Pacemakers Market Report Scope & Overview:

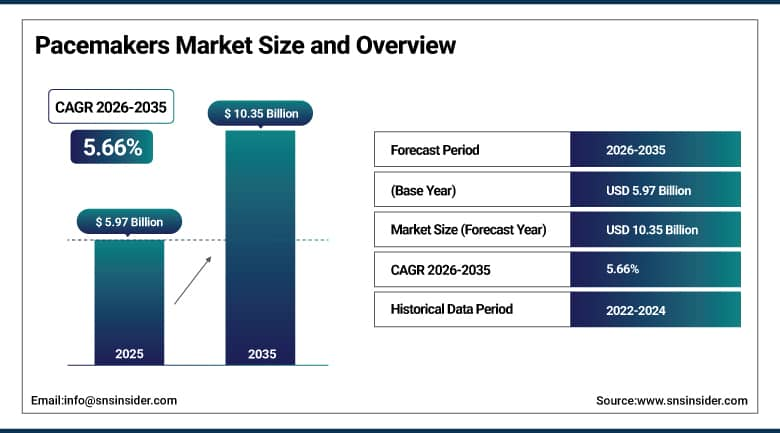

The Pacemakers Market was valued at USD 5.97 Billion in 2025 and is expected to reach USD 10.35 Billion by 2035, growing at a CAGR of 5.66% from 2026–2035.

The global pacemakers market is growing at a sustained pace. Pacemakers are implantable cardiac devices that deliver controlled electrical impulses to regulate heartbeat rhythm in patients with bradycardia, heart block, sick sinus syndrome, and other rhythm disorders. The market is driven by the growing incidence of cardiovascular diseases creating demand for pacemaker implantation across regions, technology development and innovation including leadless pacemakers and AI-powered remote monitoring solutions enhancing patient outcomes, and improved healthcare expenditure and infrastructure enabling broader patient access to cardiac rhythm management therapy. Remote monitoring and digital health technology adoption are improving patient management and post-implant care, while the expanding patient demographic is progressively broadening the addressable pacemaker patient base.

In 2024, Medtronic received FDA approval for the Micra AV2 leadless pacemaker, the next-generation version of the world's smallest pacemaker with enhanced AV synchrony capability that coordinates atrial and ventricular contractions without transvenous leads. The AV2's improved sensing algorithm extends synchronized pacing to a broader population of patients with AV block who previously required conventional transvenous dual-chamber systems, expanding the leadless pacemaker's clinical eligibility beyond the single-chamber Micra VR's patient population.

Market Size and Forecast:

-

Market Size in 2026E: USD 6.31 Billion

-

Market Size by 2035: USD 10.35 Billion

-

CAGR: 5.66% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

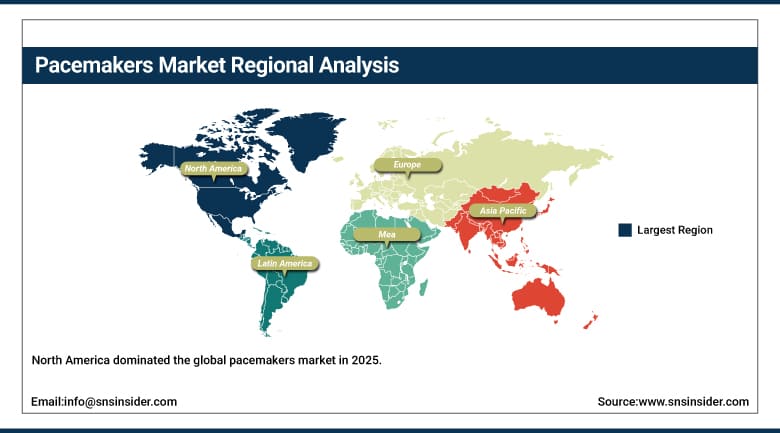

Largest Region: North America

To Get More Information On Pacemakers Market - Request Free Sample Report

Pacemakers Market Trends:

-

Leadless pacemakers are gaining adoption by eliminating leads and reducing infection risks, improving patient safety and outcomes.

-

MRI-compatible pacemakers are becoming standard as most patients require MRI scans during their device lifetime.

-

Remote monitoring solutions enable continuous patient tracking, reducing clinic visits and improving long-term device management efficiency.

-

Conduction system pacing improves physiological heart activation, offering advantages over traditional right ventricular pacing approaches.

-

AI-powered pacemakers automatically optimize device settings using patient data, enhancing personalization and therapy effectiveness.

U.S. Pacemakers Market Outlook:

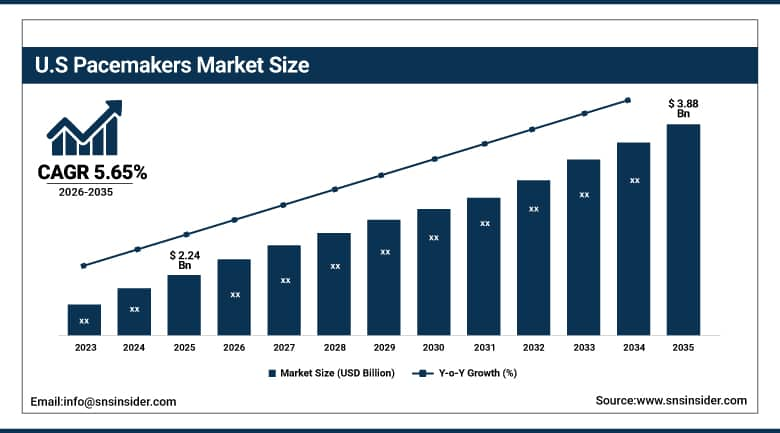

The U.S. Pacemakers Market was valued at approximately USD 2.24 Billion in 2025 and is expected to reach approximately USD 3.88 Billion by 2035, growing at a CAGR of approximately 5.65%.

The U.S. is the world’s most commercially significant pacemakers market within North America’s dominant revenue position. Medtronic, Abbott (St. Jude Medical), Boston Scientific, and BIOTRONIK’s U.S. commercial operations collectively define the North American cardiac rhythm management landscape. The FDA’s established pacemaker approval pathway, CMS’ national coverage determination for permanent cardiac pacemaker implantation, and the large electrophysiology and interventional cardiology community create the world’s most commercially mature pacemaker market. The aging U.S. population’s growing bradycardia and conduction disorder incidence, combined with the leading-edge technology adoption culture that sustains premium device specification including Micra leadless and MRI-conditional systems, creates the most commercially valuable per-implant pacemaker market globally.

Abbott received expanded FDA approval for the Aveir DR dual-chamber leadless pacemaker system in 2024, enabling the world's first fully leadless dual-chamber pacing system to communicate between separate atrial and ventricular leadless devices implanted through catheter delivery. The dual-chamber leadless system's ability to provide coordinated AV synchrony without any transvenous leads represents the most significant pacemaker technology advancement in decades, creating a new premium device category whose clinical differentiation from conventional lead systems creates above-commodity pricing that sustains above-average per-implant commercial value.

Pacemakers Market Segment Analysis:

-

By Product, the implantable pacemakers segment dominated the pacemakers market with 65.0% share in 2025, while the external/transcutaneous pacemakers segment serves acute hospital and emergency settings and is the fastest growing.

-

By Technology, the dual-chamber pacemakers segment dominated the pacemakers market with approximately 48% share in 2025, while the leadless pacemakers segment is the fastest growing.

-

By Application, the bradycardia segment dominated the pacemakers market with 24.5% share in 2025, while the congestive heart failure/CRT segment is the fastest growing.

-

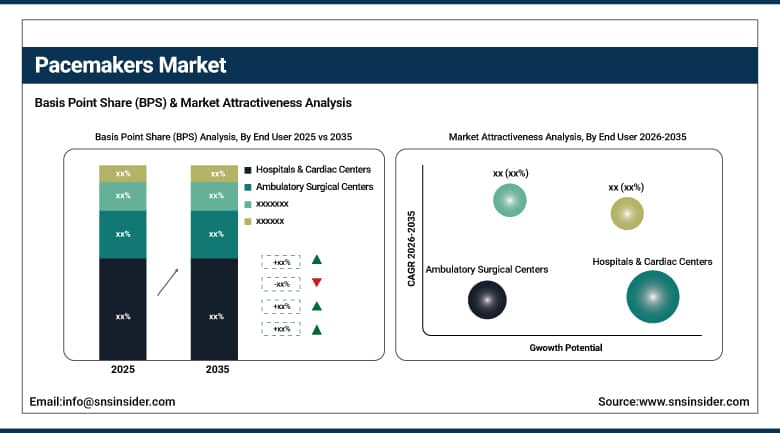

By End User, the hospitals & cardiac centers segment dominated the pacemakers market with approximately 65% share in 2025, while the ambulatory surgical centers segment is the fastest growing.

By End User, hospitals dominate, ASCs grow fastest

Hospitals and cardiac centers retained the dominant end-user position with approximately 65% of the pacemakers market in 2025. The pacemaker implantation procedure’s cardiac catheterization laboratory requirement, fluoroscopic guidance infrastructure, and post-implant electrophysiology monitoring necessity create inherent concentration in specialist cardiac facilities. Each hospital cardiac Center that establishes electrophysiology programme creates pacemaker implantation volume that scales with the programme’s patient referral network and procedural case volume.

Ambulatory surgical centers are the fastest-growing end user because technological simplification of selected pacemaker implantation procedures, particularly leadless pacemaker catheter delivery whose entirely endovascular approach eliminates surgical pocket creation, is creating outpatient eligibility for carefully selected lower-risk patients. Each ASC that establishes pacemaker implantation capability reduces per-procedure cost whose economics create payer motivation for outpatient procedure approval that compounds with the technology’s progressive simplification.

By Product, implantable dominates, external grows fastest in acute settings

Implantable pacemakers retained the dominant product position with 65.0% of the pacemakers market in 2025. Implantable pacemaker’s commercial primacy reflects its role as the definitive long-term cardiac rhythm management solution for the vast majority of patients with permanent conduction system disease. Each patient with symptomatic bradycardia, AV block, or sick sinus syndrome requiring pacemaker therapy creates implantable device procurement whose per-patient commercial value reflects the device’s multi-year therapeutic benefit at premium medical technology pricing. Medtronic’s, Abbott’s, and Boston Scientific’s comprehensive implantable pacemaker portfolios spanning single-chamber, dual-chamber, CRT, and leadless systems create the commercial diversity that sustains implantable segment dominance across diverse patient populations and clinical indications.

External pacemakers serve an essential acute setting role in perioperative management, post-cardiac surgery temporary pacing, and emergency bradycardia treatment whose hospital critical care infrastructure investment creates consistent procurement. The fastest growth in external pacemakers reflects critical care unit expansion, increasing cardiac surgery volumes, and the growing recognition of transcutaneous and transvenous temporary pacing’s role in bridging patients to permanent device implantation or recovery.

By Technology, dual-chamber dominates, leadless grows fastest

Dual-chamber pacemakers retained the dominant technology position with approximately 48% of the pacemakers market in 2025. Dual-chamber’s clinical superiority for the majority of pacemaker-indicated patients reflects the haemodynamic benefit of coordinated atrial-ventricular pacing whose maintenance of AV synchrony prevents pacemaker syndrome, improves cardiac output, and reduces atrial fibrillation risk relative to ventricular single-chamber alternatives. Each patient with second or third degree AV block, sick sinus syndrome with chronotropic incompetence, or symptomatic bradycardia requiring rate and AV synchrony support creates dual-chamber implantation whose clinical guideline endorsement sustains the technology’s dominant adoption.

Leadless pacemakers are the fastest-growing technology because the extraordinary recent clinical development from single-chamber to dual-chamber leadless capability, with Abbott’s Aveir DR and Medtronic’s Micra AV2 creating new clinical eligibility for patients with AV block, is creating rapidly expanding patient selection criteria. Each lead-related complication avoided through leadless implantation creates clinical outcome evidence whose documentation sustains physician adoption. The leadless pacemaker’s premium per-unit pricing above conventional transvenous systems creates above-average revenue growth per additional implant that sustains the segment’s fastest-growing commercial momentum.

By Application, bradycardia dominates, CRT grows fastest

Bradycardia retained the dominant application position with 24.5% of the pacemakers market in 2025. Bradycardia’s commercial primacy reflects its position as the most prevalent pacemaker indication whose sinus bradycardia, sick sinus syndrome, and AV block collectively create the largest aggregate pacemaker patient population. The aging population’s progressive conduction system degeneration creates consistent growth in bradycardia incidence that sustains the application category’s dominant commercial position. Each new bradycardia patient whose symptomatic heart rate below 60 bpm creates functional limitation creates pacemaker implantation motivation whose clinical benefit in symptom resolution and activity normalization sustains patient willingness to accept device therapy.

Congestive heart failure and CRT is the fastest-growing application because cardiac resynchronization therapy’s Class I guideline indication for heart failure patients with LVEF ≤35% and wide QRS creates systematic clinical adoption momentum that compounds with the extraordinary global heart failure burden. Each heart failure patient whose echocardiographic and ECG assessment identifies electrical desynchrony creates CRT pacemaker implantation eligibility whose treatment creates mortality reduction, hospitalization reduction, and quality of life improvement whose evidence sustains patient and physician therapy adoption.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Pacemakers Market Insights

North America dominated the global pacemakers market in 2025 with the highest per-capita pacemaker implantation rate and most commercially sophisticated cardiac rhythm management ecosystem. The United States accounts for approximately 87.4% of North American revenues through Medtronic, Abbott, and Boston Scientific’s commercial dominance whose combined portfolio creates the global pacemaker technology standard. FDA’s rapid device approval pathway, CMS’ national coverage determination, and the advanced electrophysiology community collectively sustain the U.S.’s premium device specification culture.

Canada contributes approximately 12.6% of North American revenues through its provincial healthcare system’s cardiac device programme, the growing electrophysiology specialist community, and Health Canada’s approved pacemaker portfolio creating consistent institutional procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Pacemakers Market Insights

Europe is a technically sophisticated pacemakers market where CE marking’s product approval standard, BIOTRONIK’s German commercial leadership, and the European Heart Rhythm Association’s clinical guideline infrastructure create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced cardiac Center network, BIOTRONIK’s domestic commercial presence, and the statutory health insurance’s cardiac device reimbursement.

France, Italy, and the United Kingdom are significant secondary markets where national health system cardiac device programmes, the cardiologist community’s technology adoption, and European guideline-driven CRT and leadless implantation growth create consistent pacemaker procurement.

Asia Pacific Pacemakers Market Insights

Asia Pacific is the fastest-growing regional pacemakers market, driven by the rapidly aging population’s growing bradycardia and conduction disorder incidence, expanding cardiac Center infrastructure, and the progressive adoption of advanced pacemaker technology including leadless systems. China accounts for approximately 44.8% of Asia Pacific revenues through its expanding hospital cardiac programme, the government’s healthcare investment, and the growing electrophysiology specialist community whose advanced device adoption creates above-average per-implant commercial value.

Japan’s advanced cardiac care infrastructure, South Korea’s sophisticated hospital system, and India’s rapidly expanding cardiac Center network create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Pacemakers Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced cardiac hospital network, the Ministry of Health’s cardiac device programme, and the growing electrophysiology community whose above-average technology adoption creates premium device procurement. Brazil leads Latin American revenues at approximately 44.2% through its large public hospital cardiac programme, the growing private cardiac Center network, and the electrophysiology community’s advanced device adoption.

UAE’s advanced private cardiac hospital sector and South Africa’s cardiac Center network create significant MEA secondary markets whose pacemaker procurement reflects the progressive adoption of advanced cardiac rhythm management across both national healthcare systems.

Market Dynamics:

Growth Drivers: Aging population increasing conduction disorder incidence and leadless technology expanding indication eligibility

The aging global population is the pacemakers market’s most structurally certain growth driver. The progressive degeneration of the cardiac conduction system with age creates exponentially increasing bradycardia and AV block incidence in the population demographic whose age distribution is most rapidly growing globally. Each year’s progression of the baby boomer cohort creates additional pacemaker candidates whose symptomatic bradycardia creates device implantation motivation. The WHO’s projection that the global population over 65 will double to 2 billion by 2050 creates a commercial demand trajectory whose pacemaker component compounds with aging population growth and advancing healthcare access.

Leadless pacemaker technology’s progressive expansion from single-chamber VVI to dual-chamber AV synchronous capability creates new clinical eligibility that substantially expands the leadless-indicated patient population beyond the initial AV block-free single-chamber indication. Each new leadless indication approval creates physician adoption momentum whose evidence-based expansion of clinical use creates commercial growth that compounds with premium device pricing.

Restraints: High device cost limiting access in emerging markets and reimbursement constraint in public healthcare systems

Pacemaker device cost, ranging from USD 3,000-15,000 for implantable systems depending on technology complexity, creates access barriers in emerging market healthcare systems whose public healthcare budget cannot accommodate universal cardiac device coverage at developed market implantation rates. Each healthcare system that restricts advanced pacemaker specification to government-approved basic devices creates market limitation that moderates premium technology adoption below the clinically indicated rate in cost-constrained environments.

Public healthcare system reimbursement constraint creates downward pricing pressure on established pacemaker technologies whose premium product differentiation must be justified within reimbursement category caps that moderate per-implant commercial value growth. Each health technology assessment decision that declines to reimburse premium pacemaker indications creates adoption limitation that moderates market growth below the technical capability frontier.

Opportunities: Conduction system pacing adoption and remote monitoring SaaS ecosystem

Conduction system pacing through His-bundle and left bundle branch area pacing represents the most clinically innovative near-term technique whose physiological ventricular activation pattern creates haemodynamic advantage over conventional right ventricular apex pacing. Each electrophysiology programme that adopts conduction system pacing as standard technique creates premium lead and programming procurement whose clinical outcomes evidence sustains adoption momentum.

Remote monitoring digital health ecosystem development creates the most commercially valuable long-term value addition to the pacemaker market. Each implanted pacemaker patient’s connection to a home monitoring platform creates recurring data subscription revenue whose per-patient annual value compounds with the growing global implanted device population. Medtronic’s CareLink, Abbott’s MyMerlin, and Boston Scientific’s LATITUDE collectively demonstrate the commercial ecosystem whose data management and clinical decision support value creates healthcare system adoption motivation that sustains SaaS revenue.

Recent Developments:

-

2026: Medtronic plc continued global expansion of the Micra AV2 and Micra VR2 leadless pacemaker platforms, featuring improved battery longevity and enhanced pacing algorithms.

-

2025: Abbott reported strong 2025 growth in its Cardiac Rhythm Management business driven by accelerating adoption of the AVEIR leadless pacemaker portfolio.

-

2025: Boston Scientific Corporation advanced development of the EMPOWER leadless pacemaker and modular CRM platform, integrating leadless pacing with subcutaneous ICD technology.

Pacemakers Market Key Players are:

-

Medtronic PLC

-

Abbott Laboratories (St. Jude Medical)

-

Boston Scientific Corporation

-

BIOTRONIK SE & Co. KG

-

MicroPort Scientific Corporation

-

Lepu Medical Technology Co., Ltd.

-

Shree Pacetronix Ltd.

-

Oscor Inc.

-

Osypka Medical GmbH

-

Shenzhen Qinming Medical Instruments Co., Ltd.

-

Shenzhen Pacemaker Medical Co., Ltd.

-

Sorin Group (LivaNova PLC)

-

Cook Medical Inc.

-

Braile Biopharma

-

CCC Medical Devices

-

Ela Medical (MicroPort)

-

Cardioelectronica

-

Vitatron

-

Sanan Medical

-

Medico S.p.A.

Pacemakers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.97 Billion |

| Market Size by 2035 | USD 10.35 Billion |

| CAGR | CAGR of 5.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Implantable Pacemakers, External/Transcutaneous Pacemakers) • By Technology (Single-Chamber, Dual-Chamber, Biventricular/CRT, Leadless Pacemakers) • By Application (Bradycardia, Sick Sinus Syndrome, Heart Block, Atrial Fibrillation, Congestive Heart Failure/CRT, Long QT Syndrome, Others) • By End User (Hospitals & Cardiac Centers, Ambulatory Surgical Centers, Cardiac Catheterization Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic PLC, Abbott Laboratories (St. Jude Medical), Boston Scientific Corporation, BIOTRONIK SE & Co. KG, MicroPort Scientific Corporation, Lepu Medical Technology Co., Ltd., Shree Pacetronix Ltd., Oscor Inc., Osypka Medical GmbH, Shenzhen Qinming Medical Instruments Co., Ltd., Shenzhen Pacemaker Medical Co., Ltd., Sorin Group (LivaNova PLC), Cook Medical Inc., Braile Biopharma, CCC Medical Devices, Ela Medical (MicroPort), Cardioelectronica, Vitatron, Sanan Medical, Medico S.p.A. |

Frequently Asked Questions

The Pacemakers Market is expected to grow at a CAGR of 5.66% from 2026 to 2035.

The Pacemakers Market was valued at USD 5.97 Billion in 2025.

Growing incidence and prevalence of cardiovascular diseases and conduction disorders in an aging global population creating pacemaker implantation demand.

Implantable Pacemakers dominated the Pacemakers Market with 65.0% share in 2025.

Bradycardia dominated the Pacemakers Market with 24.5% share in 2025.

Get in Touch