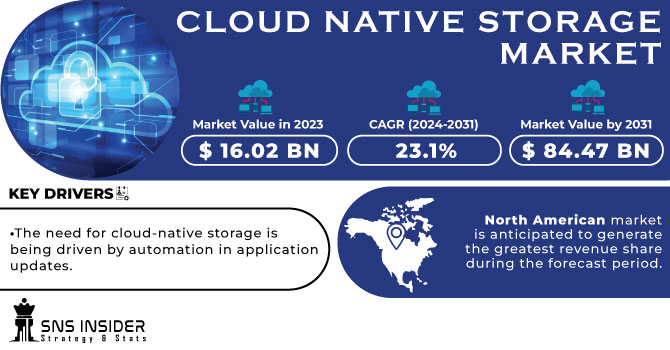

The Cloud Native Storage Market size was valued at US$ 16.02 Billion in 2023 and is projected to reach US$ 84.47 Billion in 2031 with a growing CAGR of 23.1% Over the Forecast Period of 2024-2031.

Cloud Native Storage is a method tailored to address the unique storage requirements of cloud-native applications. These applications, which embrace the principles of microservices, containerization, dynamic scaling, and continuous delivery, are purposefully designed to excel in cloud environments. Unlike conventional monolithic applications, cloud-native applications are frequently deployed across distributed systems and heavily rely on cloud-based infrastructure, resulting in distinct storage needs. Cloud Native Storage should effortlessly interface with container orchestration technologies like Kubernetes, among other key qualities and factors. It should be able to enable stateful apps operating inside containers and dynamically provision container storage volumes. Because cloud-native applications are dynamic in nature, cloud-native storage solutions must be extremely scalable. They ought to be able to manage the quick scaling up or down of resources as needed by the application workload.

To Get More Information on Cloud Native Storage Market - Request Sample Report

Drivers

The need for cloud-native storage is being driven by automation in application updates.

The Demand for Cloud Native Storage Is Growing Due to Faster Data Backup and Recovery

Businesses can build automated environments for continuous testing and deployment using cloud-native architecture. Every six months or so, banks would conduct system changes that were very carefully planned out, and they would tell consumers in advance of any anticipated downtime by publishing on banking websites. The majority of banking and financial apps, on the other hand, would probably update every week or even every day if they had native cloud storage, without having to halt operation or alert users. The same technology that automates application provisioning and deployment serves as the basis for both the seamless upgrade process and thorough testing. One of the most important benefits of using containers and cloud-native storage is what programmers refer to as continuous deployment.

Restrains

Network usage and latency issues in public cloud infrastructures have become a significant concern in recent times.

Opportunities

Faster data backup and recovery resulting in a demand for native cloud storage

Increasing demand for cloud-native storage from various industries.

Adaptability and automation of cloud-native storage Boost availability, adaptability, and dependability. Automation in cloud native storage has the benefit of allowing lost data to be swiftly recovered in the event of an issue without having to stop the service. Cloud-native storage, which offers capabilities like cross-cluster disaster recovery, automated updating, and volume encryption, facilitates data management with block storage. This is essential across all verticals. Additionally, these technologies simplify the monitoring environments and facilitate operational audits. Cloud-native storage solutions enable scalability and rapid execution of data tasks. Make it feasible to configure storage boots and stateful application backups. Utilizing cloud-native storage solutions allows organizations to automate the lifetime management of data layer components. It is a full system that gives firms stability and adaptability in addition to making them enterprise ready. In addition, it offers active directory linkages and compliance tools, which should boost demand throughout the course of the forecasted time.

Challenges

The complexity of cloud-native notions

In the event of escalated tensions, governments and organizations might become more concerned about data sovereignty and security. This could lead to increased demands for data to be stored within a specific region or country, impacting the cloud-native storage strategies of multinational companies. Geopolitical instability can cause businesses to reevaluate their investments and expansion plans. Companies might delay or modify their cloud adoption strategies until there is more clarity about the situation. This could affect the growth rate of the cloud-native storage market. Heightened tensions between nations often result in an increase in cyber-attacks and hacking attempts. Companies might invest more in cybersecurity measures, including storage solutions with enhanced security features, to protect their data from potential threats. If the conflict leads to economic challenges, governments and businesses might have to allocate resources differently. This could impact IT budgets and the willingness to invest in cloud-native storage solutions, potentially affecting the growth of the market. If the Russia-Ukraine conflict triggers broader economic instability, it could impact the overall IT spending of organizations. Cloud-native storage solutions might be considered discretionary spending and could face cutbacks in times of economic uncertainty. Organizations might reconsider their cloud strategies, including the choice between public, private, or hybrid cloud solutions. The war could influence decisions about which type of cloud and storage solution is perceived to be more resilient and secure in such a geopolitical environment.

Impact of Recession

During a recession, businesses often tighten their budgets and cut back on discretionary spending, which includes investments in new technologies and IT infrastructure. This could result in a slowdown in the adoption of cloud-native storage solutions, as organizations might delay or cancel projects that involve implementing new storage technologies. Companies might shift their focus from growth-oriented projects to cost-saving initiatives. This could lead to a decreased emphasis on adopting cutting-edge cloud native storage solutions, especially if existing storage systems are deemed sufficient to meet immediate needs. In a recession, organizations may postpone hardware and software upgrades, expansions, or migrations to cloud-native storage platforms. This could lead to a decrease in demand for new storage solutions and services, affecting the growth prospects of vendors in the cloud-native storage market. If cloud native storage providers are able to position their offerings as cost-effective solutions that help businesses optimize spending and achieve operational efficiencies, they might still find opportunities to grow their market share during a recession. The impact of a recession on the Cloud Native Storage market might extend beyond the immediate economic downturn. Businesses that delay technology investments during a recession might take time to catch up, leading to a slower recovery for the cloud-native storage market even after the economy stabilizes.

By Component

Solutions

Services

By Deployment

By Organization Size

Large Enterprises

SMEs

By Verticals

Banking, Financial Services, & Insurance

Government

Healthcare & Life Sciences

Telecommunication

IT & ITeS

Manufacturing

Energy & Utilities

Media & Entertainment

Retail & Consumer Goods

Other Verticals

Due to increased operations by major market players in the region's nations, the North American market is anticipated to generate the greatest revenue share during the forecast period. Change Healthcare continues to set the standard with its Picture Archiving and Communication Systems (PACS) and accompanying technologies for both radiology and Cardiology is being replaced by cloud-native, footprint-free medical imaging technologies as the healthcare industry moves away from on-premise imaging systems. More than 6 petabytes, or more than 9.8%, of the imaging data from Change Healthcare's existing hospital clients, have already been uploaded to the cloud. While Stratus Imaging Analytics is currently live in 74 companies, Stratus Imaging Archive is live in 43 hospitals.

Due to growing government initiatives in the region's nations, the market revenue in Asia Pacific is anticipated to see the fastest CAGR over the course of the forecast year. For instance, statistics reveal that China continues to spend more on cloud infrastructure than the rest of the globe. In total, the mainland spent USD 7.26 billion on infrastructure in the first quarter of 2022, and it is anticipated that this sum would increase over the rest of the year. Alibaba Cloud, Huawei Cloud, Tencent Cloud, and Baidu AI Cloud continue to be the top four cloud service providers in the country. As a result, the region's expanding government activities are raising the demand for cloud-native storage, which is anticipated to propel market revenue growth.

Do You Need any Customization Research on Cloud Native Storage Market - Enquire Now

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

The prominent players in the market are AWS, Google, IBM, Alibaba Cloud, VMWare, Huawei, Microsoft, Citrix, Tencent Cloud, Scality, Diamanti, Splunk, Arrikto, Rackspace, Robin.Io, MayaData, Minio, Rook, Trilio, Ondat, Ionir, Upcloud, Linbit, and others in the final report.

To power its cloud-native data centers, Alibaba Cloud revealed a new cloud infrastructure architecture in June 2022.

IBM introduced IBM FlashSystem Cyber Vault in February 2022 to assist businesses in identifying and swiftly recovering from ransomware and other intrusions. In order to create a uniform operating environment and boost application performance in a hybrid cloud environment, the business also unveiled new FlashSystem storage models based on IBM Spectrum Virtualize.

Astra Data Store, a Kubernetes-native, shared file, a unified data store for containers and VMs with comprehensive enterprise data management, was released by NetApp in October 2021.

| Report Attributes | Details |

| Market Size in 2023 | US$ 16.02 Bn |

| Market Size by 2031 | US$ 84.47 Bn |

| CAGR | CAGR of 23.1% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Public Cloud, Private Cloud) • By Organization Size (Large Enterprises, SMEs) • By Verticals (Banking, Financial Services, & Insurance, Government, Healthcare & Life Sciences, Telecommunication, IT & ITeS, Manufacturing, Energy & Utilities, Media & Entertainment, Retail & Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | AWS, Google, IBM, Alibaba Cloud, VMWare, Huawei, Microsoft, Citrix, Tencent Cloud, Scality, Diamanti, Splunk, Arrikto, Rackspace, Robin.Io, MayaData, Minio, Rook, Trilio, Ondat, Ionir, Upcloud, Linbit |

| Key Drivers | • The need for cloud-native storage is being driven by automation in application updates. • The Demand for Cloud Native Storage Is Growing Due to Faster Data Backup and Recovery |

| Market Restraints | • Network usage and latency issues in public cloud infrastructures have become a significant concern in recent times. |

Ans. The CAGR of the Cloud Native Storage Market is 22.72 %.

Ans: The value of the Cloud Native Storage Market is 13.8 billion in 2022.

Ans: four segments are covered in the Cloud Native Storage Market Report, By Component, By Deployment, By Organization Size, By Verticals.

Ans. The forecast period of the Cloud Native Storage Market is 2022-2030.

ANS: Yes, you can ask for the customization as pas per your business requirement.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of Russia-Ukraine War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Cloud Native Storage Market Segmentation, By Components

8.1 Solutions

8.2 Services

9. Cloud Native Storage Market Segmentation, By Deployment

9.1 Public Cloud

9.2 Private Cloud

10. Cloud Native Storage Market Segmentation, By Organizational Size

10.1 Large Enterprises

10.2 SMEs

11. Cloud Native Storage Market Segmentation, By Verticals

11.1 Banking, Financial Services, & Insurance

11.2 Government

11.3 Healthcare & Life Sciences

11.4 Telecommunication

11.5 IT & ITeS

11.6 Manufacturing

11.7 Energy & Utilities

11.8 Media & Entertainment

11.9 Retail & Consumer Goods

11.10 Others

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 North America Cloud Native Storage Market By Country

12.2.2 North America Cloud Native Storage Market By Components

12.2.3 North America Cloud Native Storage Market By Deployment

12.2.4 North America Cloud Native Storage Market By Organizational Size

12.2.5 North America Cloud Native Storage Market By Verticals

12.2.6 USA

12.2.6.1 USA Cloud Native Storage Market By Components

12.2.6.2 USA Cloud Native Storage Market By Deployment

12.2.6.3 USA Cloud Native Storage Market By Organizational Size

12.2.6.4 USA Cloud Native Storage Market By Verticals

12.2.7 Canada

12.2.7.1 Canada Cloud Native Storage Market By Components

12.2.7.2 Canada Cloud Native Storage Market By Deployment

12.2.7.3 Canada Cloud Native Storage Market By Organizational Size

12.2.7.4 Canada Cloud Native Storage Market By Verticals

12.2.8 Mexico

12.2.8.1 Mexico Cloud Native Storage Market By Components

12.2.8.2 Mexico Cloud Native Storage Market By Deployment

12.2.8.3 Mexico Cloud Native Storage Market By Organizational Size

12.2.8.4 Mexico Cloud Native Storage Market By Verticals

12.3 Europe

12.3.1 Eastern Europe

12.3.1.1 Eastern Europe Cloud Native Storage Market By Country

12.3.1.2 Eastern Europe Cloud Native Storage Market By Components

12.3.1.3 Eastern Europe Cloud Native Storage Market By Deployment

12.3.1.4 Eastern Europe Cloud Native Storage Market By Organizational Size

12.3.1.5 Eastern Europe Cloud Native Storage Market By Verticals

12.3.1.6 Poland

12.3.1.6.1 Poland Cloud Native Storage Market By Components

12.3.1.6.2 Poland Cloud Native Storage Market By Deployment

12.3.1.6.3 Poland Cloud Native Storage Market By Organizational Size

12.3.1.6.4 Poland Cloud Native Storage Market By Verticals

12.3.1.7 Romania

12.3.1.7.1 Romania Cloud Native Storage Market By Components

12.3.1.7.2 Romania Cloud Native Storage Market By Deployment

12.3.1.7.3 Romania Cloud Native Storage Market By Organizational Size

12.3.1.7.4 Romania Cloud Native Storage Market By Verticals

12.3.1.8 Hungary

12.3.1.8.1 Hungary Cloud Native Storage Market By Components

12.3.1.8.2 Hungary Cloud Native Storage Market By Deployment

12.3.1.8.3 Hungary Cloud Native Storage Market By Organizational Size

12.3.1.8.4 Hungary Cloud Native Storage Market By Verticals

12.3.1.9 Turkey

12.3.1.9.1 Turkey Cloud Native Storage Market By Components

12.3.1.9.2 Turkey Cloud Native Storage Market By Deployment

12.3.1.9.3 Turkey Cloud Native Storage Market By Organizational Size

12.3.1.9.4 Turkey Cloud Native Storage Market By Verticals

12.3.1.10 Rest of Eastern Europe

12.3.1.10.1 Rest of Eastern Europe Cloud Native Storage Market By Components

12.3.1.10.2 Rest of Eastern Europe Cloud Native Storage Market By Deployment

12.3.1.10.3 Rest of Eastern Europe Cloud Native Storage Market By Organizational Size

12.3.1.10.4 Rest of Eastern Europe Cloud Native Storage Market By Verticals

12.3.2 Western Europe

12.3.2.1 Western Europe Cloud Native Storage Market By Country

12.3.2.2 Western Europe Cloud Native Storage Market By Components

12.3.2.3 Western Europe Cloud Native Storage Market By Deployment

12.3.2.4 Western Europe Cloud Native Storage Market By Organizational Size

12.3.2.5 Western Europe Cloud Native Storage Market By Verticals

12.3.2.6 Germany

12.3.2.6.1 Germany Cloud Native Storage Market By Components

12.3.2.6.2 Germany Cloud Native Storage Market By Deployment

12.3.2.6.3 Germany Cloud Native Storage Market By Organizational Size

12.3.2.6.4 Germany Cloud Native Storage Market By Verticals

12.3.2.7 France

12.3.2.7.1 France Cloud Native Storage Market By Components

12.3.2.7.2 France Cloud Native Storage Market By Deployment

12.3.2.7.3 France Cloud Native Storage Market By Organizational Size

12.3.2.7.4 France Cloud Native Storage Market By Verticals

12.3.2.8 UK

12.3.2.8.1 UK Cloud Native Storage Market By Components

12.3.2.8.2 UK Cloud Native Storage Market By Deployment

12.3.2.8.3 UK Cloud Native Storage Market By Organizational Size

12.3.2.8.4 UK Cloud Native Storage Market By Verticals

12.3.2.9 Italy

12.3.2.9.1 Italy Cloud Native Storage Market By Components

12.3.2.9.2 Italy Cloud Native Storage Market By Deployment

12.3.2.9.3 Italy Cloud Native Storage Market By Organizational Size

12.3.2.9.4 Italy Cloud Native Storage Market By Verticals

12.3.2.10 Spain

12.3.2.10.1 Spain Cloud Native Storage Market By Components

12.3.2.10.2 Spain Cloud Native Storage Market By Deployment

12.3.2.10.3 Spain Cloud Native Storage Market By Organizational Size

12.3.2.10.4 Spain Cloud Native Storage Market By Verticals

12.3.2.11 Netherlands

12.3.2.11.1 Netherlands Cloud Native Storage Market By Components

12.3.2.11.2 Netherlands Cloud Native Storage Market By Deployment

12.3.2.11.3 Netherlands Cloud Native Storage Market By Organizational Size

12.3.2.11.4 Netherlands Cloud Native Storage Market By Verticals

12.3.2.12 Switzerland

12.3.2.12.1 Switzerland Cloud Native Storage Market By Components

12.3.2.12.2 Switzerland Cloud Native Storage Market By Deployment

12.3.2.12.3 Switzerland Cloud Native Storage Market By Organizational Size

12.3.2.12.4 Switzerland Cloud Native Storage Market By Verticals

12.3.2.13 Austria

12.3.2.13.1 Austria Cloud Native Storage Market By Components

12.3.2.13.2 Austria Cloud Native Storage Market By Deployment

12.3.2.13.3 Austria Cloud Native Storage Market By Organizational Size

12.3.2.13.4 Austria Cloud Native Storage Market By Verticals

12.3.2.14 Rest of Western Europe

12.3.2.14.1 Rest of Western Europe Cloud Native Storage Market By Components

12.3.2.14.2 Rest of Western Europe Cloud Native Storage Market By Deployment

12.3.2.14.3 Rest of Western Europe Cloud Native Storage Market By Organizational Size

12.3.2.14.4 Rest of Western Europe Cloud Native Storage Market By Verticals

12.4 Asia-Pacific

12.4.1 Asia Pacific Cloud Native Storage Market By Country

12.4.2 Asia Pacific Cloud Native Storage Market By Components

12.4.3 Asia Pacific Cloud Native Storage Market By Deployment

12.4.4 Asia Pacific Cloud Native Storage Market By Organizational Size

12.4.5 Asia Pacific Cloud Native Storage Market By Verticals

12.4.6 China

12.4.6.1 China Cloud Native Storage Market By Components

12.4.6.2 China Cloud Native Storage Market By Deployment

12.4.6.3 China Cloud Native Storage Market By Organizational Size

12.4.6.4 China Cloud Native Storage Market By Verticals

12.4.7 India

12.4.7.1 India Cloud Native Storage Market By Components

12.4.7.2 India Cloud Native Storage Market By Deployment

12.4.7.3 India Cloud Native Storage Market By Organizational Size

12.4.7.4 India Cloud Native Storage Market By Verticals

12.4.8 Japan

12.4.8.1 Japan Cloud Native Storage Market By Components

12.4.8.2 Japan Cloud Native Storage Market By Deployment

12.4.8.3 Japan Cloud Native Storage Market By Organizational Size

12.4.8.4 Japan Cloud Native Storage Market By Verticals

12.4.9 South Korea

12.4.9.1 South Korea Cloud Native Storage Market By Components

12.4.9.2 South Korea Cloud Native Storage Market By Deployment

12.4.9.3 South Korea Cloud Native Storage Market By Organizational Size

12.4.9.4 South Korea Cloud Native Storage Market By Verticals

12.4.10 Vietnam

12.4.10.1 Vietnam Cloud Native Storage Market By Components

12.4.10.2 Vietnam Cloud Native Storage Market By Deployment

12.4.10.3 Vietnam Cloud Native Storage Market By Organizational Size

12.4.10.4 Vietnam Cloud Native Storage Market By Verticals

12.4.11 Singapore

12.4.11.1 Singapore Cloud Native Storage Market By Components

12.4.11.2 Singapore Cloud Native Storage Market By Deployment

12.4.11.3 Singapore Cloud Native Storage Market By Organizational Size

12.4.11.4 Singapore Cloud Native Storage Market By Verticals

12.4.12 Australia

12.4.12.1 Australia Cloud Native Storage Market By Components

12.4.12.2 Australia Cloud Native Storage Market By Deployment

12.4.12.3 Australia Cloud Native Storage Market By Organizational Size

12.4.12.4 Australia Cloud Native Storage Market By Verticals

12.4.13 Rest of Asia-Pacific

12.4.13.1 Rest of Asia-Pacific Cloud Native Storage Market By Components

12.4.13.2 Rest of Asia-Pacific Cloud Native Storage Market By Deployment

12.4.13.3 Rest of Asia-Pacific Cloud Native Storage Market By Organizational Size

12.4.13.4 Rest of Asia-Pacific Cloud Native Storage Market By Verticals

12.5 Middle East & Africa

12.5.1 Middle East

12.5.1.1 Middle East Cloud Native Storage Market By Country

12.5.1.2 Middle East Cloud Native Storage Market By Components

12.5.1.3 Middle East Cloud Native Storage Market By Deployment

12.5.1.4 Middle East Cloud Native Storage Market By Organizational Size

12.5.1.5 Middle East Cloud Native Storage Market By Verticals

12.5.1.6 UAE

12.5.1.6.1 UAE Cloud Native Storage Market By Components

12.5.1.6.2 UAE Cloud Native Storage Market By Deployment

12.5.1.6.3 UAE Cloud Native Storage Market By Organizational Size

12.5.1.6.4 UAE Cloud Native Storage Market By Verticals

12.5.1.7 Egypt

12.5.1.7.1 Egypt Cloud Native Storage Market By Components

12.5.1.7.2 Egypt Cloud Native Storage Market By Deployment

12.5.1.7.3 Egypt Cloud Native Storage Market By Organizational Size

12.5.1.7.4 Egypt Cloud Native Storage Market By Verticals

12.5.1.8 Saudi Arabia

12.5.1.8.1 Saudi Arabia Cloud Native Storage Market By Components

12.5.1.8.2 Saudi Arabia Cloud Native Storage Market By Deployment

12.5.1.8.3 Saudi Arabia Cloud Native Storage Market By Organizational Size

12.5.1.8.4 Saudi Arabia Cloud Native Storage Market By Verticals

12.5.1.9 Qatar

12.5.1.9.1 Qatar Cloud Native Storage Market By Components

12.5.1.9.2 Qatar Cloud Native Storage Market By Deployment

12.5.1.9.3 Qatar Cloud Native Storage Market By Organizational Size

12.5.1.9.4 Qatar Cloud Native Storage Market By Verticals

12.5.1.10 Rest of Middle East

12.5.1.10.1 Rest of Middle East Cloud Native Storage Market By Components

12.5.1.10.2 Rest of Middle East Cloud Native Storage Market By Deployment

12.5.1.10.3 Rest of Middle East Cloud Native Storage Market By Organizational Size

12.5.1.10.4 Rest of Middle East Cloud Native Storage Market By Verticals

12.5.2. Africa

12.5.2.1 Africa Cloud Native Storage Market By Country

12.5.2.2 Africa Cloud Native Storage Market By Components

12.5.2.3 Africa Cloud Native Storage Market By Deployment

12.5.2.4 Africa Cloud Native Storage Market By Organizational Size

12.5.2.5 Africa Cloud Native Storage Market By Verticals

12.5.2.6 Nigeria

12.5.2.6.1 Nigeria Cloud Native Storage Market By Components

12.5.2.6.2 Nigeria Cloud Native Storage Market By Deployment

12.5.2.6.3 Nigeria Cloud Native Storage Market By Organizational Size

12.5.2.6.4 Nigeria Cloud Native Storage Market By Verticals

12.5.2.7 South Africa

12.5.2.7.1 South Africa Cloud Native Storage Market By Components

12.5.2.7.2 South Africa Cloud Native Storage Market By Deployment

12.5.2.7.3 South Africa Cloud Native Storage Market By Organizational Size

12.5.2.7.4 South Africa Cloud Native Storage Market By Verticals

12.5.2.8 Rest of Africa

12.5.2.8.1 Rest of Africa Cloud Native Storage Market By Components

12.5.2.8.2 Rest of Africa Cloud Native Storage Market By Deployment

12.5.2.8.3 Rest of Africa Cloud Native Storage Market By Organizational Size

12.5.2.8.4 Rest of Africa Cloud Native Storage Market By Verticals

12.6. Latin America

12.6.1 Latin America Cloud Native Storage Market By Country

12.6.2 Latin America Cloud Native Storage Market By Components

12.6.3 Latin America Cloud Native Storage Market By Deployment

12.6.4 Latin America Cloud Native Storage Market By Organizational Size

12.6.5 Latin America Cloud Native Storage Market By Verticals

12.6.6 Brazil

12.6.6.1 Brazil Cloud Native Storage Market By Components

12.6.6.2 Brazil Cloud Native Storage Market By Deployment

12.6.6.3 Brazil Cloud Native Storage Market By Organizational Size

12.6.6.4 Brazil Cloud Native Storage Market By Verticals

12.6.7 Argentina

12.6.7.1 Argentina Cloud Native Storage Market By Components

12.6.7.2 Argentina Cloud Native Storage Market By Deployment

12.6.7.3 Argentina Cloud Native Storage Market By Organizational Size

12.6.7.4 Argentina Cloud Native Storage Market By Verticals

12.6.8 Colombia

12.6.8.1 Colombia Cloud Native Storage Market By Components

12.6.8.2 Colombia Cloud Native Storage Market By Deployment

12.6.8.3 Colombia Cloud Native Storage Market By Organizational Size

12.6.8.4 Colombia Cloud Native Storage Market By Verticals

12.6.9 Rest of Latin America

12.6.9.1 Rest of Latin America Cloud Native Storage Market By Components

12.6.9.2 Rest of Latin America Cloud Native Storage Market By Deployment

12.6.9.3 Rest of Latin America Cloud Native Storage Market By Organizational Size

12.6.9.4 Rest of Latin America Cloud Native Storage Market By Verticals

13 Company Profile

13.1 AWS

13.1.1 Company Overview

13.1.2 Financials

13.1.3 Product/Services/Offerings

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 Google.

13.2.1 Company Overview

13.2.2 Financials

13.2.3 Product/Services/Offerings

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 IBM.

13.3.1 Company Overview

13.3.2 Financials

13.3.3 Product/Services/Offerings

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 Alibaba Cloud.

13.4.1 Company Overview

13.4.2 Financials

13.4.3 Product/Services/Offerings

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 VMWare.

13.5.1 Company Overview

13.5.2 Financials

13.5.3 Product/Services/Offerings

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 Huawei.

13.6.1 Company Overview

13.6.2 Financials

13.6.3 Product/Services/Offerings

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 Microsoft.

13.7.1 Company Overview

13.7.2 Financials

13.7.3 Product/Services/Offerings

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8 Citrix.

13.8.1 Company Overview

13.8.2 Financials

13.8.3 Product/Services/Offerings

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 Fidelis Cybersecurity.

13.9.1 Company Overview

13.9.2 Financials

13.9.3 Product/Services/Offerings

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 Tencent Cloud.

13.10.1 Company Overview

13.10.2 Financials

13.10.3 Product/Services/Offerings

13.10.4 SWOT Analysis

13.10.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3 Mergers & Acquisitions

15. USE Cases and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Super App Market size was recorded at USD 75.5 Bn in 2023 and is expected to reach USD 706.2 Bn by 2032, growing at a CAGR of 28.2 % over the forecast period 2024-2032.

The Digital Workplace Market size was valued at USD 30.3 Billion in 2023 and is expected to grow to USD 170.93 Billion By 2031 and grow at a CAGR of 22.5 % over the forecast period of 2024-2031.

The Online Payroll Services Market size was valued at USD 3.45 billion in 2023, with a predicted CAGR of 14.8% to reach USD 11.9 billion by 2032

The Blockchain Market Size was valued at USD 12.04 Billion in 2023 and is expected to reach USD 739.25 Billion by 2031 and grow at a CAGR of 67.3 % over the forecast period 2024-2031.

The Asset Performance Management Market size was valued at USD 2.94 Billion in 2023 and is estimated to reach USD 6.16 Billion in 2031 with a growing CAGR of 9.7% Over the Forecast Period of 2024-2031.

The Accounts Receivable Automation Market size was valued at USD 3.41 billion in 2022 and is projected to reach USD 9.59 billion in 2030 with a growing CAGR of 13.8% Over the Forecast Period of 2023-2030.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd