Bioanalytical Testing Services Market Report Scope & Overview:

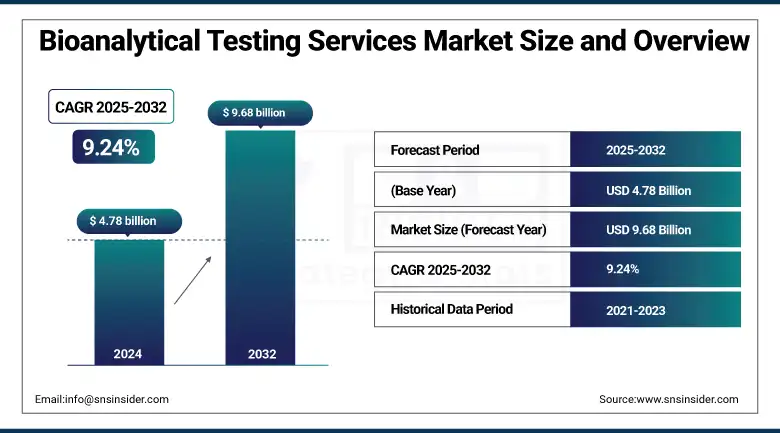

The Bioanalytical Testing Services Market size was valued at USD 4.78 billion in 2024 and is expected to reach USD 9.68 billion by 2032, growing at a CAGR of 9.24% over 2025-2032.

The global bioanalytical testing services market is experiencing strong demand driven by the increased complexity of drug molecules (e.g., biologics and biosimilars) and the subsequent need for high-throughput analytical techniques in clinical and preclinical studies. With drug makers seeking to satisfy the rigorous demands of regulators, and with a surge in the outsourcing of bioanalytical capacity, quality, and efficiency are being raised by specialized CROs. Increasing importance of bioavailability and bioequivalence (BA/BE) studies, therapeutic drug monitoring, and toxicology studies is expected to serve as a lucrative growth platform for the market.

For instance, WuXi AppTec incorporated AI-based integrated bioanalytical platforms and automated LC-MS workflows in early 2024, indicating the increasing relevance of digital transformation in the global bioanalytical testing services market.

To Get more information On Bioanalytical Testing Services Market - Request Free Sample Report

In addition, mass spectrometry and cell-based assays have become increasingly indispensable as personalized medicine and individualized drug therapy are coming to the fore. Significant innovation, R&D spending globally crossing USD 250 billion in the pharma-biotech domain, and harmonisation in regulations are driving the demand. Businesses are increasing lab footprint and implementing automated platforms to support high complexity assays, which fuels the growth of the bioanalytical testing services market. These elements support the demand and supply side as it relates to the bioanalytical testing services market globally.

In 2024, Charles River and Altasciences grew global footprints to support increasing requests for large molecule testing, as expansion followed on the lines of increasing bioanalytical testing services market size pertaining to biologics.

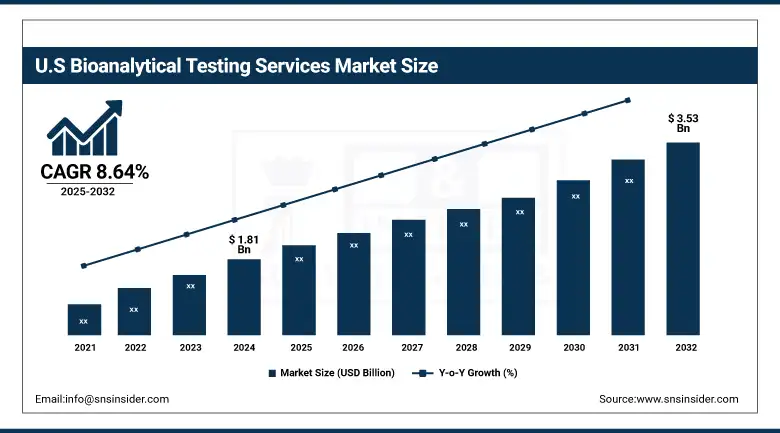

The U.S. bioanalytical testing services market size was valued at USD 1.81 billion in 2024 and is expected to reach USD 3.53 billion by 2032, growing at a CAGR of 8.64% over 2025-2032. The U.S. contributes single-handedly for a majority share in the market due to the presence of major players, stringent FDA regulations for FDA trials, and established infrastructure related to the clinical trials. In addition, there is a high level of R&D investment, over USD 90bn in pharmaceuticals in 2023. Canada is also growling because of increased clinical trial activity and investment in biologics. The U.S. is in the lead thanks to a mature regulatory environment and a large number of FDA drug approvals. 55 NDA approvals were announced in 2023, driving incremental demand for bioanalytical testing services.

Bioanalytical Testing Services Market Dynamics:

Drivers:

-

Rising R&D, Biologics Pipeline, and Regulatory Compliance Fuel Demand

The bioanalytical testing services market is predominantly driven by the burgeoning pipeline of complex biologics, gene therapies, and biosimilars, necessitating analytical support for regulatory submission and approval. The increase in clinical studies (more than 460,000 registered globally as of 2024) has notably increased demand for robust bioanalysis. Rising adoption of outsourcing models among pharmaceutical and biopharma companies is also playing a determinant role in driving the market, as companies look to reduce timelines and alleviate operational overheads.

Significant investment is being made by large CROs in next-gen tools, which include HRMS and LC-MS/MS platforms, leading to an expanded capacity. Furthermore, the increasing incidence of chronic and rare diseases drives the requirement for biomarker validation and immunogenicity testing, in turn fostering the demand for premium-quality, GLP-compliant analytical services. The regulatory bodies, including the FDA and EMA, have also revised guidelines for bioequivalence studies, now requiring stringent validation procedures and hence greater dependence on outsourcing bioanalytical services. Pharma R&D spend has also surpassed USD 280 billion globally, highlighting ongoing investment in early-stage research-especially beneficial for the bioanalytical testing services market growth.

Restraints:

-

Skilled Talent Shortage and High Compliance Burdens Hinder Scalability

The bioanalytical testing services market is replete with challenges, including a lack of skilled professionals and increasing complexity of bioanalytical techniques. The trend toward biologics and gene therapies is driving the need for customized platforms such as ligand binding assays and hybrid LC-MS systems, but many service providers are encountering challenges in scale-up, because it is difficult to run and train on these large, complex workflows in addition to leveraging the skilled and costly resources.

Moreover, with tight regulations in place like the FDA’s revised 2024 bioanalytical method validation guidance, which demands the validation, reproducibility, and traceability of methods, the cost of compliance becomes even higher for smaller CROs. This hurts smaller mid-sized players who do not operate infrastructure by impeding total capacity. A further limitation is the large capital outlay required to develop sophisticated hardware and automation platforms, so it is difficult for new entrants to access the market. Increasing project turnaround time coupled with complex sample matrices also causes delays in project execution, which negatively influences customer retention. In addition, data security and integrity on external digital infrastructures are of continuous concern, especially with sensitive data of clinical trials being processed in cloud‐based analytics ecosystems.

Bioanalytical Testing Services Market Segmentation Analysis:

By Molecule Type

Small molecules had the largest market share in the global bioanalytical testing services market in 2024 (54.7%), due to their extensive use in generic and branded drug development and less complicated analytical needs than large molecules. The market for large molecules is increasing with an increasing no of biologics and biosimilars in the pipeline, especially MAbs and glycoproteins. Large molecules also have complex structural characteristics that need more advanced testing, which sees the need for bioanalytical services rise. Advancements in ADCs and mRNA modalities are also driving growth in the segment, aided by growing R&D spend and regulatory incentives around the approval of complex biologics.

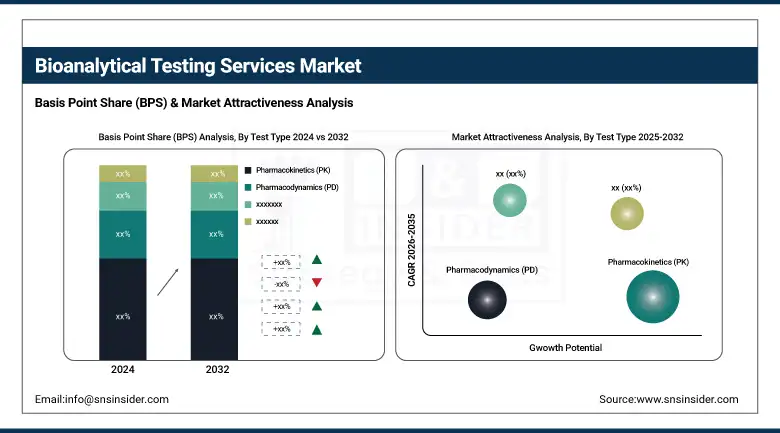

By Test Type

Pharmacokinetics (PK) testing dominated with a share of 33.2% in 2024, as it is essential to determining drug disposition (absorption, distribution, metabolism, and excretion). It is crucial in the preclinical and clinical disease stages. The bioequivalence testing segment is anticipated to witness the fastest growth on account of increasing development of generic drugs, requiring demonstration of therapeutic equivalence. Regulatory bodies such as the FDA and the EMA advocated bioequivalence testing for ANDAs, making the need even more pressing. Moreover, cost-containment pressures and patent expirations are supporting an increase in the number of generic approvals, driving the growth of the bioanalytical testing services market in this sub-segment.

By Technology

Analytical techniques held the largest market share in 2024 and were valued at USD 1.56 billion, on account of the paramount role played by them in the quantification of drugs and biomarkers. Technologies such as LC-MS/MS are commonly used due to their sensitivity and precision. The segment of genomic & molecular procedures is the most rapidly growing sector, largely due to the rising use of personalized medicine and biomarker-based drug development. These methods are vital for companion diagnostics and the estimation of gene expression and mutation status. The expanding number of cell and gene therapy programs in the pipeline, and increasing use of next-generation sequencing (NGS) in clinical programs, are adding momentum to the shift to molecular-based bioanalytical solutions.

By Service Type

The clinical bioanalytical services segment dominated in terms of revenue with a share of 48.9% in 2024, owing to the growing number of clinical trials conducted globally and growing outsourcing of clinical-phase testing by biopharmaceutical companies. The services provide support for regulatory requirements, and when high throughput of samples is required (particularly in larger object counting studies of Phase II and Phase III). The custom assay development segment is the fastest growing due to the requirement for customized bioanalytical solutions for new molecules and delivery mechanisms. Sophisticated treatment modalities, such as CAR-T therapies, bispecific antibodies, and RNA therapies, need custom assay development support, which further boosts the market share of bioanalytical testing services in this fast-growing segment.

By Application Area

Oncology was the largest application market in 2024, accounting for 37.6% of the total market share, owing to the proliferation of oncology drug trials and regulatory emphasis on precision cancer medicines. The cancer immunotherapy and the targeted therapy also require frequent biomarker and pharmacokinetics analyses. Neurology is the fastest-growing sector, mainly due to the growing pipeline of R&D for neurodegenerative disorders such as Alzheimer's and Parkinson’s. Bioanalytical hurdles CNS drugs are challenging to develop because of the lack of simple bioanalytical methods related to the blood-brain barrier issues, which makes it essential for new test strategies to be found. Rise in the development of neuroimaging biomarkers and companion diagnostics is also contributing to segmental growth in the global bioanalytical testing services market.

Bioanalytical Testing Services Market Regional Insights:

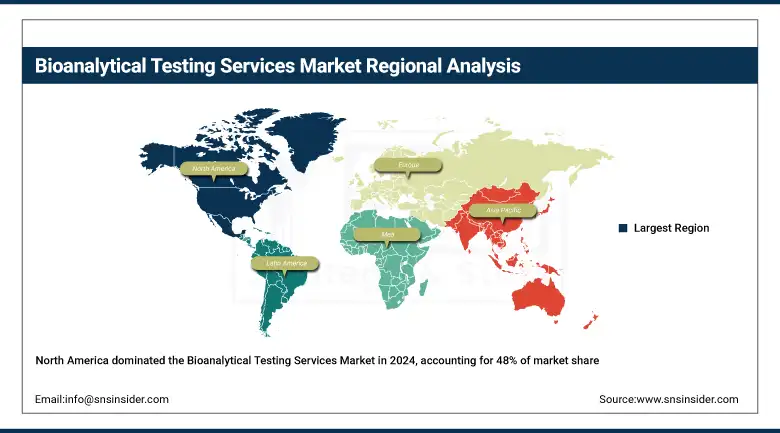

North America held a substantial share in the global bioanalytical testing services market in 2024, with more than 48% revenue share, led by the presence of a large number of pharmaceutical and biopharmaceutical companies, established CROs, and high investment in drug development.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region in the global bioanalytical testing services market due to cheap clinical trials, friendly government measures, and increasing pharmaceutical exports. The market in the region is expected to grow substantially owing to rising R&D activities in China and India. CRO infrastructure and biopharmaceutical manufacturing are being aggressively developed and expanded, with China at the forefront in terms of investment in the region. In 2023, China's life sciences R&D expenditure exceeded USD 90 billion, stimulating the demand for custom assay development and bioavailability testing. India has become a significant global centre for offshoring clinical trials, facilitated by the harmonisation of regulations and the potential for high patient recruitment rates. The pharmaceutical innovation and the neurology and oncology clinical trials of Japan continue to fuel the market's growth. South Korea is emerging in virology testing due to high biologics experimentation.

Bioanalytical Testing Services Market Key Players:

Leading bioanalytical testing services companies in the market include Thermo Fisher Scientific Inc., Charles River Laboratories International Inc., ICON Plc, IQVIA Inc., Syneos Health, SGS SA, Labcorp, Intertek Group Plc, Pace Analytical Services LLC, WuXi AppTec, Medpace Inc., Eurofins Scientific, Frontage Laboratories Inc., PPD Inc., PAREXEL International Corporation, Almac Group, Celerion Inc., Altasciences, BioAgilytix Labs, Lotus Labs, LGS Limited, Sartorius AG, CD BioSciences, Absorption Systems LLC, Bioneeds India Private Limited, Vipragen Biosciences, and Toxikon Corporation.

Recent Developments in the Bioanalytical Testing Services Market:

In June 2024, PPD, part of Thermo Fisher Scientific, announced the expansion of its bioanalytical lab in Richmond, Virginia, with advanced automation technologies and increased LC-MS/MS capacity to support growing demand for biologics and gene therapy testing.

In March 2024, Syneos Health partnered with a major Asian pharmaceutical company to enhance its bioanalytical testing capabilities in India, focusing on high-throughput biomarker analysis and cell-based assays for oncology and immunology trials.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.78 billion |

| Market Size by 2032 | USD 9.68 billion |

| CAGR | CAGR of 9.24% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Molecule Type (Small Molecules, Large Molecules) • By Test Type (Pharmacokinetics [PK], Pharmacodynamics [PD], Bioavailability Testing, Bioequivalence Testing, ADME Testing, Biomarker Testing, Cell-based Assays, Virology Testing, Other Tests [e.g., immunogenicity testing, toxicokinetics, neutralizing antibodies]) • By Technology (Sample Collection and Preparation, Method Development and Validation, Analytical Techniques, Genomic & Molecular Techniques, Other Processes [e.g., data interpretation, regulatory documentation, audit support]) • By Service Type (Preclinical Bioanalytical Services, Clinical Bioanalytical Services, Custom Assay Development, Validation & Qualification Services, Regulatory Submission Support, Other Services [e.g., batch release testing, method transfer, GxP compliance support]) • By Application Area (Oncology, Neurology, Infectious Diseases, Cardiology, Gastroenterology, Other Applications [e.g., endocrinology, metabolic disorders, rare diseases]) • By End User (Pharmaceutical & Biopharmaceutical Companies, Contract Development and Manufacturing Organizations [CDMOs], Contract Research Organizations [CROs], Others [e.g., academic institutions, government labs, regulatory agencies]) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific Inc., Charles River Laboratories International Inc., ICON Plc, IQVIA Inc., Syneos Health, SGS SA, Labcorp, Intertek Group Plc, Pace Analytical Services LLC, WuXi AppTec, Medpace Inc., Eurofins Scientific, Frontage Laboratories Inc., PPD Inc., PAREXEL International Corporation, Almac Group, Celerion Inc., Altasciences, BioAgilytix Labs, Lotus Labs, LGS Limited, Sartorius AG, CD BioSciences, Absorption Systems LLC, Bioneeds India Private Limited, Vipragen Biosciences, and Toxikon Corporation. |

Frequently Asked Questions

Trends include increased use of mass spectrometry, automation, AI-based data modeling, and greater emphasis on early-phase oncology and toxicology studies.

Outsourcing is boosting market growth by enabling cost efficiency, scalability, and faster regulatory compliance, especially through CROs and CDMOs in APAC and North America.

Small molecule testing currently dominates due to high volume in generic drug development, but large molecule testing is growing faster with the rise of biologics and monoclonal antibodies.

Rising demand for bioavailability and bioequivalence (BA/BE) studies, growth in biologics and biosimilars, and increased outsourcing by pharma/biotech companies are key growth drivers.

The global bioanalytical testing services market was valued at USD 4.78 billion in 2024, and is projected to reach over USD 9.68 billion by 2032, growing at a CAGR of around 9.24%.

Get in Touch