Cardiac Rhythm Management Devices Market Report Scope & Overview:

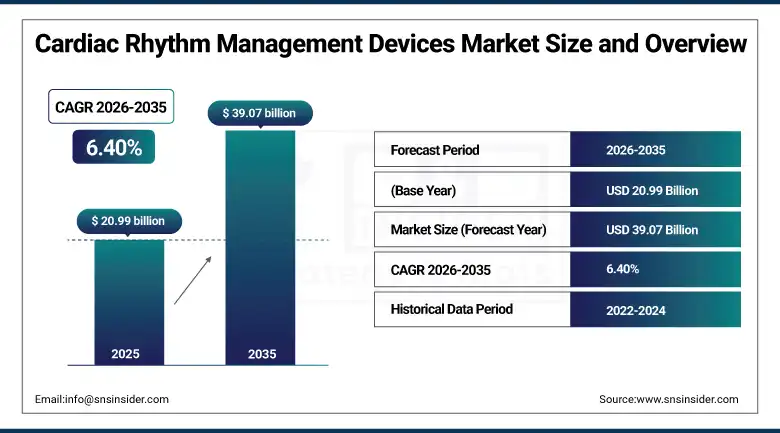

The Cardiac Rhythm Management Devices Market size was valued at USD 20.99 Billion in 2025 and is expected to reach USD 39.07 Billion by 2035, growing at a CAGR of 6.40% from 2026–2035.

The global cardiac rhythm management devices market is growing at a reliable and commercially sustained pace. Cardiovascular diseases remain the leading cause of global mortality, accounting for approximately 32% of all deaths annually. Arrhythmias, atrial fibrillation, heart failure, and sudden cardiac arrest collectively create a large and growing patient population requiring rhythm management intervention. The CDC estimates 12.1 million Americans will be affected by atrial fibrillation by 2030. Technological innovation across leadless pacemakers, subcutaneous ICDs, wearable defibrillators, and MRI-compatible CRM devices is progressively expanding the clinically appropriate patient population. Remote cardiac monitoring integration with implanted devices enables real-time physician oversight that improves outcomes and reduces hospitalisation events.

Abbott received FDA approval for its AVEIR DR dual-chamber leadless pacemaker system in 2024, the first dual-chamber leadless pacing system approved for commercial use. The approval represents a significant clinical advance as the system eliminates transvenous leads whose mechanical failure and infection risk represent the primary complication sources of conventional pacemaker systems, enabling pacing therapy for patients previously unsuitable for standard pacemaker implantation due to vascular access limitations or infection history.

Market Size and Forecast

-

Market Size in 2026E: USD 22.33 Billion

-

Market Size by 2035: USD 39.07 Billion

-

CAGR: 6.40% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Cardiac Rhythm Management Devices Market - Request Free Sample Report

Cardiac Rhythm Management Devices Market Trends

-

Leadless pacemaker adoption is accelerating as single-chamber systems achieve commercial maturity and dual-chamber systems gain regulatory approval, progressively replacing conventional transvenous pacing in suitable patients.

-

Remote cardiac monitoring integration with implantable devices is improving physician visibility into arrhythmia events, battery status, and lead integrity between clinic visits, reducing emergency hospitalisations through earlier intervention.

-

Subcutaneous ICD adoption is growing as the device’s entirely extravascular design eliminates transvenous lead complications while providing life-saving defibrillation therapy without the infection and extraction risks of conventional systems.

-

MRI-conditional device labelling has become a standard specification requirement across pacemakers and ICDs as the widespread clinical use of MRI for concurrent condition evaluation demands CRM device compatibility.

-

Cardiac resynchronisation therapy expansion into milder heart failure and non-left bundle branch block patient populations is growing with accumulating clinical evidence supporting CRT benefit in broader cardiac substrate profiles.

U.S. Cardiac Rhythm Management Devices Market Outlook

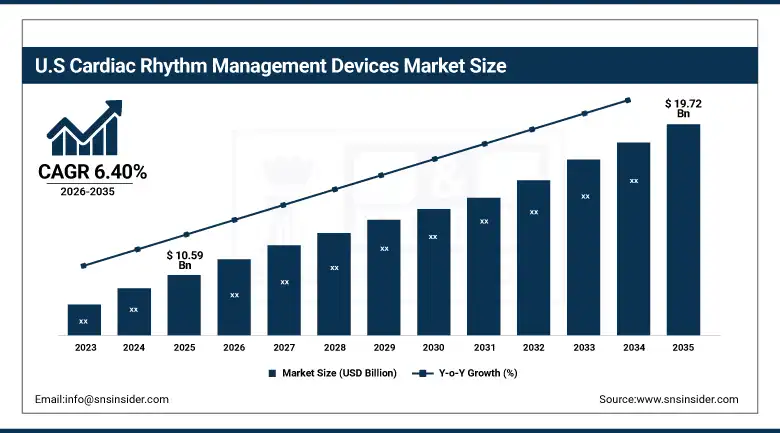

The U.S. Cardiac Rhythm Management Devices Market was valued at approximately USD 10.59 Billion in 2025 and is expected to reach approximately USD 19.72 Billion by 2035, growing at a CAGR of approximately 6.40%.

The U.S. is the world’s largest cardiac rhythm management devices market. It accounted for the majority of North America’s 44% global revenue share in 2023. Medicare and commercial insurance coverage for CRM device implantation creates the reimbursement foundation that sustains procedure volume. Medtronic, Abbott, and Boston Scientific are each headquartered or have primary manufacturing operations in the U.S., sustaining the technology innovation pipeline that sustains premium device adoption. FDA review processes for novel CRM devices including the AVEIR DR dual-chamber leadless system create structured technology refresh cycles whose commercial impact sustains market growth beyond demographic volume alone.

Boston Scientific launched its EMPOWER Modular Pacing System international expansion in 2024, receiving regulatory approval in Europe and select Asia Pacific markets for its leadless single-chamber ventricular pacemaker that clips directly to heart tissue without transvenous leads. The international expansion extends the commercial reach of the most widely studied leadless pacemaker platform beyond U.S. markets into major European and Asian cardiac intervention centres whose high procedure volumes create substantial adoption opportunity.

Cardiac Rhythm Management Devices Market Segmentation Analysis

-

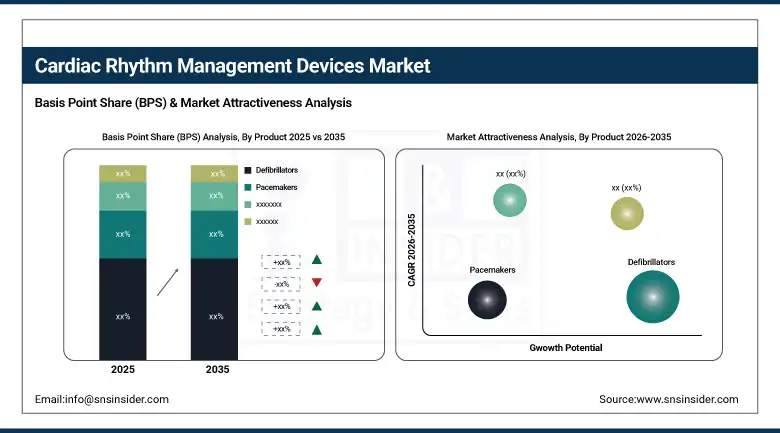

By Product, the Defibrillators segment dominated the Cardiac Rhythm Management Devices Market with approximately 43.00% share in 2025, while the Cardiac Resynchronization Therapy segment is the fastest growing.

-

By Application, the Arrhythmia segment dominated the Cardiac Rhythm Management Devices Market with approximately 58.00% share in 2025, while the Heart Failure segment is the fastest growing.

-

By End User, the Hospitals segment dominated the Cardiac Rhythm Management Devices Market with approximately 67.00% share in 2025, while the Ambulatory Surgical Centres segment is the fastest growing.

By Product, defibrillators dominate, CRT grows fastest

Defibrillators retained the dominant product position with approximately 43% of the cardiac rhythm management devices market in 2023. Their commercial primacy reflects the life-saving urgency of the clinical indication they serve. ICDs prevent sudden cardiac death in patients with structural heart disease and reduced ejection fraction whose arrhythmia risk creates a compelling clinical and medico-legal imperative for device implantation. The expanding public-access defibrillation programme, placing AEDs in airports, sports venues, and public buildings, creates additional external defibrillator procurement that compounds with clinical implantable device demand.

Cardiac resynchronization therapy is the fastest-growing product segment because clinical evidence continues expanding the patient population whose heart failure responds to CRT biventricular pacing. CRT’s ability to improve left ventricular synchrony in dyssynchronous heart failure reduces hospitalisation, improves exercise tolerance, and reduces mortality in appropriately selected patients. Ongoing clinical trials evaluating CRT in milder heart failure stages and non-traditional electrical substrates are creating new clinical guideline expansion that progressively broadens the CRT-eligible population beyond the narrow QRS criteria that initially defined the technology’s indication.

By Application, arrhythmia dominates, heart failure grows fastest

Arrhythmia retained the dominant application position in the cardiac rhythm management devices market in 2025. The global arrhythmia burden, anchored by atrial fibrillation affecting approximately 60 million people worldwide and growing at above-average rates with population ageing, creates the largest single cardiac indication for CRM device therapy. Each new AF patient whose stroke risk and symptom burden warrants device-based rhythm monitoring or control creates procurement across the rhythm management device ecosystem. The expanding use of implantable cardiac monitors for AF detection and burden quantification creates additional device procurement beyond traditional pacing and defibrillation.

Heart failure is the fastest-growing application segment because CRT therapy’s demonstrated ability to reduce heart failure hospitalisation and mortality creates compelling health-economic investment justification for the healthcare systems whose hospitalisation cost burden from heart failure is among the largest single diagnosis expenditures in developed healthcare markets. Each percentage point reduction in heart failure hospitalisation frequency through CRT and remote monitoring generates healthcare system savings whose magnitude sustains reimbursement support for device-based heart failure management at above-average benefit assessment scores relative to pharmaceutical alternatives.

By End User, hospitals dominate, ambulatory centres grow fastest

Hospitals retained the dominant end user position in the cardiac rhythm management devices market in 2025. CRM device implantation requires electrophysiology laboratory infrastructure, cardiac anaesthesia capability, post-implant monitoring, and device programming expertise whose capital and staffing requirements are available only in hospital settings for complex device procedures. High-risk patient populations, including those with reduced ejection fraction requiring ICD or CRT-D implantation, require hospital-level post-procedure monitoring whose clinical risk profile precludes outpatient migration.

Ambulatory surgical centres are the fastest-growing end user segment because straightforward pacemaker implantation for bradycardia management in low-risk patients is progressively migrating to outpatient settings as clinical pathway development demonstrates equivalent safety outcomes with substantially lower procedural cost. CMS reimbursement pathway evolution and private insurer coverage policies are progressively enabling outpatient pacemaker implantation at accredited ASCs whose volume growth creates structured device procurement demand independent of hospital market dynamics.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Cardiac Rhythm Management Devices Market Insights

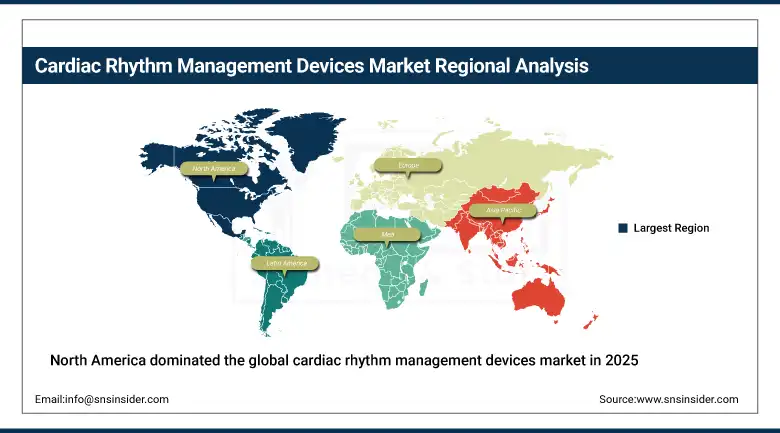

North America dominated the global cardiac rhythm management devices market in 2025, accounting for approximately 44% of global revenues. The United States accounts for approximately 87.4% of North American revenues. Advanced healthcare infrastructure, comprehensive Medicare and commercial insurance reimbursement, and the headquarters concentration of Medtronic, Abbott, and Boston Scientific collectively define the U.S. market’s commercial leadership. The high cardiovascular disease prevalence, established electrophysiology programme density, and above-average adoption of novel device technologies sustain North America’s dominant position.

Canada contributes approximately 12.6% of North American revenues through its publicly funded healthcare system’s cardiac device programme, active electrophysiology centres in major academic hospitals, and reimbursement frameworks that support adoption of clinically proven CRM technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cardiac Rhythm Management Devices Market Insights

Europe is a sophisticated cardiac rhythm management devices market where the EU MDR’s strengthened clinical evidence requirements, national health system reimbursement criteria, and the region’s leading electrophysiology centres create a technically advanced procurement environment. Germany accounts for approximately 22.3% of European revenues through its large hospital cardiology infrastructure, Biotronik’s domestic market leadership, and above-average per-capita CRM device implantation rates sustained by comprehensive statutory health insurance coverage.

The United Kingdom, France, and Italy are significant secondary markets where national health system cardiology investment, growing AF diagnosis infrastructure, and European device approval timelines create consistent demand. BIOTRONIK’s European headquarters and the continent’s active cardiac electrophysiology research community sustain European device innovation alongside U.S.-led platform development.

Asia Pacific Cardiac Rhythm Management Devices Market Insights

Asia Pacific is the fastest-growing regional cardiac rhythm management devices market, driven by rapidly expanding cardiovascular disease burden across China, India, Japan, South Korea, and Australia, combined with progressive healthcare infrastructure investment and growing device-based cardiac therapy adoption rates. China accounts for approximately 44.8% of Asia Pacific revenues through its large hospital cardiology infrastructure, government healthcare investment, and the growing domestic device manufacturer ecosystem whose competitive pricing is expanding market access.

India is the most commercially dynamic emerging market within Asia Pacific, where the combination of high cardiovascular disease burden, growing private hospital cardiology investment, and government health insurance scheme expansion through Ayushman Bharat are progressively enabling CRM device access for patient populations previously excluded by cost barriers.

MEA & Latin America Cardiac Rhythm Management Devices Market Insights

The Middle East and Africa and Latin America are growing cardiac rhythm management devices markets where healthcare infrastructure investment and rising cardiovascular disease burden are creating structured device procurement. Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s healthcare investment, the Ministry of Health’s cardiac care programme, and the private hospital sector’s above-average technology adoption.

Brazil leads Latin American revenues at approximately 44.2% through its large hospital cardiology infrastructure, ANVISA device approval framework, and the SUS public health system’s cardiac device implantation programme that provides device access to a broad patient population across Brazil’s geographically extensive healthcare network.

Growth Drivers: Rising cardiovascular disease and AF prevalence and leadless and wearable technology expanding device eligibility

Rising cardiovascular disease and atrial fibrillation prevalence is the cardiac rhythm management devices market’s most structurally reliable growth driver. The global AF patient population is expanding at above-average rates with population ageing, obesity, hypertension, and diabetes’ progression. Each new AF diagnosis creates a rhythm management evaluation whose clinical pathway may lead to CRM device implantation for monitoring, rate control, or rhythm restoration. The CDC’s projection of 12.1 million U.S. AF patients by 2030 demonstrates the demographic certainty of continued market volume growth.

Leadless pacemaker and wearable CRM technology innovation is expanding the device-eligible patient population by addressing the clinical contraindications that prevented traditional device implantation in certain patient groups. Patients with vascular access limitations, prior device infections, or limited life expectancy where lead extraction risk outweighed benefit are now eligible for leadless pacing. Wearable defibrillators bridge the gap between acute risk period and permanent ICD implantation decision, creating a new device category whose clinical adoption is creating above-average market segment growth.

Restraints: High device cost limiting access in developing markets and remote monitoring reimbursement gaps in certain healthcare systems

High CRM device cost is the most significant access barrier in developing and emerging markets where healthcare budget constraints limit device procurement to the most established patient populations at major academic centres. A dual-chamber ICD system can cost USD 15,000 to USD 40,000 including implantation, a financial threshold that excludes the majority of the potential patient population in price-sensitive healthcare markets. Domestic device manufacturer development in China and India is progressively improving affordability, but the gap between clinical need and device access remains commercially significant.

Remote monitoring reimbursement inconsistency creates adoption barriers for the connected monitoring programmes that improve outcomes in CRM device patients. Some national healthcare systems reimburse remote monitoring clinic visits; others do not. In markets without remote monitoring reimbursement, the commercial incentive for connectivity-enabled device specification is limited to device differentiation rather than supplemental procedure revenue, reducing the economic motivation for adopting premium connected device specifications.

Opportunities: Leadless dual-chamber pacing commercial expansion, remote monitoring outcome demonstration, and Asia Pacific market access programmes

Leadless dual-chamber pacing represents the most commercially transformative near-term product opportunity in the cardiac rhythm management devices market. Abbott’s FDA-approved AVEIR DR dual-chamber leadless system creates a new premium device category whose clinical superiority over single-chamber leadless systems expands the pacing indication scope that can be served without transvenous leads. The initial adoption curve in U.S. high-volume electrophysiology centres will progressively extend to European and Asian markets as regulatory approvals and physician training programmes reach clinical deployment scale.

Remote monitoring outcome demonstration is creating the health-economic evidence base that sustains reimbursement expansion for connected CRM programmes. Clinical data demonstrating hospitalisation reduction, earlier arrhythmia detection, and mortality improvement through remote monitoring creates the pharmacoeconomic argument for reimbursement policy expansion in healthcare systems whose current coverage policies do not fully reimburse remote monitoring clinical activity.

Recent Developments:

-

2024: Abbott received FDA approval for the AVEIR DR dual-chamber leadless pacemaker system in 2024, the first dual-chamber leadless pacing system commercially approved, eliminating transvenous leads that represent the primary complication source of conventional pacemaker systems.

-

2024: Boston Scientific launched international expansion of its EMPOWER Modular Pacing System in 2024, receiving European and Asia Pacific regulatory approvals for its leadless ventricular pacemaker and extending commercial access to high-volume electrophysiology centres beyond the U.S. initial launch market.

-

2024: Medtronic announced updated outcomes data for its EXTRAVASCULAR ICD system in 2024, demonstrating superior sensing and reduced inappropriate shocks compared to conventional transvenous systems, supporting expansion of the EV-ICD programme into broader patient eligibility criteria beyond the high-risk patient populations in whom the device was initially most commonly specified.

Cardiac Rhythm Management Devices Market Key Players

-

Medtronic

-

Abbott

-

Boston Scientific

-

Biotronik

-

Philips Healthcare

-

LivaNova

-

Zoll Medical

-

Nihon Kohden

-

Schiller AG

-

Mindray Medical

-

BPL Medical Technologies

-

CU Medical Systems

-

Defibtech

-

Cardiac Science

-

MED-EL

Cardiac Rhythm Management Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.99 Billion |

| Market Size by 2035 | USD 39.07 Billion |

| CAGR | CAGR of 6.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Defibrillators, Pacemakers, Cardiac Resynchronization Therapy Devices, External Defibrillators, Others) • by Application (Arrhythmia, Heart Failure, Tachycardia, Bradycardia, Others) • by End User (Hospitals, Ambulatory Surgical Centres, Cardiac Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic, Abbott, Boston Scientific, Biotronik, Philips Healthcare, LivaNova, Zoll Medical, Nihon Kohden, Schiller AG, Mindray Medical, BPL Medical Technologies, CU Medical Systems, Defibtech, Cardiac Science, MED-EL |

Frequently Asked Questions

The Cardiac Rhythm Management Devices Market is expected to grow at a CAGR of 6.40% from 2026 to 2035.

The Cardiac Rhythm Management Devices Market was valued at USD 20.99 Billion in 2025.

Rising cardiovascular disease and atrial fibrillation prevalence driven by population ageing, and leadless pacemaker and wearable defibrillator technology expanding device eligibility to patient populations previously unsuitable for conventional transvenous CRM device implantation.

Defibrillators dominated the Cardiac Rhythm Management Devices Market with approximately 43% share in 2023, while Cardiac Resynchronization Therapy is the fastest-growing segment.

North America dominated the Cardiac Rhythm Management Devices Market in 2025 with approximately 44% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch