Clinical Communication and Collaboration Market Report Scope & Overview:

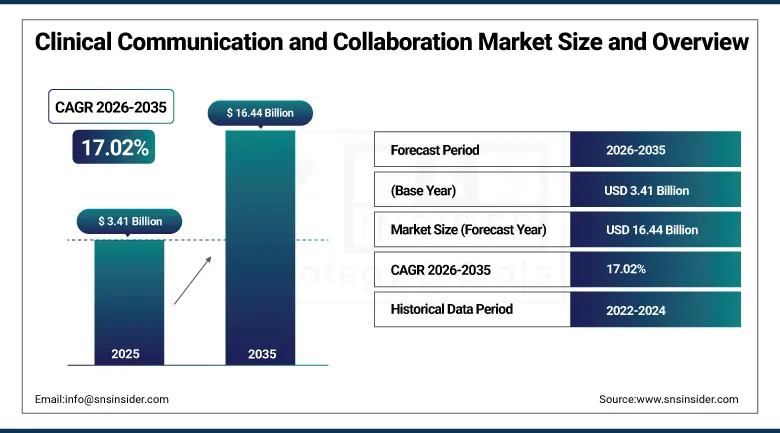

The Clinical Communication and Collaboration Market was valued at USD 3.41 Billion in 2025 and is expected to reach USD 16.44 Billion by 2035, growing at a CAGR of 17.02% from 2026–2035.

The global clinical communication and collaboration market is experiencing exceptional growth driven by an imperative need for efficient communication in the healthcare sector and the systematic replacement of legacy pager and telephone-based communication with unified digital platforms. Clinical communication and collaboration solutions encompass secure messaging, voice communication and EHR workflow connectivity that collectively eliminate the communication failures responsible for 80% of serious medical errors according to the Joint Commission. An analysis of 23,000 medical malpractice lawsuits revealed that more than 7,000 cases directly resulted from communication breakdowns, costing USD 1.7 billion and resulting in nearly 2,000 preventable deaths, creating compelling patient safety and financial motivation for CC&C platform investment. The U.S. Department of Health and Human Services’ emphasis on interoperable systems to enhance patient care coordination sustains structured government-sector market demand.

In 2024, TigerConnect expanded its clinical communication platform with AI-powered smart routing that automatically directs urgent clinical alerts to the correct on-call clinician based on role, specialty, and availability schedule, eliminating manual look-up delays that previously required nurses to call answering services or page overhead to locate the appropriate physician. The enhancement demonstrates the commercial direction of CC&C platform development toward intelligent workflow automation whose AI decision layer creates patient safety improvements measurable in sentinel event reduction metrics.

Market Size and Forecast

-

Market Size in 2026E: USD 3.99 Billion

-

Market Size by 2035: USD 16.44 Billion

-

CAGR: 17.02% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Clinical Communication and Collaboration Market - Request Free Sample Report

Clinical Communication and Collaboration Market Trends

-

AI-powered clinical decision support integration is enhancing care coordination through automated alert management, urgent notification routing, and real-time clinical risk detection

-

Growing adoption of EHR-integrated CC&C platforms is enabling seamless communication workflows across major healthcare information systems and care teams

-

Integration of telehealth capabilities with clinical communication platforms is improving coordination between in-person and virtual care environments

-

Increasing use of wearable communication devices is supporting hands-free collaboration and workflow efficiency for clinicians in fast-paced healthcare settings

-

Cybersecurity, data privacy, and regulatory compliance capabilities are becoming key purchasing criteria as healthcare organizations prioritize secure communication and patient information protection solutions

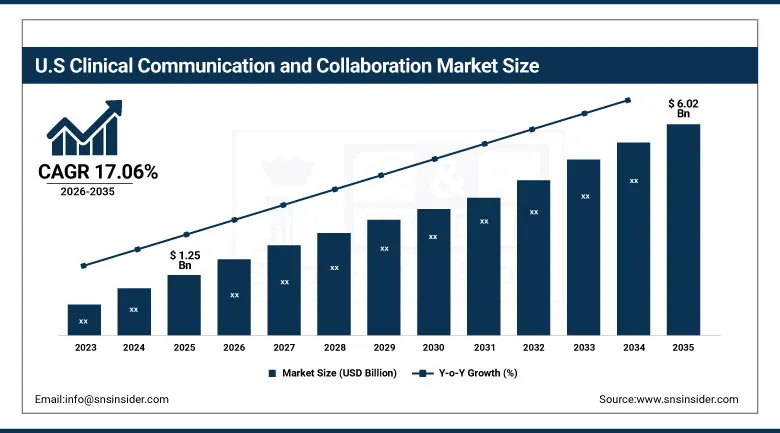

U.S. Clinical Communication and Collaboration Market Outlook

The U.S. Clinical Communication and Collaboration Market was valued at approximately USD 1.25 Billion in 2025 and is expected to reach approximately USD 6.02 Billion by 2035, growing at a CAGR of approximately 17.06%.

The U.S. is the world's most commercially sophisticated clinical communication and collaboration market within North America's dominant revenue position. The Joint Commission's sentinel event reporting requirements, HIPAA’s secure PHI communication mandates, and CMS’s value-based care quality metrics whose communication quality influences reimbursement collectively create structured institutional CC&C platform investment motivation across the U.S. healthcare system. The 59% decrease in communication failures reported by Cincinnati Children's Hospital Medical Center after pager replacement demonstrates the measurable patient safety improvement that sustains premium CC&C specification.

In 2023, Vocera (Stryker) launched an enhanced Vocera Platform integration with Epic EHR that enables automated clinical alert routing based on Epic patient assignment data, eliminating the manual nurse-to-EHR workflow interruption that required separate clinician lookup before alert delivery. The integration demonstrates the commercial value of EHR-native CC&C workflow automation whose contextual intelligence creates alert routing precision that standalone CC&C platforms without EHR connectivity cannot achieve.

Clinical Communication and Collaboration Market Segment Analysis

-

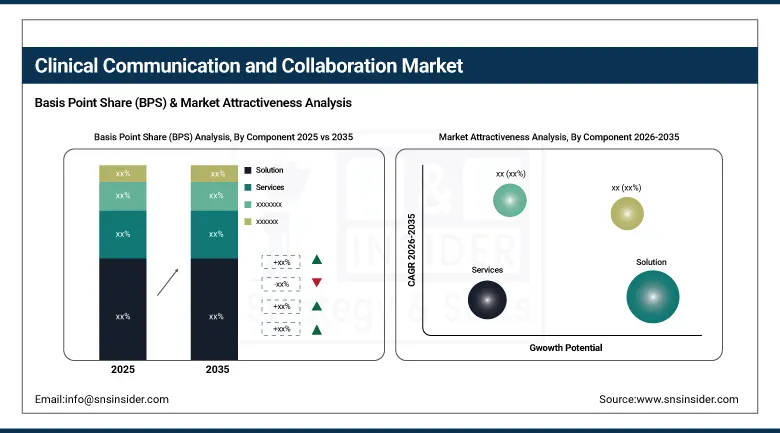

By Component, the Solution segment dominated the Clinical Communication and Collaboration Market with approximately 65% share in 2025, while the Services segment is the fastest growing with a CAGR of approximately 19.17%.

-

By Deployment, the Hosted/Cloud segment dominated the Clinical Communication and Collaboration Market with approximately 58% share in 2025, while the On-Premises deployment segment is the fastest growing.

-

By End Use, the Hospitals segment dominated the Clinical Communication and Collaboration Market with approximately 62% share in 2025, while the Physicians segment is the fastest growing.

By Component, solution dominates, services grow fastest

Solutions retained the dominant component position with approximately 65% of the clinical communication and collaboration market in 2025. The commercial insight from cross-industry CC&C research confirms that software captured 65.63% share in 2025 as device-agnostic, rapidly deployable solutions that leverage existing smartphones and PCs create commercially accessible CC&C adoption without dedicated hardware investment. Each hospital that adopts a cloud-delivered CC&C platform creates solution subscription revenue whose recurring character sustains commercial relationships through multi-year contracts. The CC&C solution’s integration with EHR, patient monitoring, and clinical alert systems creates embedded workflow value that sustains subscription renewal motivation beyond any single feature consideration.

Services are the fastest-growing component at approximately 19.17% CAGR because the complexity of enterprise CC&C migrations, whose scope encompasses workflow redesign, EHR integration configuration, change management across clinician user populations, and HIPAA compliance validation, creates multi-year consulting and implementation service demand that sustains above-average service segment revenue growth. Each major health system that migrates from pager-based to unified CC&C platform creates a multi-phase service engagement whose combined consulting, implementation, training, and managed service revenue substantially exceeds the software license value in the migration programme’s first two years.

By Deployment, cloud dominates, on-premises grows for regulated environments

Hosted and cloud deployment retained the dominant position with approximately 58% of the clinical communication and collaboration market in 2025. Cloud CC&C’s commercial advantages encompass automatic software updates that eliminate the manual upgrade cycle whose downtime risk creates hesitation in clinical environments, elastic scaling that accommodates patient census variation without infrastructure provisioning, and geographic redundancy that sustains platform availability during local infrastructure failures. Healthcare systems operating across multiple hospital campuses benefit particularly from cloud CC&C’s unified communication environment that on-premises alternatives serving individual site installations cannot efficiently replicate across distributed geographic footprints.

On-premises deployment is the fastest-growing segment because regulated healthcare environments including government hospital networks, Veterans Affairs facilities, and defense healthcare organizations whose classified or sensitive PHI processing creates data sovereignty requirements that mandate localized infrastructure are creating structured on-premises CC&C procurement. Each healthcare organization whose compliance framework prevents cloud PHI processing creates on-premises deployment demand that compounds with regulatory tightening in government-sector healthcare.

By End Use, hospitals dominate, physicians grow fastest

Hospitals retained the dominant end-use position with approximately 62% of the clinical communication and collaboration market in 2025. The hospital environment’s communication complexity, encompassing multi-specialty care teams, shift-change handoff coordination, emergency response activation, and continuous patient monitoring alert management, creates the most commercially intensive CC&C platform deployment requirement of any healthcare setting. The Joint Commission’s finding that 80% of serious medical errors are associated with miscommunication during care transfer creates patient safety motivation for hospital CC&C investment that is independent of operational efficiency ROI. Each hospital that replaces pagers with unified CC&C platforms creates a commercial relationship whose EHR integration, ongoing training, and platform expansion sustain long-duration revenue.

Physicians and ambulatory care are the fastest-growing segment because care delivery’s systematic migration toward outpatient settings, telemedicine, and physician group practices creates CC&C adoption among care teams that historically lacked enterprise communication platform investment. Each ambulatory surgical center, specialty physician practice, and integrated physician network that adopts CC&C for care team coordination and telehealth integration creates new commercial procurement channels whose aggregate compounds with the outpatient care sector’s extraordinary growth pace. The Hospital of the University of Pennsylvania’s 14% decrease in patient days from secure messaging implementation demonstrates measurable outcome improvement that physician practice administrators increasingly use as CC&C investment justification.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Clinical Communication and Collaboration Market Insights

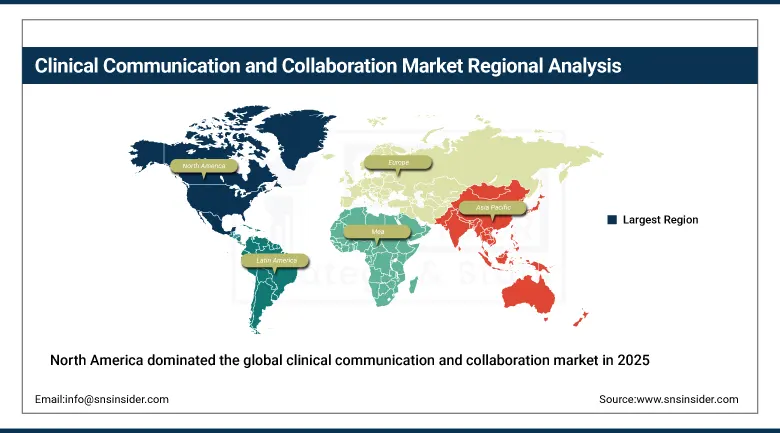

North America dominated the global clinical communication and collaboration market in 2025 driven by the most advanced digital health infrastructure, stringent regulatory requirements for secure clinical communication, and the highest per-capita healthcare IT investment globally. The United States accounts for approximately 87.4% of North American revenues through TigerConnect, Vocera (Stryker), Spok Holdings, Cisco, and Cerner's commercial operations whose combined portfolio defines the domestic CC&C technology standard.

Canada contributes approximately 12.6% of North American revenues through its provincial health system’s digital health transformation programme’s, the healthcare interoperability investment, and the growing telehealth sector’s care coordination platform demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Clinical Communication and Collaboration Market Insights

Europe is a technically sophisticated clinical communication and collaboration market where NHS England’s digital transformation programme, EU eHealth interoperability frameworks, and GDPR’s secure health data communication requirements create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its hospital sector’s digital health investment, the Telematik-Infrastruktur connectivity programme, and the healthcare IT sector’s CC&C platform adoption.

The United Kingdom and France are significant secondary markets where NHS’s systematic pager replacement programme creating structured CC&C procurement and France’s Hébergeurs de Données de Santé certified cloud health data framework creating secure messaging adoption motivation.

Asia Pacific Clinical Communication and Collaboration Market Insights

Asia Pacific is the fastest-growing regional clinical communication and collaboration market, driven by China's healthcare digitalization investment, India's Ayushman Bharat Digital Mission creating health IT infrastructure, Japan's hospital information system modernization, and Southeast Asia's growing private hospital sector’s digital communication investment. China accounts for approximately 44.8% of Asia Pacific revenues through its hospital digital transformation programme, the government’s healthcare interoperability mandate, and the private hospital sector’s premium CC&C platform adoption.

India represents the most commercially dynamic emerging market within Asia Pacific where the Ayushman Bharat Digital Mission’s health ID and health data exchange infrastructure creates the interoperability foundation whose CC&C platform integration creates structured procurement motivation across the growing private hospital and physician network sectors.

MEA & Latin America Clinical Communication and Collaboration Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s healthcare digitalization investment, the Ministry of Health’s hospital communication platform programme, and the growing private hospital sector’s premium CC&C adoption. Brazil leads Latin American revenues at approximately 44.2% through its large private hospital network’s digital health investment, the SUS public health system’s interoperability programme, and the growing telehealth sector’s care coordination platform demand. Growing healthcare digitization across both regions and expanding telemedicine adoption collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Patient safety imperative and pager replacement mandate creating systematic CC&C procurement

The patient safety imperative created by documented evidence that 80% of serious medical errors involve communication failures during care transfers creates non-discretionary CC&C platform investment motivation across healthcare systems whose quality metrics, accreditation requirements, and malpractice liability collectively sustain premium platform specification. Each Joint Commission accreditation cycle that evaluates communication system adequacy creates institutional motivation for CC&C investment whose patient safety documentation value sustains procurement independent of operational efficiency ROI calculation.

The systematic healthcare sector migration from pagers, which remain deployed in over 80% of U.S. hospitals despite their limitations, toward unified digital CC&C platforms is creating the most commercially significant replacement procurement cycle in clinical communication history. Each hospital that eliminates pager infrastructure creates CC&C platform procurement whose deployment scope across the hospital’s clinician population creates multi-year subscription revenue that compounds with EHR integration and advanced feature adoption.

Restraints: EHR integration complexity and clinician change management resistance

EHR integration complexity creates implementation barriers whose engineering effort and extended configuration timeline require healthcare IT investment that competes with other digital health project priorities. Each EHR system version update creates CC&C platform integration re-validation requirements whose maintenance burden moderates the speed at which integrated workflow value is delivered to clinician end users.

Clinician resistance to workflow change, particularly among physicians whose established communication habits create adoption barriers for new platform requirements, moderates the pace of CC&C platform utilization growth after initial deployment. Each hospital that deploys CC&C but faces incomplete clinician adoption creates partial value realization whose ROI limitation moderates expansion investment enthusiasm in subsequent budget cycles.

Opportunities: AI-powered care coordination and rural/ambulatory care CC&C expansion

AI-powered care coordination represents the most commercially premium CC&C platform development direction whose intelligent alert routing, predictive care team assembly, and automated handoff documentation create clinical workflow automation that sustains premium platform pricing above basic secure messaging alternatives. Each AI feature that demonstrates measurable reduction in response time, missed alert, or communication failure creates evidence-based justification for platform upgrade procurement.

Rural and ambulatory care CC&C expansion represents the most commercially accessible near-term growth opportunity whose care setting migration from inpatient toward outpatient creates new CC&C procurement channels previously served by informal communication methods. Each rural critical access hospital and ambulatory surgery center that adopts CC&C for care coordination creates commercial procurement that compounds with the outpatient care sector’s growth trajectory.

Recent Developments:

-

2024: TigerConnect expanded its clinical communication platform in 2024 with AI-powered smart routing that automatically directs urgent clinical alerts to the correct on-call clinician based on role, specialty, and availability schedule, eliminating manual look-up delays in physician location.

-

2024: Vocera (Stryker) launched enhanced Vocera Engage platform updates in 2024 with improved AI-driven workflow automation and expanded integration with Epic EHR clinical documentation, enabling context-aware alert routing based on real-time patient assignment data.

-

2023: Vocera (Stryker) launched the enhanced Vocera Platform integration with Epic EHR in 2023, enabling automated clinical alert routing based on Epic patient assignment data and eliminating the manual nurse-to-EHR workflow interruption required for clinician identification before alert delivery.

-

2023: Spok Holdings introduced its Spok Care Connect platform upgrade in 2023 with enhanced HIPAA-compliant secure messaging, on-call schedule management, and critical test result notification automation, targeting the large installed base of hospital pager system users seeking migration to unified digital communication platforms.

-

2023: Microsoft extended Teams integration capabilities for healthcare communication in 2023 through expanded Microsoft Cloud for Healthcare CC&C features, enabling clinical teams to use secure Teams-based messaging with EHR workflow integration for care coordination across hospital and ambulatory care settings.

Clinical Communication and Collaboration Market Key Players

-

TigerConnect Inc.

-

Vocera Communications Inc. (Stryker Corporation)

-

Spok Holdings Inc.

-

Cisco Systems Inc.

-

Microsoft Corporation

-

Epic Systems Corporation

-

Oracle Health (Cerner Corporation)

-

Imprivata Inc.

-

Halo Health

-

OnPage Corporation

-

Ascom Holding AG

-

Starfish Medical

-

PerfectServe Inc.

-

Diagnotes Inc.

-

PatientSafe Solutions (CipherHealth)

-

Medscape (WebMD Health)

-

Cureatr Inc.

-

Paging Solutions Inc.

-

MobileSmith Health

-

CareCore National

Clinical Communication and Collaboration Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.41 Billion |

| Market Size by 2035 | USD 16.44 Billion |

| CAGR | CAGR of 17.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution, Services) • by Deployment (Hosted/Cloud, On-premises) • by End Use (Hospitals, Physicians, Clinical Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | TigerConnect Inc., Vocera Communications Inc., Spok Holdings Inc., Cisco Systems Inc., Microsoft Corporation, Epic Systems Corporation, Oracle Health, Imprivata Inc., Halo Health, OnPage Corporation, Ascom Holding AG, Starfish Medical, PerfectServe Inc., Diagnotes Inc., PatientSafe Solutions, Medscape, Cureatr Inc., Paging Solutions Inc., MobileSmith Health, CareCore National |

Frequently Asked Questions

The Clinical Communication and Collaboration Market is expected to grow at a CAGR of 17.02% from 2026 to 2035.

The Clinical Communication and Collaboration Market was valued at USD 3.41 Billion in 2025.

The patient safety imperative from documented evidence that 80% of serious medical errors involve communication failures creating non-discretionary CC&C investment, and the systematic healthcare sector migration from legacy pager infrastructure toward unified digital platforms creating the most commercially significant replacement cycle in clinical communication history.

Solution dominated the Clinical Communication and Collaboration Market with approximately 65% share in 2025, while Services is the fastest growing segment with a CAGR of approximately 19.17%.

North America dominated the Clinical Communication and Collaboration Market in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch