Computerized Physician Order Entry Market Report Scope & Overview:

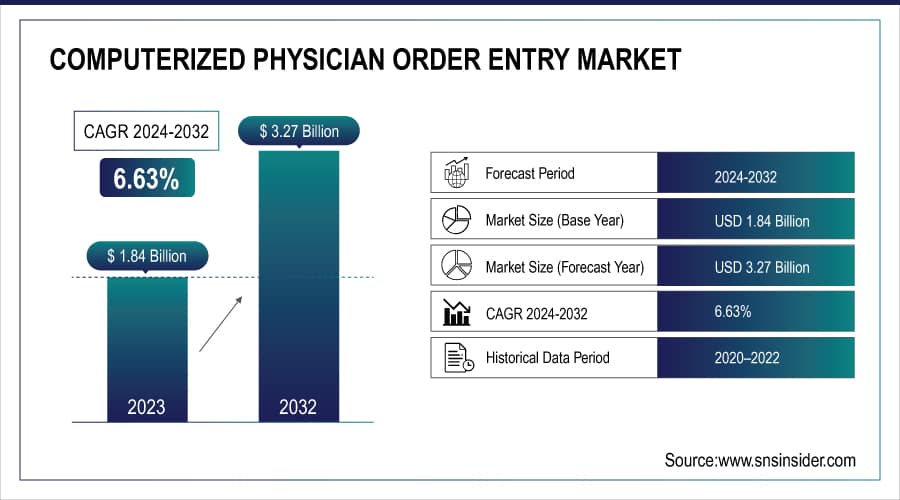

The Computerized Physician Order Entry Market size was valued at USD 1.84 billion in 2023 and is expected to grow to USD 3.27 billion by 2032 and grow at a CAGR of 6.63% over the forecast period of 2024-2032.

The computerized physician order entry market is showing promising growth with an increasing need for solutions to minimize medication errors. Along with this primary reason, computerized physician order entry solutions are being used to improve the efficiency of healthcare service procedures, reducing the time and costs incurred. High adoption in the advanced regions and increasing awareness in the developing countries to optimize the healthcare experience are the factors expected to keep the market growth pace in higher single digits during the forecast period.

CPOE applications are not limited to just reducing errors. These solutions increase the efficiency by reducing the wait time and save costs wastage during the process. In addition, the captured data can be processed by integration with advanced analytics and the recent advancement in AI-ML technologies. The rapid and accurate decision-making using the latest technologies is expected to pivot the healthcare service quality at the global level.

According to a study discussed in The 6th International Conference on Public Health, effective use of CPOE can potentially save around USD 65 per admission. The average number of hospital admissions in the USA per year is around 5,860/hospital. This translates to a saving of USD 380,900 per hospital per year. The figures can go significantly higher when we consider other healthcare facilities.

The application of CPOE is not limited to hospital settings. With the rapid adoption of telemedicine, CPOE solutions have found new growth avenues in ambulatory care, home settings, specialty care, and even clinical research. In specialty care, these rapidly evolving CPOE tools are being used extensively to handle complex drug regimens for diseases including cancer and other degenerative conditions.

Computerized Physician Order Entry Market Size and Forecast:

-

Market Size in 2023: USD 1.84 billion

-

Market Size by 2032: USD 3.27 billion

-

CAGR: 6.63% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

To Get More Information On Computerized Physician Order Entry Market - Request Free Sample Report

Computerized Physician Order Entry Market Trends

-

Rising adoption of healthcare IT solutions and electronic health records (EHRs is driving demand for CPOE systems to improve clinical workflow efficiency and reduce medication errors across hospitals and ambulatory care settings.

-

Growing emphasis on patient safety and regulatory compliance is accelerating the implementation of CPOE platforms, as these systems help minimize adverse drug events through standardized, legible, and automated physician orders.

-

Advancements in clinical decision support systems (CDSS integration within CPOE solutions are enhancing real-time alerts, drug–drug interaction checks, allergy warnings, and dosage guidance to support accurate clinical decision-making.

-

Increasing deployment of cloud-based and web-based CPOE solutions is improving system scalability, interoperability, and accessibility, particularly for small- and mid-sized healthcare facilities.

-

Government initiatives, healthcare digitization programs, and incentive-based reimbursement policies are encouraging widespread adoption of CPOE systems in both developed and emerging healthcare markets.

-

Integration of CPOE with hospital information systems (HIS, pharmacy management systems, and laboratory information systems is streamlining care coordination and improving overall operational efficiency.

-

Emerging trends toward AI-enabled analytics, predictive ordering, and mobile-based physician interfaces are enhancing user experience, reducing administrative burden, and supporting value-based care models within the CPOE ecosystem.

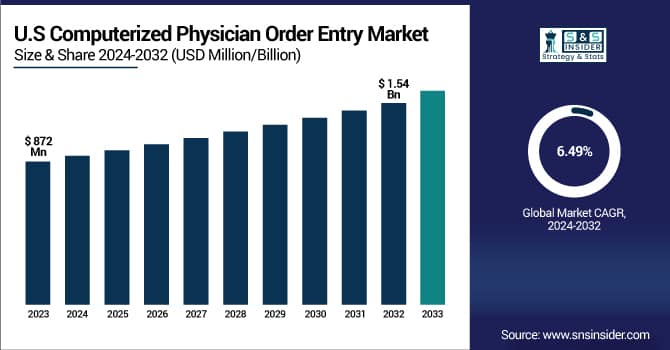

The U.S. Computerized Physician Order Entry Market was valued at approximately USD 872 million in 2023 and is expected to reach around USD 1.54 billion by 2032, exhibiting a CAGR of 6.49% from 2024 to 2032. Growth is driven by increased implementation of electronic health records (EHRs), regulatory mandates for digital healthcare infrastructure, and the need to automate clinical workflows to improve patient safety and reduce medication errors.

Computerized Physician Order Entry Market Drivers

-

Enhancing Patient Safety: Reducing Medication Errors Through Computerized Physician Order Entry (CPOE)

According to a report published by the World Health Organization, globally, medication errors alone cause a loss of more than USD 42 Billion each year. In the USA, more than 100,000 medication errors are reported per year. The majority of these are prescription errors. Other common medication errors occur while reading the prescription, wrong dosages, failure to consider the patient's medical history, administration, and lack of patient awareness. Almost all of these errors can be mitigated by the smart use of a computerized physician order entry market.

-

Driving CPOE Market Growth: The Role of AI, Cloud Solutions, and Data Security Compliance

The rapid technological advancements and integration with data analytics and AI tools are expected to be major decision-makers in future market growth. Along with the data collection, storage, and processing abilities of these tools, features such as cloud-based solutions and telemedicine are helping mitigate the risks associated with data security. Healthcare service-providing facilities can easily keep their operations aligned with the data security policies including HIPAA, HITECH, and GDPR.

In addition, The algorithms, which keep adapting per case, help with personalized cases. The system can now suggest the dose regimen based on the patient history, estimate the prognosis, and detect or predict potential adverse drug reactions continuously during the course.

Computerized Physician Order Entry Market Restraints

-

Addressing Resistance to Change in CPOE Implementation Among Healthcare Providers

The implementation of Computerized Physician Order Entry (CPOE) systems frequently encounters pushback since healthcare providers might favor conventional, familiar approaches. Moving to CPOE requires significant training and adjustment, which may initially disturb existing workflows. Furthermore, healthcare practitioners might worry about the dependability of technology and the precision of data, leading to reluctance. Nevertheless, tackling these obstacles with intuitive designs, thorough training, and highlighting the advantages of minimizing errors and enhancing patient care can facilitate the adoption process and propel CPOE system integration ahead.

Computerized Physician Order Entry Market Segment Analysis

By Type

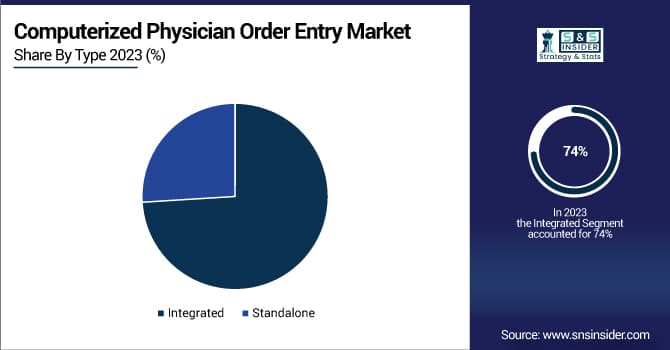

The integrated segment captured the largest market share in 2023, with a share of around 74%. The integrated systems can extend their services on multiple platforms such as procurement, nursery, and pharmacy. This ensures a smooth workflow between each node of the service chain. This is the reason hospitals prefer integrated CPOE systems to facilitate all operations within the setting. The integrated systems are usually a part of broader electronic health records systems (EHR), which is a mandate to maintain in developed regions.

Standalone systems are expected to witness a high adoption rate and show the fastest growth rate with a CAGR of 8.47% during the forecast period. The standalone systems are preferred by smaller healthcare facilities owing to their affordability. These systems also require minimum IT infrastructure as compared to its counterpart. These key factors are expected to drive the segment growth, especially in the high-growth, yet price-sensitive regions including Asia Pacific and Latin America.

By Component

In 2023, the services sector led the Computerized Physician Order Entry (CPOE) market, holding a revenue share of approximately 53%. This is primarily because of the ongoing requirement for system implementation, support, and maintenance. As healthcare systems grow more intricate, the need for specialized services to enhance CPOE efficiency and integrate into current workflows rises.

The hardware sector, projected to expand at a CAGR of 8.48% from 2024 to 2032, is fueled by innovations in medical equipment and computing infrastructure. Advanced hardware is crucial for accommodating the growing complexity of CPOE systems, guaranteeing top-notch data security and efficiency. The increasing acceptance of digital health solutions and the necessity for strong infrastructure position this segment for swift expansion.

By Delivery Mode

In 2023, online solutions dominated the Computerized Physician Order Entry (CPOE) market, capturing the highest revenue share of around 46%. This supremacy arises from the adaptability and availability of online systems, enabling healthcare professionals to access essential information from any place. Moreover, they are simpler to incorporate into current healthcare systems, which makes them greatly favored by large hospitals and multi-site healthcare networks.

Cloud-based CPOE systems are projected to achieve the highest CAGR of 7.89% between 2024 and 2032. This expansion is motivated by the rising need for scalable and affordable solutions that cloud technology provides. Cloud-based solutions offer immediate data sharing, lower operational expenses, and facilitate simple updates and maintenance, making them appealing to healthcare institutions aiming for improved collaboration and operational effectiveness.

By End-use

In 2023, the largest share of the revenue was held by hospitals, at 46%. Hospitals are the best-funded and resourceful and can implement the CPOE systems fully into their operations for better patient care. The systems help in making patient orders easier, reducing errors, and maintaining regulatory standards, and hence they continue to hold a large share of the market.

Ambulatory centers are likely to witness the highest CAGR of 8.51% between 2024 and 2032 as outpatient services gain in popularity. These facilities reap several advantages from implementing CPOE systems, which contribute to efficiency and safety in patients of fast-paced, non-hospital settings. Rising outpatient needs lead more ambulatory centers to invest in advanced CPOE systems to improve the delivery of service and patient outcomes.

Regional Analysis

North America held a market share of more than 55% in the global CPOE market, in 2023. The dominance of North America is attributed to the availability of advanced healthcare infrastructure paired with the high adoption of healthcare IT solutions. The IT solutions are supported through regulations such as the Health Information Technology for Economic and Clinical Health (HITECH) Act. Over 95% of hospitals in the U.S. have implemented CPOE systems which are now pivotal to their operations, underlying a robust commitment to improved patient safety and medication error reduction.

Get Customized Report as Per Your Business Requirement - Enquiry Now

On the other hand, Asia-Pacific is expected to show the fastest growth with approximately a CAGR rate of 9.08%. The strong growth is supported by massive government efforts in China and India to digitalize healthcare as a national priority. For example, China has been heavily investing money in its healthcare IT which is projected to hit more than $20 billion in the next two years, significantly focused on improving hospital information systems and CPOE as well. The government in India is promoting all sectors of the Indian economy to be digital through the Digital India program which stimulates the adoption of advanced technologies such as CPOE systems, especially in healthcare. Increasing healthcare infrastructure investments by Asia-Pacific nations and an equal emphasis on healthcare digitalization, are the factors driving the growth in this region. High potential in the Asia Pacific region is not only attracting global players, but it is opening up opportunities for local new entrants as well.

KEY PLAYERS

-

IBM (IBM Watson Health, IBM Clinical Development)

-

Cerner Corporation (Cerner Millennium, PowerChart)

-

SAS Institute Inc. (SAS Health Analytics, SAS Advanced Analytics)

-

Veradigm LLC (Veradigm EHR, Veradigm CPOE)

-

Optum, Inc. (Optum Health Platform, Optum Cloud-Based EHR)

-

Verisk Analytics, Inc. (Verisk Health Analytics, Verisk Data Solutions)

-

Athenahealth, Inc. (AthenaOne, AthenaClinicals)

-

Carestream Health (Carestream Radiology Information System, Carestream PACS)

-

Philips Healthcare (Philips IntelliSpace, Philips Epic)

-

Allscripts Healthcare, LLC (Allscripts Sunrise, Allscripts TouchWorks)

-

Siemens Healthineers GmbH (Siemens Soarian, Siemens Syngo)

-

Koninklijke Philips N.V. (Philips HealthSuite, Philips IntelliSpace)

-

Medical Information Technology, Inc. (MEDITECH) (MEDITECH Expanse, MEDITECH Web EHR)

-

eClinicalWorks (eClinicalWorks EHR, eClinicalWorks Care Coordination)

-

Epic Systems Corporation (EpicCare, Epic Beacon)

-

General Electric (GE) (GE Centricity, GE Healthcare Imaging)

-

McKesson Corporation (McKesson Paragon, McKesson EnterpriseRx)

-

CareCloud Inc. (CareCloud Central, CareCloud EHR)

-

First Databank, Inc. (First Databank Drug Information System, First Databank CPOE)

Recent Developement

-

Oracle's 2024 EHR innovations enhance order management, medication error detection, and closed-loop tracking, benefiting the Computerized Physician Order Entry (CPOE) market. They are also incorporating AI to reduce clinician burnout through automation.

-

Veradigm's October 2024 update integrates advanced natural language processing (NLP) with its EHR dataset, providing deeper clinical insights. This advancement supports clinical trials and regulatory submissions, benefiting the CPOE market.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.84 Billion |

| Market Size by 2032 | USD 3.27 Billion |

| CAGR | CAGR of 6.63% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Integrated, Standalone) • By Component (Software, Hardware, Services) • By Delivery Mode (On-Premises, Web-Based, Cloud-Based) • By End User (Hospital, Ambulatory Centers, Physician’s Office, Emergency Healthcare Services) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM, Oracle, Cerner Corporation, SAS Institute Inc., Veradigm LLC, Optum Inc., Verisk Analytics Inc., Athenahealth Inc., Carestream Health, Philips Healthcare, Allscripts Healthcare LLC, Siemens Healthineers GmbH, Koninklijke Philips N.V., Medical Information Technology Inc., eClinicalWorks, Epic Systems Corporation, General Electric (GE), McKesson Corporation, CareCloud Inc., First Databank Inc. |

Frequently Asked Questions

Ans: Services are essential for implementation, support, and maintenance as healthcare systems grow more complex.

Ans: North America leads with over 55% share, driven by advanced infrastructure and regulatory support.

Ans: With a CAGR of 7.89%, cloud-based solutions offer scalability, cost-efficiency, and seamless data sharing.

Ans: Ambulatory centers are set to grow at an 8.51% CAGR, driven by rising outpatient service needs.

Ans: The Computerized Physician Order Entry Market size was valued at USD 1.84 billion in 2023 and is expected to grow to USD 3.27 billion by 2032 and grow at a CAGR of 6.63% over the forecast period of 2024-2032.

Get in Touch