Chlorine Dioxide Market Report Scope & Overview:

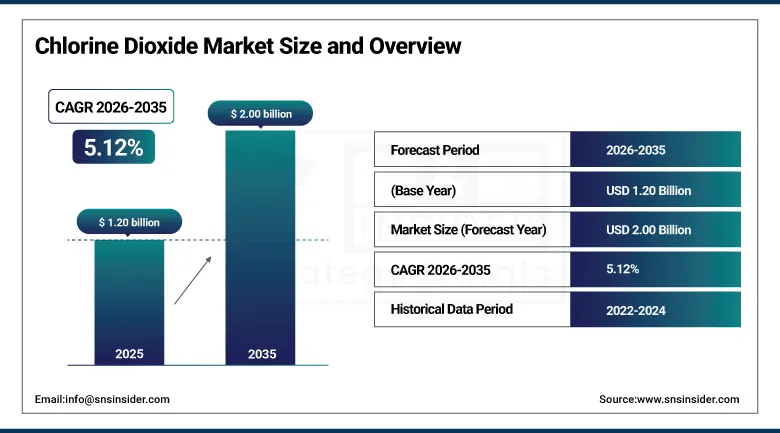

The Chlorine Dioxide Market was valued at USD 1.20 Billion in 2025 and is expected to reach USD 2.00 Billion by 2035, growing at a CAGR of 5.12% from 2026–2035.

The global chlorine dioxide market is growing at a sustained and commercially broad-based pace. Chlorine dioxide (ClO₂) is a powerful oxidizing and disinfecting agent. Its ability to eliminate bacteria, viruses, biofilms, and organic contaminants at low concentrations without producing trihalomethane or haloacetic acid disinfection by-products creates environmental and regulatory advantages over chlorine-based alternatives. The market is driven by the growing demand for water treatment, increasing regulatory restrictions on organochlorine compounds in pulp bleaching, the surge in food and beverage industry antimicrobial application demand, and the rising adoption of on-site chlorine dioxide generation systems that improve safety and reduce transportation logistics costs for this hazardous chemical.

In 2024, Ecolab expanded its Seloxy chlorine dioxide generation system portfolio with new compact on-site generation units designed for food processing and beverage facilities, enabling smaller operations to adopt ClO₂ sanitation. The expansion reflects the commercial strategy of creating accessible entry points for food and beverage sector adoption whose regulatory pressure for effective pathogen control at food contact surfaces creates structured demand for alternatives to conventional chlorine sanitizers.

Market Size and Forecast

-

Market Size in 2026E: USD 1.26 Billion

-

Market Size by 2035: USD 2.00 Billion

-

CAGR: 5.12% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Chlorine Dioxide Market - Request Free Sample Report

Chlorine Dioxide Market Trends

-

On-site chlorine dioxide generation systems are gaining adoption by improving safety, reducing transport risks, and supporting regulatory compliance in water treatment facilities.

-

Phase-out of chlorine-based bleaching in pulp and paper industries is driving demand for chlorine dioxide as an eco-friendly alternative bleaching agent.

-

Food and beverage sector usage is increasing for produce washing and sanitation due to GRAS status and low sensory impact of chlorine dioxide.

-

Smart monitoring and automated dosing systems are improving chlorine dioxide control efficiency, ensuring regulatory compliance and optimized chemical usage.

-

Healthcare applications are expanding as chlorine dioxide is adopted for high-level disinfection of surfaces, equipment, and air systems post-pandemic.

The U.S. Chlorine Dioxide Market Outlook

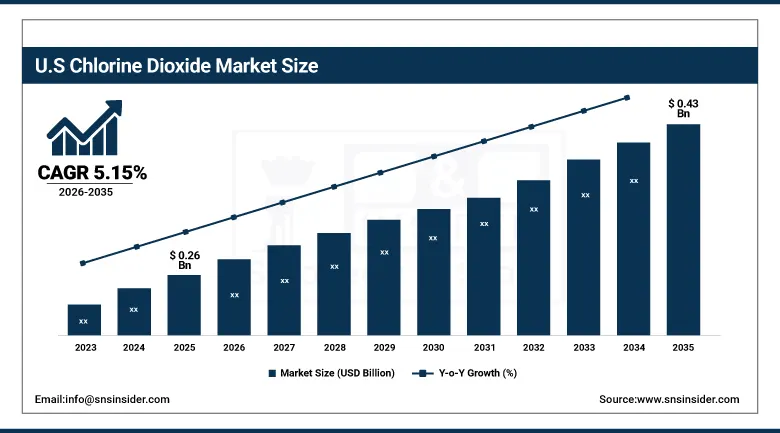

The U.S. chlorine dioxide market was valued at approximately USD 0.26 Billion in 2025 and is expected to reach approximately USD 0.43 Billion by 2035, growing at a CAGR of approximately 5.15%.

The U.S. is the most commercially sophisticated chlorine dioxide market within North America. Ecolab, Evoqua Water Technologies, CDG Environmental, and ERCO Worldwide serve the domestic market across water treatment, food processing, pulp bleaching, and industrial applications. EPA's Stage 2 Disinfectants and Disinfection By-Products Rule create regulatory motivation for municipal water utilities to evaluate chlorine dioxide's DBP-free profile as an alternative to chlorination for finished water disinfection. USDA FSIS's food processing water treatment approval for chlorine dioxide in poultry and meat processing creates structured food sector procurement that sustains the U.S. food and beverage application development.

Evoqua Water Technologies launched its OSEC electrolytic chlorine dioxide generation system upgrade in 2024 with enhanced efficiency and digital connectivity. The upgrade addresses the dual requirement of water utilities whose EPA Stage 2 DDBPR compliance creates motivation for DBP-reducing disinfection alternatives and whose operational efficiency programme creates demand for automated dosing management that reduces chemical consumption and operator intervention.

Chlorine Dioxide Market Segment Analysis

-

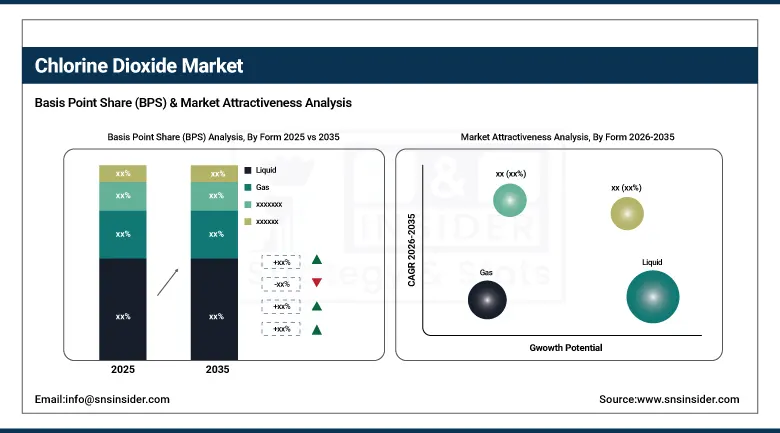

By Form, the liquid segment dominated the chlorine dioxide market with approximately 60% share in 2025, while the gas segment is the fastest growing.

-

By Application, the industrial water treatment segment dominated the chlorine dioxide market with approximately 38% share in 2025, while the food & beverages segment is the fastest growing.

-

By End User, the pulp & paper industry segment dominated the chlorine dioxide market with approximately 35% share in 2025, while the municipal water treatment segment is the fastest growing.

By Form, liquid dominates, gas grows fastest

Liquid chlorine dioxide retained the dominant form position with approximately 60% of the chlorine dioxide market in 2025. Liquid form’s commercial primacy reflects the relative simplicity of stabilized liquid ClO₂ formulations distribution and application logistics compared to gaseous generation systems whose infrastructure and safety management requirements create higher adoption barriers. Stabilized liquid chlorine dioxide solutions, typically at concentrations of 0.5-5% ClO₂, are compatible with standard chemical dosing pump infrastructure whose familiarity across industrial and food processing operations creates specification accessibility.

Gas is the fastest-growing form because on-site electrolytic and chemical precursor generation technology’s progressive improvement in safety, control precision, and capital cost accessibility is creating adoption of gaseous ClO₂ in applications whose performance requirements demand the superior biofilm penetration and dissolved organic matter reactivity that gaseous delivery provides. Municipal drinking water treatment’s taste and odor control application, and hospital disinfection’s fumigation application each create structured demand for generated gaseous ClO₂ whose performance advantages over stabilized liquid alternatives justify the on-site generation infrastructure investment.

By Application, industrial water treatment dominates, food & beverages grows fastest

Industrial water treatment retained the dominant application position with approximately 38% of the chlorine dioxide market in 2025. ClO₂’s exceptional efficacy against biofilm-forming bacteria including Legionella, its stable biocidal activity across a broad pH range of 4-10, and its oxidative capacity against sulfur-reducing bacteria create specification advantages in cooling tower water treatment whose Legionella control requirement sustains consistent industrial procurement. Process water disinfection in pharmaceutical, chemical, and electronics manufacturing facilities creates structured industrial water treatment demand that sustains the application category’s commercial dominance.

Food and beverages is the fastest-growing application because food safety regulatory pressure, consumer expectations for pathogen-free fresh produce, and the food processing industry’s search for DBP-free sanitizers that maintain sensory quality are creating structured above-average ClO₂ demand growth. USDA FSIS-approved chlorine dioxide application in poultry processing water reduces Salmonella and Campylobacter contamination without creating chlorinated off-flavors that conventional chlorine alternatives produce.

By End User, pulp & paper dominates, municipal water treatment grows fastest

Pulp and paper retained the dominant end-user position with approximately 35% of the chlorine dioxide market in 2025. The pulp and paper industry’s adoption of elemental chlorine-free bleaching sequences as the global standard, driven by environmental regulation restricting organochlorine compound formation and the paper market’s customer specification for ECF-bleached pulp, creates high-volume consistent ClO₂ consumption that sustains the industry’s dominant market position.

Municipal water treatment is the fastest-growing end user because EPA’s Stage 2 Disinfectants and Disinfection By-Products Rule’s maximum contaminant level compliance requirement is creating evaluation of chlorine dioxide as a primary disinfectant whose DBP formation profile producing chlorite and chlorate and haloacetic acids creates regulatory differentiation for utilities whose source water organic matter creates DBP compliance challenges with conventional chlorination. Each municipal water utility that adopts ClO₂ as a pre-oxidant or primary disinfectant creates procurement whose volume scales with the system’s treatment capacity.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Chlorine Dioxide Market Insights

North America is the fastest-growing regional chlorine dioxide market, driven by EPA Stage 2 DDBPR compliance motivation in municipal water treatment, the food processing sector’s regulatory-driven pathogen control investment, and the pulp and paper industry’s established ECF bleaching infrastructure. The United States accounts for approximately 87.4% of North American revenues through Ecolab, Evoqua, CDG Environmental, and ERCO World wide’s commercial operations.

Canada contributes approximately 12.6% of North American revenues through its large pulp and paper industry’s ClO₂ consumption, the municipal water treatment sector’s progressive DBP compliance investment, and ERCO World wide’s Canadian ClO₂ production operations whose supply to both domestic and export markets sustain North American commercial scale.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chlorine Dioxide Market Insights

Europe is a technically sophisticated chlorine dioxide market where EU water framework directive requirements, REACH regulation’s chemical safety framework, and the Biocidal Products Regulation’s ClO₂ approval create structured institutional demand across water treatment, food processing, and healthcare applications. Germany accounts for approximately 22.3% of European revenues through its advanced industrial water treatment, ProMinent GmbH’s domestic manufacturing and commercial operations, and the food processing sector’s stringent hygiene standard.

The United Kingdom, France, and the Netherlands are significant secondary markets where the pulp industry’s ECF bleaching, municipal water treatment investment, and food processing sector’s antimicrobial application create consistent ClO₂ procurement. EU BREF documents for food processing and water treatment create regulatory framework that sustains institutional ClO₂ adoption motivation.

Asia Pacific Chlorine Dioxide Market Insights

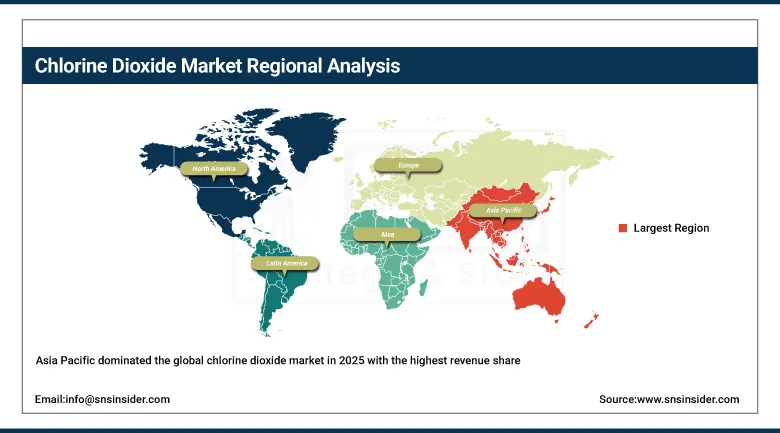

Asia Pacific dominated the global chlorine dioxide market in 2025 with the highest revenue share. China accounts for approximately 44.8% of Asia Pacific revenues through its large pulp and paper industry’s ECF bleaching adoption, the extraordinary scale of industrial water treatment requirements across chemical, petrochemical, and manufacturing sectors, and the growing food processing industry’s antimicrobial application. The region’s rapid industrialization, expanding food processing sector, and progressive water quality regulation create above-average ClO₂ demand growth that sustains Asia Pacific’s commercial leadership.

India, Japan, and South Korea are significant secondary markets within Asia Pacific where textile processing water treatment, electronics manufacturing process water, and expanding food export sector quality compliance create consistent ClO₂ procurement that compounds with industrial development investment.

MEA & Latin America Chlorine Dioxide Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its desalination plant biofouling control, industrial water treatment in petrochemical facilities, and the food processing sector’s HACCP compliance creating antimicrobial procurement. Brazil leads Latin American revenues at approximately 44.2% through its large pulp and paper industry whose eucalyptus kraft ECF bleaching creates significant ClO₂ consumption, and the food processing sector’s export quality requirement sustaining antimicrobial application investment.

UAE’s advanced industrial water treatment and South Africa’s paper industry create significant MEA secondary markets whose ClO₂ procurement reflects the regional industrial development and food safety standard advancement.

Market Dynamics

Growth Drivers: Water treatment DBP regulation and pulp bleaching organochlorine restriction creating structural ClO₂ demand

EPA Stage 2 Disinfectants and Disinfection By-Products Rule’s maximum contaminant level requirements for trihalomethanes and haloacetic acids create the most commercially certain structural ClO₂ demand driver in the water treatment market. Each municipal water utility whose source water total organic carbon creates DBP formation during chlorination that exceeds Stage 2 MCLs has regulatory compliance motivation for ClO₂ adoption as a pre-oxidant or primary disinfectant whose reaction with organic matter forms chlorite and chlorate rather than regulated THM and HAA compounds.

Environmental regulation restricting elemental chlorine use in pulp bleaching creates the most commercially established structural ClO₂ demand across the paper industry’s ECF bleaching sequences. Each paper mill that maintains ECF bleaching certification for European and North American market access creates consistent ClO₂ procurement whose long-term supply agreements sustain commercial relationships.

Restraints: Chlorite and chlorate by-product regulatory limits and ClO₂ instability creating handling complexity

Chlorite and chlorate, ClO₂’s primary disinfection by-products, are regulated by EPA’s Stage 1 DDBPR whose maximum contaminant level for chlorite at 1.0 mg/L creates operational constraints for municipal water utilities that must balance adequate ClO₂ dosing for disinfection efficacy against chlorite accumulation limits. Each utility whose source water and distribution system characteristics create chlorite MCL compliance challenges creates adoption limitation that constrains ClO₂ application rate and commercial procurement volume.

Chlorine dioxide’s instability above 10% concentration creating explosion risk, its requirement for on-site generation or stabilized precursor chemistry for safe transport, and the technical expertise required for safe system operation create adoption barriers in smaller industrial and commercial applications.

Opportunities: Food safety regulatory expansion and healthcare disinfection adoption

Food safety regulatory expansion globally, with FDA’s Food Safety Modernization Act’s preventive control requirements and USDA FSIS’s pathogen reduction performance standards, is creating structured institutional motivation for ClO₂ adoption in food processing water treatment whose efficacy against regulated pathogens creates compliance value. Each new FDA food safety guidance that endorses ClO₂ as an approved antimicrobial agent creates market access for new food processing application categories.

Healthcare and hospital disinfection represents a growing premium application whose broad-spectrum efficacy against Clostridioides difficile spores, MRSA, Candida auris, and COVID-19 creates institutional procurement motivation beyond conventional disinfectant alternatives. ClO₂’s ability to penetrate and eliminate biofilms in hospital HVAC and water systems creates Legionella management application whose patient safety motivation sustains premium system investment.

Recent Developments:

-

2025: Ecolab expanded chlorine dioxide-based water treatment solutions for food processing plants, strengthening industrial hygiene and sanitation compliance globally.

-

2025: IEC Fabchem Limited received regulatory approvals in India for new chlorine dioxide product lines, expanding industrial and municipal water treatment applications.

-

2025: Industry shift toward on-site chlorine dioxide generation systems accelerated due to safety improvements, reduced storage risks, and regulatory compliance needs.

Chlorine Dioxide Market Key Players are:

-

Ecolab Inc.

-

Xylem Inc.

-

ProMinent GmbH

-

Grundfos Pumps Corporation

-

CDG Environmental LLC

-

ERCO Worldwide (Superior Plus Energy)

-

Sabre Technologies LLC

-

Accepta Ltd.

-

AquaPulse Systems Inc.

-

Tecme Srl

-

Iotronic Elektrogerätebau GmbH

-

IEC Fabchem Limited

-

Vasu Chemicals LLP

-

Occidental Chemical (OxyChem)

-

Bio-Cide International Inc.

-

Ioteq Chemicals

-

Shree Chlorates

-

American Elements

-

Akzo Nobel N.V.

-

Gulbrandsen Chemicals Inc.

Chlorine Dioxide Market Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.20 Billion |

| Market Size by 2035 | USD 2.00 Billion |

| CAGR | CAGR of 5.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form (Liquid, Gas, Powder/Solid) • By Application (Industrial Water Treatment, Pulp & Paper Processing, Oil & Gas, Medical & Healthcare, Food & Beverages, Municipal Water Treatment, Others) • By End User (Pulp & Paper Industry, Municipal Water Treatment, Industrial Water Treatment, Food & Beverage Industry, Healthcare & Pharmaceutical, Oil & Gas Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ecolab Inc., Xylem Inc., ProMinent GmbH, Grundfos Pumps Corporation, CDG Environmental LLC, ERCO Worldwide (Superior Plus Energy), Sabre Technologies LLC, Accepta Ltd., AquaPulse Systems Inc., Tecme Srl, Iotronic Elektrogerätebau GmbH, IEC Fabchem Limited, Vasu Chemicals LLP, Occidental Chemical (OxyChem), Bio-Cide International Inc., Ioteq Chemicals, Shree Chlorates, American Elements, Akzo Nobel N.V., Gulbrandsen Chemicals Inc. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 5.12% from 2026 to 2035.

The market was valued at USD 1.20 Billion in 2025.

Growing demand for water treatment solutions that avoid trihalomethane and haloacetic acid disinfection by-products.

Liquid dominated the market with approximately 60% share in 2025.

Asia Pacific dominated the market in 2025 with the highest revenue share.

Get in Touch