Aidoc Medical Ltd., Arterys Inc., Qure.ai Technologies Pvt. Ltd., Zebra Medical Vision Ltd., Viz.ai Inc., Lunit Inc., Infervision Medical Technology Co., Ltd., PathAI Inc., Agfa-Gevaert Group, Hologic Inc., Samsung Medison Co., Ltd., Riverain Technologies LLC, Subtle Medical Inc. |

Frequently Asked Questions

The Artificial Intelligence (AI) in Diagnostic Imaging Market was valued at USD 2.92 billion in 2025.

The market is projected to reach USD 24.73 billion by 2035.

The market is expected to expand at a CAGR of 23.83% during the forecast period.

North America dominated the global market owing to strong healthcare IT infrastructure and rapid adoption of AI-enabled radiology technologies.

On-Premise AI Solutions accounted for the largest revenue share of 52.00% in 2025.

Get in Touch